Markets

Commodity Futures Markets Struggle Under Weight of Strong Harvests and Global Uncertainty

Commodity markets kicked off the month of August on a reasonably uncertain footing, as a mix of strong harvest reports, shifting global weather patterns, and renewed macroeconomic jitters sent ripples across futures markets. From grains to softs, traders have been weighing up robust supply signals against lingering questions about demand, trade flows, and ongoing geopolitical risk.

The first week of August brought renewed pressure across the commodity markets, as futures for grains, softs, and oilseeds slid on a mix of strong crop outlooks, shifting weather conditions, and macroeconomic headwinds. U.S. harvest progress—particularly in wheat and corn—continues at a solid pace, with improving yields and cooler temperatures reinforcing bearish sentiment. At the same time, global supply concerns remain in the background, with dryness in parts of Canada, Russia, and Ukraine tempering the overall optimism.

Outside of grains, export demand remains uneven, and geopolitical tensions—especially in the Black Sea region—add further complexity to price movements. Soft commodities like coffee, sugar, and cotton also faced sell-offs, triggered in part by weaker-than-expected U.S. jobs data and shifting trade policies. With volatility returning to the broader economic landscape and harvest season ramping up, markets appear stuck in a tug-of-war between robust supply narratives and lingering global uncertainties.

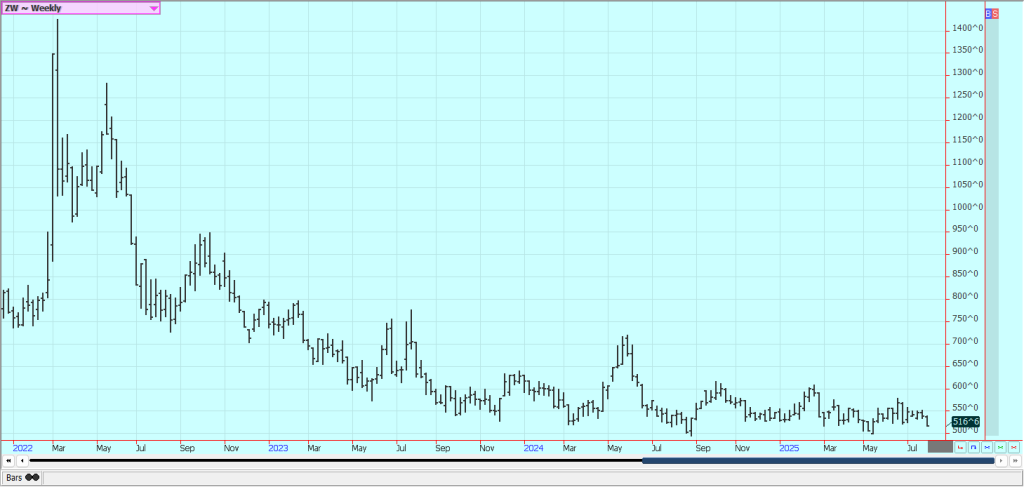

Wheat Futures

Wheat was lower last week, with Chicago the weaker market. Ideas of solid harvest progress and good yields are still around and are forcing the selling. Harvest conditions for Winter Wheat appear to be good in the US, and Spring Wheat development is currently good. Rains have been good in the northern Great Plains, but Canada has been a little too dry for best yield potential, and the northern Plains had hot and dry areas earlier in the year. Canada could still produce an average to above-average crop. Russia is still being watched for dry weather that has so far hurt yields, and Ukraine is watched for the same reason and because of the war that could destroy some fields. Russian Black Sea prices have been firming, as producers are not making sales and are looking for higher prices to offset yield losses. Southern Hemisphere crops appear to be good. The weekly export sales report showed sales within trade expectations.

Corn Futures

Corn was lower last week on what appeared to be commercial buying based on another week of strong export sales and speculative selling on widespread record crop production predictions, based on additional forecasts for improving weather for the Midwest. Cooler temperatures should return for the next few days, then a slow warming trend could develop. Most of the Midwest has seen adequate or greater precipitation, and production ideas are high. Yield estimates near or above 186 bushels per acre are frequently heard. Demand for Corn in world markets remains strong. The weekly export sales report showed that sales were at the high end of trade expectations. Oats were lower but held recent lows on the weekly charts.

Futures held the recent trading ranges as the US Dollar rallied due to the FEC decision to raise interest rates by 0.5% and create renewed fears about a recession developing here and around the world. USDA cut export demand by 75 million bushels and added the same amount to ending stocks. Ending stocks are now estimated at 1.257 billion bushels. Upside price action was hurt by another week of less export sales, with Corn hurt by a weak export sales report and lower-than-expected biofuels mandates offered by EPA last week. Corn futures showed almost no reaction to news that the Chinese government will ease lockdown restrictions on the populace in response to large protests seen in the country over the last week, with Corn finding support on speculative short covering and a weaker US Dollar. The Dollar lost about one cent on Wednesday and was about unchanged on Friday. The weekly charts show that Corn is against resistance areas, but Oats appear to be putting together a longer-term bottom.

The price action in the second half of last week has not been strong. Demand overall was weak. The US Dollar index was sharply lower last week and lost about 4,500 points, but less than a month ago calmed. Corn also found support from the Ukraine-Russia news, as Russia is now asking for major changes in the deal to permit exports from Black Sea ports. Prices were hurt in range trading. The weekly export sales report showed poor sales and was considered bearish for prices. Futures continue to hold longer-term support areas on the charts.

Ukraine apparently bombed a bridge connecting Russia and Crimea, and Russia bombed some Ukraine cities including Kiev in retaliation. It is more possible that the agreement to allow Ukraine to export grain could be cancelled, and Russia might have trouble too due to the increased tensions.

The river is low due to the dry conditions seen in most of the central parts of the US, and there are no forecasts for an improvement soon. Barge traffic has been reduced and could be stopped soon unless the river levels improve, but the improvement for now appears to be short term.

World petroleum values soared last week as OPEC and Russia moved to cut production in an effort to keep prices high. The OPEC move could create a lot of new demand for Ethanol and give the processors a nice margin. It is expected that harvest selling could limit any additional upside moves in the market.

Oats were also about unchanged for the week after moving sharply lower on Friday. Export basis levels were stronger at the Gulf but weak in the Midwest river areas due to the low river levels last week, as demand ideas were weak and as USDA caught up with weekly export sales reports. The Corn sales were not exciting to anyone in its reports released last Monday but remain in a trading range.

Corn was slightly higher last week as the US Dollar moved to new highs for the last 20 years and hurt demand ideas, and as the US harvest starts to come closer to reality. There is talk that China is about to end its zero-tolerance Covid policy and start to reopen the economy. That could mean new Corn demand for the market. This talk has not been confirmed. Corn followed Soybeans and Wheat higher, and these ideas should be confirmed later today by USDA.

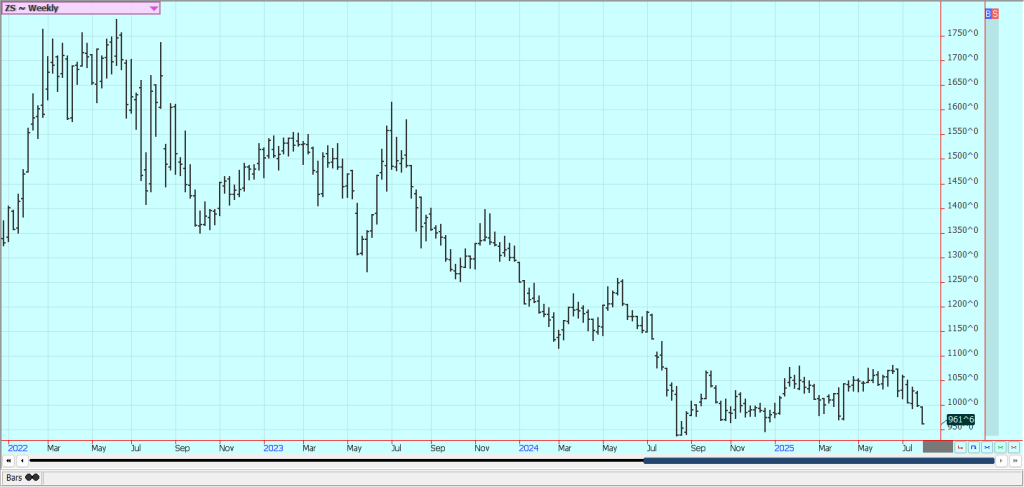

Soybeans and Soybean Meal Futures

Soybeans and the products were lower again yesterday as good growing conditions continue in the Midwest. Temperatures should turn cooler early this week and then turn a little warmer. Prices are now reported to be higher in Brazil, but China and other buyers are still buying there for political reasons. Export demand remains lower for US Soybeans, as China has been taking almost all the exports from South America. The weekly export sales report showed sales within expectations of the trade.

Rice Futures

Rice was a little lower again last week on what is reported to be fund and large speculator selling. Chart trends are still down on the daily charts. The cash market has been mostly quiet, with low bids from buyers in domestic markets and average or less export demand. New crop harvesting has started in Louisiana, with reports of good but not great yields and quality. There is more concern about the crops in Arkansas, where it has turned very hot. Milling quality of the old crop Rice remains below industry standards, and it takes more Rough Rice to create the grain for sale to stores and exporters. Rice is heading in most growing areas now, and harvest has started near the Gulf Coast.

Palm Oil and Vegetable Oils Futures

Palm Oil futures were higher last week, but the rally appears to be limited for now. There was talk that India will soon be buying a lot with festivals coming soon. Ideas that current increased production levels mean higher inventories in MPOB monthly data are still around. Canola was a little lower. Trends are mixed to up on the daily charts and on the weekly charts. The weather has generally been dry for crop development in the Prairies, with warm and dry weather still around.

Cotton Futures

Cotton was lower last week and closed near the lows of the week, as better weather is expected for the Delta and Southeast for the coming week, and crop condition reports were mostly unchanged. The weekly export sales report showed weak demand once again. The economic news on Friday of weaker-than-expected jobs data from the Commerce Dept for the recent quarter caused the stock market, crude oil, and grains to sell off. There are still reports of hotter and drier weather in West Texas. There are still ideas that growing conditions are generally good. There are still reports of better weather in Texas and into the Southeast, and demand concerns caused by the tariff wars are still around. It is starting to turn dry in West Texas again, however. Condition is rated behind last year. The monsoon in India is good, and good production there is possible.

Frozen Concentrated Orange Juice and Citrus Futures

Futures were sharply lower to limit down on both Thursday and Friday on speculative selling. Trends are down. The selling came in response to news that President Trump had decided to remove OJ from the punishing tariffs on Brazil announced earlier in the year. So, the actions by the president have created major highs and lows in the market. Development conditions are good in Florida now, with daily rounds of showers. This could change in the next few weeks, as hot weather is expected. The poor production potential for the crops comes from weather but also the greening disease that has caused many Florida producers to lose trees.

Coffee Futures

New York and London were both lower last week, with selling seen on Friday on news of employment weakness in the US. The Commerce Dept said Friday that job growth was poor in the most recent quarter. In addition, comments from the USTR that Coffee and Cocoa might be able to be imported without tariffs were viewed as negative for prices. Robusta is still more available to the market, with Brazil looking for new markets not in the US for its Coffee due to the US tariffs imposed on imports from Brazil. Arabica has been weaker recently, also on the current good weather in Brazil. Prices had been dropping for several weeks and are much more moderate than before, as supplies available to the market have ticked up. The Brazil Robusta harvest continues, and Indonesia continues to harvest. Vietnam is done with its harvest, and domestic prices were firm last week. The Brazil Arabica harvest is near the end and is expected to be less this year.

Sugar Futures

Both markets were lower last week on increasing fears about tariffs and the condition of the US economy, and despite news of less sucrose found in Brazil Sugarcane. US job growth was reported to be poor in the most recent quarter, according to the Commerce Dept. Ideas of good supplies for the market from good growing conditions for cane and beets around the world continue. The South-Center Brazil harvest is faster now amid drier conditions. Production in Center-South Brazil has also been strong. Good growing conditions are reported in India and Thailand after a fast start to the monsoon season. Good rains are still reported in Thailand. Sugar prices in Brazil are now cheap enough that at least some refiners could increase ethanol production and cut back on sugar production. However, the total recovered sugar juice has been less in Brazil this year.

Cocoa Futures

New York closed a little lower and London was slightly higher last week, as buying from more stressful weather reported for West Africa remained. News of weak employment data for the most recent quarter from the Commerce Dept and from the USTR noting that tariffs could be lifted on Cocoa and Coffee imports hurt US prices on Friday, but futures in both markets have been in a tight range all week. There are still reports of increased production potential in other countries outside of West Africa, including Asia and Central America. The market anticipates good demand and less production from Ivory Coast and Ghana. Adequate soil moisture in Ivory Coast is fostering abundant flowering on trees, signaling a healthy October-to-March main crop despite mainly below-average rain in most of the main growing regions last week. Temperatures have turned colder in West Africa, and this could be a danger to crops.

__

(Featured image by James Baltz via Unsplash)

DISCLAIMER: This article was written by a third party contributor and does not reflect the opinion of Born2Invest, its management, staff or its associates. Please review our disclaimer for more information.

This article may include forward-looking statements. These forward-looking statements generally are identified by the words “believe,” “project,” “estimate,” “become,” “plan,” “will,” and similar expressions. These forward-looking statements involve known and unknown risks as well as uncertainties, including those discussed in the following cautionary statements and elsewhere in this article and on this site. Although the Company may believe that its expectations are based on reasonable assumptions, the actual results that the Company may achieve may differ materially from any forward-looking statements, which reflect the opinions of the management of the Company only as of the date hereof. Additionally, please make sure to read these important disclosures.

Futures and options trading involves substantial risk of loss and may not be suitable for everyone. The valuation of futures and options may fluctuate and as a result, clients may lose more than their original investment. In no event should the content of this website be construed as an express or implied promise, guarantee, or implication by or from The PRICE Futures Group, Inc. that you will profit or that losses can or will be limited whatsoever.

Past performance is not indicative of future results. Information provided on this report is intended solely for informative purpose and is obtained from sources believed to be reliable. No guarantee of any kind is implied or possible where projections of future conditions are attempted.

The leverage created by trading on margin can work against you as well as for you, and losses can exceed your entire investment. Before opening an account and trading, you should seek advice from your advisors as appropriate to ensure that you understand the risks and can withstand the losses.

The TopRanked.io Weekly Digest: What’s Hot in Affiliate Marketing [LiveChat Affiliates Review]

Quick Disclosure: We’re about to tell you how LiveChat Affiliates run a top-notch affiliate program. And we really mean it....

German SMEs Face Tighter Bank Lending, Turn to Alternatives

Access to bank loans for German SMEs is tightening despite strong financing needs. About 37.8 percent face restrictive lending, driven...

Bitcoin Stalls as Geopolitical Risks and Crypto Industry Tensions Persist

Bitcoin is moving sideways near $72,000 amid ongoing Iran tensions, while ETF inflows remain strong. Quantum security debates continue. Ethereum...

Geopolitical Tensions and Trade Disruptions Reshape Global Commodities Markets

Geopolitical tensions and disrupted trade routes, especially around the Strait of Hormuz, are reshaping global commodities markets. Agriculture faces supply...

Germany Sees 413 Cannabis Cultivation Clubs Two Years After Partial Legalization

Two years after partial cannabis legalization in Germany, 413 cultivation clubs have been established nationwide. Lower Saxony leads in clubs...

|

|

|  |

|

|

-

Crypto2 weeks ago

Crypto2 weeks agoBitcoin Slides, Ethereum EEZ Emerges, Worldcoin Hits Low

-

Crypto18 hours ago

Crypto18 hours agoBitcoin Stalls as Geopolitical Risks and Crypto Industry Tensions Persist

-

Africa1 week ago

Africa1 week agoCasablanca Stock Exchange Profits Surge in 2025 as Growth Momentum Strengthens

-

Africa3 days ago

Africa3 days agoForeign Exchange Markets Walk a Tightrope Amid Geopolitical Tensions and Policy Uncertainty