Markets

Global Sugar Prices Fall Amid Higher Production Outlook and Mixed Market Trends

Sugar prices in New York and London fell last week amid expectations of higher Brazil and Asian production, despite UNICA reporting a 65% drop in Brazil’s late-December output. Weak Brazilian Real supports sales. India and Thailand expect strong crops, but adverse weather may limit supply. Mixed trends persist in daily and weekly charts.

Wheat: Chicago closed a little higher and Kansas City and Minneapolis were slightly lower last week on reports of weaker overseas values and chart trends are mixed. Russian and Ukrainian prices were soft earlier this week despite less Wheat on offer. Buyer have not been active lately. USDA showed stronger than expected weekly export sales, but the sales were not strong enough to create much meaningful buying interest.

The USDA reports were not bullish to Wheat as plantings were higher than trade expectations as were world ending stocks estimates. The growing conditions in the US are very good. Reports of very beneficial rains for the Great Plains and Midwest and reports of steady to firm prices quoted in Russia and steady prices Argentina were around and helped keep the US market mostly steady in current ranges.

Wheat farmers in the US planted the Winter crops under good conditions. Australia has seen too much rain recently that has downgraded Wheat quality, but Australia still has a very big crop to sell into world markets.

Weekly Chicago Soft Red Winter Wheat Futures

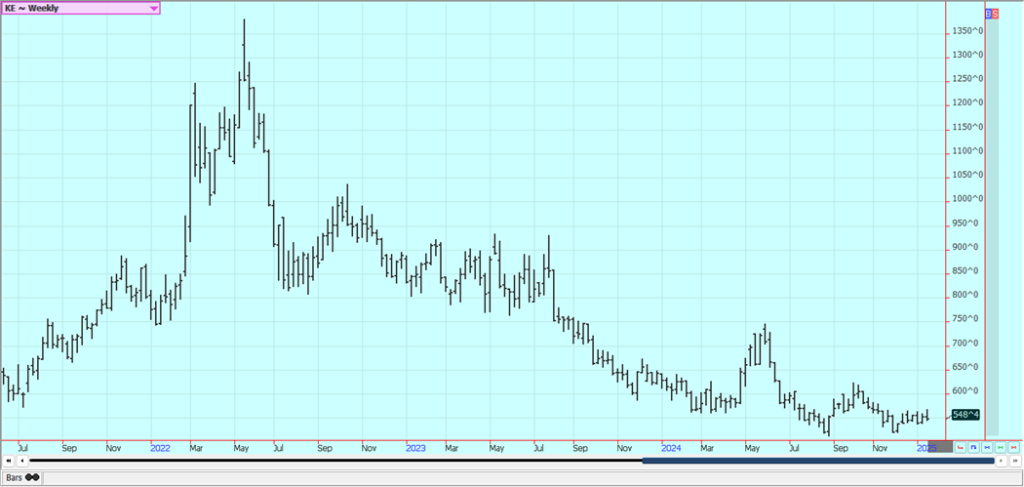

Weekly Chicago Hard Red Winter Wheat Futures

Weekly Minneapolis Hard Red Spring Wheat Futures

Soybeans and Soybean Meal: Soybeans closed higher despite reports of beneficial rains seen in southern Brazil and Argentina. More rain will be needed before the harvest to finish the crops, but the reported rains went a long way to keeping yield estimates strong for both regions. The fundamentals remain mixed to bearish. Bullish US production estimates released by USDA a week ago showed that ending stocks are now estimated at 350 million bushels. This is still a lot of Soybeans but much less than before.

President Trump wants to stop the use of bio fuels as part of his war on the green economy hurt demand ideas for Soybean Oil. The tariffs that Trump plans to impose could be a detriment to sales of all products. Brazil looks to produce much more than a year ago and some estimates range as high as 175 million tons for the country. Brazilian farmers have planted what is expected to be a very big crop in central and northern areas of the country.

Demand has been very strong so far this year, in part as many buyers try to get bought ahead of any new tariffs that the Trump administration might impose and in part as the dryness seen before the harvest made US Soybeans easier to store for use down the road. Soybeans are offered cheaper in South America now and the weekly export sales report showed less sales than seen earlier in the season.

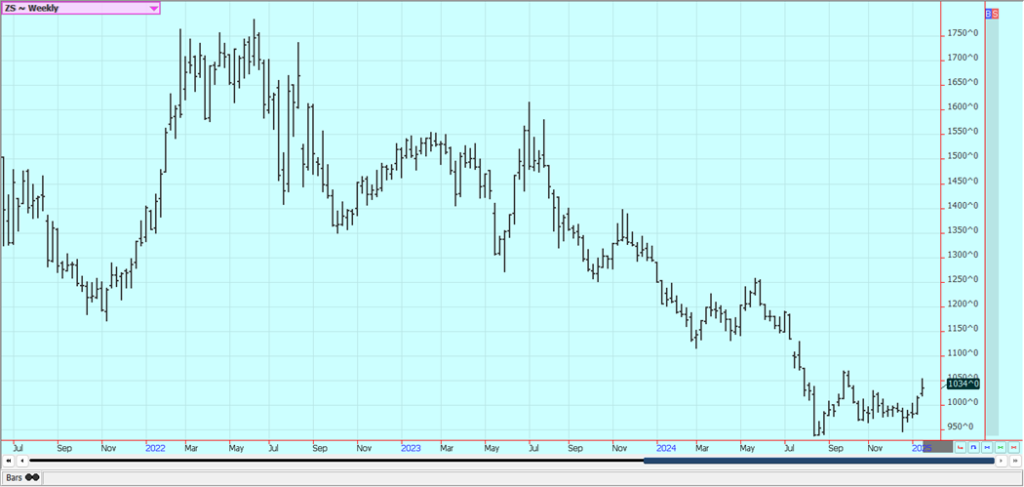

Weekly Chicago Soybeans Futures

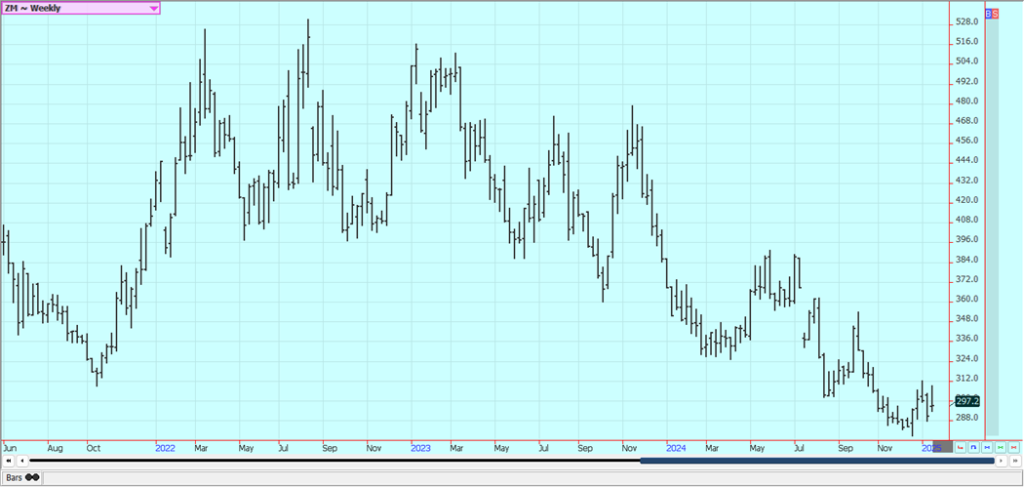

Weekly Chicago Soybean Meal Futures

Rice: Rice closed higher last week. Futures showed some weakness late in the week on reports of beneficial rains in South American production areas. Argenztina and southern Brazil saw the best rain in a long time and selling was seen in many ag markets with strong South American ties. Prices got very cheap early this Winter but have rebounded as farmers have not been selling. Export sales have not been strong, and domestic demand is there but is not strong enough right now to bid prices much higher.

Milling yields have been called poor at 50 lbs instead of 55 lbs. There are some questions about the milling quality of the new crop Rice and that will help keep demand from mills for good Rice stronger than it might have been. The trends are still up the daily charts. Generally weak Asian prices are still reported. Brazil prices remain strong, but the difference is gone to world buyers as the Real is much lower against the US Dollar.

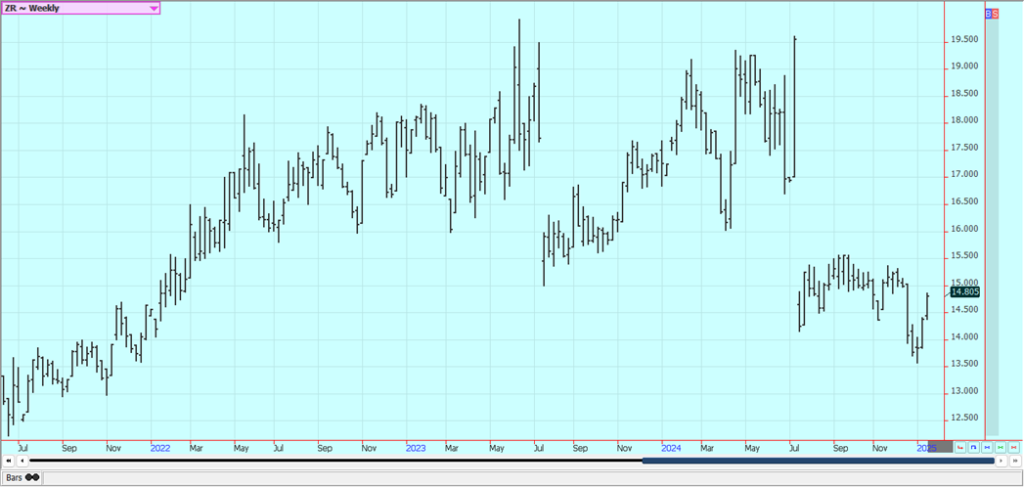

Weekly Chicago Rice Futures

Palm Oil and Vegetable Oils: Palm Oil was lower last week on demand concerns. Indonesia wants to use a blend of 40% of Plam Oil in its gasoline mixtures, but this has proved to be expensive and might need to be reduced and allow for increased exports. Demand from China has not been good and demand from India has been reduced. Ideas of weaker production caused by too much rain and reports of good demand provided support.

Chart trends are down. Canola was lower along with the price action in Chicago. The market is holding above the December highs in part due to the bullish USDA reports. The harvest is over in Canada and the crops are locked away in the bin. Producers will try to wait for higher prices before selling much, especially with the cold weather in place now.

Weekly Malaysian Palm Oil Futures:

Weekly Chicago Soybean Oil Futures

Weekly Canola Futures

Cotton: Cotton was higher last week, but March made new contract lows on Thursday despite strong weekly export sales. The US Dollar has been strong and Crude Oil futures have been weaker. Selling has come from news that Trump will impose some big tariffs on China, but the tariffs posted were not as high as he had threatened before during the campaign.

China has big problems with its domestic economy with consumer buying interest not strong and many people not working. The government has said it will take stimulus measures for the economy there next year, but its Cotton demand is expected to stay soft. There are still reports of weaker demand potential against an outlook for good US production in the coming year.

Weekly US Cotton Futures

Frozen Concentrated Orange Juice and Citrus: FCOJ closed lower last week, but near the highs of the week as another cold front is expected in the east early this week. Chart trends are mixed on the daily charts. The short term supply scenario remains very tight as USDA maintained its Florida production estimate at 12 million boxes and estimated US production at 60.3 million boxes from 60.6 million in its previous estimate.

The lack of lower production goes against ideas of declining demand and even if demand is holding well. The market remains well supported in the longer term based on forecasts for tight supplies in Florida. The reduced production appears to be mostly at the expense of the greening disease and some extreme weather seen in the last couple of years. There are no weather concerns to speak of for Brazil or Florida right now, but cold weather for Florida this week should be monitored in case damage becomes possible.

Weekly FCOJ Futures

Coffee: New York was higher and London was a little lower last week on reports of improving rains for southern Brazil and increased offers by Vietnam producers before the Tet holiday. The producers need the money for the festivities and to help tide them over with much of the country closed during the festival. The rains in Brazil are falling in the dry southern area as central areas have had good rains in recent weeks and are already in good condition. Tight Arabica availability went against tight Robusta availability as the harvest has stalled in Vietnam due to too much rain.

The rains are also hurting the quality of the harvest as it is more difficult to dry and store the beans correctly. Reports of reduced offers from Brazil on weather induced short crops continue and there are also reports of too much rain in parts of Central America damaging crops there. In Brazil, CECAFE said that 2024 exports were 50.4 million bags, a new record that is not likely to be repeated this year. The flow of coffee from Brazil should slow this year, an off-year in the country’s biennial crop cycle, while dry weather last year could also reduce the size of the 2025/26 harvest.

Weekly New York Arabica Coffee Futures

Weekly London Robusta Coffee Futures

Sugar: New York and London were lower last week. Ideas of increasing Brazil and Asian sugar cane production are keeping sugar prices low overall. The move came despite the UNICA news of reduced sugar production and processing in the latest reporting period in center south Brazil. UNICA said that the production for the last two weeks in December was 65% less than the year before at 1.73 million tons. Sugar production was 64,000 tons, down 73% from the previous year, ane ethanol production was 486 million liters, down 8% from the previous year.

Center-south Brazil, India, and Thailand all have improved production potential. The Brazilian Real has been very weak lately to encourage sugar sales and help keep pressure on prices. Trends are mixed in both markets on the daily charts and on the weekly charts. Indian and Thai sugar mills are expecting strong crops of cane. Supplies available to the market could be less in the next six months due to adverse growing conditions seen in Brazil during the production period. Total Brazil sugar production has been affected by drought seen earlier in the year and the fires that destroyed crops in some areas.

Weekly New York World Raw Sugar Futures

Weekly London White Sugar Futures

Cocoa: New York and London closed higher last week as Ivory Coast port arrivals remain above projec-tions but are expected to fade. There is talk that production will be short of demand for the fourth year in a row, but demand has been weakening. The European grind was down 5.4% from last year and the Asian grind was down 0.52%. Cocoa processing in North America fell in the fourth quarter of 2024 to 102,761 metric tons, down 1.16% from the same period a year earlier.

Cocoa processing in Brazil was 5.5% less. Chart trends are tuning down in both markets on the daily charts. Producers in Ghana and in Ivory Coast have been fighting against too much rain that has made it hard to harvest and deliver crops. It has been very dry in West Africa lately. The trade also noted ICE-certified cocoa stocks have been rising of late, but that overall cocoa supply is set to remain sharply constrained for several seasons due to structural problems in Ivory Coast and Ghana.

Weekly New York Cocoa Futures

Weekly London Cocoa Futures

__

(Featured image by pasja1000 via Pixabay)

DISCLAIMER: This article was written by a third party contributor and does not reflect the opinion of Born2Invest, its management, staff or its associates. Please review our disclaimer for more information.

This article may include forward-looking statements. These forward-looking statements generally are identified by the words “believe,” “project,” “estimate,” “become,” “plan,” “will,” and similar expressions, including with regards to potential earnings in the Empire Flippers affiliate program. These forward-looking statements involve known and unknown risks as well as uncertainties, including those discussed in the following cautionary statements and elsewhere in this article and on this site. Although the Company may believe that its expectations are based on reasonable assumptions, the actual results that the Company may achieve may differ materially from any forward-looking statements, which reflect the opinions of the management of the Company only as of the date hereof. Additionally, please make sure to read these important disclosures.

Futures and options trading involves substantial risk of loss and may not be suitable for everyone. The valuation of futures and options may fluctuate and as a result, clients may lose more than their original investment. In no event should the content of this website be construed as an express or implied promise, guarantee, or implication by or from The PRICE Futures Group, Inc. that you will profit or that losses can or will be limited whatsoever.

Past performance is not indicative of future results. Information provided on this report is intended solely for informative purpose and is obtained from sources believed to be reliable. No guarantee of any kind is implied or possible where projections of future conditions are attempted. The leverage created by trading on margin can work against you as well as for you, and losses can exceed your entire investment. Before opening an account and trading, you should seek advice from your advisors as appropriate to ensure that you understand the risks and can withstand the losses.

ECSP Crowdfunding vs. eWpG Bonds: Overcoming SME Financing Limits

The ECSP Regulation limits annual crowdfunding per project promoter to €5 million, requiring a full prospectus for higher amounts, which delays...

Germany’s Cannabis Reform Shows Limited Risks but Calls for Regulatory Adjustments

Two years after Germany’s partial cannabis legalization, an evaluation finds no significant rise in consumption and some reduction in the...

Ortus Secures €97M Green Loan to Expand Solar Portfolio in Italy

Ortus Power Resources Italy secured a €97 million green, non-recourse loan to refinance 23 MW of operating solar plants and...

Foreign Exchange Markets Walk a Tightrope Amid Geopolitical Tensions and Policy Uncertainty

Foreign exchange markets remain fragile amid geopolitical tensions, monetary shifts, and persistent volatility. The dollar stayed a safe haven without...

Crypto Holds Steady as Tensions Rise and Regulatory Concerns Grow

Crypto markets remained cautious as a US ultimatum to Iran nears expiry. Bitcoin and Ethereum traded sideways despite strong ETF...

|

|

|  |

|

|

-

Fintech2 weeks ago

Fintech2 weeks agoDZ Bank Pioneers Blockchain Bond Issuance, Advancing Tokenized Finance

-

Africa13 hours ago

Africa13 hours agoForeign Exchange Markets Walk a Tightrope Amid Geopolitical Tensions and Policy Uncertainty

-

Markets1 week ago

Markets1 week agoCotton Prices Rise Amid War Tensions, Weather Risks, and Supply Concerns

-

Biotech5 days ago

Biotech5 days agoGilead Sciences Advances Growth Strategy with Focus on HIV, Oncology, and Innovation