Featured

Chinese demand spurs growth in the soybeans market

World vegetable oils markets were mixed last week. Palm Oil closed higher after news of renewed demand interest from India and China and on reports of less production from Malaysia. SGS reported improved exports in its data. Rice was a little higher in new crop months and much lower in old crop July. Coffee futures were lower in both New York and London as the Brazil harvest is underway.

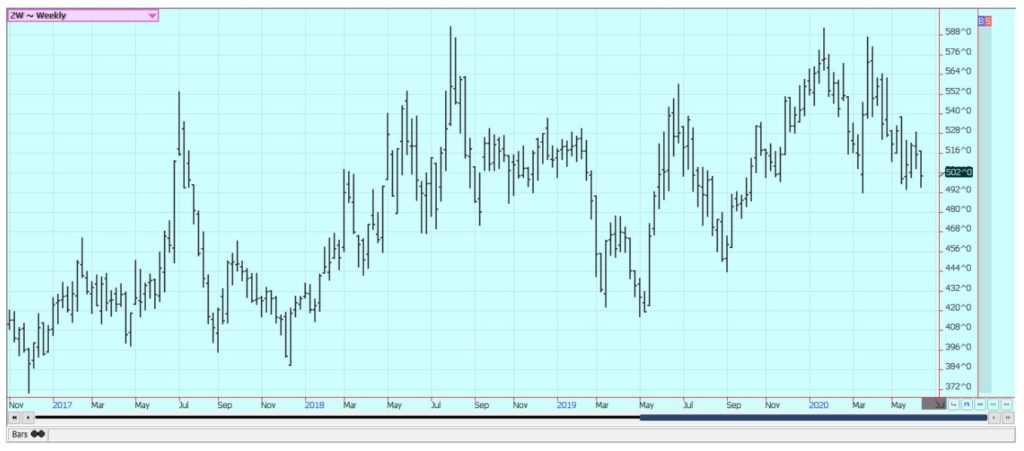

Wheat

Wheat markets were lower for the week after USDA raised US production prospects and raised world ending stocks levels. The moves by USDSA pointed to tough competition down the road for US export sales. The Winter Wheat markets hold to bearish trends on the weekly charts and this is especially true for the HRW market. Spring Wheat markets show down trends as the US and Canadian crops are getting planted and are reported to be in mostly good condition. The harvest has started in the central and southern Great Plains with variable yields reported because of freeze damage and then stress from hot and dry weather, but the yields from USDA were a little higher than expected and ay cuts to HRW production were offset by better SRW and White Wheat production. It remains dry in the western sections of the Great Plains but this will aid harvest progress now. Better rains are reported in Europe and Russia. Russia could turn hot and dry starting this week but soil moisture is good for now. Australia remains in good condition. The harvest is coming and prices usually start to move lower soon and remain down through the harvest.

Corn

Corn was a little lower on the weekly charts as the current seasonal rally appeared to stall. USDA made no big changes in its ending stocks estimates as it cut production due to losses last year in the Dakotas but also cut demand due to less ethanol production. Many in the trade expect further cuts to ethanol demand in coming reports. Meats processors are back and are aiming to restore 80% to 85% of capacity kill rates in their plants. The backlog of Cattle and Hogs will slowly disappear under this scenario and meats wholesale and retail prices will fall. This will take some time, but it is starting to come to pass. Ethanol demand is also improving as lockdown orders are lifter in most states and in Europe. Demand for gasoline and ethanol has gotten a little stronger and should continue to improve over time. The US weather and growing conditions are becoming more important as Corn enters its greatest demand time for moisture. It will be hot and dry this week in the Great Plains and Midwest, but forecasts call for more rains after that. This implies that generally good growing conditions should continue. Continued hot and dry weather would imply yield loss potential and be a reason to see prices move sharply higher as funds and speculators in general are short the market. Oats gave up their rally last week and chart trends are turning down in a big way. Demand should start to back off now that many are leaving the house and are working again.

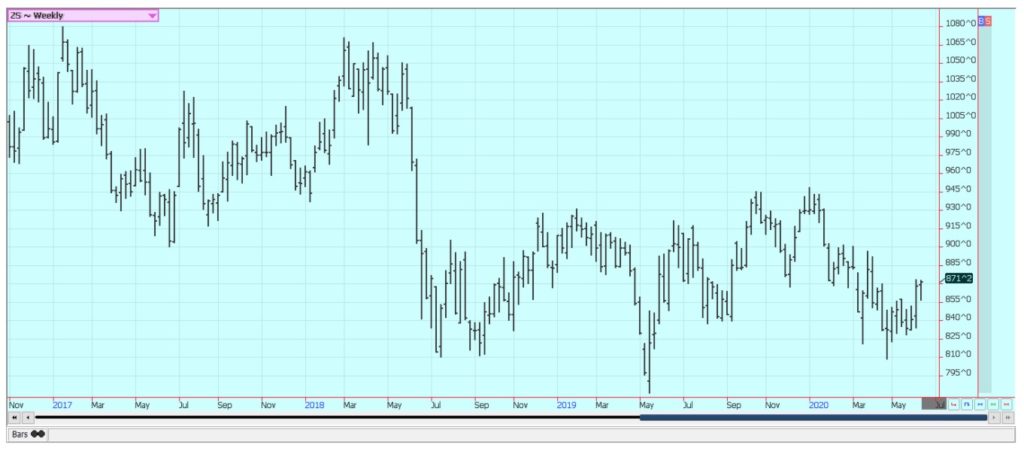

Soybeans and Soybean Meal

Soybeans were higher on improved Chinese demand. China is thought to have bought more than 1.0 million tons of US Soybeans in the past week, defying the talk that it would avoid US Soybeans due to the war of words between the two countries on Hong Kong and general human rights issues. The Chinese moves to clamp down on Hong Kong dissent was going to be a big negative for bilateral relations as the political situation between the US and China has deteriorated. China is looking to curb the dissent in Hong Kong over moves to bring the city more under central government control from Beijing. It is also moving against Muslims in western parts of the country. The world has objected and the US has now imposed some additional sanctions on the country. The sanctions were designed to keep trade flowing between the countries so the Chinese kept buying. China has remained a very active buyer in South America even as it has increased Soybeans buying here in the US, so the overall amount taken from the US might not match the hopes of the trade. Brazil prices have been creeping higher for the rest of the world as it starts to run out of Soybeans to export, so China and the rest of the world will look to the US and Argentina for additional supplies. The US weather is considered good for growing Soybeans at this time, but traders are watching for potentially hot and dry weather for an extended period that could cut yield potential. Forecasts call for a hot and dry week this week, but rains are expected after that.

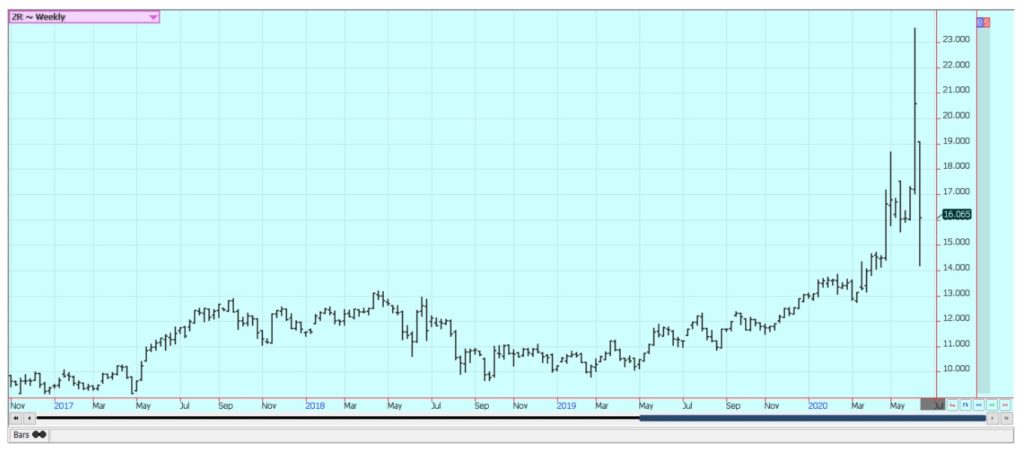

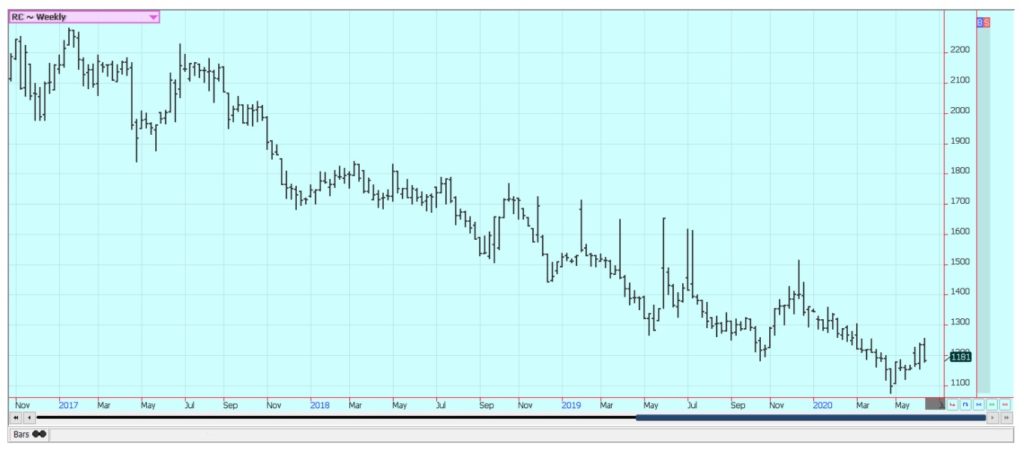

Rice

Rice was a little higher in new crop months and much lower in old crop July. July started to collapse a week ago as the funds initially bought the market and then were forced to sell. The selling continued for most of the week last week, but July managed to close limit up on Friday. New crop months were relatively little changed as new crop prospects appear solid for increased production in the coming year. The funds were initially buying the old crop futures on ideas of supply tightness and started to buy again on Friday for the same reason. The combination of good export buying in general and the buying inside the US due to the Coronavirus has made the market short Rice. There are ideas that the mills are well covered into new crop, but little Rice is available from producers. The crops that got planted are in very good condition in the south and near the Gulf Coast but planting has been problematic in parts of Mississippi, Arkansas, and Missouri. Ideas are that the long grain will get planted and producers will not plant medium grain if some prevent planting is needed.

Palm Oil and Vegetable Oils

World vegetable oils markets were mixed last week. Palm Oil closed higher after news of renewed demand interest from India and China and on reports of less production from Malaysia. SGS reported improved exports in its data last week. Palm Oil has been hoping for better demand from importers as world economies slowly open after being closed by the Coronavirus epidemic. Indonesia continues to focus its Palm Oil on internal demand for bio fuels. Soybean Oil was lower last week and Canola was higher. Canola fell initially on improved growing conditions in the Canadian Prairies. Canola has found support from the weaker Canadian Dollar. Canola is more of a food oil than the others, although it also has bio fuels uses. The weather has been warmer the past couple of weeks after weeks of cold and wet weather.

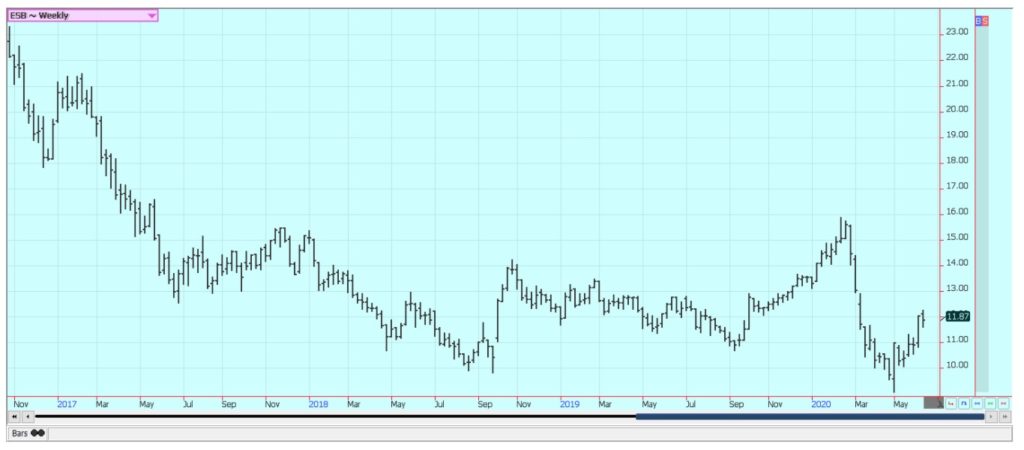

Cotton

Cotton closed lower bet held support on the weekly charts. Signs of an improving economy in the US and around the world really helped ideas of better Cotton demand as did reports of a lot of masks being made for use during the Coronavirus epidemic. There is concern that China will stop fulfilling its obligations in the Phase One trade deal due to ramped up US rhetoric on the Chinese response to the Coronavirus epidemic and now the unrest in Hong Kong. The world is starting to slowly recover from the Coronavirus scare and some stores are starting to open again after being closed for weeks. The retail demand has been slow to develop as many consumers got hurt economically due to stay at home orders during the height of the pandemic and have little disposable funds to spend on clothes. Demand will slowly improve but the industry should have plenty of supplies to work with in the short term. The US weather situation is mixed, with good rains noted in the Southeast and good conditions in the Midsouth. However, it has been very hot and dry in West Texas and crops there are suffering.

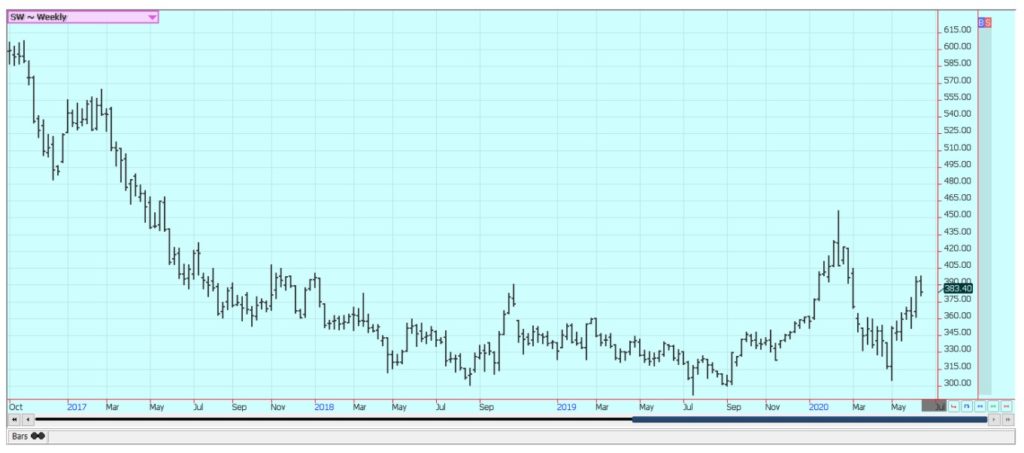

Frozen Concentrated Orange Juice and Citrus

FCOJ was lower with much of the selling coming on Friday. The selling came for chart based reasons as futures were unable to take out recent highs even though USDA released reduced production estimates for US production. Florida production is now estimated at less than 68 million boxes. Support is coming from the continued effects from the Coronavirus that are keeping people at home and drinking Orange Juice. Demand from grocery stores has remained strong in response to the increased consumer demand. Inventories in cold storage remain solid so there will be FCOJ to meet the demand. There is increasing concern about the food service demand not improving even with the partial opening of the states. The weather in Florida is currently good for the crops. Southern areas are cooler and have seen more frequent showers. The tree condition is called good. The Valencia harvest is in full swing. Brazil has been dry and irrigation has been used.

Coffee

Futures were lower in both New York and London as the Brazil harvest is underway and starting to expand. Ideas are that production will be very strong this year as it is the on year for the trees. The strong production ideas are coming despite hot and dry weather seen in the country at flowering time. Vietnam also had hot and dry weather at flowering time and production ideas there are less than original expectations of a bumper crop. The demand from coffee shops and other food service operations is improving but is still at very low levels. Consumers are still drinking Coffee at home, but many smaller roasters are actively trying to unload green coffee already bought a there are only a few outlets for sales at this time. The logistics of moving Coffee from Central and South America remain difficult. Producers have had trouble getting workers to pick the cherries and mills and processors have had trouble getting workers to staff the plants. Shipping logistics have improved somewhat, but many are still having trouble getting the Coffee to ports to move to consumer nations. Indonesian producers are more active sellers.

Sugar

New York and London closed lower in part on weaker petroleum prices. The market acts as if there is a short supply of White Sugar available. The Brazil mills are trying to cover the lack of White Sugar in the market but might switch back to producing ethanol soon if prices continue to improve for the ethanol. Brazil mills are currently producing about 48% Sugar from the cane crush, from about 33% a year ago. The overall crush rate is below year ago levels. Reports indicate that little is on offer from India in part due to logistical and harvest problems caused by the Coronavirus. India is thought to have a very big crop of Sugarcane this year but getting it into Sugar and into export position has become extremely difficult. Thailand might also have less this year due to reduced planted area and erratic rains during the monsoon season. There are reduced flows from rivers from China as well.

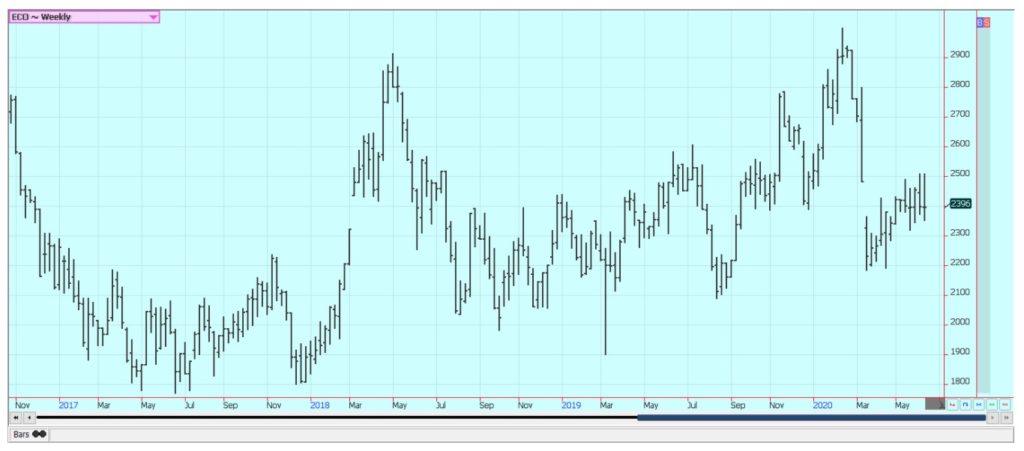

Cocoa

New York and London closed lower for the week but a little higher on Friday. New York is showing a double top on the charts at about 2300 July. There are a lot of demand worries as the Coronavirus is not going away and could be making a comeback in the US. Harvest is now over for the main crop in West Africa and the results so far are very good. The reports from West Africa imply that a big harvest in the region. However, the Midcrop could be less due to dry weather earlier in the season. Arrivals are on a pace about the same as last year. Ideas are that Southeast Asia also has good crops.

—

(Featured image by pnmralex via Pixabay)

DISCLAIMER: This article was written by a third party contributor and does not reflect the opinion of Born2Invest, its management, staff or its associates. Please review our disclaimer for more information.

This article may include forward-looking statements. These forward-looking statements generally are identified by the words “believe,” “project,” “estimate,” “become,” “plan,” “will,” and similar expressions. These forward-looking statements involve known and unknown risks as well as uncertainties, including those discussed in the following cautionary statements and elsewhere in this article and on this site. Although the Company may believe that its expectations are based on reasonable assumptions, the actual results that the Company may achieve may differ materially from any forward-looking statements, which reflect the opinions of the management of the Company only as of the date hereof. Additionally, please make sure to read these important disclosures.

Youth Cannabis Use in Colorado Is Falling — But the Full Story Is More Complex

The 2026 Colorado survey shows teen cannabis use fell to 10 percent in 2025, down from 21 percent in 2015....

Morocco’s Growth Holds at 4.6% as Agriculture Offsets Economic Pressures

Morocco’s economy grew 4.6% in Q1 2026, driven by a strong agricultural rebound offsetting declines in industry. Services expanded moderately...

Abivax Shares Surge as New Trial Data Eases Safety Concerns Over Ulcerative Colitis Drug

Abivax shares surged nearly 36% after positive updated trial results for its ulcerative colitis drug obefazimod reassured investors following earlier...

El Dorado Raises $9M to Expand Cross-Border Fintech Platform

El Dorado, a Latin American fintech improving cross-border financial services, raised a $9 million Series A led by Paradigm with...

Bitcoin Stalls Near $60K as Strategy Moves, ETFs Outflow, and EU MiCA Rules Take Effect

Bitcoin hovers near $60,000 with ETF outflows, while Strategy boosts reserves, sells BTC, and raises dividends to reassure investors. Ethereum...

|

|

|  |

|

|

-

Impact Investing2 weeks ago

Impact Investing2 weeks agoAI Adoption in Italian Retail Stalls Despite Strong Experimentation

-

Cannabis1 day ago

Cannabis1 day agoCannabis Dominates Global Drug Use: Trends, Risks, and Shifting Markets

-

Impact Investing1 week ago

Impact Investing1 week agoEU Weighs More Free Emission Permits in ETS Review to Boost Industry Competitiveness

-

Crypto5 days ago

Crypto5 days agoBitcoin and Ethereum Slide as Market Pressure Builds Amid Strategy Concerns and Layer 2 Disruptions