Markets

Both Sugar Markets Closed Lower Last Week

Both sugar markets closed lower last week and both markets remain in a trading range. There are still ideas that the Brazil harvest can be strong for the next few weeks if not longer and production data released a few weeks ago by CONAB indicated that the cane harvest could be less, but that Sugar production could be higher.

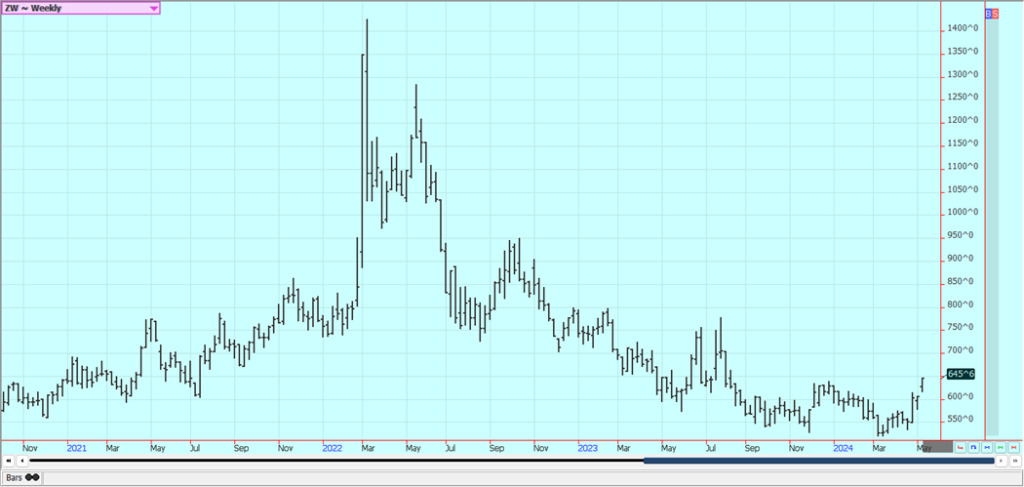

Wheat: Wheat was higher last week on reports of frosts and freezing temperatures in Russian growing areas. Reports indicate that Russia will still have plenty of Wheat for export in the coming year. USDA issued its latest reports on Friday and included a field survey of Winter Wheat production. Winter Wheat production was estimated at 1.288 billion bushels which was a little below the average trade estimate.

Ending stocks for Wheat were also below the trade estimate at 766 million bushels. The weather is still a key, with extreme dryness reported in Russia and parts of the US and too wet conditions reported in Europe. The weekly export sales report showed poor sales once again and sales are not likely to improve anytime soon with the Dollar strength.

Big world supplies and low world prices are still around. Export sales remain weak on competition from Russia, Ukraine, and the EU as those countries look to export a lot of Wheat in the coming period. Black Sea offers are still plentiful, but Russia has been bombing Ukraine again and shipments might be hurt from that origin.

Weekly Chicago Soft Red Winter Wheat Futures

Weekly Chicago Hard Red Winter Wheat Futures

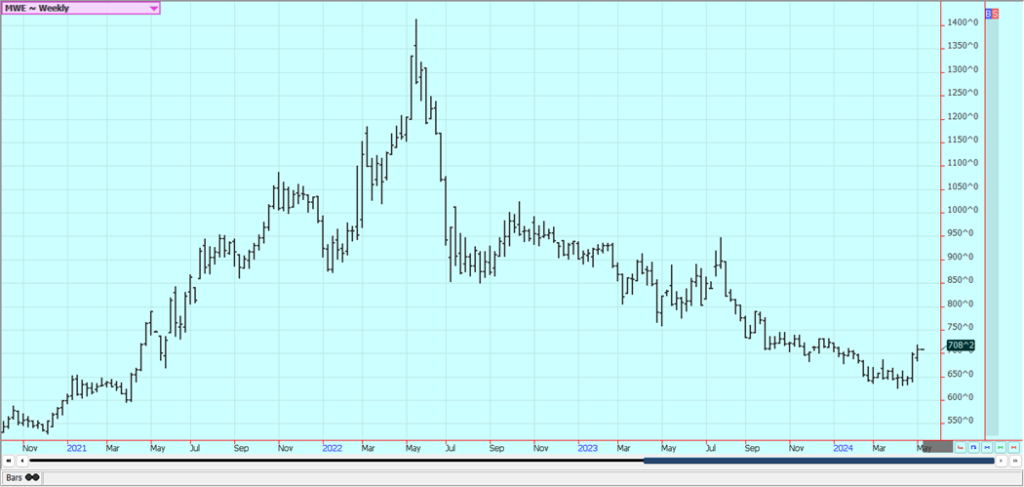

Weekly Minneapolis Hard Red Spring Wheat Futures

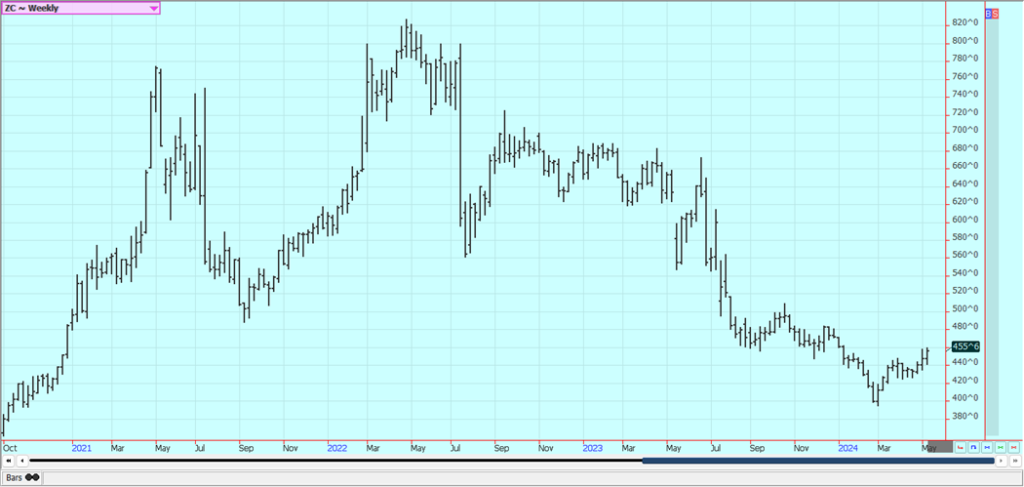

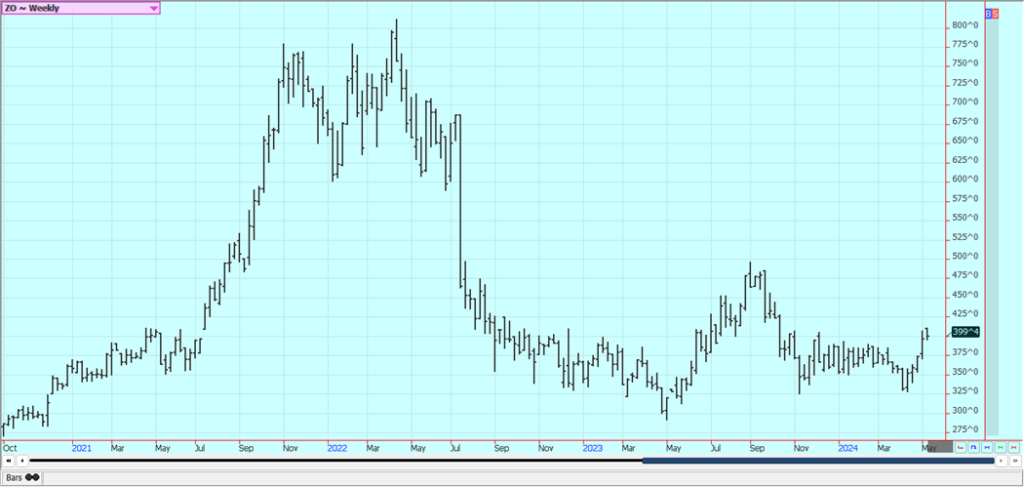

Corn: Corn and Oats closed higher last week in reaction to the USDA reports. USDA estimated high production at 14.860 billion bushels, but ending stocks were a little below trade expectations at 2.102 billion bushels. USDQ anticipates better demand for US Corn with the cheaper prices seen now. USDA made no real changes to South American production estimates.

The Argentine crop has been hit by stunting disease that robs yields and the Brazil Winter crop is suffering from hot and dry weather. Demand has been the driving force behind the rally but now South American weather is the driving force. Increased demand was noted in most domestic categories along with rising basis levels, and export demand has been strong. Ethanol demand has turned less due to weaker petroleum prices seen lately. There is very dry weather for the Winter crops in central and northern Brazil

Weekly Corn Futures

Weekly Oats Futures

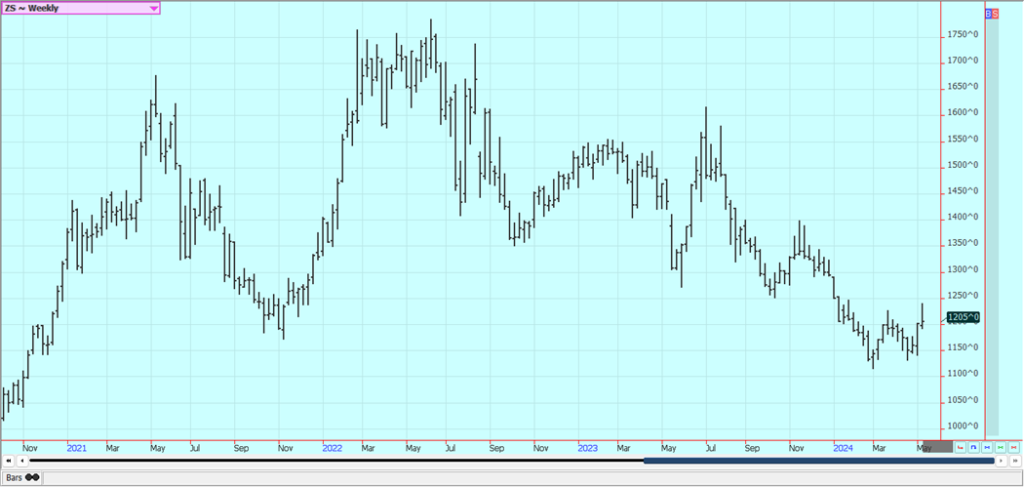

Soybeans and Soybean Meal: Soybeans and the products closed a little higher, mostly on reports of severe flooding in southern Brazil. Support for Soybeans came from reports of excessive rains falling on unharvested crops in southern Brazil. Rains up to 400 mm were reported by newswires. USDA released its first estimates for the coming crop year and held production potential at high levels at 4.450 billion bushels.

Export and domestic demand were increased but ending stocks also were estimated higher qt 450 million bushels. Futures rallied anyway and the rally on what appeared to be negative news can often mean that higher prices are coming this week and for the next couple of weeks. Domestic demand has been strong in the US but has suffered as crushers were crushing for oil. Oil demand has suffered as cheaper alternatives for feedstocks hit the bio fuels market. Funds remain short in the market.

Weekly Chicago Soybeans Futures

Weekly Chicago Soybean Meal Futures

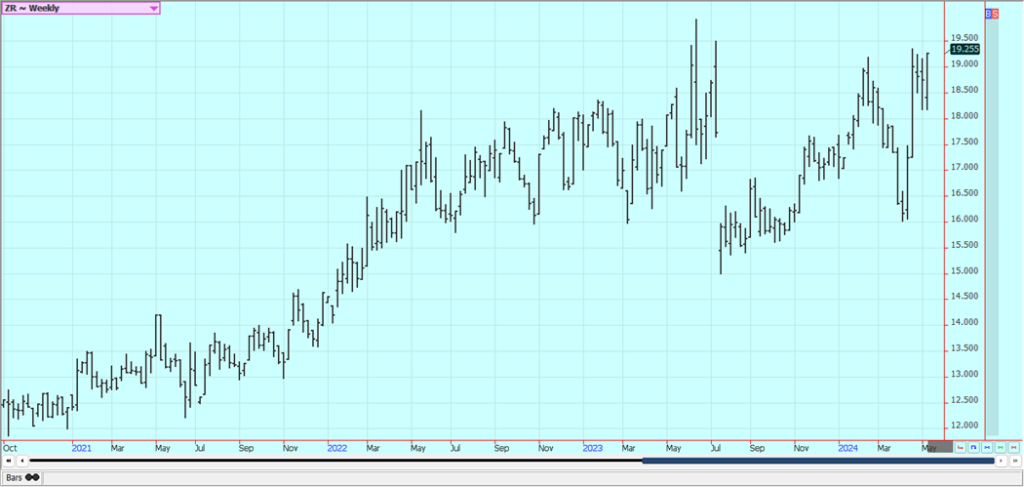

Rice: Rice closed higher and near recent highs last week. The futures market overall remained in a short term trading range. Support comes from adverse weather in South American growing areas while new selling is noted from the potential for a big crop in the US. The big US crops are now in doubt from reports of extreme rains in southern growing areas and especially near Houston. Supply tightness is expected to give way to increased production this year and greatly increased supplies this Fall. These ideas are reflected in the prices seen in the cold crop and the new crop.

Weekly Chicago Rice Futures

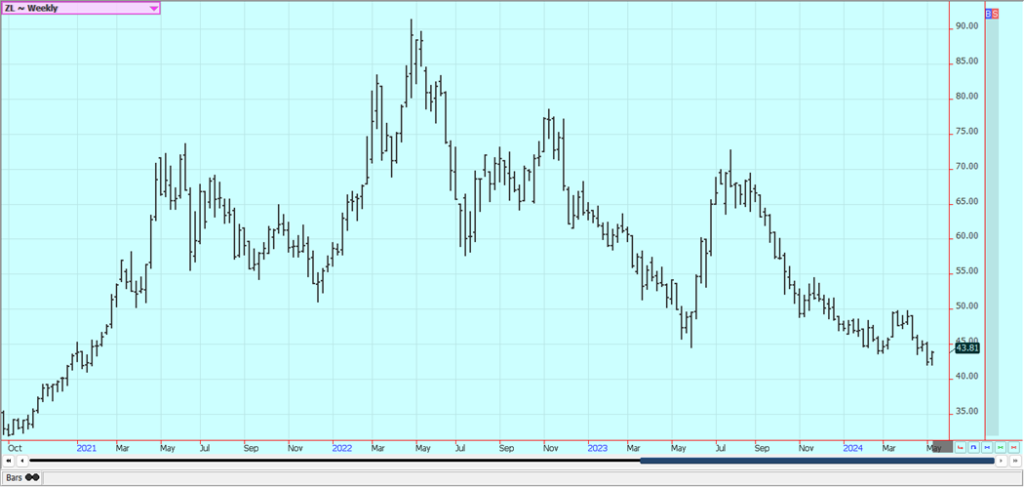

Palm Oil and Vegetable Oils: Palm Oil was lower on ideas of weaker bio fuels demand despite reports of strong demand from India and reports of reduced production. Trends are down on the daily and weekly charts. Canola was higher despite weaker prices in world vegetable oils markets as the market pays attention to Chicago price action and the flooding in Brazil. Farmers concentrate on fieldwork and not selling.

Weekly Malaysian Palm Oil Futures:

Weekly Chicago Soybean Oil Futures

Weekly Canola Futures

Cotton: Cotton was lower last week and trends are still mixed in the market. USDA increased production for the coming year and also increased demand and ending stocks. Increased production came mosly on a big increase in harvested acreage. The report was bearish for futures. Demand remains a problem. The export sales report showed poor sales once again and demand is not likely to improve with the Dollar stronger.

USDA made no changes to the domestic supply or demand sides of the balance sheets, but did cut world ending stocks slightly. Trends are still down on the weekly charts. Demand has been weaker so far this year. The US economic data has been positive, but the Chinese economic data has not been real positive and demand concerns are still around. However, Chinese consumer demand has held together well, leading some to think that demand for Cotton in world markets will increase over time.

Weekly US Cotton Futures

Frozen Concentrated Orange Juice and Citrus: FCOJ closed sharply higher last week and broke out of the trading range for higher levels. USDA released its latest production estimates and Florida production was estimated at 17,8 million boxes, down 5% from the last estimate but still 13% above the production of last year. Florida early and mid season and navel production was left at 6.80 million boxes, unchanged from the previous estimate, but Valencia production was cut 8% to 11 million boxes.

Nielsen is reporting less retail demand due to the higher prices and volumes sold at retail have sagged. The reduced production appears to be at the expense of the greening disease. There are no weather concerns to speak of for Florida or for Brazil right now. The weather has improved in Brazil with some moderation in temperatures and increased rainfall amid reports of short supplies in Florida and Brazil are around but will start to disappear as the weather improves and the new crop gets harvested.

Weekly FCOJ Futures

Coffee: New York closed slightly higher last week and London closed lower and traders say that the market could have made a low on the charts. There were indications that Brazil and Vietnam producers were now offering Coffee, Vietnamese producers are reported to have about a quarter of the crop left to sell or less and reports indicate that Brazil producers are reluctant sellers for now after selling a lot earlier in the year.

The next Robusta harvest in Brazil is continuing and offers for all Coffee increased last week in part on weakness in the Real. Roasters and other buyers are pulling back from the market in hopes of lower prices down the road.

Weekly New York Arabica Coffee Futures

Weekly London Robusta Coffee Futures

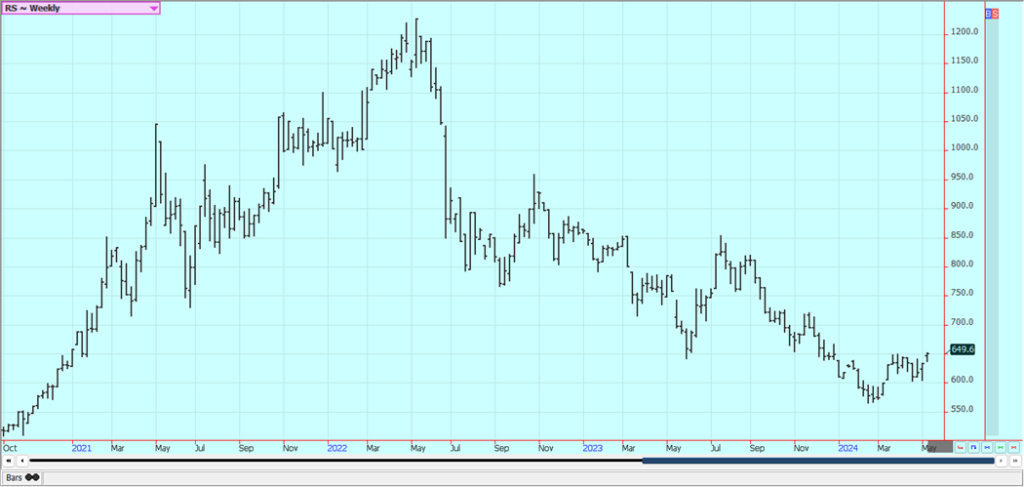

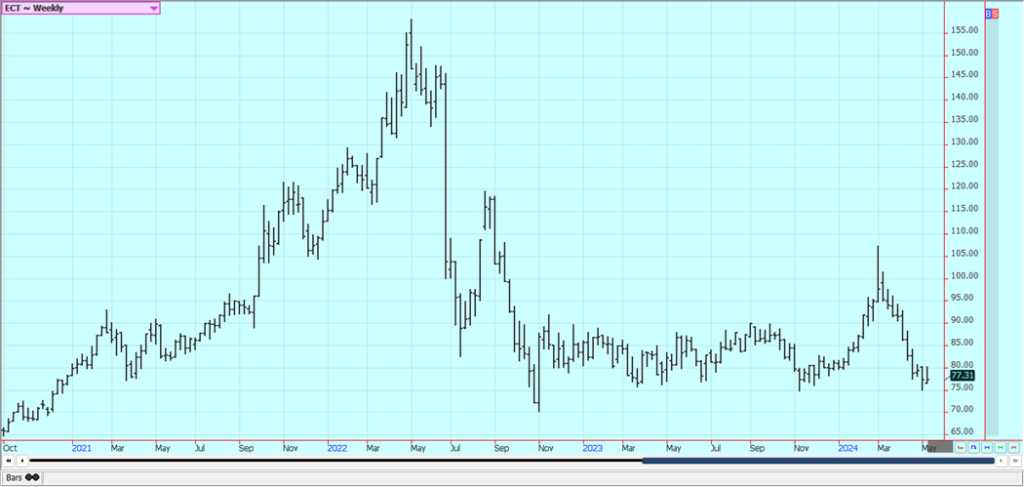

Sugar: Both markets closed lower last week and both markets remain in a trading range. There are still ideas that the Brazil sugar harvest can be strong for the next few weeks if not longer and production data released a few weeks ago by CONAB indicated that the cane harvest could be less, but that Sugar production could be higher.

Indian sugar production estimates are creeping higher but are still reduced from recent years. There are worries about the Thai and Indian production, but data shows better than expected sugar production from both countries. Offers from Brazil are still active but other origins. are still not offering in large amounts.

Weekly New York World Raw Sugar Futures

Weekly London White Sugar Futures

Cocoa: Both markets were higher last week in recovery trading. Trends are trying to turn up on the daily charts. It seemed that speculators were liquidating long positions. Production concerns in West Africa as well as demand from nontraditional sources along with traditional buyers keep supporting fu-tures. Production in West Africa could be reduced this year due to the extreme weather which includ-ed Harmattan conditions.

The availability of Cocoa from West Africa remains very restricted and pro-jections for another production deficit against demand for the coming year are increasing. Ideas of tig8ht supplies remain based on more reports of reduce arrivals in Ivory Coast and Ghana continue. Mid crop harvest is now underway and here are hopes for additional supplies for the market from the second harvest. Demand continues to be strong, especially from traditional buyers of Cocoa.

Weekly New York Cocoa Futures

Weekly London Cocoa Futures

__

(Featured image by Jason via Unsplash)

DISCLAIMER: This article was written by a third party contributor and does not reflect the opinion of Born2Invest, its management, staff or its associates. Please review our disclaimer for more information.

This article may include forward-looking statements. These forward-looking statements generally are identified by the words “believe,” “project,” “estimate,” “become,” “plan,” “will,” and similar expressions. These forward-looking statements involve known and unknown risks as well as uncertainties, including those discussed in the following cautionary statements and elsewhere in this article and on this site. Although the Company may believe that its expectations are based on reasonable assumptions, the actual results that the Company may achieve may differ materially from any forward-looking statements, which reflect the opinions of the management of the Company only as of the date hereof. Additionally, please make sure to read these important disclosures.

Futures and options trading involves substantial risk of loss and may not be suitable for everyone. The valuation of futures and options may fluctuate and as a result, clients may lose more than their original investment. In no event should the content of this website be construed as an express or implied promise, guarantee, or implication by or from The PRICE Futures Group, Inc. that you will profit or that losses can or will be limited whatsoever.

Past performance is not indicative of future results. Information provided on this report is intended solely for informative purpose and is obtained from sources believed to be reliable. No guarantee of any kind is implied or possible where projections of future conditions are attempted. The leverage created by trading on margin can work against you as well as for you, and losses can exceed your entire investment. Before opening an account and trading, you should seek advice from your advisors as appropriate to ensure that you understand the risks and can withstand the losses.

Blockchain Evolves Toward AI, Finance and Quantum Security

Blockchain is evolving beyond crypto into finance, AI applications, and digital markets, while security and regulation remain challenges. Quantum threats...

The Italian Crowdinvesting Market Faces Sharp Decline in 2026

Italian crowdinvesting market continued to decline in 2026, with fundraising falling 36.8% year-on-year to €164.19 million. Platforms and active campaigns...

Sartorius Stedim Biotech Maintains Growth Momentum in H1 2026

Sartorius Stedim Biotech reported solid H1 2026 results, with revenue reaching €1.527 billion and EBITDA rising to €479 million. Growth...

Bank of Africa Launches BOA MDM Network to Boost Diaspora Investment in Morocco

Bank of Africa launched the BOA MDM Network to channel diaspora remittances into productive investment, aiming to raise their share...

Switzerland’s Medical Cannabis Reform Advances Access, But Barriers Remain

Switzerland’s 2022 medical cannabis reform improved patient access by removing federal approval requirements, but challenges remain. MEDCAN highlights barriers including...

|

|

|  |

|

|

-

Impact Investing2 weeks ago

Impact Investing2 weeks agoItaly’s Startup Ecosystem Shrinks but Becomes More Digital and Specialized

-

Fintech1 day ago

Fintech1 day agoBlockchain Evolves Toward AI, Finance and Quantum Security

-

Africa1 week ago

Africa1 week agoSenegal’s Debt Strategy: Choosing Between Restructuring and Financial Innovation

-

Biotech3 days ago

Biotech3 days agoBiotech Revival: Big Pharma Bets on Innovation and Acquisitions