Crypto

42% Returns and a $10+ Trillion Opportunity: BlackRock, HSBC & Oxbridge Re Are Tokenizing the World

The race to tokenize the world is on as major firms like BlackRock and Oxbridge Re, via its SurancePlus subsidiary, roll out their first rounds of Real World Assets (RWAs) tokenized on the blockchain. This is unlocking new opportunities for savvy investors, including access to markets like reinsurance contracts where early investors are already reaping steep double-digit returns.

While “crypto” in all of its flavors might have faded into the distance for the average investor right now, 2024 has been a huge year for those paying attention.

For starters, the SEC kicked off the year by approving Bitcoin ETFs in January. Then, just a couple of weeks ago, it did the same for Ethereum ETFs.

Already, these two massive federal ticks of approval are big news. But they’re far from the biggest development in crypto this year.

That prize belongs to the coming of age of “tokenization” — the use of a blockchain to buy, hold, and trade assets.

More specifically, 2024 is the year when tokenization has gone majorly institutional, thus washing away its “junky JPEGs on the blockchain” image as major institutions race to bring objectively valuable Real World Assets (RWAs) to the blockchain.

To give some idea of how big this is, BlackRock [NYSE: BLK] is currently rolling out its plans to tokenize $10 trillion in RWAs. The first tokenized fund in this series — the BlackRock USD Institutional Digital Liquidity Fund — dropped in March this year.

That was about the same time HSBC (NYSE: HSBC) opened up access to its tokenized gold to retail investors.

Of course, while HSBC and BlackRock might be the most prominent, they’re far from the first institutional issuer to hit the market.

Beating BlackRock to the tokenized-RWAs punch by a full year, reinsurance upstart Oxbridge Re Holdings Limited (NASDAQ: OXBR) launched its first series of tokenized RWAs via its SurancePlus subsidiary last year. Specifically, it launched a series of tokenized reinsurance contracts to a select group of early investors.

This year, those investors are on track to hit a 42% annualized return.

I’ll repeat that, just to prove it’s not a typo — investors in SurancePlus’s first series of tokenized reinsurance contracts (DeltaCat Re) are on track to hit a 42% annualized return this year.

Of course, with returns like that, you’re 100% correct in assuming there are some major caveats here.

There are.

And we’ll get to that soon.

But for now, the big takeaway here is that tokenization is not just here to stay — it’s also opening up some investment opportunities that were once the exclusive domain of institutions and the ultra-wealthy.

The Massive Tokenization Opportunity

Although it took big names like HSBC and BlackRock to first get my attention on this, it wasn’t until I started digging a little that I fell upon SurancePlus’s claimed 42% annualized returns.

That’s when tokenization really got my attention. After all, those returns beg so many questions. Notably:

- Is this just some dodgy HYIP?

- If not, are these abnormal returns?

- If not, what’s in it for SurancePlus/Oxbridge Re?

The first question, I’ll answer right off the bat. No, Bernie Madoff didn’t reincarnate as a reinsurance salesman.

Turns out, the SurancePlus offering is as legitimate as Berkshire Hathaway (NYSE: BRK-A / BRK-B) and Lloyds of London — two reinsurance providers you’ve probably heard of.

As for how I know this, that was by answering my other two burning questions.

So let’s work backward, starting with what’s in it for Oxbridge Re.

Tokenizing Reinsurance Contracts: What’s In it For Oxbridge Re/SurancePlus

To understand what these SurancePlus reinsurance tokens are all about, the first thing we need is a basic understanding of what reinsurance is.

In short, reinsurance is the insurance that consumer-facing insurance providers take out to protect themselves from catastrophic events.

To give an example, think back to 2005 — the year Hurricanes Katrina, Rita, and Wilma struck. These sorts of events are what the insurance industry calls a “major claims event” — an event so catastrophic that the inundation of claims would turn all but the biggest, most diversified providers into an insolvent mess in the blink of an eye.

Thus, to protect themselves and their clients, responsible insurance companies offload at least some of their exposure by taking out reinsurance contracts. Essentially, it’s insurance for insurance companies.

As we saw before, Berkshire Hathaway and Lloyds of London are two such companies. But they’re far from the only ones. Other names include Munich Reinsurance Company [FRA: MUV2], Swiss Re [SIX: SREN], and Oxbridge Re (NASDAQ: OXBR).

Naturally, these contracts don’t come cheap. In return for taking on risk for insurance companies, reinsurance providers demand massive premiums. After all, they’ve got businesses to run, too, so they need to guarantee they’ll stay profitable in the face of multiple major claims events.

These massive premiums partly explain how SurancePlus’s first tokenized reinsurance contracts are currently on track to deliver a 42% annualized return.

However, it doesn’t answer the next burning question — why would Oxbridge Re turn its nose up at keeping such massive profits for itself?

The answer to that lies in a little hint I dropped earlier — Oxbridge is a relative upstart.

To illustrate, take a look at some of the other players in the reinsurance markets.

Munich Re was founded in 1880.

Swiss Re was in 1863.

And Lloyds… it was founded in 1689.

Oxbridge, on the other hand, first burst onto the Nasdaq in 2014.

Now, in many industries, this could almost be a benefit. Fast, nimble companies without centuries of institutional overhead can do incredible things.

But reinsurance is a bit different. Growth is limited by current assets. Specifically, reinsurance companies need to keep a sharp eye on their solvency ratio — the balance of current assets against future liabilities.

In plain English, that means if a reinsurance company doesn’t have sufficient assets to cover future catastrophic events, it can’t keep selling reinsurance contracts.

And that’s where Oxbridge has used its fast and nimble status to its advantage. Instead of sitting on its hands and growing relatively slowly over the next century, it’s constantly looking to take outside capital on board.

And, with tokenization now working its way into institutional finance in a major way, Oxbridge saw the opportunity, added two and two together, and ran with it.

Thus the SurancePlus subsidiary was founded, and its first tokenized reinsurance contracts were born.

Now, as for how Oxbridge plans to grow through its SurancePlus offering, that’s simple. SurancePlus takes a slice of any profits made over the contract period. For the current offering, the profit split looks like this:

- Investors are entitled to a 20% preferred return

- The remaining profits are split 80/20 — 80% to the investor, 20% to SurancePlus.

Is SurancePlus’s 42% Return Abnormal?

To cut straight to the chase, SurancePlus’s tokenized reinsurance contracts won’t always give such stellar returns. Over the long term, returns are probably going to be slightly more modest. Although, ultimately, that will depend on what the weather does.

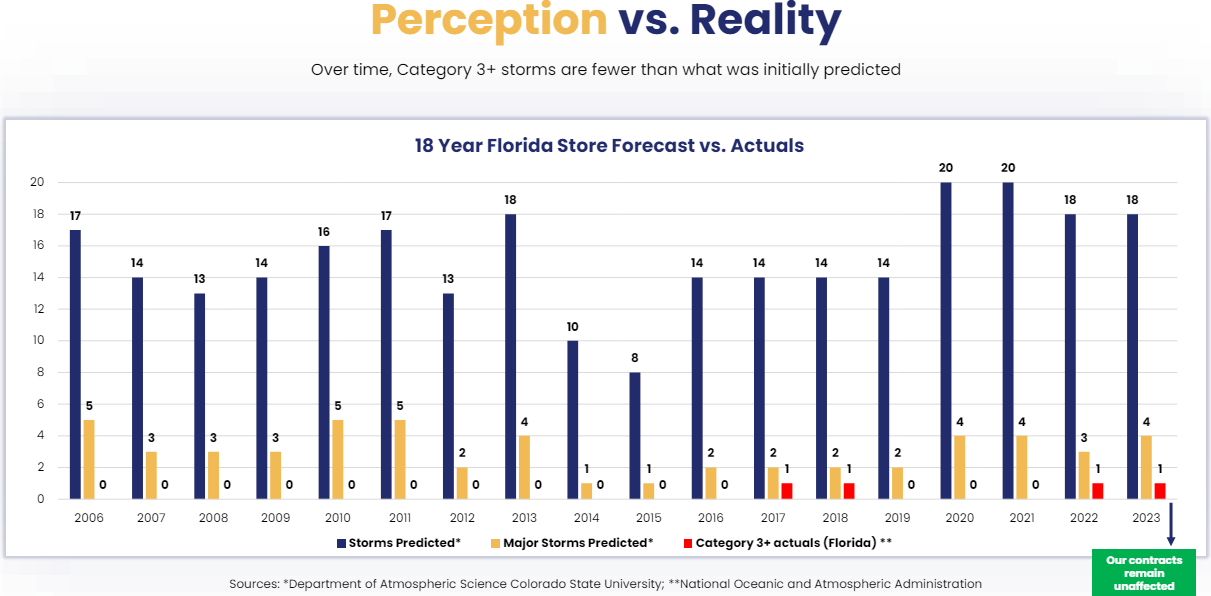

To explain, let’s get one thing straight — the reinsurance contracts SurancePlus is tokenizing are concentrated on the Florida market. Smack bang in the middle of hurricane alley.

That’s why returns are so massive — reinsurance premiums are through the roof here.

As for the impact this can have on future returns, that depends on the probability of a catastrophic “major claims event” like in 2005. Basically, if 2005 happens all over again, then there’s probably a pretty good chance you’re gonna lose a good chunk of your principal, if not all of it.

But with that said, the next question is so what?

For context, those sorts of events are said to only happen once every 100 years for a reason.

So, if you can think of reinsurance contracts as a long-term investment opportunity, then I’ll let you do the math on how many times you make your money back in 100 years at an annualized return of 42%. (Hint: If you double your money in two years, that works out to an annualized return of 41.42%.)

Of course, the next Hurricane Katrina isn’t the only risk — smaller hurricanes still happen, and they can eat into the returns investors in SurancePlus reinsurance tokens will see. Generally, this will start to happen at the Category 3+ level, although at Cat 3, the impact is generally minor, if any.

To put the full risk into better perspective, take a look at the history since the last massively catastrophic hurricane events of 2005.

At that rate, we’re still looking at massive returns deep into the double digits over the long term. The only trick is seeing reinsurance as a long-term play, not a quick way to make a fast buck.

This is what Llloyds of London and its ilk have been doing for hundreds of years. And with tokenization now democratizing access to these sorts of investment opportunities, it should be what retail investors start doing, too.

What’s Next for SurancePlus and Oxbridge as Tokenization Takes Off?

Right now, tokenizing is still in its infancy. But if BlackRock’s $10 trillion promise is a sign of things to come, things are about to explode.

But there is a lot of very smart money making some very big bets on this. BlackRock’s $10 trillion promise is just one example, but there are plenty of others clambering to get in.

This is perhaps most evident if we take a look at where VCs are investing besides AI. To give two recent examples, two startups building on-chain insurance marketplaces, Nayms and Re, recently closed major funding rounds at $80 million and $100 million valuations, respectively.

That’s insane money.

Especially when we consider that they’re simply intermediaries in the exchange of tokens. And even more so when we consider their existing traction. Nayms, for example, has only acted as the intermediary on about $1.6 million worth of reinsurance tokens. And, right now, it’s attempting to sell another $12.8 million by March next year.

Effectively, VCs are valuing Nayms at $80 million off the back of an expected $14.4 million in tokens by next year.

Meanwhile, SurancePlus has slipped under the radar a little, overshadowed by its parent company, Oxbridge Re [NASDAQ: OXBR], which is currently hovering around a market cap of about $12-13 million.

Clearly, investors are sleeping on (or simply not seeing) the SurancePlus opportunity yet. Instead, they’re valuing Oxbridge Re as though it were a traditional, pure-play reinsurance provider. But with the momentum behind tokenization and its SurancePlus play, Oxbridge Re is on a fast-track path to explosive growth.

Oxbridge Re, on the other hand, clearly seems to know what it’s sitting on with SurancePlus. Just yesterday, the company announced its intention to explore options to increase shareholder value big time. Some options here include “a sale, spinout, merger, divestiture, recapitalization, and other strategic transactions, or continuing to operate as a public, independent company.”

Whatever the case, there is one thing that’s almost guaranteed here — any move along these lines would force shareholders to reevaluate Oxbridge for what it really is. That is, a fast-growing company on the bleeding edge of a tokenization boom. This should bring about a massive reassessment of its current valuation.

As for what a fair valuation would look like, things are moving too fast to pin that down exactly right now. But to put some perspective on it, SurancePlus has already closed its $5 million DeltaCat Re token issuance — already well ahead of Nayms. And right now, SurancePlus is fast closing on its current EpsilonCat Re series, which is double the size at $10 million.

That brings the total value of both the Epsilon and Delta token issuance to $15 million.

Now, does this mean SurancePlus/Oxbridge Re should be valued similarly to Nayms and Re?

That, I don’t know for sure.

Ultimately, we’re comparing apples and oranges here. Nayms and Re are, effectively, intermediaries, whereas SurancePlus is the token issuer.

Practically, that leaves SurancePlus with a much bigger cut of the value of any tokens it issues. Remember, it skims a healthy 20% of the profit remaining after its investors receive their preferred 20% return. In real terms, to use the 43% return to investors on the DeltaCat Re tokens as an example, that works out to about 5-6% a year for SurancePlus on every token it issues.

That might seem like chump change for now while it’s only got $15 million worth of tokens in the works. But, remember, that’s just the beginning.

In the long term, SurancePlus has more or less given itself a license to print money. Within limits, of course. The number of tokens it issues is, after all, limited by the size of the reinsurance market and people’s willingness to buy tokenized RWAs.

To put numbers on those, reinsurance is worth $444 billion this year, and there aren’t that many players fighting for that. Oxbridge Re is one of them.

And, if BlackRocks $10 trillion tokenization move is anything to go by, the market for SurancePlus tokens is only just getting started.

Long story short — SurancePlus should be worth a heck of a lot more than Oxbridge Re’s current market cap. Probably even more than Re and Nayms.

Oh, and did I mention the CEO of this hidden reinsurance gem?

That’s Jay Madhu. He’s also a founder/director at HCI Group [NYSE: HCI]. That went public at $7 a share. Today, HCI’s hovering around $100.

To learn more about Oxridge Re, visit its page on Yahoo Finance.

To learn more about the next issuance of SurancePlus tokenized reinsurance contracts (EpsilonCat Re), visit SurancePlus.

__

(Featured image by Shubham Dhage via Unsplash)

DISCLAIMER: This article was written by a third party contributor and does not reflect the opinion of Born2Invest, its management, staff or its associates. Please review our disclaimer for more information.

This article may include forward-looking statements. These forward-looking statements generally are identified by the words “believe,” “project,” “estimate,” “become,” “plan,” “will,” and similar expressions. These forward-looking statements involve known and unknown risks as well as uncertainties, including those discussed in the following cautionary statements and elsewhere in this article and on this site. Although the Company may believe that its expectations are based on reasonable assumptions, the actual results that the Company may achieve may differ materially from any forward-looking statements, which reflect the opinions of the management of the Company only as of the date hereof. Additionally, please make sure to read these important disclosures.

Blockchain Evolves Toward AI, Finance and Quantum Security

Blockchain is evolving beyond crypto into finance, AI applications, and digital markets, while security and regulation remain challenges. Quantum threats...

The Italian Crowdinvesting Market Faces Sharp Decline in 2026

Italian crowdinvesting market continued to decline in 2026, with fundraising falling 36.8% year-on-year to €164.19 million. Platforms and active campaigns...

Sartorius Stedim Biotech Maintains Growth Momentum in H1 2026

Sartorius Stedim Biotech reported solid H1 2026 results, with revenue reaching €1.527 billion and EBITDA rising to €479 million. Growth...

Bank of Africa Launches BOA MDM Network to Boost Diaspora Investment in Morocco

Bank of Africa launched the BOA MDM Network to channel diaspora remittances into productive investment, aiming to raise their share...

Switzerland’s Medical Cannabis Reform Advances Access, But Barriers Remain

Switzerland’s 2022 medical cannabis reform improved patient access by removing federal approval requirements, but challenges remain. MEDCAN highlights barriers including...

|

|

|  |

|

|

-

Markets7 days ago

Markets7 days agoOil Surge, Weak Stocks, and a Potential Turn for Gold

-

Markets2 weeks ago

Markets2 weeks agoQuiet Markets Await a Catalyst as Jobs and Oil Support Sentiment

-

Crypto4 days ago

Crypto4 days agoBitcoin ETFs Lead as German Stock Exchange Debuts Mining ETF

-

Crowdfunding2 weeks ago

Crowdfunding2 weeks agoInsight Foto Festival Launches €4,500 Crowdfunding Campaign to Support 2026 Edition