Markets

Cotton Market Weakens Amid Demand Concerns and Bearish Trends

Cotton prices fell last week with no bullish catalysts and downward trends on daily and weekly charts. Demand outlook is pressured by a weakening global economy, especially in the US, and shifting tariffs that discourage buying. USDA data showed lower production, steady demand, and reduced ending stocks, offering limited support to the market overall recently.

Wheat: Wheat closed a little lower last week on the weather that was cold, has now moderated to above normal temperatures. Temperatures were cold enough a week ago to promote Winterkill, but most areas got some snow cover to protect crops now. This was not true when the cold came a couple of weeks ago. The snow came after the cold weather was a factor.

Concerns on the condition of the Winter Wheat crops moving forward are growing as there is little snow cover and some very cold temperatures are occurring that could have created Winterkill over the weekend again. Many parts of the Great Plains are too dry for best yield potential.

Weekly Chicago Soft Red Winter Wheat Futures

Weekly Kansas City Hard Red Winter Wheat Futures

Weekly Minneapolis Hard Red Spring Wheat Futures

Unavaiable today

Corn: Corn was higher last week. Trends are mixed but are trying to turn up due to excessive supplies as seen in the recent USDA reports after trending higher in recent weeks to the recent demand based rally and after production was increased in the annual report. USDA increased production in the annual reports and the increased supplies have made it hard for prices to rally at all despite reports of strong demand. Temperatures in the Midwest should average above normal next week. Oats were lower and trends are mixed.

Weekly Corn Futures

Weekly Oats Futures

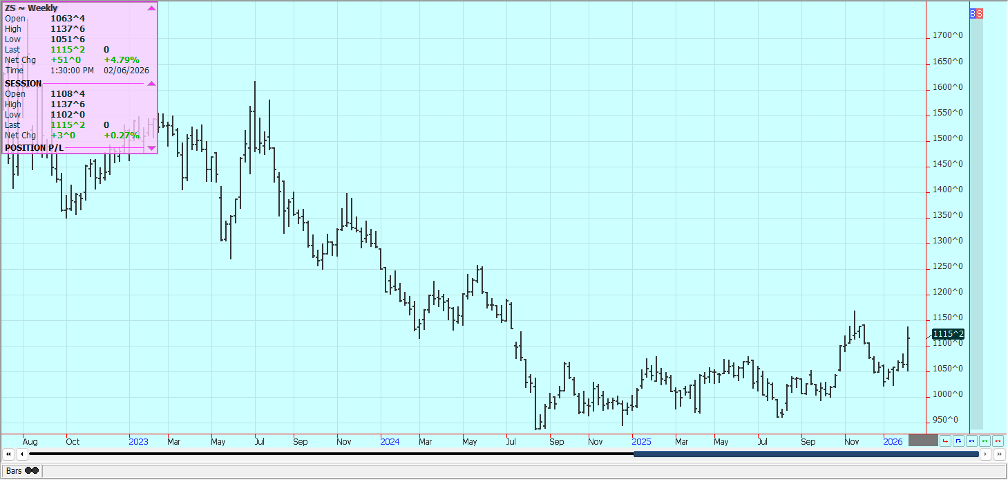

Soybeans and Soybean Meal: Soybeans and the products were higher last week on mostly speculative buying after President Trump indicated that he is asking the Chinese to buy another 8 million tons of US Soybeans. The Chinese have not commented on the Trump statements. There are ideas of additional Chinese demand soon but it will be up to the government to buy as US Soybeans are too high priced for commercial demand from China or almost anywhere else.

The tariff wars between the two countries add another layer of cost onto the Soybeans. It still seems that the market is now more concerned about big supplies coming soon from South America with the Soybeans harvest there now underway. Brazil Soybeans are now 10% harvested. The South American crops are expected to be very large and large South American crops will pressure world prices. Temperatures will average above normal in the Midwest next week.

Weekly Chicago Soybeans Futures

Weekly Chicago Soybean Meal Futures

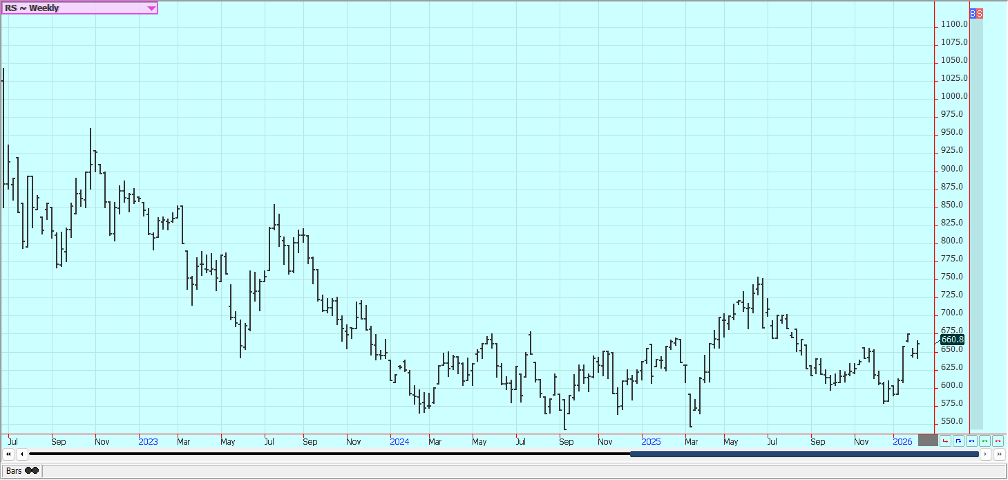

Rice: Rice was higher last week and trends are still up. Futures have been recovering for the last month after a very long and sizable down move. Traders anticipate less production this year in the US and around the world due to low prices. Weaker world prices are expected by the FAO in the coming year. Asian Rice prices are under pressure now due to a weaker Indian Rupee that forced costs for Indian Rice lower. Trends are up in the market but demand remains moderate for US Rice.

Weekly Chicago Rice Futures

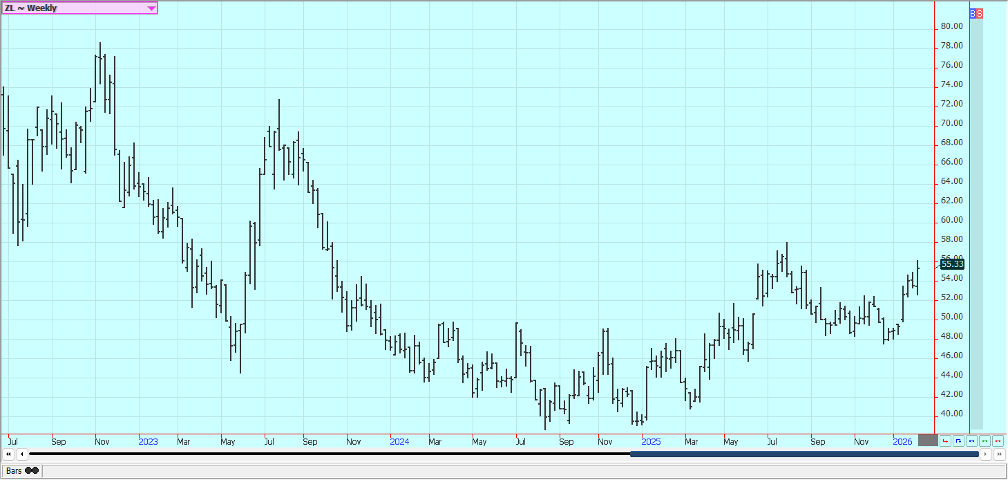

Palm Oil and Vegetable Oils: Palm Oil futures were lower last week. Ideas of increasing seasonal demand and on ideas that Palm Oil is relatively cheap in the world market are still around. Demand ideas are in a state of flux right now with some looking for weaker demand and other looking for improved demand. Production is expected to drop in the short term.

Canola was higher last week on mostly speculative buying and strong demand ideas. Canada and China reached agreement on a new trade deal which is expected to result in part in new sales of Canola to China There are ideas of a big Soybeans harvest coming from South America.

Weekly Malaysian Palm Oil Futures:

Weekly Chicago Soybean Oil Futures

Weekly Canola Futures

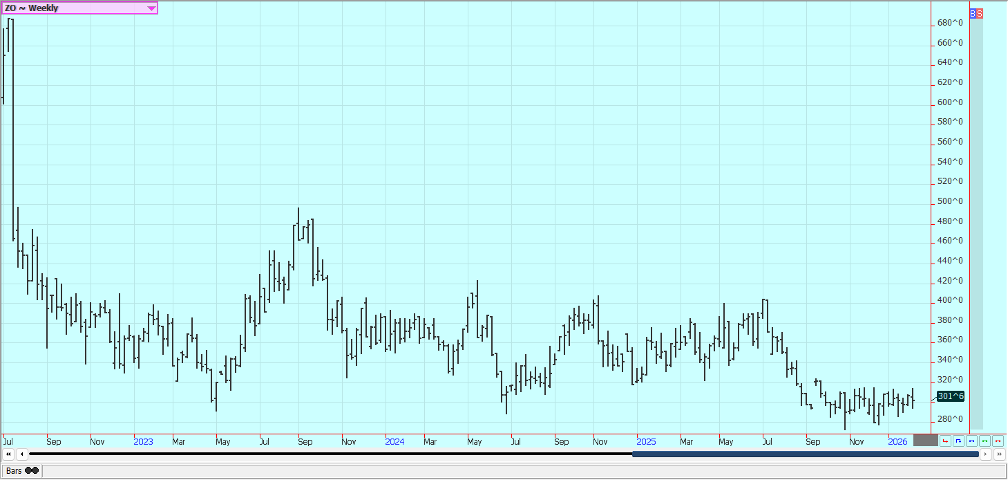

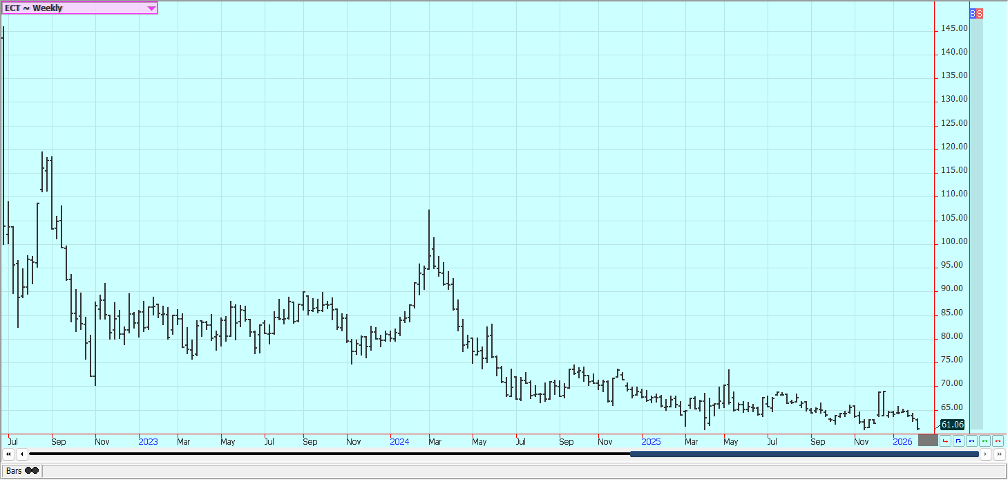

Cotton: Cotton was lower last week as there does not appear to be any bullish news for the market coming soon. Trends are down on the daily and weekly charts. There are cotton demand concerns moving forward on weak world economy ideas led by the US weakened economy and demands in world forums.

Tariffs on other nations that change all the time were creating an atmosphere not conducive for new cotton demand. The USDA reports released a couple of weeks ago showed less cotton production and unchanged demand. Ending stocks were less.

Weekly US Cotton Futures

Frozen Concentrated Orange Juice and Citrus: Futures lower last week and closed on a weak note as the Florida harvest is active and the weather remains benign for harvest progress as conditions are mostly dry. Weather for the next crop was very cold in January and into early February and some damage to trees and fruit is possible.

Chart trends are down. The cold and dry Winter weather has created more ideas of some crop losses. Traders are worried about demand even with overall low prices. The weather is considered good for production in Brazil and Mexico. Scattered showers are reported in Brazil.

Weekly FCOJ Futures

Coffee: Both markets closed lower last week on good weather for growing and harvesting seen in Brazil and Vietnam. The trends are down in New York and in London on the daily and weekly charts. There are still reports of increasing harvest sales from Vietnam as the new harvest is active. There are reports of very good conditions in Brazil and a large crop is forecast.

Most farmers are holding for better prices but seem to have lost that battle for now . Scattered showers are being reported now to improve tree condition in Brazil. Mexico is in good condition, as is Central America. Vietnam has scattered showers lately and conditions there are called good. Vietnamese producers are selling new crop Coffee.

Weekly New York Arabica Coffee Futures

Weekly London Robusta Coffee Futures

Sugar: New York and London were a little lower last week and trends are down on the daily and weekly charts. There are good supplies for the market from good growing conditions for cane and beets around the world continue. The prospect of a big global surplus in the 2025/26 season was keeping the market on the defensive with a rise in production in India and Thailand set to increase supplies especially for White Sugar while global consumption is expected to remain steady. Indian crops are seeing good finishing weather and production ideas have been increasing

Weekly New York World Raw Sugar Futures

Weekly London White Sugar Futures

Cocoa: New York and London closed a little higher last week, with London the stronger market. Short term trends are still mixed to down. A big main crop harvest is anticipated in West Africa and rains have been positive for crops lately. Mostly dry conditions in Ivory Coast’s cocoa-growing regions are re-ported now. There are still reports of increased production potential in other countries outside of West Africa, including Asia and Central America.

The market feels that there is less demand and the lack of demand is expected to continue. Weak demand has led to a build-up on unsold supplies in both Ivory Coast and Ghana, while the prospect of another global surplus in 2026/27 are real. Cocoa demand has fallen sharply after prices nearly tripled in 2024, prompting chocolate makers to reformulate ingredi-ents and shrink the size of their bars.

Weekly New York Cocoa Futures

Weekly London Cocoa Futures

__

(Featured image by Sze Yin Chan via Unsplash)

DISCLAIMER: This article was written by a third party contributor and does not reflect the opinion of Born2Invest, its management, staff or its associates. Please review our disclaimer for more information.

This article may include forward-looking statements. These forward-looking statements generally are identified by the words “believe,” “project,” “estimate,” “become,” “plan,” “will,” and similar expressions, including with regards to potential earnings in the Empire Flippers affiliate program. These forward-looking statements involve known and unknown risks as well as uncertainties, including those discussed in the following cautionary statements and elsewhere in this article and on this site. Although the Company may believe that its expectations are based on reasonable assumptions, the actual results that the Company may achieve may differ materially from any forward-looking statements, which reflect the opinions of the management of the Company only as of the date hereof. Additionally, please make sure to read these important disclosures.

Futures and options trading involves substantial risk of loss and may not be suitable for everyone. The valuation of futures and options may fluctuate and as a result, clients may lose more than their original investment. In no event should the content of this website be construed as an express or implied promise, guarantee, or implication by or from The PRICE Futures Group, Inc. that you will profit or that losses can or will be limited whatsoever.

Past performance is not indicative of future results. Information provided on this report is intended solely for informative purpose and is obtained from sources believed to be reliable. No guarantee of any kind is implied or possible where projections of future conditions are attempted. The leverage created by trading on margin can work against you as well as for you, and losses can exceed your entire investment. Before opening an account and trading, you should seek advice from your advisors as appropriate to ensure that you understand the risks and can withstand the losses.

ECSP Crowdfunding vs. eWpG Bonds: Overcoming SME Financing Limits

The ECSP Regulation limits annual crowdfunding per project promoter to €5 million, requiring a full prospectus for higher amounts, which delays...

Germany’s Cannabis Reform Shows Limited Risks but Calls for Regulatory Adjustments

Two years after Germany’s partial cannabis legalization, an evaluation finds no significant rise in consumption and some reduction in the...

Ortus Secures €97M Green Loan to Expand Solar Portfolio in Italy

Ortus Power Resources Italy secured a €97 million green, non-recourse loan to refinance 23 MW of operating solar plants and...

Foreign Exchange Markets Walk a Tightrope Amid Geopolitical Tensions and Policy Uncertainty

Foreign exchange markets remain fragile amid geopolitical tensions, monetary shifts, and persistent volatility. The dollar stayed a safe haven without...

Crypto Holds Steady as Tensions Rise and Regulatory Concerns Grow

Crypto markets remained cautious as a US ultimatum to Iran nears expiry. Bitcoin and Ethereum traded sideways despite strong ETF...

|

|

|  |

|

|

-

Business5 days ago

Business5 days agoTopRanked.io Weekly Affiliate Digest: What’s Hot in Affiliate Marketing [Bovada Affiliate Program]

-

Biotech2 weeks ago

Biotech2 weeks agoNHS Funds Breakthrough CAR-T Therapy Breyanzi for Lymphoma Treatment in Spain

-

Crowdfunding1 hour ago

Crowdfunding1 hour agoECSP Crowdfunding vs. eWpG Bonds: Overcoming SME Financing Limits

-

Fintech1 week ago

Fintech1 week agoCrypto Lending Hits $30 Billion, Becomes Key DeFi Pillar