Markets

Why Coffee Markets Closed Higher Last Week

Both coffee markets closed higher last week on reports of logistical and weather-related problems in Brazil ports. Showers and rains are now being reported in central and southern growing areas of Brazil, with the biggest amounts in the south by far. Loading at and transportation to ports has been affected by the rain as well. Demand for Robusta and lower quality Arabicas remains around the market.

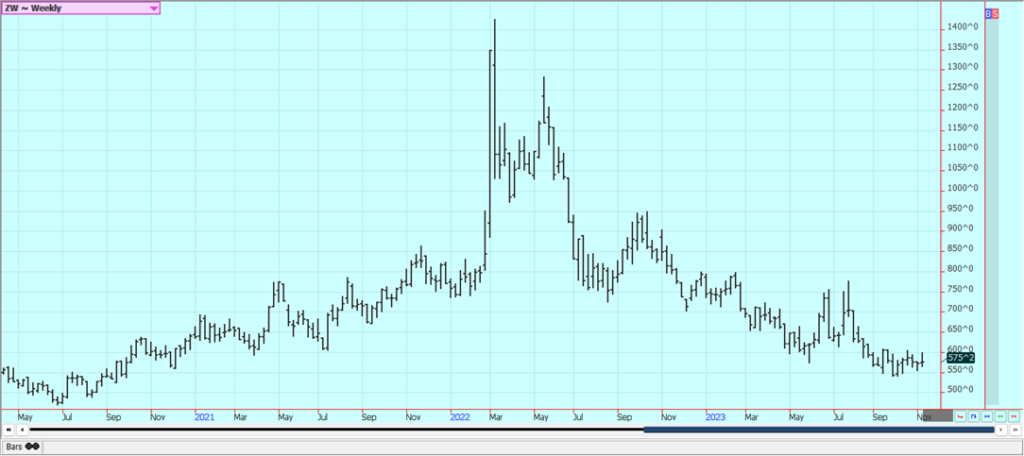

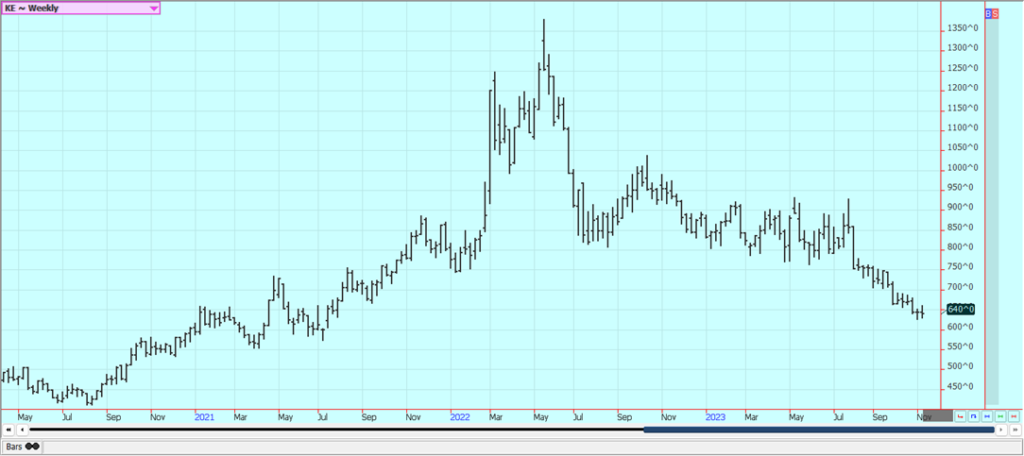

Wheat: Wheat markets were lower for HRW, but higher for SRW and HRS last week in lifeless trading. The USDA estimates showed higher-than-expected ending stock estimates for the US and the world. USDA increased imports by 10 million bushels and cut back slightly on domestic demand while leaving export demand unchanged. US ending stocks were estimated at 684 million bushels, from 670 million last month.

USDA increased world Wheat production and also demand for ending stocks estimates of 258.7 million tons, from 258.1 million last month Ukraine is still exporting through the Black Sea. Russia is still exporting and offering Wheat into the world market and is reporting that it is larger than originally thought. Ukraine and the EU countries are offering as well and are getting new business.

Demand has been poor for US Wheat as Russian production looks strong, but exports are expected to increase for the rest of the marketing year. Weather forecasts call for drier weather for Australia, with production losses now expected. There are reports of some showers in both countries to raise production estimates slightly but not enough to bring production close to averages. Argentine conditions are reported to be good after a very dry start but showers and rains in recent weeks. It has been too wet in southern Brazil and much of the Wheat grown there is expected to be feed grade instead of milling grade.

Weekly Chicago Soft Red Winter Wheat Futures

Weekly Chicago Hard Red Winter Wheat Futures

Weekly Minneapolis Hard Red Spring Wheat Futures

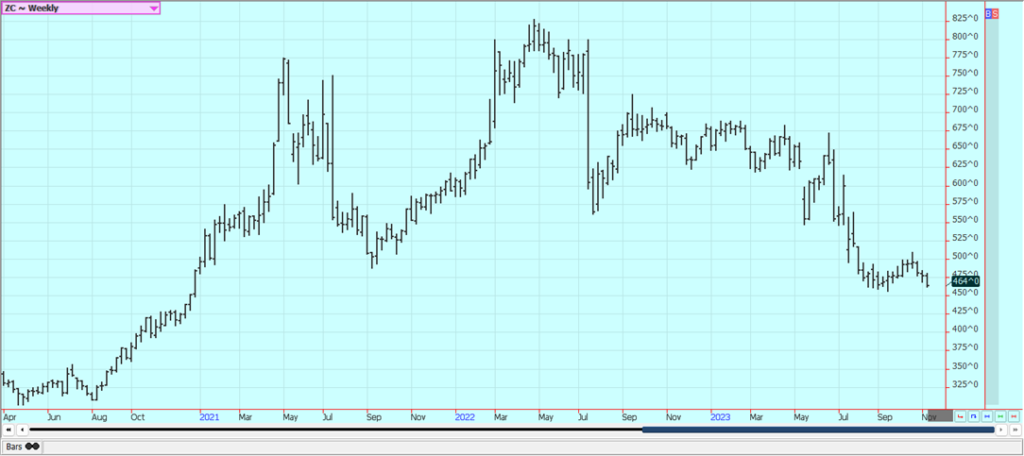

Corn: Corn closed lower last week and made new contract lows in response to the USDA reports. USDA increased yields and production much more than expected and US production is now estimated at 15.234 billion bushels, from 15.064 billion last month. Demand was increased slightly for just about all categories but ending stocks were higher at 2.156 billion bushels, from 2.111 billion last month.

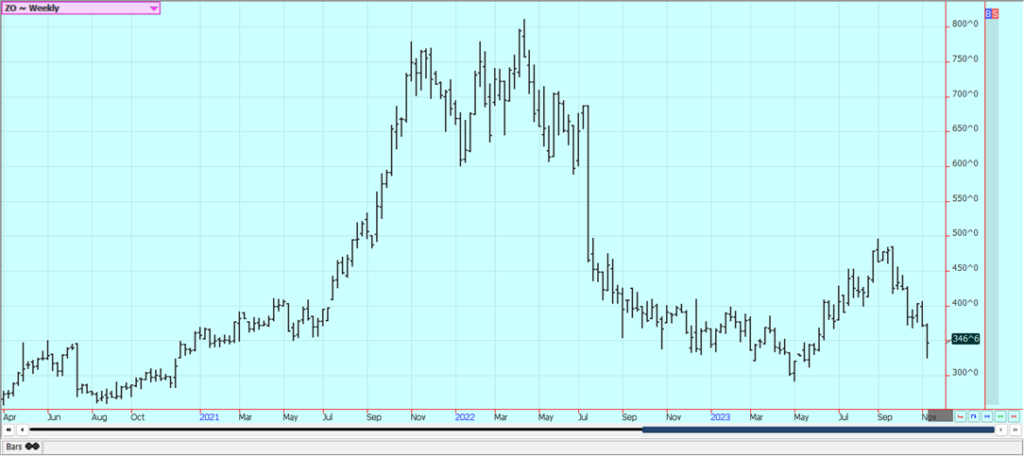

World-ending stocks were increased to 315 million tons, from 312.4 million last month. The weekly export sales report was strong last week. Oats closed lower but made a hook reversal higher on Friday and could see additional buying this week. It is still hot and dry in central and northern Brazil and in Argentina although some beneficial rains have been reported in Argentina and a few showers are reported in central and northern Brazil. Southern Brazil is much too wet. The weather patterns seem stuck in South America.

Weekly Corn Futures

Weekly Oats Futures

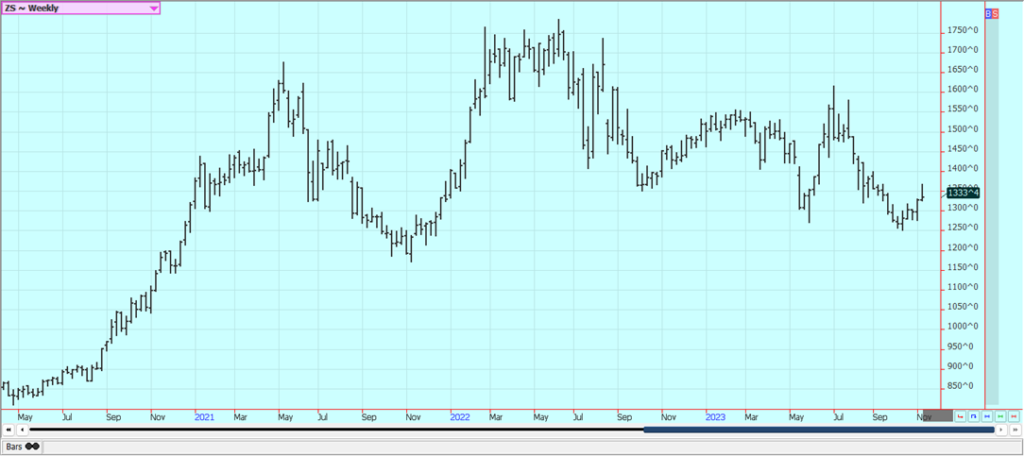

Soybeans and Soybean Meal: Soybeans closed a little higher last week despite late-week selling that developed in response to the USDA reports. Soybean Meal and Soybean Oil were higher. The weekly export sales report was strong and strong sales have been reported to China and unknown destinations on the daily reporting system. But, USDA issued bearish reports. USDA estimated yields and production a little higher at 4.129 billion bushels, from 3.104 billion last month. The trade had expected a slight decline in production.

Ending stocks were 245 million bushels, from 220 million last month. World stocks were estimated at 114.5 million tons, from 115.6 million last month. Futures have rallied a lot lately and were due a correction. The selling could be running out of steam as futures are just above support areas on the daily charts. The trade remains concerned about the weather forecasts for South America. Brazil remains mostly hot and dry in northern areas and too wet in southern areas. These weather trends are expected to continue.

Weekly Chicago Soybeans Futures

Weekly Chicago Soybean Meal Futures

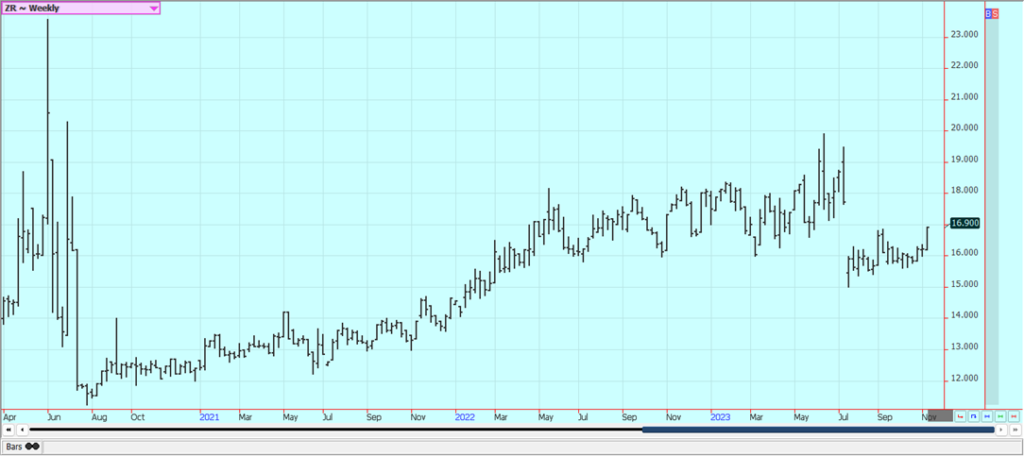

Rice: Rice closed higher again Friday in part to the USDA reports. Buying was seen all week as the harvest had ended and the crops are in the bin. The USDA reports showed that production was cut back and demand was left unchanged for an ending stocks estimate of 40.9 million cwt, from 41.8 million last month.

The production losses were spread between long and medium/short grains. Ending stocks levels for long grain are now 22.2 million cwt and are 15.4 million cwt for medium/short grain. Futures on Friday smashed through some important resistance areas and completed a sharp five day rally. The weekly chart trends have turned up.

Weekly Chicago Rice Futures

Palm Oil and Vegetable Oils: Palm Oil was higher last week on news of strong export demand from MPOB. Production was high but this was expected. The strong demand was not expected. Private surveyors showed that the strong demand continues for the month to date. Trends are mixed on the daily charts. Canola closed higher and near the highs of the week. The crop is harvested and it is in bins, so it will take some price movement to get new farm sales. Trends are bottoming on the daily charts in this market.

Weekly Malaysian Palm Oil Futures

Weekly Chicago Soybean Oil Futures

Weekly Canola Futures:

Cotton: Cotton closed lower last week, but rallied late in the week despite bearish USDA reports. It appears that the bearish reports were already part of the price and now the market is trying to form at least a short-term bottom on the charts The weekly export sales report was strong and helped support prices. The monthly USDA reports were mostly ignored as market factors.

USDA increased yields and production to 13.090 million bales. The demand side showed a little lower domestic demand but unchanged export demand. Ending stocks levels were increased to 320 million bales from 280 million last month. World ending stocks levels were also increased. There are still many concerns about demand from China and the rest of Asia due to the slow economic return of China in the world market. There are production concerns about Australian and Indian Cotton as both countries are likely to suffer the effects of El Nino starting this Fall.

Weekly US Cotton Futures

Frozen Concentrated Orange Juice and Citrus: FCOJ closed lower last week with most of the cart damage done early in the week, and the trends on the daily charts are mixed. January has assumed top step position with the expiration of November futures and the change accounted for a large part of the decline on the weekly charts. There are no weather concerns to speak of for Florida right now with the hurricane season all but over and no major storms hitting the state recently.

Reports of short supplies in Florida and Brazil are around. Futures are also being supported by forecasts for an above-average hurricane season that could bring a storm to damage the trees once again. Historically low estimates of production due in part to the hurricanes and in part to the greening disease that has hurt production, but conditions are significantly better now with scattered showers and moderate temperatures.

Weekly FCOJ Futures

Coffee: Both markets closed higher last week on reports of logistical and weather-related problems in Brazil ports. Showers and rains are now being reported in central and southern growing areas of Brazil, with the biggest amounts in the south by far. Loading at and transportation to ports has been affected by the rain as well.

Demand for Robusta and lower quality Arabicas remains around the market. The lack of offers from Asia, mostly from Vietnam but also Indonesia remains a main feature of the market, but the offers are starting to improve. Offers from Brazil and other countries in Latin America should be increasing

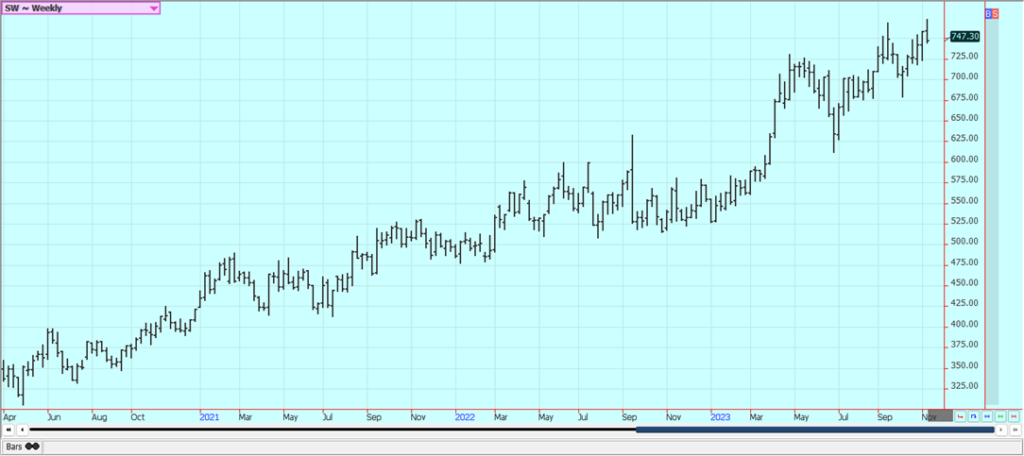

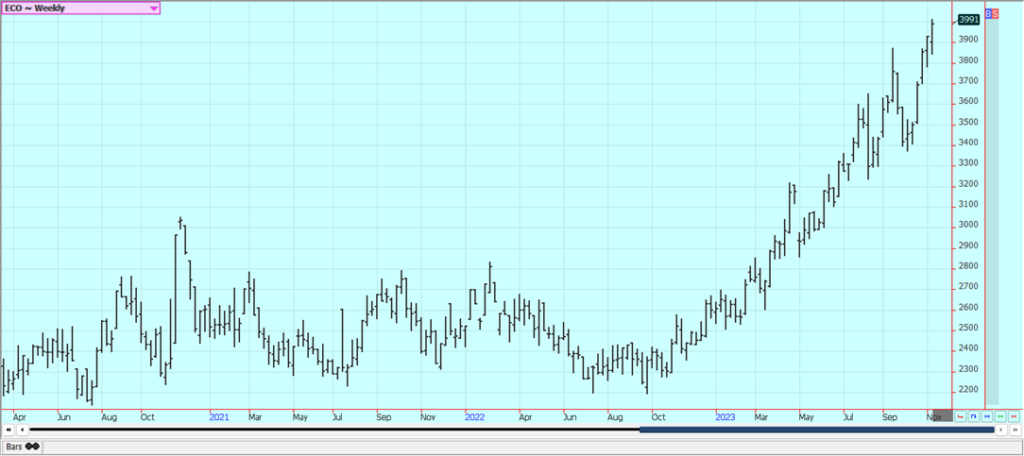

Weekly New York Arabica Coffee Futures

Weekly London Robusta Coffee Futures

Sugar: New York and London closed lower last week as Future shied away from making new contract highs. There are still port delays in Brazil and too much rain in central and southern areas of the country. The market is still short of Sugar. There are still forecasts for and reports of rain in Brazil. The market continues to see stressful conditions in Asian production areas. The Brail rains is underway now and have been heavy in the south.

There are worries about the Thai and Indian production potential due to El Nino. Offers from Brazil are still active but other origins are still not offering or at least not offering in large amounts, and demand is still strong. Brazil ports are very congested so shipment of Sugar has been slower. Unica said that the Brazil Center South sugar crush was 34.6 million tons, up 8/1% from last year. Mills produced 2.4 million tons of Sugar, up 9.4% from last year, and 1.8 billion liters of Ethanol, up 11% from last year.

Weekly New York World Raw Sugar Futures

Weekly London White Sugar Futures

Cocoa: New York and London closed higher last week and at new highs for the move. Traders are worried about another short production year and these feelings have been enhanced by El Nino which could threaten West African crops with hot and dry weather later this year. Cocoa arrivals at Ivory Coast ports dropped 16.2% for the marketing year when compared to last year. The main crop harvest comes into focus and as farmers in West Africa report that many areas have too much rain that has caused harvest delays and could lead to disease.

Scattered to isolated showers are reported in the region now. Ideas of tight supplies remain based on more reports of reduced arrivals in Ivory Coast and Ghana continue, Midcrop production ideas are lower now with diseases reported in the trees due to too much rain that could also affect the main crop production. Port arrivals in top grower Ivory Coast in the week to Nov. 5 totaled 63,000 metric tons, up from 53,000 tons in the same week last season. For the season-to-date, however, they are down 16.7% from the same period last season.

Weekly New York Cocoa Futures

Weekly London Cocoa Futures

__

(Featured image by PublicDomainPictures via Pixabay)

DISCLAIMER: This article was written by a third party contributor and does not reflect the opinion of Born2Invest, its management, staff or its associates. Please review our disclaimer for more information.

This article may include forward-looking statements. These forward-looking statements generally are identified by the words “believe,” “project,” “estimate,” “become,” “plan,” “will,” and similar expressions. These forward-looking statements involve known and unknown risks as well as uncertainties, including those discussed in the following cautionary statements and elsewhere in this article and on this site. Although the Company may believe that its expectations are based on reasonable assumptions, the actual results that the Company may achieve may differ materially from any forward-looking statements, which reflect the opinions of the management of the Company only as of the date hereof. Additionally, please make sure to read these important disclosures.

Futures and options trading involves substantial risk of loss and may not be suitable for everyone. The valuation of futures and options may fluctuate and as a result, clients may lose more than their original investment. In no event should the content of this website be construed as an express or implied promise, guarantee, or implication by or from

The PRICE Futures Group, Inc. that you will profit or that losses can or will be limited whatsoever. Past performance is not indicative of future results. Information provided on this report is intended solely for informative purpose and is obtained from sources believed to be reliable. No guarantee of any kind is implied or possible where projections of future conditions are attempted. The leverage created by trading on margin can work against you as well as for you, and losses can exceed your entire investment. Before opening an account and trading, you should seek advice from your advisors as appropriate to ensure that you understand the risks and can withstand the losses.

Blockchain Evolves Toward AI, Finance and Quantum Security

Blockchain is evolving beyond crypto into finance, AI applications, and digital markets, while security and regulation remain challenges. Quantum threats...

The Italian Crowdinvesting Market Faces Sharp Decline in 2026

Italian crowdinvesting market continued to decline in 2026, with fundraising falling 36.8% year-on-year to €164.19 million. Platforms and active campaigns...

Sartorius Stedim Biotech Maintains Growth Momentum in H1 2026

Sartorius Stedim Biotech reported solid H1 2026 results, with revenue reaching €1.527 billion and EBITDA rising to €479 million. Growth...

Bank of Africa Launches BOA MDM Network to Boost Diaspora Investment in Morocco

Bank of Africa launched the BOA MDM Network to channel diaspora remittances into productive investment, aiming to raise their share...

Switzerland’s Medical Cannabis Reform Advances Access, But Barriers Remain

Switzerland’s 2022 medical cannabis reform improved patient access by removing federal approval requirements, but challenges remain. MEDCAN highlights barriers including...

|

|

|  |

|

|

-

Crypto2 weeks ago

Crypto2 weeks agoBitcoin’s Price Drops as Investors Turn to Layer 2 Solutions

-

Markets6 days ago

Markets6 days agoSugar Markets Balance Biofuel Demand and Global Supply

-

Africa2 weeks ago

Africa2 weeks agoMorocco Cuts Card Fees to Spur Digital Payments, but Uncertainty Remains

-

Biotech3 days ago

Biotech3 days agoSartorius Stedim Biotech Maintains Growth Momentum in H1 2026