Featured

Why Sugar Production in Brazil Could Increase Considerably

New York and London closed higher last week as the US Dollar worked lower. Ideas are that mills in Brazil will be encouraged to produce more Sugar than Ethanol due to policy changes proposed by the Lula administration. These ideas were enhanced by the news that Brazil’s president Lula has frozen fuel taxes at current levels, giving Ethanol producers a reason to switch to Sugar.

Wheat: Wheat markets were higher last week in response to the USDA reports. USDA estimated Winter Wheat planted area at 37 million acres, from 33.3 million last year. However, current ending stocks were estimated at 567 million bushels, from 571 million last month. World ending stock levels were increased due to big Russian production and the difficulty of moving grain from the Black Sea. The quarterly stocks report showed supplies at 1.280 billion bushels now, from 1.377 billion last year. There are still ideas of weak demand and big Russian production that should help foster price weakness in the world market. Russia offered to Egypt earlier this week at what were considered very low prices. The demand for US Wheat in international markets has been a disappointment all year and was hindered by low prices and aggressive offers from Russia. Ukraine is also looking for new business for its crops and Russia is aggressive in the world market as it looks for cash to fund the war. The demand for US Wheat still needs to show up and there is still not enough demand news to help support futures.

Weekly Chicago Soft Red Winter Wheat Futures

Weekly Chicago Hard Red Winter Wheat Futures

Weekly Minneapolis Hard Red Spring Wheat Futures

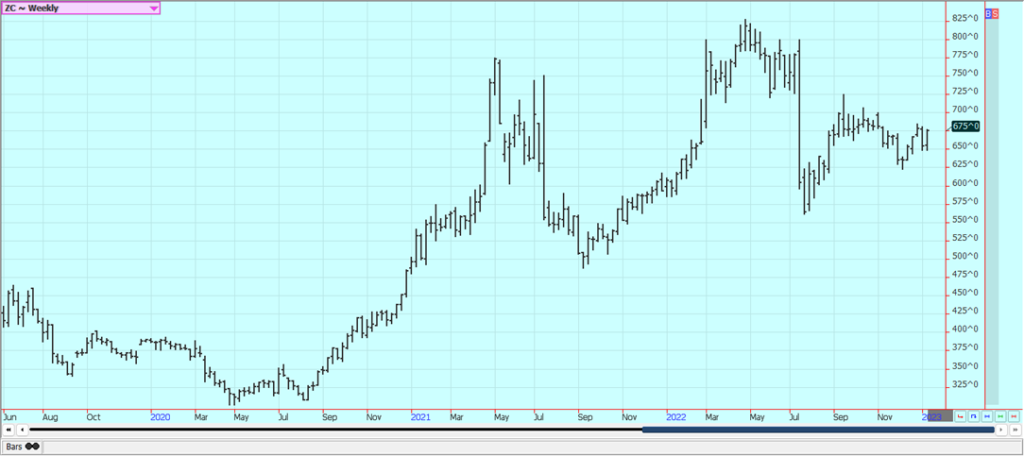

Corn: Corn and Oats closed higher last week in response to the USDA reports that were considered bullish for prices. USDA cut production to just 13,730 billion bushels, from 13.930 billion last year. Both markets remain in trading ranges on the weekly charts. Harvested acreage was cut to account for the loss. Yields were up 1.0 bushels per acre to 173.3 bu/acre. Ending stocks were cut to 1.242 billion bushels for the US and 296.4 million tons for the world. Quarterly stocks showed that current supplies are 10.809 billion bushels, from 11.641 billion last year. Brazil and Argentina estimates were about unchanged. Demand for US Corn remains muted even as forecasts for only light rains or dry conditions in southern Brazil and Argentina were seen. Brazil has been hanging on for its Summer crop but Argentina has suffered through some extreme drought. The Brazil Winter crop is harvested. Weak demand overall for US Corn remains a big problem for the market. There are increasing concerns about demand with the Chinese economic problems caused by the lockdowns creating the possibility of less demand as South America has much better crops this year to compete with the US for sales. China is now moving rapidly to open the economy and allow people to move around with no lockdowns so the demand could start to improve. The improvement might take some time as the Chinese people get Covid, but they should be past this episode in a few weeks and demand might start to improve at that time. South American prices are currently close to or above those in the US.

Weekly Corn Futures

Weekly Oats Futures

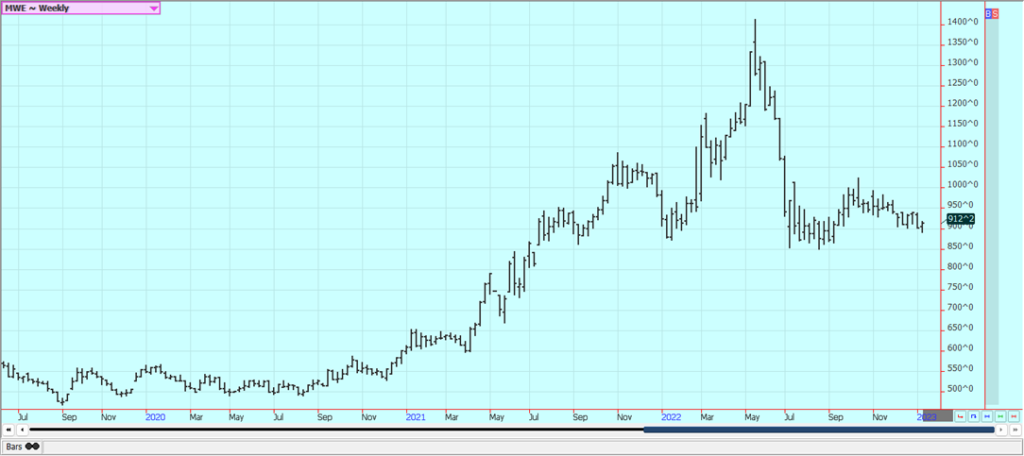

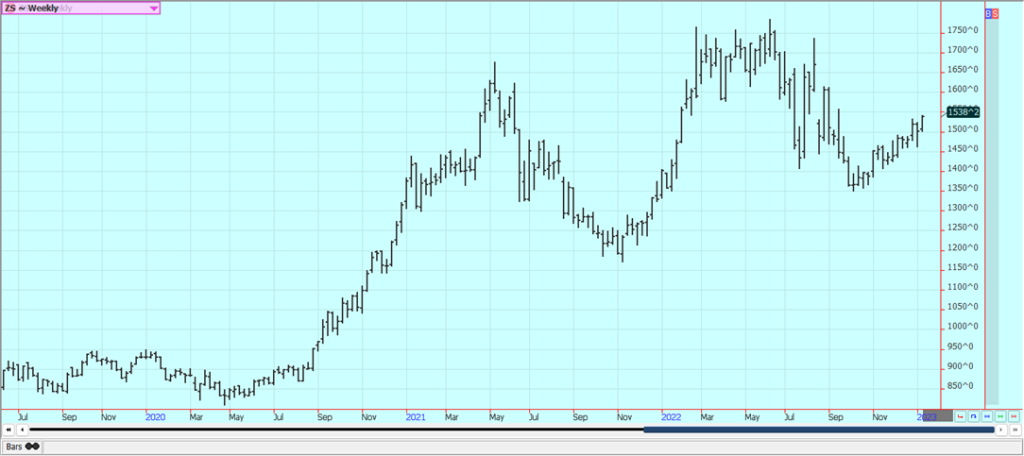

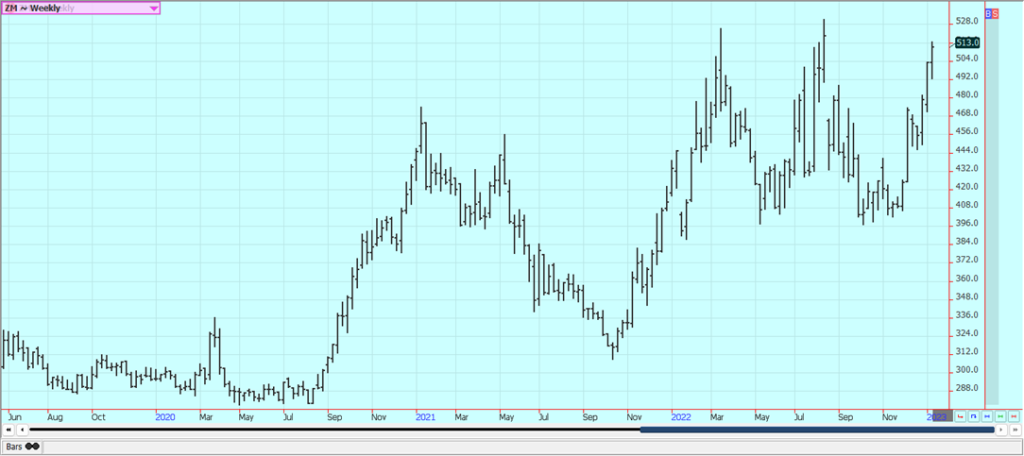

Soybeans and Soybean Meal: Soybeans were higher last week in response to the USDA reports. Soybean Meal also closed higher and made new highs for the move, but Soybean Oil closed a little lower in range trading. USDA showed production at 4.276 billion bushels, from 4.346 billion last year. USDA cut yields a bit and also cut harvested area. US ending stocks were less than expected at 210 million bushels, from 220 million last month. The quarterly stocks report showed that Soybeans supplies are currently at 1.280 billion bushels, from 1.377 billion last year. Brazil and Argentina production estimates were left unchanged. Soybean Meal closed higher on reports that the Argentine Meal basis was at record highs. Farmers are not selling many Soybeans in the US as many are waiting for a rally to sell into. Drier weather is the forecast for this week for southern Brazil and Argentina which could stress crops in both areas again, Current forecasts suggest that the showers will be few and far between and not able to make a real dent in the drought. Central and northern Brazil remain in very good condition with scattered showers reported. Production potential for Brazil is called very strong even with potential problems and losses in the south. Even so, production of less than 150 million tons is possible now. Argentine production ideas continue to drop with the drought as planting is delayed and the crops already in the ground are stressed. Production estimates are now closer to 40 million tons than original projections near 50 million. There was news that China has started to ease Covid restrictions after some demonstrations by the Chinese people. Ideas that Chinese demand will improve, but this could take some time as a very large part of the population now has Covid. This has delayed a robust economic return for the country. Export demand for the US is on pace for what is needed to meet USDA projections.

Weekly Chicago Soybeans Futures:

Weekly Chicago Soybean Meal Futures

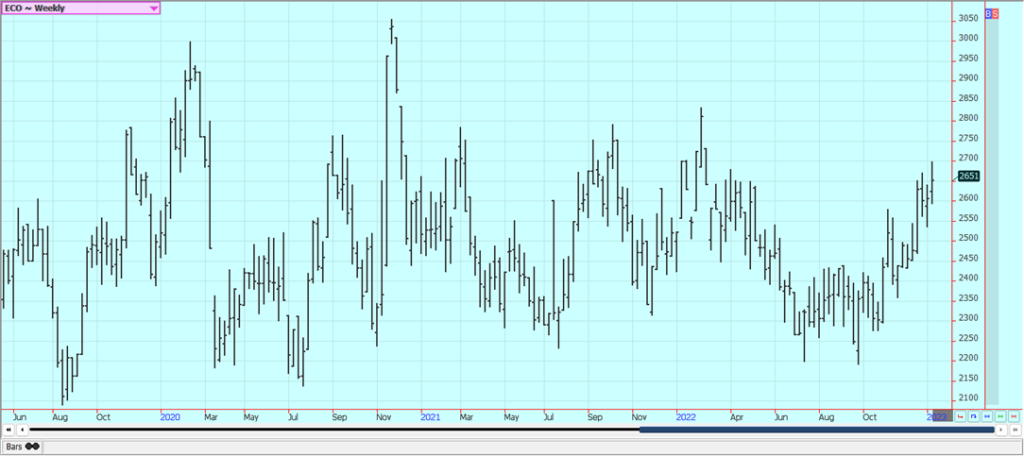

Rice: Rice was higher in response to the USDA reports. USDA estimated US production at 160.4 million cwt this month, from 164.3 million last month. Ending stocks were estimated at 32.1 million cwt, from 38.1 million last month. Long Grain production was estimated at `18.2 million cwt, from 131.7 million last month. Ending stocks were estimated at 21.8 million cwt, from 27.3 million last month. World ending stocks are now estimated at 169.98 million tons, from 168.64 million last month, and are now estimated at 61.98 million tons with China out of the equation, from 60.64 million last month. The US Dollar was sharply lower and world petroleum prices were higher last week to help Rice rally. There is not much going on in the domestic market right now. Most Rice farmers were not paying much attention to the market. Demand in general has been slow to moderate for Rice for both exports and domestic uses.

Weekly Chicago Rice Futures

Palm Oil and Vegetable Oils: Palm Oil closed lower last week as demand ideas remain uncertain and as the production uncertainty continues. Current forecasts call for the rainy season to end soon and for fieldwork and harvest conditions to improve. Indonesia will now permit exporters to sell six tons for every tons sold internally instead of eight as before. Ideas of better demand and less production are still around, with production falling due to seasonal factors. Hopes for improved demand from China were reported. China has tried to relax some Covid restrictions so that the economy can start to function again. However, new outbreaks of the virus are being reported and infection rates are rapidly increasing. Ideas are that supply and production will be strong, but demand ideas are now weakening and the market will continue to look to the private data for clues on demand and the direction of the futures market. There are still reports of too much rain in Malaysia. Canola was lower again last week. Demand for export has been less. Farmers are holding tight to harvested supplies. Reports indicate that domestic demand has been strong due to favorable crush margins. Production was much improved this year on better weather during the Summer.

Weekly Malaysian Palm Oil Futures

Weekly Chicago Soybean Oil Futures

Weekly Canola Futures:

Cotton: Cotton was lower last week and remains firmly inside the trading range created over the last couple of months. The USDA reports were considered bearish as USDA increased domestic production estimates and cut US and world demand to increase ending stocks for both. US ending stocks were estimated at 4.20 million bales, from 3.5 million last month. World ending stocks were estimated at 89.93 million bales, from 89.56 million last month. Ideas of weak demand continue to be heard and the weekly export sales report was poor once again. Futures have been stuck in the same trading range since the beginning of November but are showing bad demand fundamentals. Overall, the demand for US Cotton has not been strong. Some ideas that demand could soon increase as China could start to open its economy in the next couple of months were hurt by news of Covid outbreaks in China. Covid is now widespread in China so the beneficial economic effects of the opening are being delayed but these effects should start to be felt as the people there achieve immunity over the next few weeks.

Weekly US Cotton Futures

Frozen Concentrated Orange Juice and Citrus: FCOJ was a little lower last week despite a late week rally based on smaller Florida production estimates from USDA. Trends are still trying to turn up again on the daily charts. Demand should start to improve now with the holidays now over. USDA estimated Florida Oranges production at just 18 million boxes, from 20 million in its previous estimate. US production was estimated at 2.7 million tons, down 22% from last month. The supply situation in the US and in the world market looks very tight. Historically low estimates of production due in part to the hurricanes and in part to the greening disease have hurt production remain in place but are apparently part of the price structure now. The weather remains generally good for production around the world for the next crop but not for production areas in Florida that have been impacted in a big way by the two storms. Brazil has some rain and the conditions are rated good. Mostly dry conditions are in the forecast for the coming days. The Florida Movement and Pack report showed that inventories are 40% less than last year. Nielsen showed that US stores sold 35.17 million gallons of Orange Juice in December. This is down 7.2% from 2021 and down 5.9% from 2019.

Weekly FCOJ Futures

Coffee: New York was lower and London closed higher last week as Brazil offers increased and those from Vietnam decreased. Ideas of a big production for Brazil continue due primarily to rains falling in Coffee production areas now and as offers stayed strong from Brazil and increasingly from Vietnam. Vietnamese sellers should remain more active in the next couple of weeks as they try to get sales on the books before the Tet holiday. Ideas are that the buy side needs Coffee now. There are ideas that the production potential for Brazil had been overrated and reports of too much rain in Vietnam affected the harvest progress. The weather in Brazil is currently very good for production potential but worse conditions seen earlier in the growing cycle hurt the overall production prospects as did bad weather last year. Ideas are that the market will have more than enough Coffee either way when the next harvest comes in a few months. Vietnam exported 187,077 tons of Coffee last month, up 53% from the previous month. Vietnamese 2022 exports were 13.8% higher than in 2021.

Weekly New York Arabica Coffee Futures

Weekly London Robusta Coffee Futures

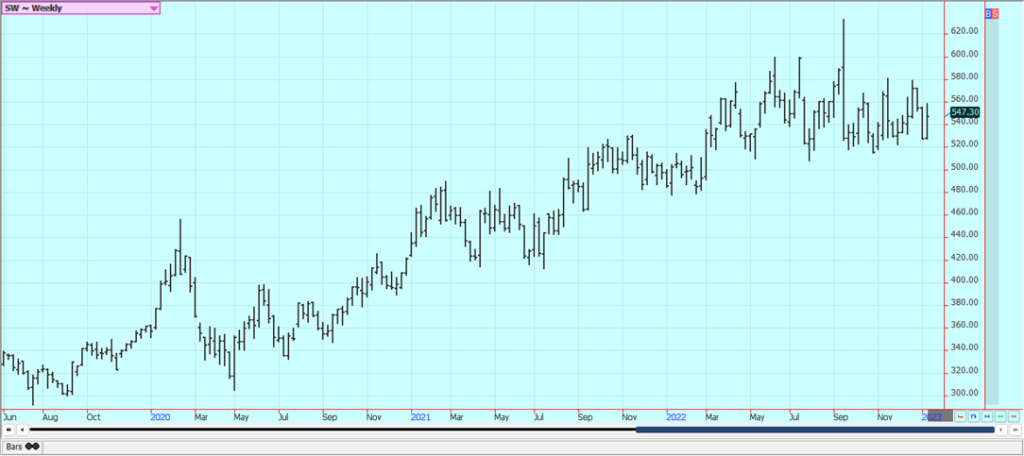

Sugar: New York and London closed higher last week as the US Dollar worked lower. Ideas are that mills in Brazil will be encouraged to produce more Sugar than Ethanol due to policy changes proposed by the Lula administration. These ideas were enhanced by the news that Brazil’s president Lula has frozen fuel taxes at current levels, giving Ethanol producers a reason to switch to Sugar as Ethanol profit margins could be squeezed by the tax moves. The harvest has been delayed in Thailand. Australian and Central American harvests are also delayed. There is talk that production in India will be reduced this year after some bad weather and reduced yields reported in Maharashtra. The weather in Brazil remains good for the next crop but bad for harvest and loading at ports as it is still raining in production areas. World Sugar is expected to be in a big surplus production next year. Unica said last week that Brazil mills crushed 2.6 million tons of Sugarcane in the last two-week period, from just 8,500 tons in the same period last year. The mills produced 165,000 tons of Sugar and 322.2 million liters of Ethanol.

Weekly New York World Raw Sugar Futures

Weekly London White Sugar Futures

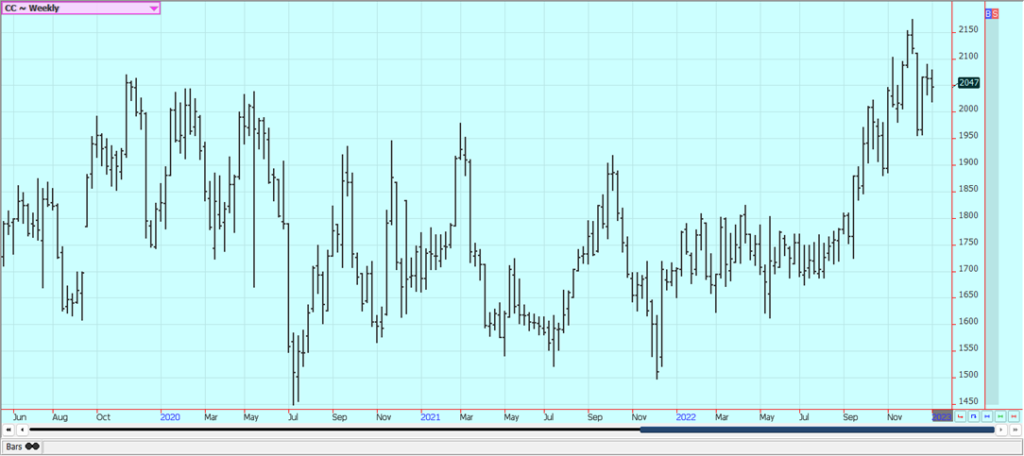

Cocoa: New York and London closed lower last week with the biggest losses in New York due to currency considerations. Ivory Coast arrivals appear to have improved lately with the recent rally in futures prices. Ivory coast arrivals are now 1.172 million tons, up 14% from last year. The Ivory Coast Cocoa grind is now 113,803 tons, up 6.9% from last year. Good production is reported and traders are worried about the world economy moving forward and how that could affect demand. Supplies of Cocoa are as large as they will be now for the rest of the marketing year. Reports of scattered showers along with very good soil moisture from showers keep big production ideas alive in Ivory Coast. Nigeria is reporting that Harmattan winds have arrived, but no significant effects are reported for now. The weather is good in Southeast Asia.

Weekly New York Cocoa Futures

Weekly London Cocoa Futures

__

(Featured image by Faran Raufi via Unsplash)

This article may include forward-looking statements. These forward-looking statements generally are identified by the words “believe,” “project,” “estimate,” “become,” “plan,” “will,” and similar expressions. These forward-looking statements involve known and unknown risks as well as uncertainties, including those discussed in the following cautionary statements and elsewhere in this article and on this site. Although the Company may believe that its expectations are based on reasonable assumptions, the actual results that the Company may achieve may differ materially from any forward-looking statements, which reflect the opinions of the management of the Company only as of the date hereof. Additionally, please make sure to read these important disclosures.

Futures and options trading involves substantial risk of loss and may not be suitable for everyone. The valuation of futures and options may fluctuate and as a result, clients may lose more than their original investment. In no event should the content of this website be construed as an express or implied promise, guarantee, or implication by or from The PRICE Futures Group, Inc. that you will profit or that losses can or will be limited whatsoever. Past performance is not indicative of future results. Information provided on this report is intended solely for informative purpose and is obtained from sources believed to be reliable. No guarantee of any kind is implied or possible where projections of future conditions are attempted. The leverage created by trading on margin can work against you as well as for you, and losses can exceed your entire investment. Before opening an account and trading, you should seek advice from your advisors as appropriate to ensure that you understand the risks and can withstand the losses.

The TopRanked.io Weekly Digest: What’s Hot in Affiliate Marketing [LiveChat Affiliates Review]

Quick Disclosure: We’re about to tell you how LiveChat Affiliates run a top-notch affiliate program. And we really mean it....

German SMEs Face Tighter Bank Lending, Turn to Alternatives

Access to bank loans for German SMEs is tightening despite strong financing needs. About 37.8 percent face restrictive lending, driven...

Bitcoin Stalls as Geopolitical Risks and Crypto Industry Tensions Persist

Bitcoin is moving sideways near $72,000 amid ongoing Iran tensions, while ETF inflows remain strong. Quantum security debates continue. Ethereum...

Geopolitical Tensions and Trade Disruptions Reshape Global Commodities Markets

Geopolitical tensions and disrupted trade routes, especially around the Strait of Hormuz, are reshaping global commodities markets. Agriculture faces supply...

Germany Sees 413 Cannabis Cultivation Clubs Two Years After Partial Legalization

Two years after partial cannabis legalization in Germany, 413 cultivation clubs have been established nationwide. Lower Saxony leads in clubs...

|

|

|  |

|

|

-

Impact Investing2 days ago

Impact Investing2 days agoSwitzerland Aligns Corporate Sustainability Rules with EU Standards

-

Cannabis1 week ago

Cannabis1 week agoLowryder: The Autoflowering Revolution in Cannabis Cultivation

-

Impact Investing5 days ago

Impact Investing5 days agoWhy 2026 Could Mark a Turning Point for Sustainability

-

Business2 weeks ago

Business2 weeks agoTopRanked.io Weekly Affiliate Digest: What’s Hot in Affiliate Marketing [1xBet Affiliate Program]