Business

Corn and soybeans ahead of market predictions

Thanks to USDA Perspective Plantings, corn and soybeans closed higher this week. Despite a drop, cotton and sugar remain unfazed.

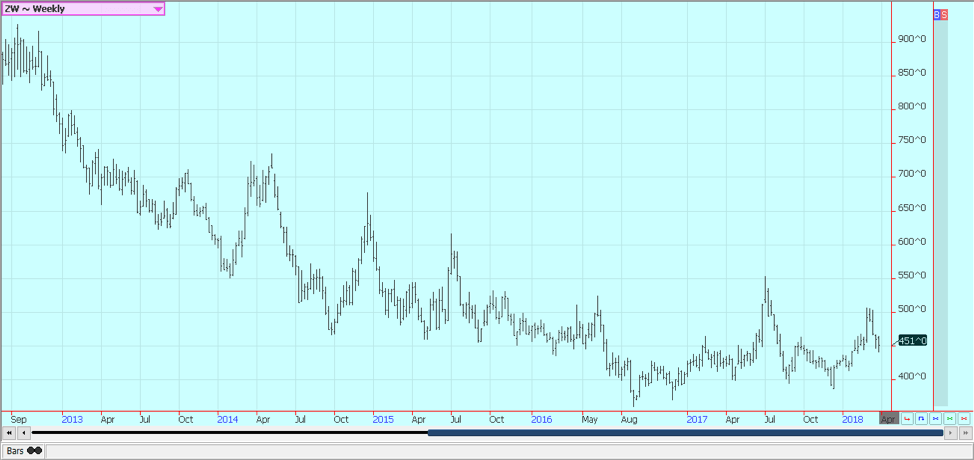

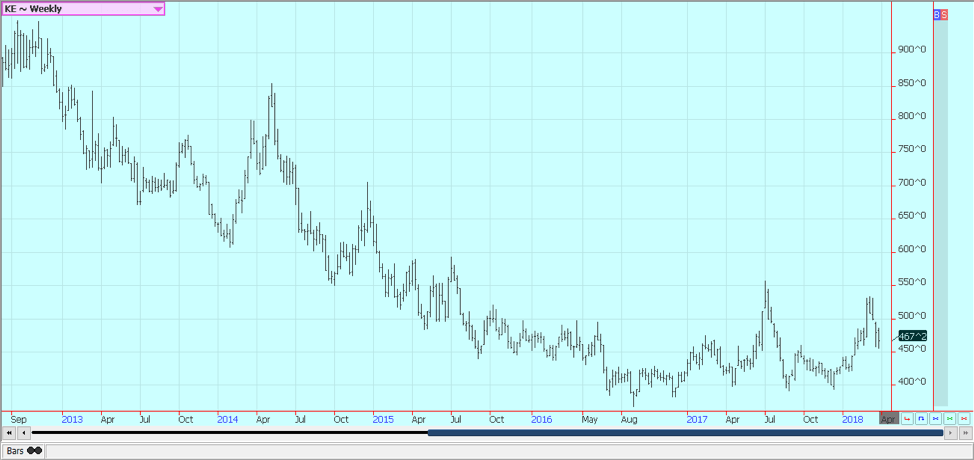

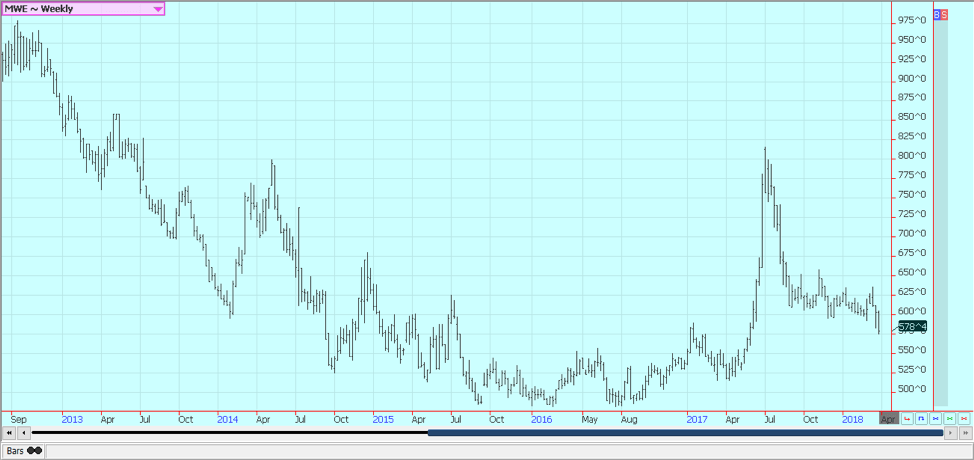

Wheat

Wheat markets were lower last week as the USDA reports were not really bullish for Wheat. The reports showed that the quarterly stocks were about as estimated by the trade.

Winter Wheat markets in Chicago closed higher on Friday, but only in sympathy with the rallies in Corn and Soybeans. Minneapolis moved lower as the Perspective Plantings reports showed that a big increase in Spring Wheat acreage was planned. That estimate was a bearish shock to the market, and chart trends in Minneapolis turned down due to that report. Forecasts still call for dry weather in Texas and Oklahoma and it is dry again in Kansas.

The weekly export sales report was improved, but cumulative sales and shipments remain behind the pace needed to make USDA targets. Lower futures prices and a weaker US Dollar have put US Wheat back into the mix for world buyers. Wheat futures are still in a weather market, and it remains very dry in the western Great Plains. La Nina conditions are still affecting the production potential for Hard Red Winter areas, but La Nina is fading, so chances for rains should start to improve. However, the systems keep missing the area and go to the north instead. A large part of the HRW crop is still rated in poor to very poor condition as crops start to come out of dormancy.

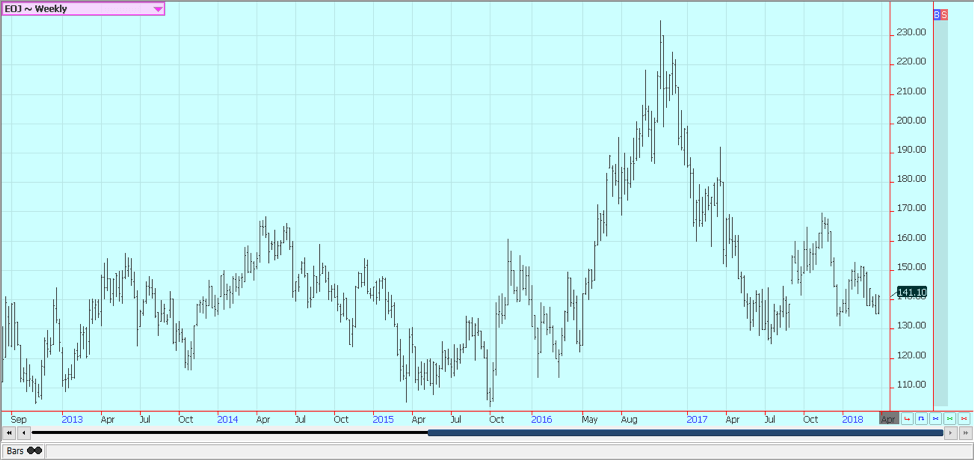

Weekly Chicago Soft Red Winter Wheat Futures © Jack Scoville

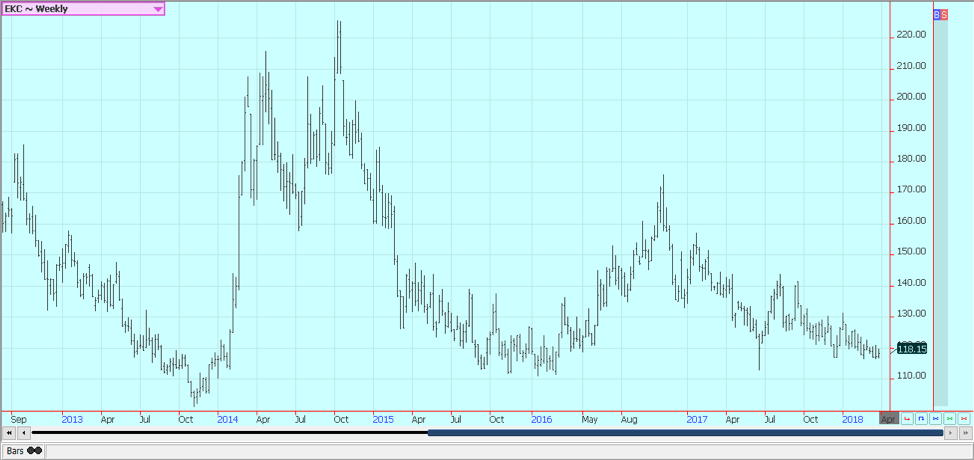

Weekly Chicago Hard Red Winter Wheat Futures © Jack Scoville

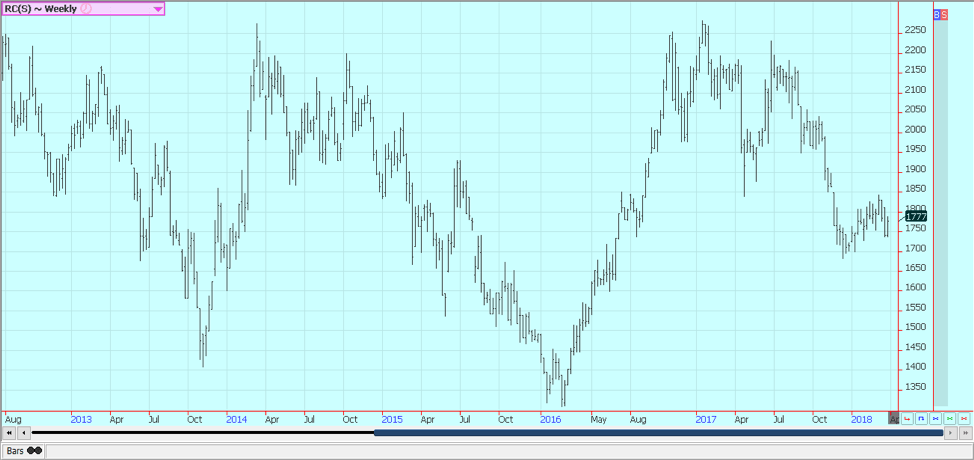

Weekly Minneapolis Hard Red Spring Wheat Futures © Jack Scoville

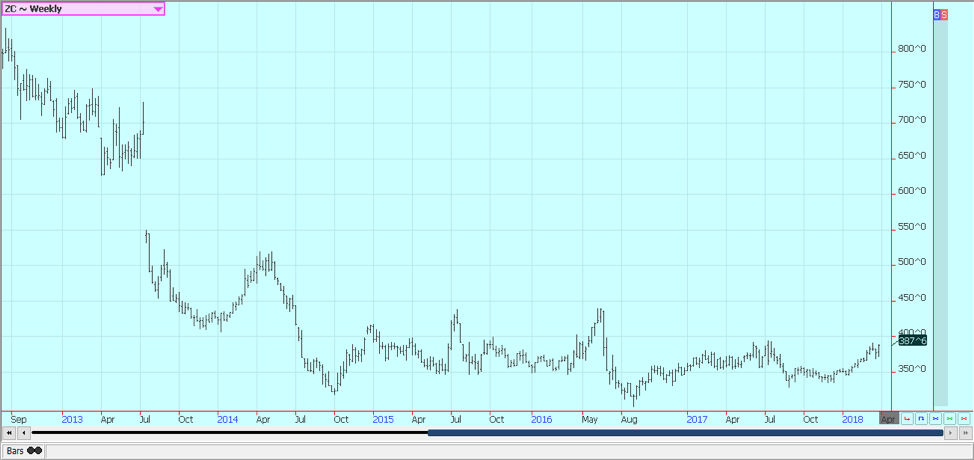

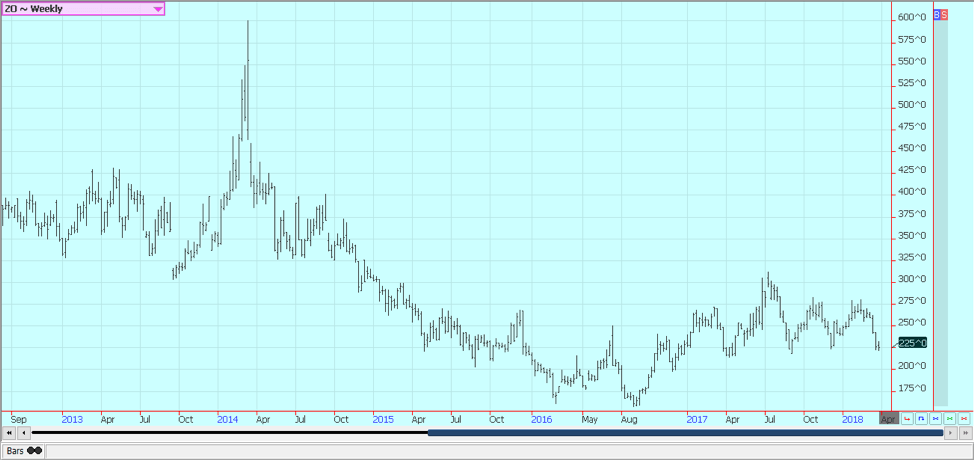

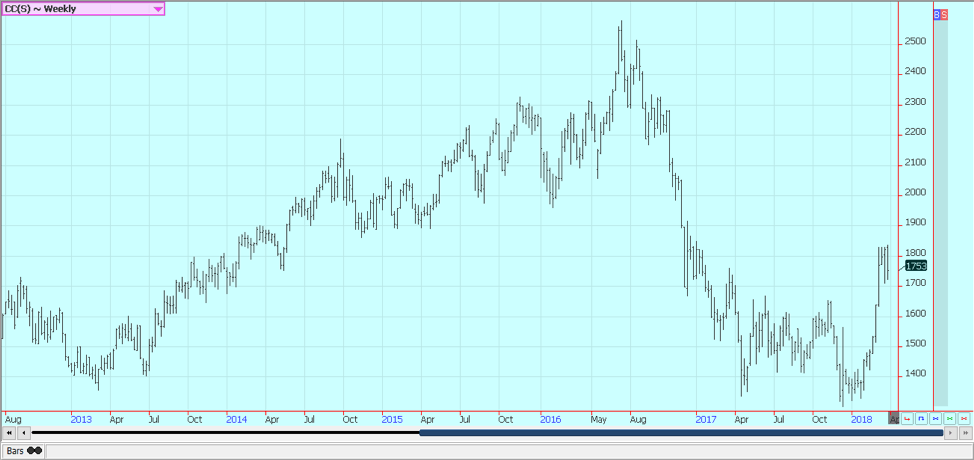

Corn

Corn closed sharply higher in reaction to the USDA Prospective Plantings report. The planned Corn acreage this year, at just over 88 million acres, was well below the average trade guess and the planted area last year. The report created massive fund buying, especially in the first hour after the release of the report.

Trends turned up with the move yesterday, and more buying is possible early this week. The report reflected producer and banker concerns about planting Corn and selling it at a profit. That means it will take much better prices to entice more Corn planted acreage. However, such acreage might not really be needed as a quick calculation shows that this planted area could produce about 14 billion bushels of Corn.

The quarterly stocks report showed ample supplies as supplies were above any trade guess at 8.888 billion bushels. However, the market focus was on the other report, and the stocks report was largely ignored. The market is looking for demand and saw another week off strong export sales.

Corn is a demand market with reasons to move higher over time, but the market is also working through big supplies still located in the US. Ethanol and export demand remain very strong. Trends turned up in Corn on the daily charts on Friday, but the weekly charts hold a more sideways to up view. Upside potential could be limited to about 395 May at this time. Many farmers are expected to make new Corn sales into the cash market on this rally.

Weekly Corn Futures © Jack Scoville

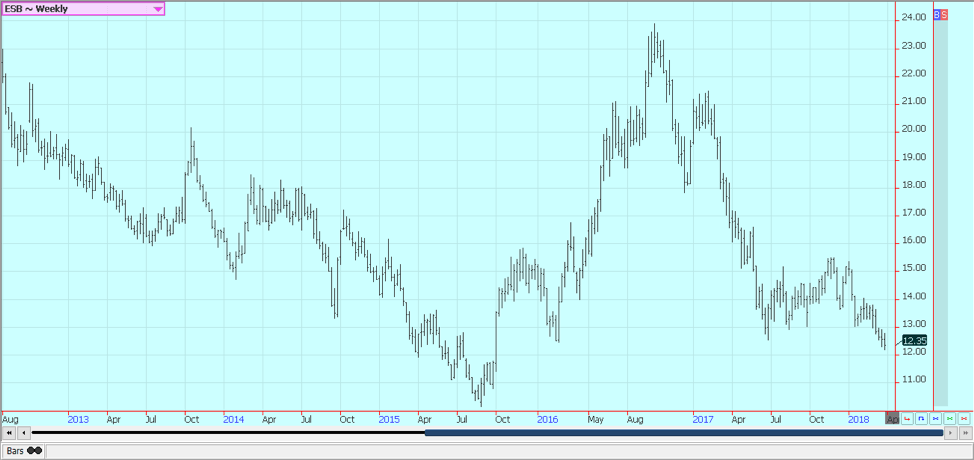

Weekly Oats Futures © Jack Scoville

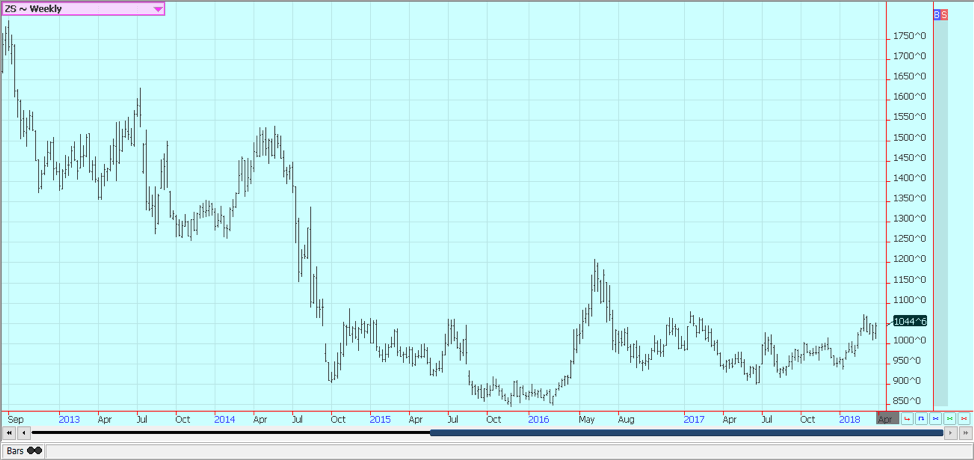

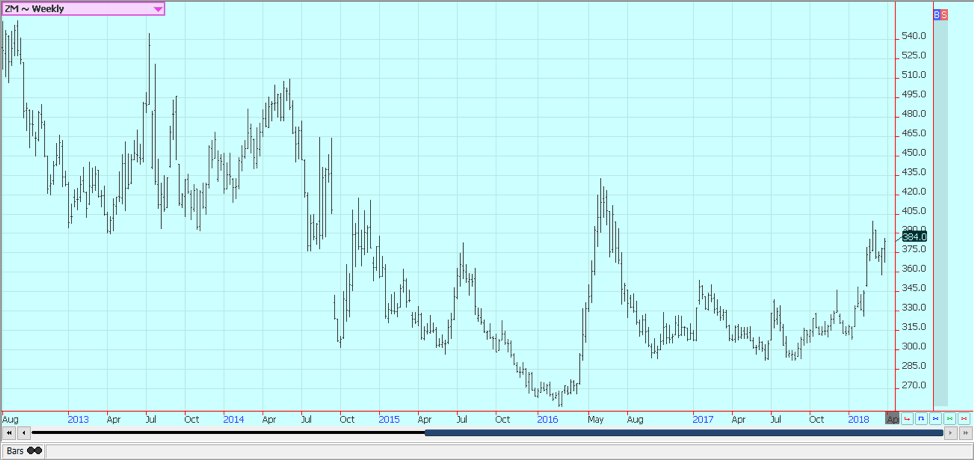

Soybeans and Soybean Meal

Soybeans and products were higher in reaction to the USDA Prospective Plantings reports. Funds became huge buyers after the reports were released, but both markets faded against some important short-term resistance areas. The weekly charts show the potential for Soybeans and Soybean Meal to move significantly higher this year.

The reports showed the potential for a much less planted area than expected by the trade. The estimates were about 2.4 million acres below the average trade guess and much below the planted of last year. The report was the bullish surprise for Friday. The quarterly stocks report showed that inventories were at the high end of expectations and not a reason to buy. But it was the plantings reports that caught the attention of the trade. It is still a weather market that is making for improved demand.

Stronger export demand for US Soybeans is expected to continue due to the drought and reduced production in Argentina and less selling from Brazil. Brazil has a big crop, but has already sold a lot of Soybeans and might not have much more export capacity for now. Argentina is dry again. Some demand is shifting to the US as Argentine cash market offers are very high priced and Brazil ports are operating at or near capacity already. Strong domestic demand has helped support Soybeans and Soybean Meal.

Weekly Chicago Soybeans Futures © Jack Scoville

Weekly Chicago Soybean Meal Futures © Jack Scoville

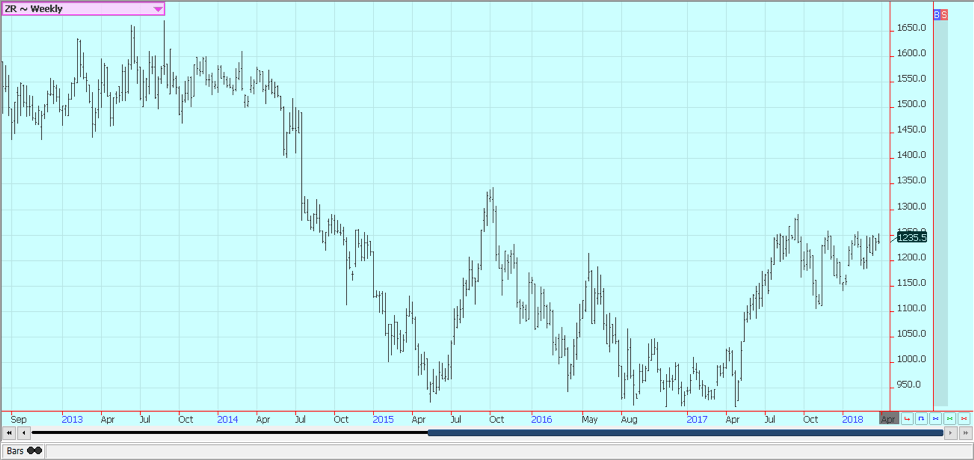

Rice

Rice was about unchanged for the week despite the USDA quarterly stocks and planted area reports. The reports showed that current supplies are tight and likely to get tighter in the next few months. In particular, the on farm stocks are now very low as most farmers have already sold. There are 83 million hundredweights of Rough Rice, with all but 12.55 million now off the farm.

The report showed that farmers intend to plant about 2.68 million acres of Rice this year. This is about 12% more than last year. The report showed that farmers will plant more Rice this year, but the increase in planted area is not considered burdensome. Indications are that producers are more willing to plant other crops instead of Rice, and early ideas of a significant increase in planted Rice area have gone away.

Farmers and bankers are worried about profitability, and planting other crops such as Soybeans or Cotton could mean better returns for some producers. Any move lower might not last long and go very deep as the fundamental situation still remains bullish in the eyes of most analysts. The US cash market bids remain generally strong amid tight supplies. The charts show that Rice once again faded from an important resistance area just above 1250 May.

Weekly Chicago Rice Futures © Jack Scoville

Palm Oil and Vegetable Oils

World vegetable oils prices were mixed to lower again last week. The market sees big supplies of Palm Oil right now in both Indonesia and Malaysia and has big questions about demand. Palm Oil is effectively shut out of the Indian market for now. Demand from China remains a question.

Many analysts now note the big Soybeans imports by China and think that China will have more than enough Soybean Oil produced from the imported Soybeans to cut import demand for all vegetable oils including Palm Oil. Malaysia has moved to impose its own export taxes of 5% starting with the month of April.

The Malaysian Ringgit has been moving higher against the US Dollar, and this has firmed up prices for Palm Oil in the world market in Dollar terms. Canola markets remain mostly in up trends as the trade is hoping for new business from any US-China tariff fight.

Deliveries to elevators have been strong due in part to forward selling earlier in the year, but new sales are hard to come by. US demand for Soybean Oil in biofuels should remain strong, and stronger export demand is anticipated due to the threat of reduced production in Argentina.

Weekly Malaysian Palm Oil Futures © Jack Scoville

Weekly Chicago Soybean Oil Futures © Jack Scoville

Weekly Canola Futures © Jack Scoville

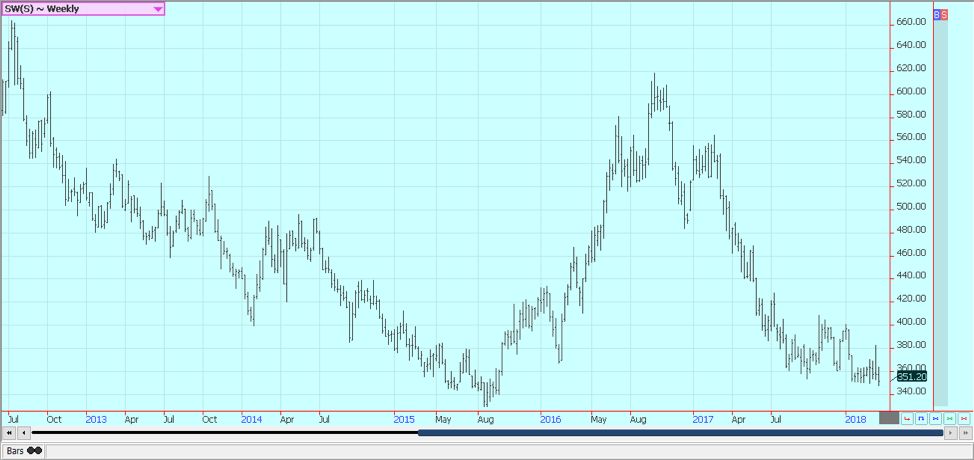

Cotton

Cotton was a little lower last week. Speculators were the best sellers, but turned buyers on Friday in end of the month and end of the quarter position squaring and despite the Perspective Plantings reports that showed increased area potential for Cotton this year. The increased area had been generally expected, but the magnitude of the projected increase was above most trade expectations. Farmers in just about all production areas plan to plant more Cotton.

It is drier in the Delta and Texas after some big rains that hit again in the second half of last week, and drier weather will be seen in the Southeast. Demand has been strong. USDA showed another week of strong export sales on Thursday, although the sales were lower than in the previous week. Export sales have been very strong and above many trade expectations at the beginning of the marketing year.

Prices overall have been much higher than most commercials had expected, but the recent carry spread weakness could be a sign that merchants have been able to get covered in the last couple of weeks. Prices could remain strong until closer to harvest, but there is a chance that the highs have been seen.

Weekly US Cotton Futures © Jack Scoville

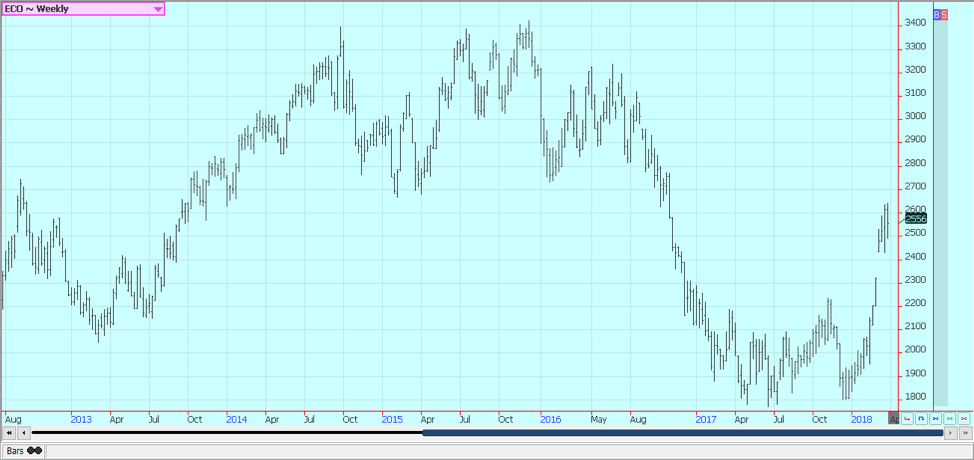

Frozen Concentrated Orange Juice and Citrus

FCOJ was unchanged on Thursday traded sideways for the week. The market is still dealing with a short crop against weak demand. The current weather is good as temperatures are warm and it is mostly dry, but some big rains are reported in northern parts of the state. The harvest is progressing well and fruit is being delivered to processors. Producers are now into the Valencia crop with the early and mid harvest completed. Florida producers are actively harvesting and performing maintenance on land and trees. Flowering has been coming to an end in the groves, and fruit is forming and developing. Irrigation is being used.

Weekly FCOJ Futures © Jack Scoville

Coffee

Futures managed to close slightly higher for the week. Trends are sideways to down on the charts. Funds and other speculators were on both sides of the market. Traders sense underlying interest in buying the market amid ideas that the bearish news is finally priced in. Origin is offering in Central America and is still finding weak differentials. Some business is getting done and exports are active.

Traders anticipate big crops from Brazil and from Vietnam this year and have seen no reason to cover the short position in a big way. New York traders are talking about good weather currently being reported in Brazil and expect another bumper crop. Robusta remains the stronger market as Vietnamese producers and merchants are not willing to sell at current prices and are willing to wait for a rally.

Weekly New York Arabica Coffee Futures © Jack Scoville

Weekly London Robusta Coffee Futures © Jack Scoville

Sugar

Futures were lower for the week. Trends are down again in both markets and both markets are making new contract lows. Traders hear about big production form the world producers and have no real reason to buy. Ideas that Sugar supplies available to the market can increase in the short term have been key to any selling. India will export up to 4.0 million tons of Sugar this year after being a net importer for the last couple of years.

The government there is reducing or eliminating export taxes in an effort to promote selling in world markets. It has a significant surplus after several years of lower production. Thailand has produced a record crop and is selling. Mills in Brazil have decided to make more Ethanol as world Crude Oil and products prices have been very strong. Brazil still has plenty of Sugar to sell even with the different refining mix.

Weekly New York World Raw Sugar Futures © Jack Scoville

Weekly London White Sugar Futures © Jack Scoville

Cocoa

Futures were mostly sideways last week. Ideas of smaller world production that has been largely sold remain part of the rally, and ideas of strong demand from processors remain the other part of the rally. Most of the trade anticipate the increased demand, and current West Africa weather is hot enough and dry enough to create production concerns.

There have been reports recently of delayed deliveries to ports. It has been hot and dry in many parts of West Africa, but showers and more seasonal temperatures have been seen in the last week to improve overall production conditions. The mid-crop harvest is starting, and wire reports indicate that some initial mid-crop harvest is underway in Nigeria. No yield reports have been seen yet. Demand has been improving and is likely to continue to improve as processing margins are said to be very strong.

Weekly New York Cocoa Futures © Jack Scoville

Weekly London Cocoa Futures © Jack Scoville

Futures and options trading involves substantial risk of loss and may not be suitable for everyone. The valuation of futures and options may fluctuate and as a result, clients may lose more than their original investment. In no event should the content of this website be construed as an express or implied promise, guarantee, or implication by or from The PRICE Futures Group, Inc. that you will profit or that losses can or will be limited whatsoever. Past performance is not indicative of future results. Information provided on this report is intended solely for informative purpose and is obtained from sources believed to be reliable. No guarantee of any kind is implied or possible where projections of future conditions are attempted.

The leverage created by trading on margin can work against you as well as for you, and losses can exceed your entire investment. Before opening an account and trading, you should seek advice from your advisors as appropriate to ensure that you understand the risks and can withstand the losses.

_

DISCLAIMER: This article expresses my own ideas and opinions. Any information I have shared are from sources that I believe to be reliable and accurate. I did not receive any financial compensation in writing this post, nor do I own any shares in any company I’ve mentioned. I encourage any reader to do their own diligent research first before making any investment decisions.

Why 2026 Could Mark a Turning Point for Sustainability

Amid geopolitical crises and climate pressures, companies must seek alternative strategies, as sustainability becomes a key driver of value. By...

Dow Jones Rebounds as Markets Shrug Off Iran Conflict

A shortened trading week saw the Dow Jones rebound from a 10 percent correction, closing between key BEV levels. Outlook...

Iran War Drives Oil Surge and Rising Financial Risks

The war continues pushing oil prices higher, with Brent above 140 while futures lag. Energy stocks weakened despite highs. Headline...

TopRanked.io Weekly Affiliate Digest: What’s Hot in Affiliate Marketing [Bovada Affiliate Program]

This week, we're mashing up 80s tech with 2020s private messaging apps. Why? Because Big Tech just dropped a big...

Euro Stablecoins Struggle to Compete with Dollar Dominance in Crypto Markets

Euro stablecoins remain marginal despite the euro’s global importance, with minimal trading volume compared to dollar rivals like USDT and...

|

|

|  |

|

|

-

Impact Investing7 days ago

Impact Investing7 days agoItalian Unlisted Banks Lag on ESG Sustainability

-

Crypto2 weeks ago

Crypto2 weeks agoThe Iran War Tests Bitcoin and Crypto Market Resilience

-

Crypto4 days ago

Crypto4 days agoEuro Stablecoins Struggle to Compete with Dollar Dominance in Crypto Markets

-

Crypto2 weeks ago

Crypto2 weeks agoCrypto Markets Volatile as Bitcoin Hovers, Solana Eyes AI Integration

You must be logged in to post a comment Login