Markets

Cotton Prices Firm as Demand Lags and Global Production Outlook Improves

Cotton prices rose last week and may be forming a daily chart low. Demand remains quiet despite positive but dated export sales. Farmers are holding back due to low prices, and limited new Chinese buying continues to pressure the market. U.S. harvest is mostly complete with good yields, and India’s strong monsoon supports solid production prospects.

Wheat: Wheat closed a little higher in Chicago and KC last week. The weekly charts show that trends are in a short term range. World prices turned weaker last week due to reports of strong production in exporter countries. Production has been good in northern hemisphere countries. Southern hemisphere crops appear to be very good. Demand has been weaker for various origins including Russia.

Weekly Chicago Soft Red Winter Wheat Futures

Weekly Kansas City Hard Red Winter Wheat Futures

Weekly Minneapolis Hard Red Spring Wheat Futures

Unavaiable today

Corn: Corn was higher last week. Ideas are that demand is less now due to increased competition in the world market. Trends are mixed in the market. The harvest is almost over in all areas of the Midwest. There are ideas that US production might not be super strong due to disease such as rust to offset the demand losses. Temperatures should average below normal this week and there are forecasts for some rain early this week. Oats were lower, but trends are turning up anyway.

Weekly Corn Futures

Weekly Oats Futures

Soybeans and Soybean Meal: Soybeans and Soybean Oil were higher last week, but Soybean Meal closed a little lower. The White House said it was talking to Chin about Soybeans again and that a deal is within reach again. A deal had been announced several weeks ago for massive Soybeans purchases by China but apparently as of now it was not real.

The US will have to compete with South America for sales in a diminishing Chinese market and US prices are currently too high to complete many new sales. The Chinese hog herd is being reduced and this means less demand for Soybeans and Soybean Meal. Temperatures will average below normal in the Midwest this week.

Weekly Chicago Soybeans Futures

Weekly Chicago Soybean Meal Futures

Rice: Rice was lower last week as the selling in this market continues unabated. Ideas are that the market is too cheap and that farmers have sold what needs to be sold for now. The recent selling has been to be relentless and appears tied to the weaker prices in Asia and especially India. Trends are down in the market. The harvest is over in the delta and Mid South.

California is about done with its harvest. Yields and quality are mixed, but quality appears better than a year ago. The cash market has been slow with low bids from buyers in domestic markets and average or less export demand. The charts show that futures are in a short term trading range.

Weekly Chicago Rice Futures

Palm Oil and Vegetable Oils: Palm Oil futures were a little higher last week despite fears of increasing production and weakening demand. There are still Indonesian plans to increase the use of Palm Oil in biofuels blends. There are still ideas of increasing production. The market sentiment overall is turning bearish on ideas of increasing stocks to the market and on some concerns about demand Canola was higher and moved back into the heart of the recent trading range on the daily charts. Trends are still mixed on the daily charts but up on the weekly charts.

Weekly Malaysian Palm Oil Futures:

Weekly Chicago Soybean Oil Futures

Weekly Canola Futures

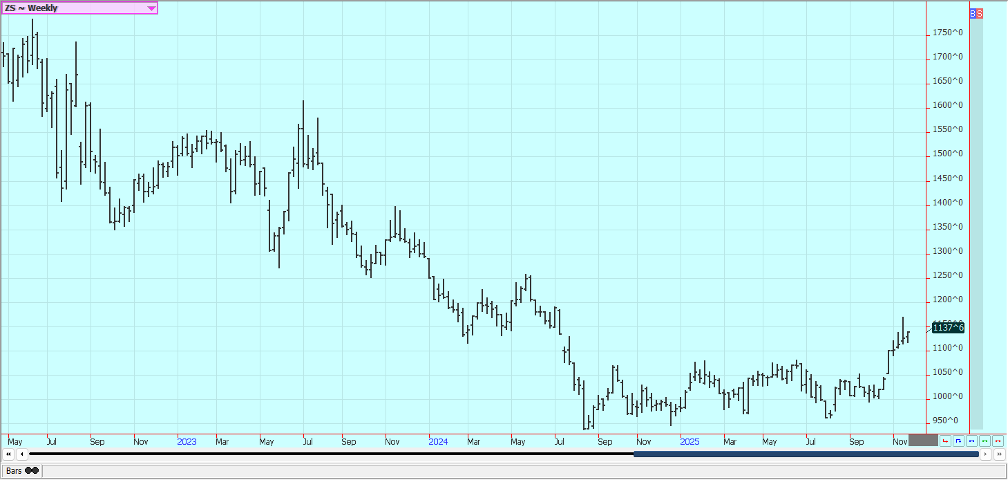

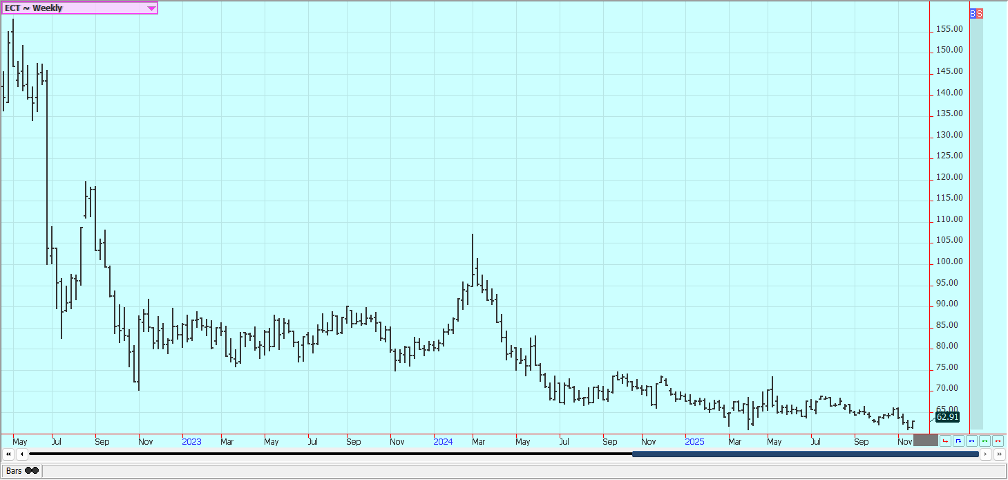

Cotton: Cotton was higher last week and might be in the process of completing a low on the daily charts. Some traders still hope for some new Cotton demand but as the cash market appears to be quiet. The weekly export sales report was positive once again, but old news. Cotton farmers are not selling too much due to price.

A lack of new Chinese demand for cotton has been important and a reason to see lower US prices. The lack of cotton demand seems to be part of the price for now. The US cotton harvest is over in most areas and initial yield reports are good. The monsoon in India is good and a good cotton production there is possible.

Weekly US Cotton Futures

Frozen Concentrated Orange Juice and Citrus: Futures were higher last week, and the trends are mixed on the daily charts. Traders are worried about demand even with lower prices. FCOJ from Brazil has been subjected to tariffs but those have been stopped by the US for now. The weather is considered good for production here and in Brazil and Mexico. Development conditions are good in Florida and in Brazil now with occasional showers in Florida and dry weather in Brazil.

Weekly FCOJ Futures

Coffee: New York and London were higher last week, and trends are mixed in New York and in London. Scattered showers are being reported now to improve tree condition in Brazil. Mexico is in good condition, as is Central America.

Vietnam has seen too much rain as typhoons hit the country, and big rains are reported in central areas again and are causing flooding and yield and quality concerns. The rains are easing now. Wire reports say that Brazil farmers are not selling even with tariffs removed by the US government.

Weekly New York Arabica Coffee Futures

Weekly London Robusta Coffee Futures

Sugar: New York and London were a little higher last week. Trends are sideways but are trying to turn up. There are still ideas of good supplies for the market from good growing conditions for cane and beets around the world continue. Production in Center-South Brazil has also been strong, but the south center harvest is almost over.

The prospect of a big global surplus in the 2025/26 season was keeping the market on the defensive with a rise in production in India and Thailand set to increased supplies while global consumption is expected to remain steady.

Weekly New York World Raw Sugar Futures

Weekly London White Sugar Futures

Cocoa: New York closed mixed and London closed a little higher last week. A big main crop harvest is anticipated in West Africa. Demand concerns in West Africa continue. Light rains mixed with heat in Ivory Coast’s cocoa-growing regions last week signaled a positive outlook for the main crop. There are still reports of increased production potential in other countries outside of West Africa, including Asia and Central America.

The market feels that there is less demand and the lack of demand is expected to continue. Traders are concerned over poor quality beans in Ivory Coast and talk that both Ivory Coast and Ghana have stopped marketing beans due to low prices. The beans are in ports now and available. The EU is expected to lift its forest restrictions on imports of certain products including Cocoa for an-other year.

Weekly New York Cocoa Futures

Weekly London Cocoa Futures

__

(Featured image by Trisha Downing via Unsplash)

DISCLAIMER: This article was written by a third party contributor and does not reflect the opinion of Born2Invest, its management, staff or its associates. Please review our disclaimer for more information.

This article may include forward-looking statements. These forward-looking statements generally are identified by the words “believe,” “project,” “estimate,” “become,” “plan,” “will,” and similar expressions, including with regards to potential earnings in the Empire Flippers affiliate program. These forward-looking statements involve known and unknown risks as well as uncertainties, including those discussed in the following cautionary statements and elsewhere in this article and on this site. Although the Company may believe that its expectations are based on reasonable assumptions, the actual results that the Company may achieve may differ materially from any forward-looking statements, which reflect the opinions of the management of the Company only as of the date hereof. Additionally, please make sure to read these important disclosures.

Futures and options trading involves substantial risk of loss and may not be suitable for everyone. The valuation of futures and options may fluctuate and as a result, clients may lose more than their original investment. In no event should the content of this website be construed as an express or implied promise, guarantee, or implication by or from The PRICE Futures Group, Inc. that you will profit or that losses can or will be limited whatsoever.

Past performance is not indicative of future results. Information provided on this report is intended solely for informative purpose and is obtained from sources believed to be reliable. No guarantee of any kind is implied or possible where projections of future conditions are attempted. The leverage created by trading on margin can work against you as well as for you, and losses can exceed your entire investment. Before opening an account and trading, you should seek advice from your advisors as appropriate to ensure that you understand the risks and can withstand the losses.

Argentina Introduces Automatic Authorization to Boost Crowdfunding and Investment Growth

The national government introduced automatic authorization for crowdfunding platforms, simplifying registration under CNV rules to speed investments and reduce bureaucracy....

Gilead’s $5 Billion Tubulis Deal Boosts Evotec Stake

Gilead is acquiring German biotech firm Tubulis for up to $5 billion, benefiting Evotec, which holds a 3.14 percent stake...

Switzerland Aligns Corporate Sustainability Rules with EU Standards

Switzerland proposes new sustainability rules to align with European Union standards. The law targets large companies, requiring ESG reporting and...

Bitcoin Leads Crypto Rally as Iran Ceasefire Boosts Markets

The US and Iran agreed to a two-week ceasefire, boosting crypto markets. Bitcoin surged above $71,500, Ethereum topped $2,200, while...

ECSP Crowdfunding vs. eWpG Bonds: Overcoming SME Financing Limits

The ECSP Regulation limits annual crowdfunding per project promoter to €5 million, requiring a full prospectus for higher amounts, which delays...

|

|

|  |

|

|

-

Impact Investing1 week ago

Impact Investing1 week agoItalian Unlisted Banks Lag on ESG Sustainability

-

Crypto6 days ago

Crypto6 days agoEuro Stablecoins Struggle to Compete with Dollar Dominance in Crypto Markets

-

Crypto2 weeks ago

Crypto2 weeks agoCrypto Markets Volatile as Bitcoin Hovers, Solana Eyes AI Integration

-

Cannabis1 day ago

Cannabis1 day agoGermany’s Cannabis Reform Shows Limited Risks but Calls for Regulatory Adjustments