Featured

Corn and Oats closed a little higher and other updates to agricultural stocks

This is a weekly update regarding the prices of several agricultural products and commodities. This has been both a good week and a bad week for several agricultural sectors across the United States and Canada. There are, as usual, many factors that go into these fluctuating stock prices, such as the trade war with China and climate change. Tracking stock price fluctuations is the key to success.

Wheat

Wheat markets were mixed as Chicago SRW and Minneapolis Spring Wheat futures closed slightly lower and Chicago HRW closed a little higher. Futures found support on Friday on talk that China was interested in buying high protein Wheat in the US.

China has already bought some US Wheat this year as Australia has big production problems again due to drought. They could easily buy more as both sides in the trade negotiations seem to be moving to a positive resolution for both sides.

The market got a positive bit of news late last week as the Bolsa de Buenos Aires cut its Wheat production estimate due to poor weather.

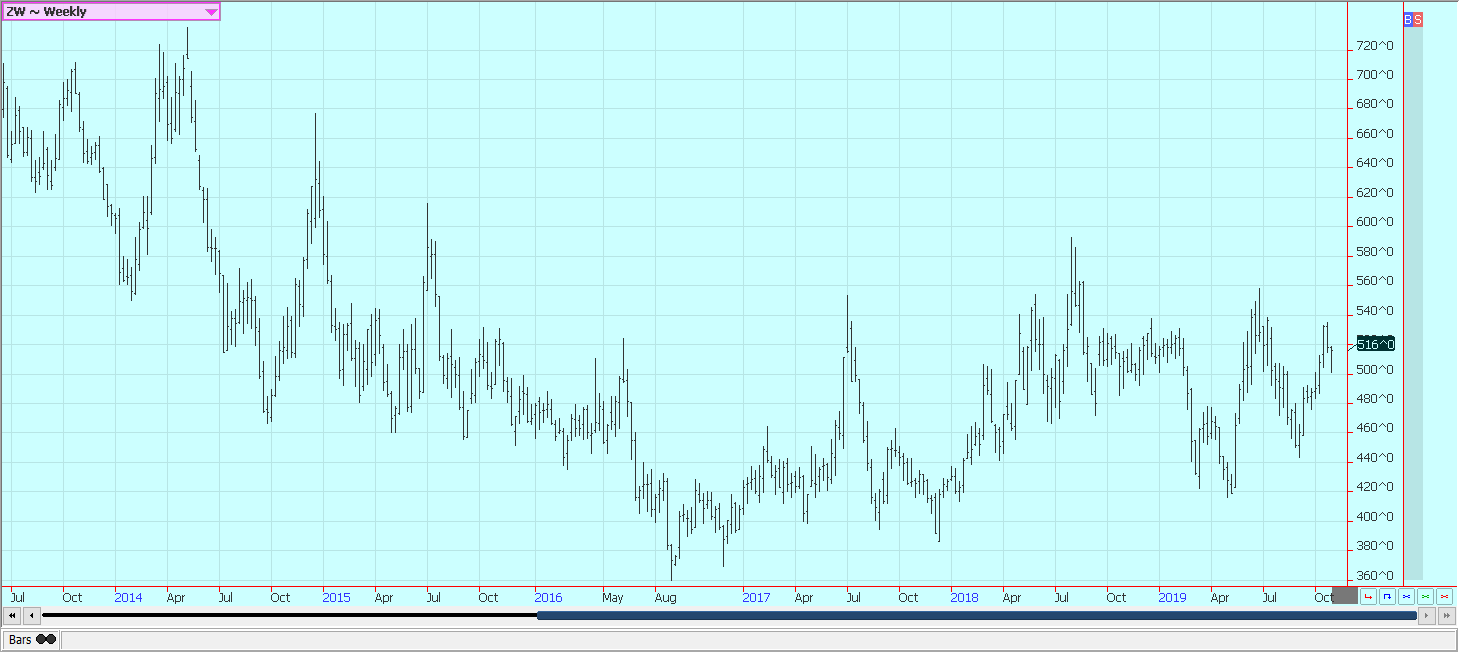

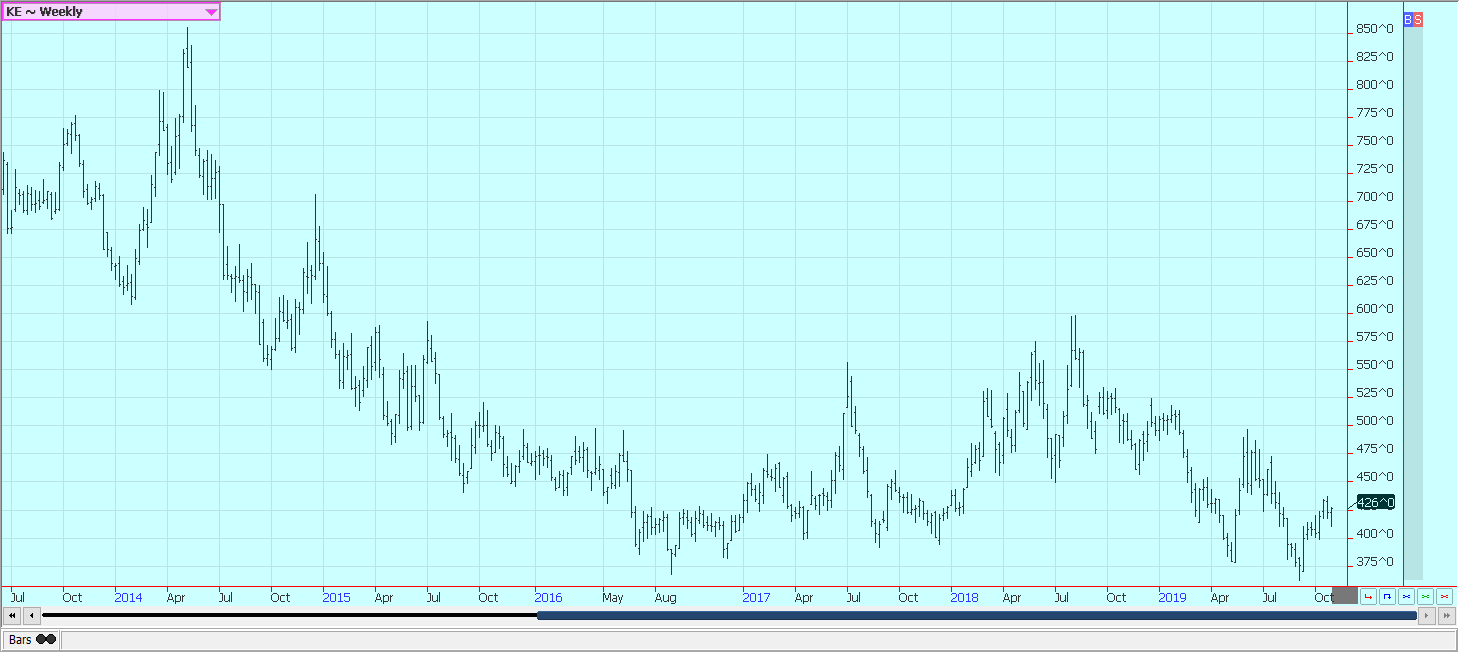

Russia continued to dominate the world market even at higher prices. US export sales were on the weaker side once again last week. The weekly charts for Chicago Winter Wheat futures suggest the market is in a short term correction but Minneapolis Spring Wheat futures show the potential for more price weakness.

US Winter crops are being planted now under uneven conditions. It has been cold but not cold enough to stop fieldwork. There was some significant snow in panhandle areas of Texas and Oklahoma and snow and rain were seen in the Midwest.

Australia is once again seeing significant yield losses as a drought in the country extends into the third year. It has been dry in parts of Argentina, especially southern areas, and Wheat production potential has started to suffer.

The weaker crops in the south have supported better demand ideas for US Wheat but the demand has yet to show. Russia and Europe continue to compete for sales and have captured most of the export volume until now.

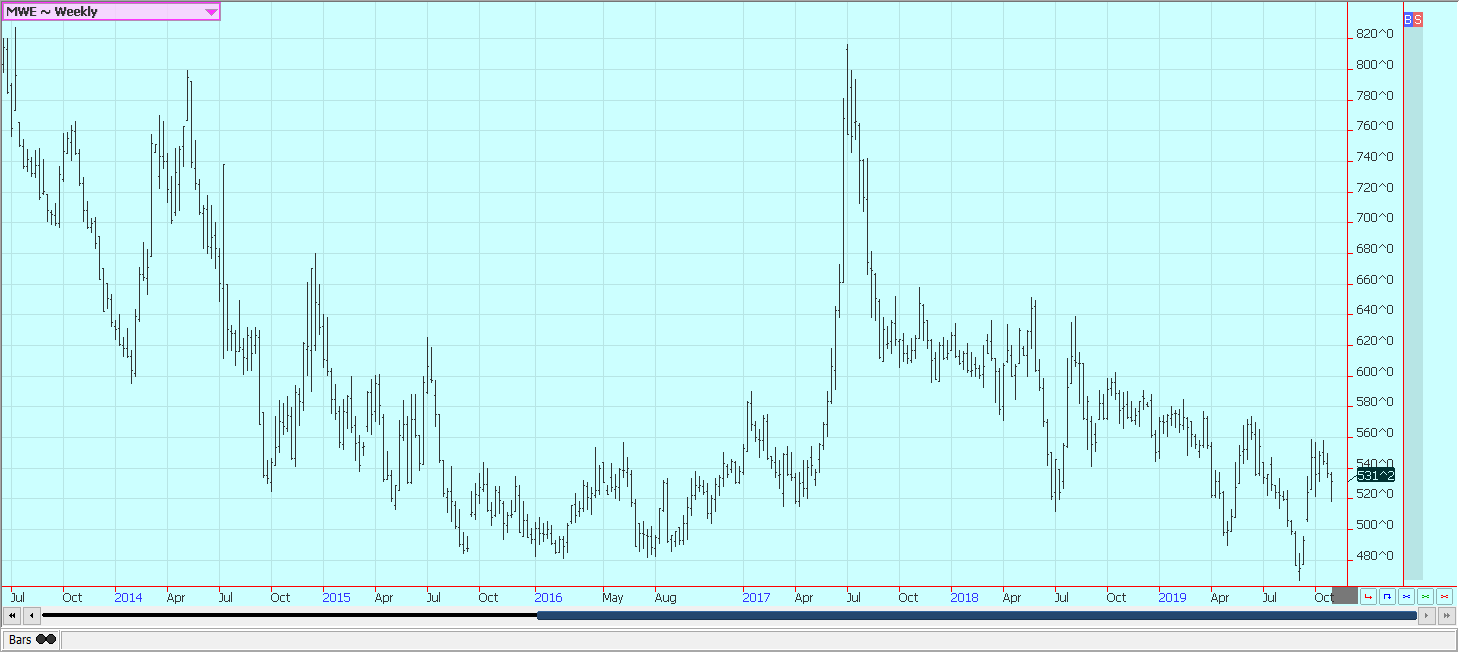

Weekly Chicago soft red winter wheat futures

Weekly Chicago hard red winter wheat futures

Weekly Minneapolis hard red spring wheat futures

Corn

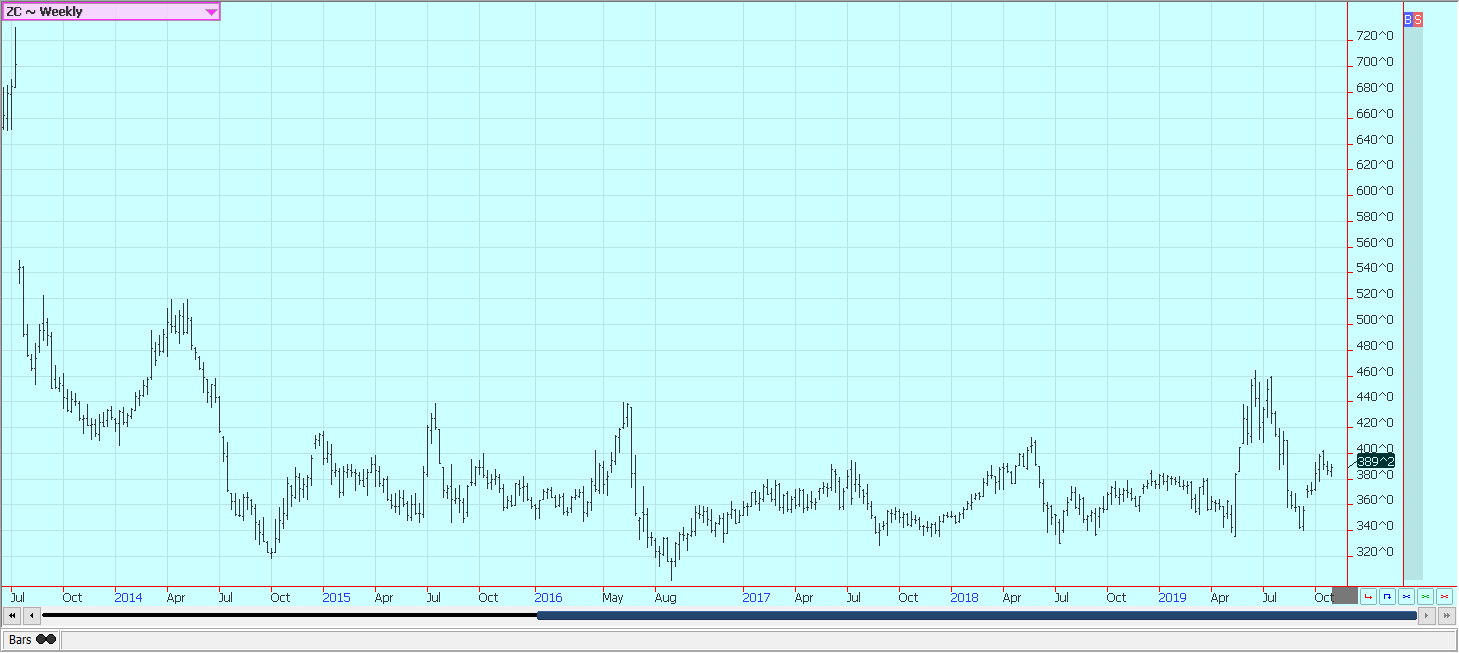

Corn and Oats closed a little higher last week. Oats look ready to rally more in the coming weeks based on the charts. Corn is still feeling harvest pressure and the lack of demand and really did not seem interested in going too far in either direction. The harvest was slow in many parts of the Midwest last week due to snow and rain.

The activity should be able to increase this week as the weather will be cold but drier. Yield data shows mixed crops but some very good results. A few farmers have reported yield potential above a year ago. These reports are mostly in western areas. Yield reports in central and eastern states have been more varied.

Some farmers are waiting for crops to dry down more before beginning the harvest. The USDA weekly export sales report showed improved demand, but not enough demand to change the narrative of a bad export pace. Export demand remains bad but ethanol demand should continue to improve as petroleum prices have been firming.

USDA will issue its latest production and supply and demand estimates on Friday and many expect the agency to cut export demand again in its projections and to increase ending stocks. Production is more difficult to estimate due to the uneven crops, but USDA might not drop yield estimates very much or it could leave them about unchanged.

Weekly corn futures:

Weekly oats futures

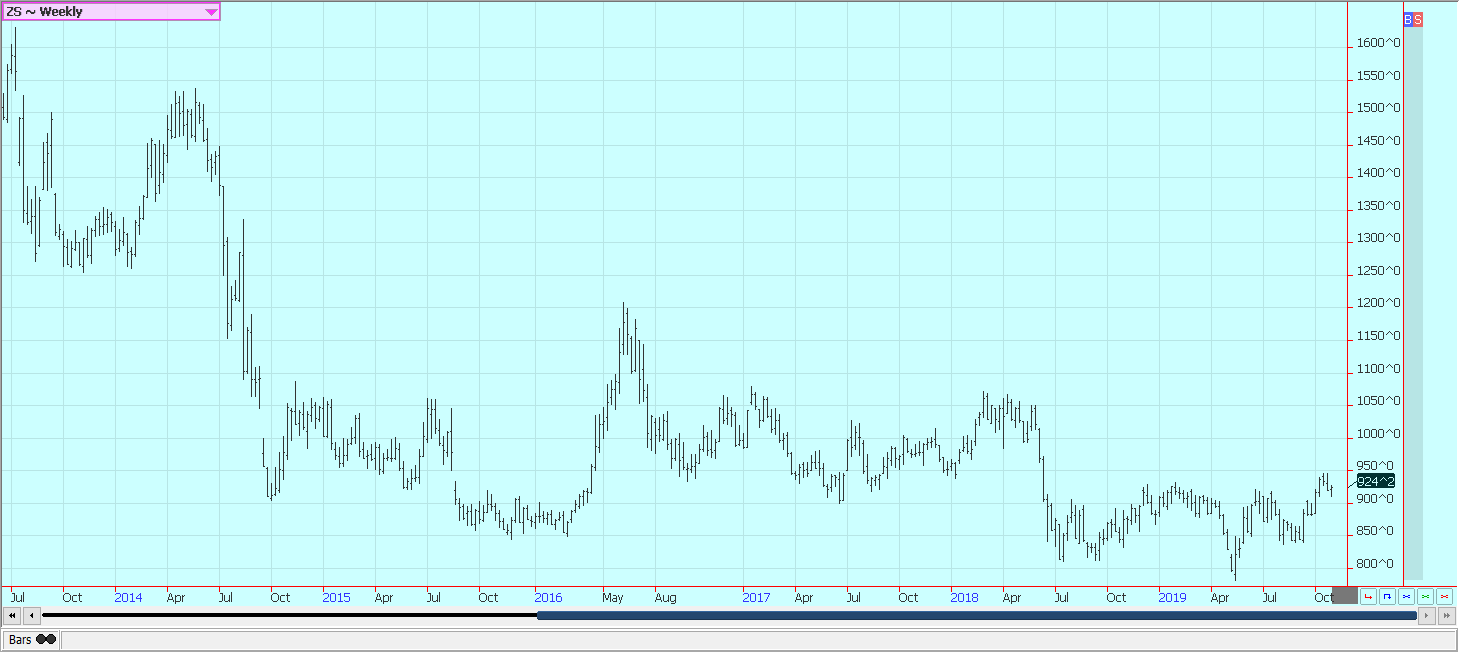

Soybeans and soybean meal

Soybeans and Soybean Oil were a little higher and Soybean Meal was slightly lower for the week. Soybeans found support from reports of good progress by both sides in the trade talks with China.

China did express some uneasiness about the US side moving the goal-posts at the end of the talks and expressed doubt that the next phases in the trade talks would go smoothly, but the chance for a trade truce and increased Chinese buying of US Agricultural goods are real.

China did, in fact, make some purchases late last week that was noted in the daily reporting system by USDA. The weekly USDA data showed that farmers were more focused on the Soybeans harvest than Corn last week and data released on Monday should show this trend as well. Yield reports show that yields are generally better in western areas than to the east with some very good yields reported in the west.

The market is keeping a closer eye on the weather in South America. It has been too dry in parts of central and northern Brazil and the planting progress has been delayed. There are forecasts for more rain to allow better planting progress appearing in the next couple of weeks.

USDA will release its next monthly supply and demand and production reports on Friday. USDA need not make any real changes in the supply and demand reports this month. Production might not change that much from last month, either.

Weekly Chicago soybeans futures:

Weekly Chicago soybean meal futures

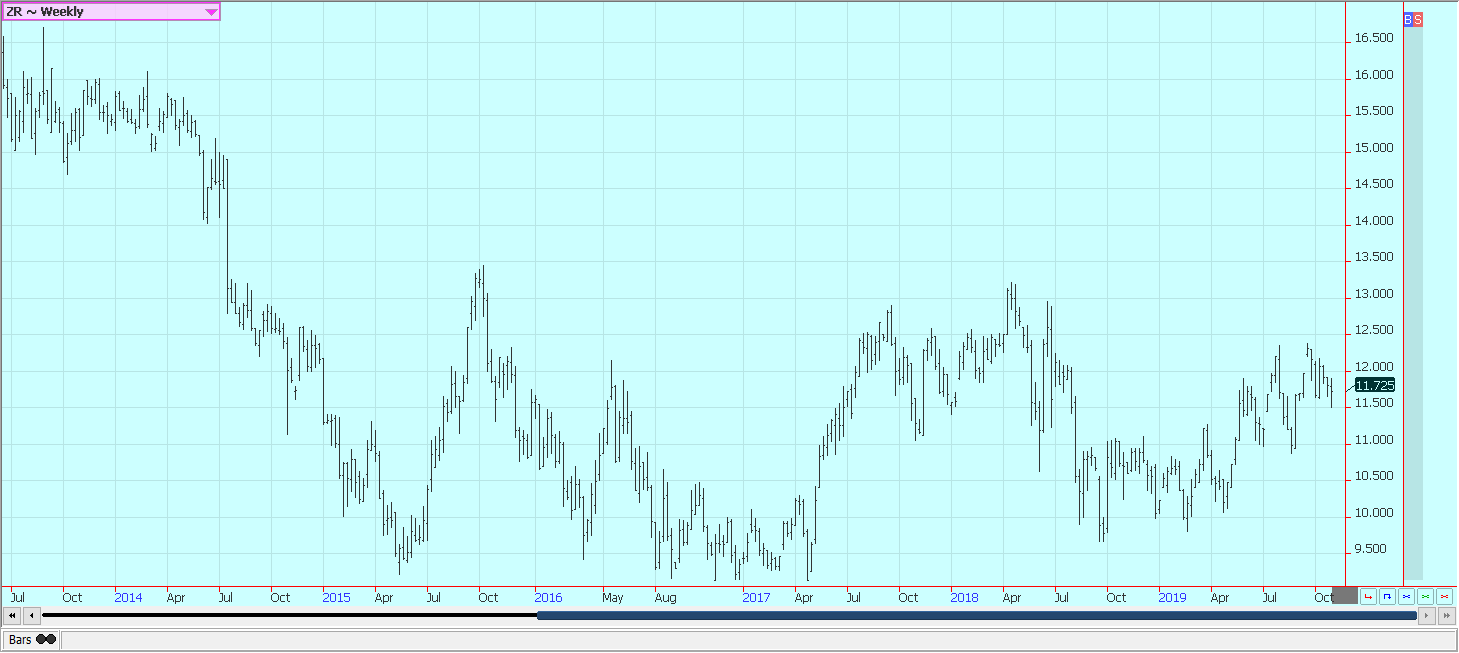

Rice

Rice was a little lower and closed in the middle of the weekly range after making new lows for the move. The harvest is mostly over in all areas and field yields appear to be generally below last year but still stronger than some analysts had expected. California is about done with its harvest with good crops reported.

Milling quality is said to be lower on later harvested Rice but was good for the early harvested Rice. Basis levels are reported to be firmer as the harvest comes to an end and Rice gets put in on-farm storage. There are ideas that not much Rice is available to the cash market right now as much of the new Rice has been put into storage.

The export sales report was strong again last week and showed a good demand for long grain. Export demand has been holding well and this gives hope for higher prices down the road. The best buyer has been in Mexico and Central America has been buying in greater volumes as well. The charts maintain a bullish longer-term outlook.

Weekly Chicago rice futures

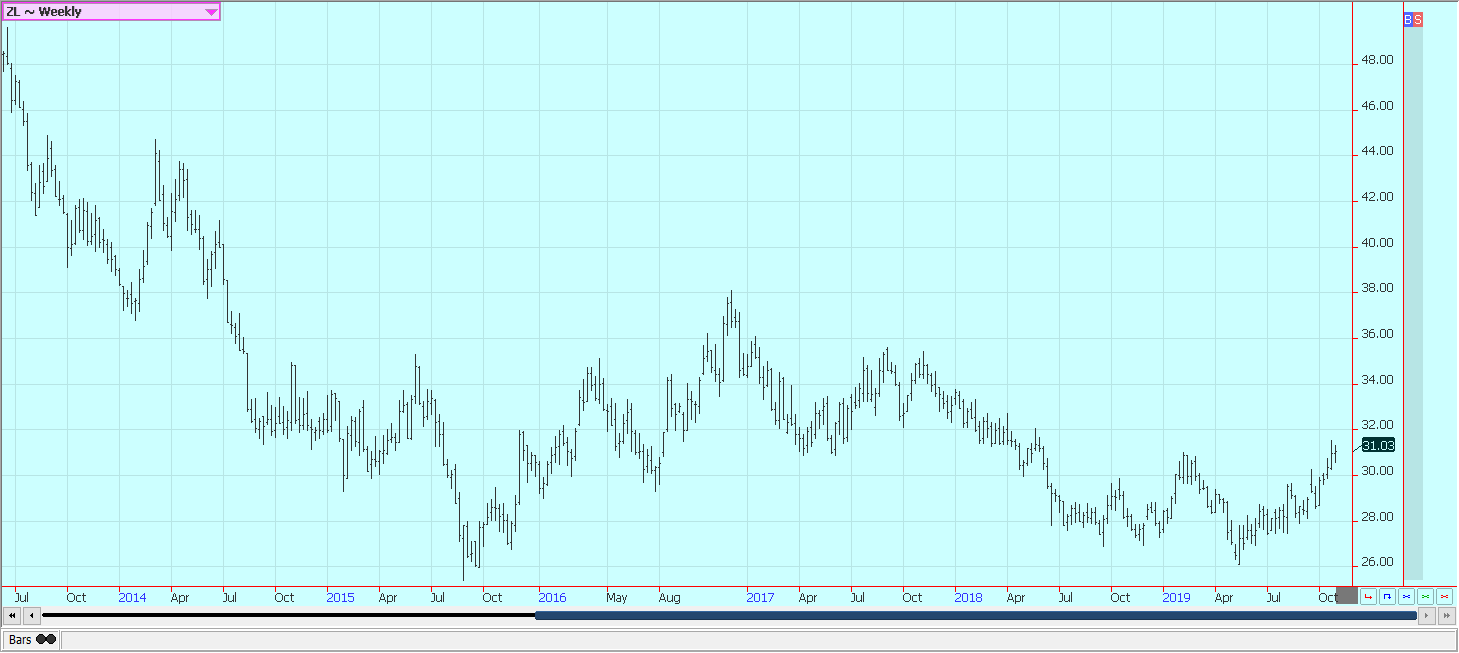

Palm oil and vegetable oils

World vegetable oils markets were mixed with Palm Oil and Soybean Oil higher and Canola a little higher. Palm Oil got stronger export news last week as the private surveyors showed that the export pace for the month is now above from the pace of the previous month.

The increase in demand has been dramatic and could continue. Soybean Oil trailed Palm Oil higher and did not have the big demand-based buying.

Trends are up in both markets but both could be a little overbought now for the short term. Palm Oil has especially rallied and could be vulnerable to a significant correction. Canola was lower last week as the harvest remained active.

Progress has been slow but producers have been active and have been delivering into the commercial system. The harvest is starting to wind down now as producers in Manitoba and Saskatchewan are over 80% complete with the Canola harvest. The weather has improved and farmers have been active sellers. Canola charts are keeping a mixed longer-term outlook.

Weekly Malaysian palm oil futures:

Weekly Chicago soybean oil futures

Weekly canola futures:

Cotton

Cotton was slightly lower and closed near the lows of the week. Some buying interest came from a talk that the US and China were close to a partial deal that would allow agricultural exports to flow to China in exchange for a truce in the tariff increases.

Both sides are reporting good progress but there has been no indication that China is interested in buying US Cotton in the short term. Cotton producers hope that China will buy some Cotton from the US but China has not been doing this.

China reported that imports from all sources were down 38% from last year in September. Export demand for the US has not been real strong as world economies are turning softer. The harvest is quite active.

Quality reports have been high until now and the crop yields appear to be in line with the USDA estimates. Western areas are also reporting good quality and yields. Good quality and yields are being reported in the Delta and Southeast.

Weekly U.S. cotton futures

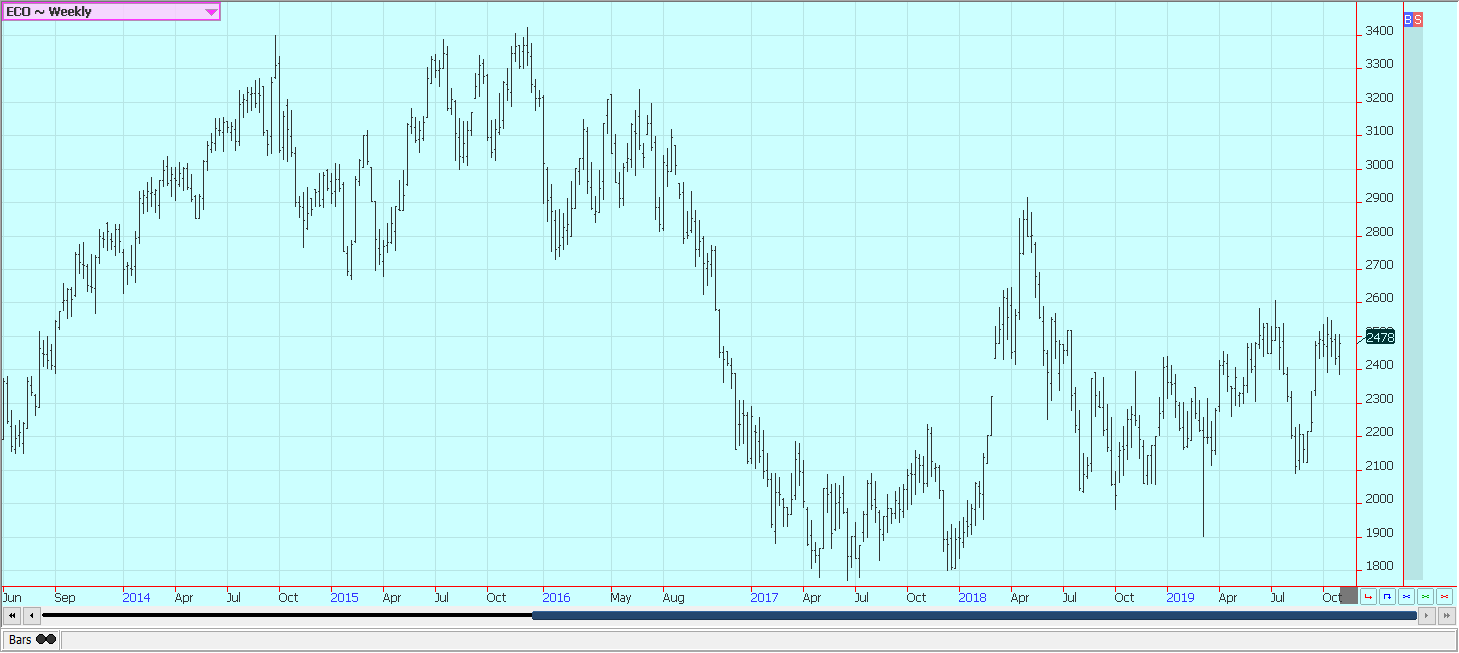

Frozen Concentrated Orange Juice and Citrus: FCOJ was lower and trends turned down on the daily and weekly charts. Futures had held the same range for months but now are starting to look for lower prices and new demand as the US crop appears to be more than big enough.

Good growing conditions and increased oranges production estimates by USDA have been bearish. The weather has been great for the trees as there have been frequent periods of showers and no hurricanes or other severe storms so far this year.

Some areas have been dry lately and irrigation is being used. Crop yields and quality should be high for Florida this year. Inventories of FCOJ in the state are high and are more than 30% above last year. Rains are falling in Brazil and trees are flowering now.

Weekly FCOJ futures

Coffee

Futures were higher on Friday and for the week in New York. London was higher for the week and unchanged on Friday. The rally is coming despite ideas of big new crop production in both Brazil and Vietnam as exporters are running tight on supplies.

The Brazilian crop is developing but some exporters say they are out of previous crop supplies to sell. The Asian harvest is underway but producers do not seem to be sold on ideas that prices are too low to provide profits.

Vietnam exports remain behind a year ago, but the market anticipates bigger offers as producers and traders will need to create new storage space and are expected to do this by selling old-crop Coffee.

Reports from Brazil indicate that flowering is off to a very good start. Rains are expected to start again in Coffee areas on Monday. Overall the Coffee areas remain in a rain deficit but have had some timely rains to start flowering.

Many now anticipate a big crop from Brazil next year despite stressful conditions earlier. Vietnam crops are thought to be big despite some uneven growing conditions this year.

Weekly New York arabica coffee futures

Weekly London robusta coffee futures

Sugar

Futures closed a little higher in New York and in London last week. Overall charts trends are trying to turn up for the medium term. Reports indicate that little is on offer from India. Thailand might also have less this year due to reduced planted area.

However, most think there is still more than enough Sugar for any demand and that India will have to sell sooner or later. Reports from India indicate that the country is seeing relatively good growing conditions and still holds large inventories from last year.

However, these supplies are apparently not moving and this could be due to less government subsidy for mills and exporters. A major storm was reported in western India and Pakistan last week that could have affected Sugar and Cotton. Reports of improving the weather in Brazil imply good crops there.

Weekly New York world raw sugar futures

Weekly London white sugar futures

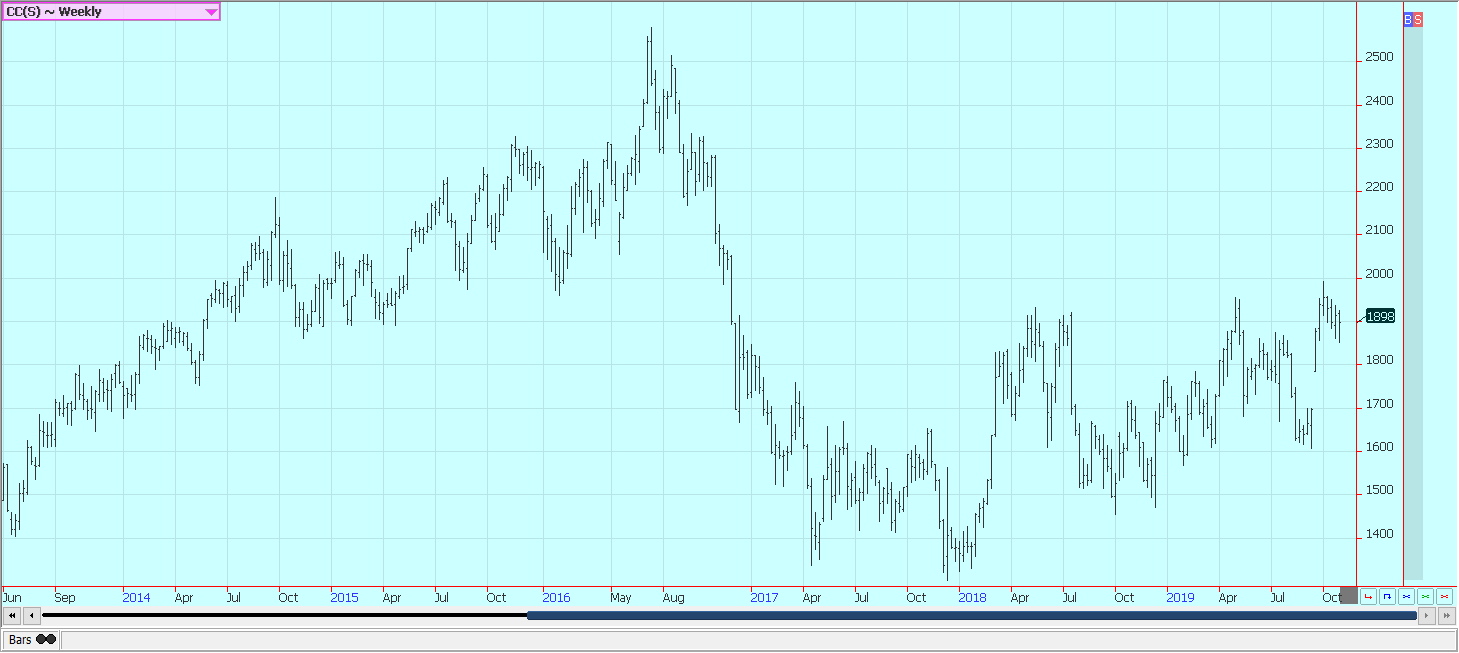

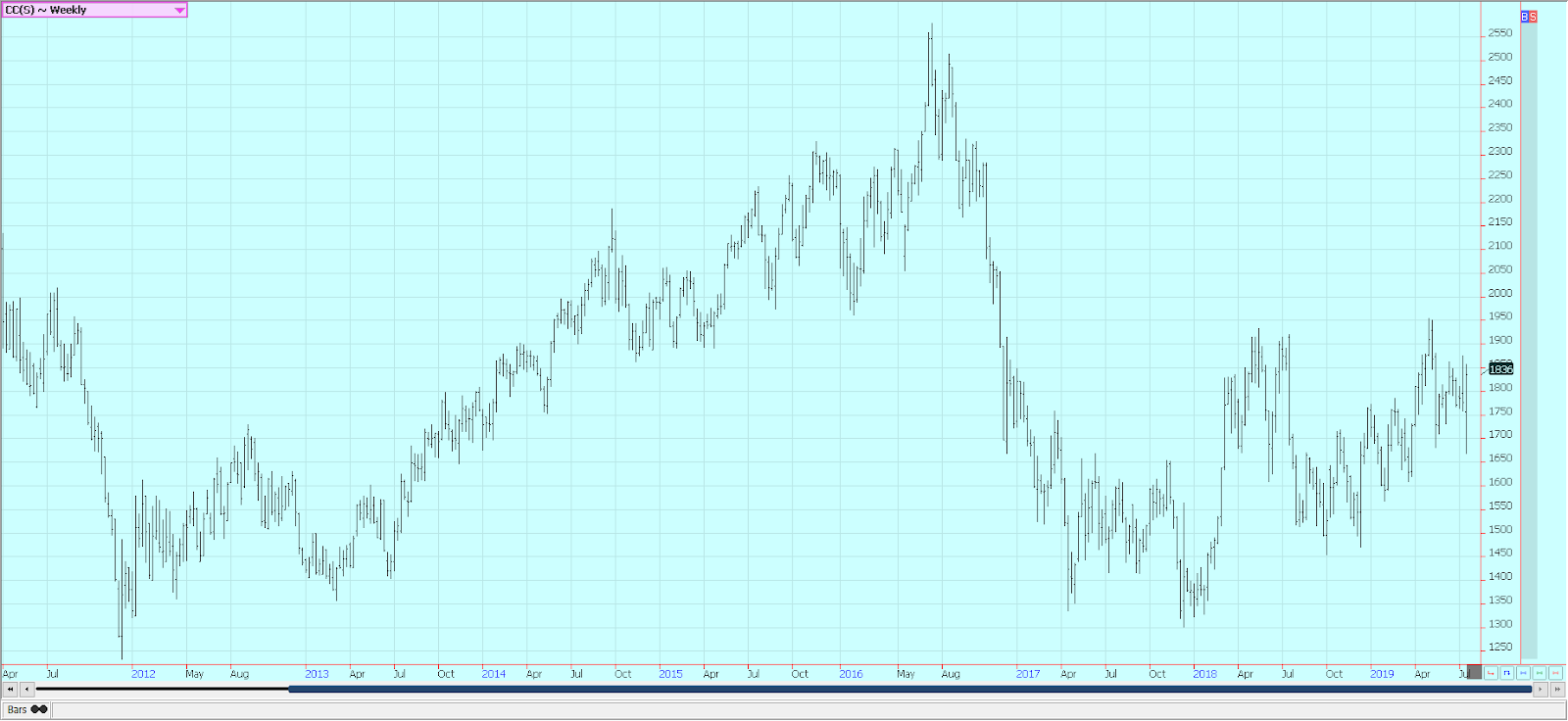

Cocoa

Futures closed higher after a big rally on Friday. The market had turned trends down on Thursday but could not follow through and bulls bought and pushed the market through the losses. Harvest is now active in West Africa and reports are that good volumes and quality are expected.

The quarterly grind data was mixed and left people wondering how good the demand for chocolate will be. Chart trends are mixed in New York but still mostly down in London. The reports from West Africa imply that a big harvest is possible in the region. Ivory Coast arrivals are strong and are above year-ago levels.

The weather in Ivory Coast has improved due to reports of frequent showers. The precipitation is a little less now so there are no real concerns about disease. Ideas are that the next crop will be very good.

Both Ivory Coast and Ghana are doing what they can do boost Cocoa prices and maintain good earnings for producers by paying a living wage differential and are looking to regulate the flow of Cocoa into the world market.

The moves could force the big Cocoa processors and grinders to pay more as they contract for Cocoa well in advance to ensure adequate supplies.

Weekly New York cocoa futures

Weekly London cocoa futures

—

(Featured image by Lorenzo Cafaro via Pixabay)

DISCLAIMER: This article was written by a third party contributor and does not reflect the opinion of Born2Invest, its management, staff or its associates. Please review our disclaimer for more information.

This article may include forward-looking statements. These forward-looking statements generally are identified by the words “believe,” “project,” “estimate,” “become,” “plan,” “will,” and similar expressions. These forward-looking statements involve known and unknown risks as well as uncertainties, including those discussed in the following cautionary statements and elsewhere in this article and on this site. Although the Company may believe that its expectations are based on reasonable assumptions, the actual results that the Company may achieve may differ materially from any forward-looking statements, which reflect the opinions of the management of the Company only as of the date hereof. Additionally, please make sure to read these important disclosures.

Anemic Labor Market and the End of Passive Money Flows

Weakened labor market is reducing passive inflows to stocks as supply and demand fall together. Immigration declines, aging population, and...

The TopRanked.io Weekly Digest: What’s Hot in Affiliate Marketing [NiftyPM Affiliate Program Review]

As any marketer (affiliate or not) can tell you, the old "it's AI-powered" line has been a real champ when...

Fes-Meknes Drives Investment Growth with Diversified Sectors and Industrial Expansion

In 2025, Morocco’s Fes-Meknes region approved 444 projects worth 17.85 billion dirhams, creating over 18,500 jobs. Investment focused on energy,...

Peru’s Crowdfunding Sector Shrinks Amid License Revocation

Peru’s securities regulator revoked Inversiones Neurona SAC’s crowdfunding license at the company’s request, following compliance checks. Previously suspended for failing...

EU Biotechnology Law Aims to Boost Innovation and Cut Trial Delays

EU Commissioner Olivér Várhelyi proposed a Biotechnology Law to boost competitiveness, cut clinical trial times, and reduce fragmentation. Measures include...

|

|

|  |

|

|

-

Africa5 days ago

Africa5 days agoModernizing Traditional Commerce in Fes-Meknes Through Financial Inclusion

-

Crypto2 weeks ago

Crypto2 weeks agoCrypto Markets React as Trump Signals Iran War End

-

Business3 days ago

Business3 days agoThe TopRanked.io Weekly Digest: What’s Hot in Affiliate Marketing [NiftyPM Affiliate Program Review]

-

Biotech1 week ago

Biotech1 week agoNovo Nordisk: Stable Growth and Defensive Biotech Stock for DACH Investors in 2026