Markets

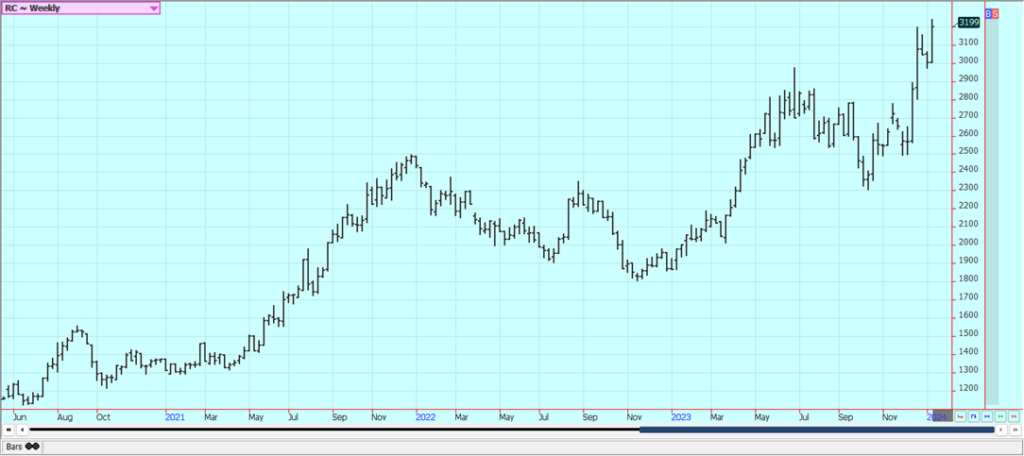

Rice Futures Are Trying to Complete a Sideways Formation with a Move to Higher Prices

Rice closed higher on Friday but a little lower for the week. USDA issued its WASDE and production estimates and production was increased via increased yields. The increase was in long grain with medium and short grain production estimated lower than the previous year. Demand showed increases on the domestic side but unchanged demand potential on the export side.

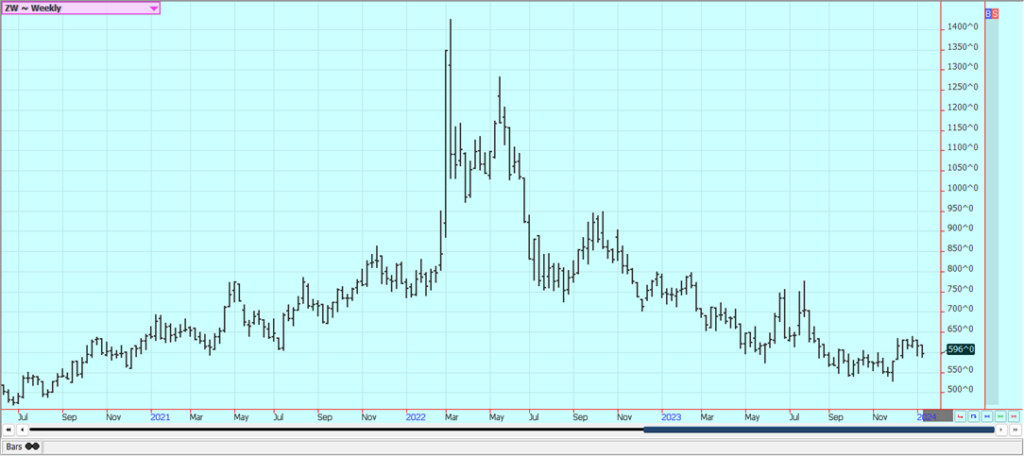

Wheat: Wheat markets were lower last week in response to the USDA reports that were actually price positive and the advent of very cold weather into the central US. There should be snow cover to protect the crops so little if any damage is expected. USDA cut its ending stocks estimates and also showed less than expected planted area for Wheat for the coming year.

The big weakness in Corn and Soybeans caused weakness in Wheat as did a dismal export sales pace to date for US Wheat. Black Sea offers are still plentiful and Russian prices appear to be about 260.00 per tons FOB with Ukrainian prices about the same. EU countries are offering as well and are getting new business. Demand has been poor for US Wheat as Russia production looks strong.

Weekly Chicago Soft Red Winter Wheat Futures

Weekly Chicago Hard Red Winter Wheat Futures

Weekly Minneapolis Hard Red Spring Wheat Futures

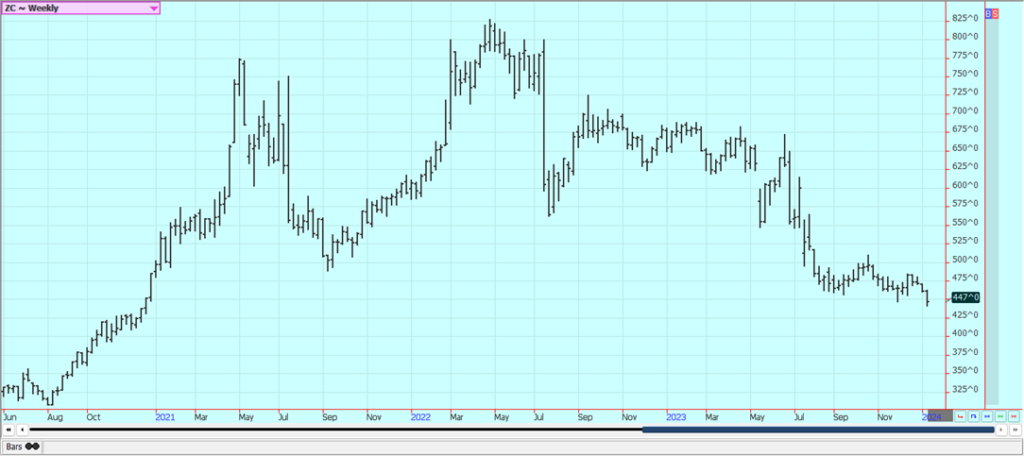

Corn: Corn closed lower last week with much of the selling seen on Friday in response to the USDA reports. USDA increased yields by over 3 bu/acre to177.4 bu/acre and increased production to 15.342 billion bushels. Ending stocks were estimated at 2.163 billion bushels, from 2.131. billion last month. USDA left export demand unchanged but increased domestic demand in all categories but not enough to change the trajectory of higher stocks.

The CONAB Brazil production estimate released on Wednesday that was reduced for the coming year due to reduced Winter Corn planted area and USDA reduced its production estimate as well. Oats were higher in sympathy with Corn as no changes were made to the balance sheets. The market anticipates increased selling from US producers, but many have sold enough, and elevators and processors are reported to be full. There are also forecasts for a lot of very cold air for the Midwest to keep farmers inside and not opening the bins. Producers are also looking for higher prices now as crops are in the bin for the Winter. Ideas of weak demand are keeping prices low. The market feels that there is more than enough Corn for any demand.

Weekly Corn Futures

Weekly Oats Futures

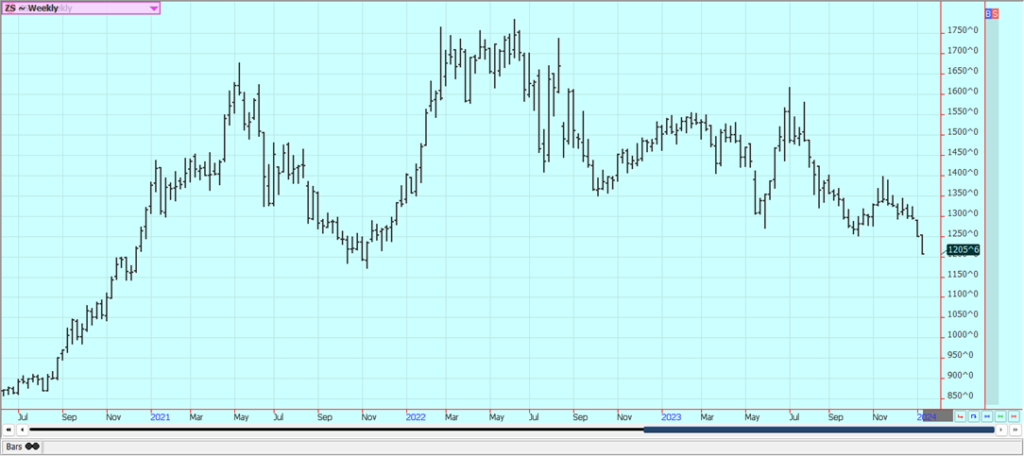

Soybeans and Soybean Meal: Soybeans and the products closed lower last week, with much of the selling coming on Friday in response to the USDA reports that showed an increase in yields, production, and ending stocks for Soybeans. Production was raised to 4.165 billion bushels in response to a yield estimate of a50.6 bu/acre, from49.8 bu/acre in November. Ending stocks were estimated at 280 million bushels from 238 million in December.

Brazil production was cut to 157 million tons, but this was spied out by the US changes and the continued strong production potential in Argentina. CONAB on Wednesday estimated production down at just over 155 million tons, but this would still be a new record production. The precipitation keeps falling in Brazil is expected to continue through this weekend. Soybean Meal was weaker on increasing confidence that Argentina will return as a major exporter and as US crushers are crushing for oil and have a lot of extra meal available.

There are some forecasts for significant rains and rains this week in central and northern Brazil and less wet conditions in the south. The trade remains concerned about the weather forecasts for South America but is holding to ideas of production over 150 million tons. Our source suggests that production in Brazil could be much less due to the extreme weather seen already. Brazil has been mostly hot and dry in northern areas and too wet in southern areas. Argentina crops are reported o be in good condition with enough moisture. These weather trends are expected to continue this week.

Weekly Chicago Soybeans Futures

Weekly Chicago Soybean Meal Futures

Rice: Rice closed higher on Friday but a little lower for the week. USDA issued its WASDE and production estimates and ptoduction was increased via increased yields. The increase was in long grain with medium and short grain production estimated lower than the previous year. Demand showed increases on the domestic side but unchanged demand potential on the export side.

Ending stocks were increased to 24 million cwt for long grain from 21.2 million before. USDA cut its all Rice ending stocks estimate to 41.5 million cwt from 41.9 million in December. Demand reports have been weaker lately and have featured traditional buyers in Latin America and Asia. Futures are trying to complete a sideways formation with a move to higher prices and might have started on this quest on Friday. The market acts firm despite the USDA long grain reports as world data showed cuts to ending stocks levels.

Weekly Chicago Rice Futures

Palm Oil and Vegetable Oils: Palm Oil was higher last week in reaction to weaker than expected December production and stocks data posted by MPOB. It estimated production at 1.550 million tons, down 13.3% from November. Demand was also down, but ending stocks were estimated at 2.291 million tons, down 4.6%. Trends are turning up on the daily charts and are sideways on the weekly charts.

Canola was higher last week in consolidation trading after the release of the USDA reports. Current forecasts call for drier weather in southern Brazil and wetter weather in central and northern areas this week. The Canola crop is harvested, and it is in bins, so it will take some price movement to get new farm sales. Trends are down on the daily charts in this market.

Weekly Malaysian Palm Oil Futures

Weekly Chicago Soybean Oil Futures

Weekly Canola Futures:

Cotton: Cotton closed lower on Friday but higher for the week. USDA released its annual production report and the latest batch of WASDE report on Friday. The production report from USDA was bullish to prices as a cut in harvested area led to decreased production of 121.41 billion bales despite increased yields. Ending stocks were trimmed to 2.90 million bales from 310 million in December even with a cut in demand.

Export and residual demand were cut. World ending stocks levels showed increased stocks and this hurt the price action in Cotton on Friday. The US economic data has been positive, but the Chinese economic data has not been real positive and demand has been down. There are still many concerns about demand from China and the rest of Asia due to the slow economic return of China in the world market.

Weekly US Cotton Futures

Frozen Concentrated Orange Juice and Citrus: FCOJ closed higher last week after a few weeks of downside price action. It was a price recovery week for futures as new demand was found.. The moves imply that supply is finally getting bigger than demand and imply that consumer demand has dropped significantly in recent weeks. There are no weather concerns to speak of for Florida right now with the hurricane season all but over and no major storms hitting the state recently.

The weather has improved in Brazil with some moderation in temperatures and increased rainfall in the forecast for this week. Brazil got more than expected rains over the weekend. Reports of short supplies in Florida and Brazil are around. Historically low estimates of production in Florida due in part to the hurricanes and in part to the greening disease that have hurt production, but conditions are significantly better now with scattered showers and moderate temperatures.

Weekly FCOJ Futures

Coffee: New York closed lower and London closed higher last week on index fund buying in New York and as Robusta offers remain difficult to find. London was the leader last week on the rally. The chart trends for both markets imply that more rallies can be expected in the next few weeks. Rains continued to fall in parts of Brazil Coffee areas and Vietnamese and Brazilian producers remain reluctant sellers.

Brazil production areas are seeing some very beneficial rainfall this current week. Arabica and Robusta areas were affected by drought, but the current forecasts call for a lot of help in affected areas. Brazil weather remains uneven but is improving for the best crop production.

Weekly New York Arabica Coffee Futures

Weekly London Robusta Coffee Futures

Sugar: New York and London closed higher last week and are testing the upside of the trading range on the weekly charts. So far, the markets have failed to confirm a new up trend. Brazil weather forecasts call for dryness in the south and continued scattered showers in central and northern areas this week. The market continues to see stressful conditions in Asian production areas but has noted that India has changed its Ethanol policy to make more Sugar available to the market.

There are worries about the Thai and Indian production potential due to El Nino and talk that India could turn into an importer next year. Offers from Brazil are still active but other origins. are still not offering or at least not offering in large amounts except for Ukraine, and demand is still strong. Brazil ports are very congested, so ship-ment of Sugar has been slower. UNICA said that the Brazil Sugarcane crush was 4.87 million tons in the second half of December, up 80% from last year. Sugar production was 235,800 tons, up 36% from last year. Ethanol production was 526.1 million liters, up 63% from last year.

Weekly New York World Raw Sugar Futures

Weekly London White Sugar Futures

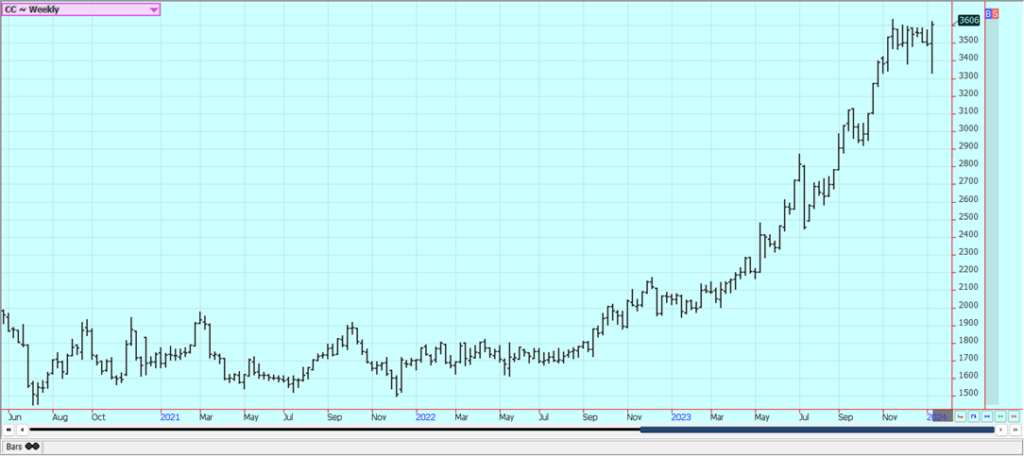

Cocoa: Both markets closed higher last week after trading lower early in the week. The weekly chart patterns display the potential for hook reversals to higher prices in coming weeks. The availability of Cocoa from West Africa remains restricted and projections for another production deficit against de-mand for the coming year are increasing.. The harvest seems to be coming and demand could be a problem with the current very high prices.

Traders are worried about another short production year and these feelings have been enhanced by El Nino that could threaten West Africa crops with hot and dry weather later this year. The main crop harvest is starting in parts of West Africa so the losses will become minor for now. Scattered to isolated showers are reported in the region now and the harvest is coming. Ideas of tight supplies remain based on more reports of reduced arrivals in Ivory Coast and Ghana continue,

Weekly New York Cocoa Futures

Weekly London Cocoa Futures

__

(Featured image by almatel via Pixabay)

DISCLAIMER: This article was written by a third party contributor and does not reflect the opinion of Born2Invest, its management, staff or its associates. Please review our disclaimer for more information.

This article may include forward-looking statements. These forward-looking statements generally are identified by the words “believe,” “project,” “estimate,” “become,” “plan,” “will,” and similar expressions. These forward-looking statements involve known and unknown risks as well as uncertainties, including those discussed in the following cautionary statements and elsewhere in this article and on this site. Although the Company may believe that its expectations are based on reasonable assumptions, the actual results that the Company may achieve may differ materially from any forward-looking statements, which reflect the opinions of the management of the Company only as of the date hereof. Additionally, please make sure to read these important disclosures.

Futures and options trading involves substantial risk of loss and may not be suitable for everyone. The valuation of futures and options may fluctuate and as a result, clients may lose more than their original investment. In no event should the content of this website be construed as an express or implied promise, guarantee, or implication by or from The PRICE Futures Group, Inc. that you will profit or that losses can or will be limited whatsoever.

Past performance is not indicative of future results. Information provided on this report is intended solely for informative purpose and is obtained from sources believed to be reliable. No guarantee of any kind is implied or possible where projections of future conditions are attempted. The leverage created by trading on margin can work against you as well as for you, and losses can exceed your entire investment. Before opening an account and trading, you should seek advice from your advisors as appropriate to ensure that you understand the risks and can withstand the losses.

Ecobnb Turns Sustainable Tourism Into Measurable Impact

Ecobnb’s sustainable tourism platform generated significant environmental and social impact in 2025, avoiding 58,207 kg of CO₂ and adding 583...

Sugar Markets Balance Biofuel Demand and Global Supply

Sugar markets in New York and London were mostly unchanged as the Iran conflict renewed interest in biofuels. Drought concerns...

The $40 Trillion Trap: Disinflation Is Not Deliverance

U.S. debt has reached $40 trillion, with $24 billion weekly interest, while deficits accelerate. Despite disinflation in CPI, from cooling...

FinTech Matures as AI and Infrastructure Drive the Next Growth Phase

Fintech markets are entering a mature phase, shifting from rapid growth to consolidation, specialization, and sustainable business models. Zurich and...

Bitcoin, and Ethereum Rise, While Cardano Enters Transition

Bitcoin and Ethereum posted modest weekend gains, supported by ETF inflows. A new proposal may protect Bitcoin from quantum threats....

|

|

|  |

|

|

-

Fintech5 days ago

Fintech5 days agoAdvanced Blockchain Under Pressure Amid Crypto Market Shifts

-

Impact Investing2 weeks ago

Impact Investing2 weeks agoICSC Raises €500M Social Bond, Expanding Sustainable Investment Reach

-

Fintech1 day ago

Fintech1 day agoFinTech Matures as AI and Infrastructure Drive the Next Growth Phase

-

Fintech1 week ago

Fintech1 week agoWithings Achieves Profitability in 2025 with 90% Growth Since 2018