Business

What’s new in the agriculture market this week (December 5-11)

US domestic markets remain mostly quiet, but reports indicate that supplies in temporary storage are disappearing.

Weekly commentary and analysis of the U.S. agriculture market. What are this week’s the essential changes in the market?

Wheat

US markets were mixed last week, with the Chicago markets closing higher and Minneapolis closing lower. The leader to the upside was Soft Red Winter, with Hard Red Winter posting smaller gains. It was a small reversal in the strong trend this year in the protein spreads. The higher quality and higher protein Wheat has held a significant and increasing premium, and the spread differentials remain very strong between Minneapolis and the Chicago markets. Meanwhile, Soft Red Winter and Hard Red Winter are trading at parity, when normally Hard Red Winter also carries a price premium due to higher protein.

This result comes despite reports of huge supplies of lower quality Wheat available in the world market, so something is going on. USDA released its monthly supply and demand update on Friday. It left US estimates unchanged, which met general expectations of the trade. It increased world production and ending stocks levels due to better production in Australia. West Australia suffered from a hard freeze in October, and significant production losses were expected. Instead, ABARES and USDA are forecasting record production for the country. Australia has been active in the world market and has sold at least 500,000 tons to India and smaller amounts in Southeast Asia. Philippines bought 55,000 tons of Australian Wheat last week.

The market is also watching US weather. It will be very cold in the Midwest and Great Plains this week, with damaging cold possible. Wheat in the Great Plains has been poorly established due to the dry weather and might not have the root development in some areas to withstand the cold. Production losses are possible in the Great Plains this week from Kansas to the south. The best potential for losses should be in Kansas.

Weekly Chicago Wheat Futures © Jack Scoville

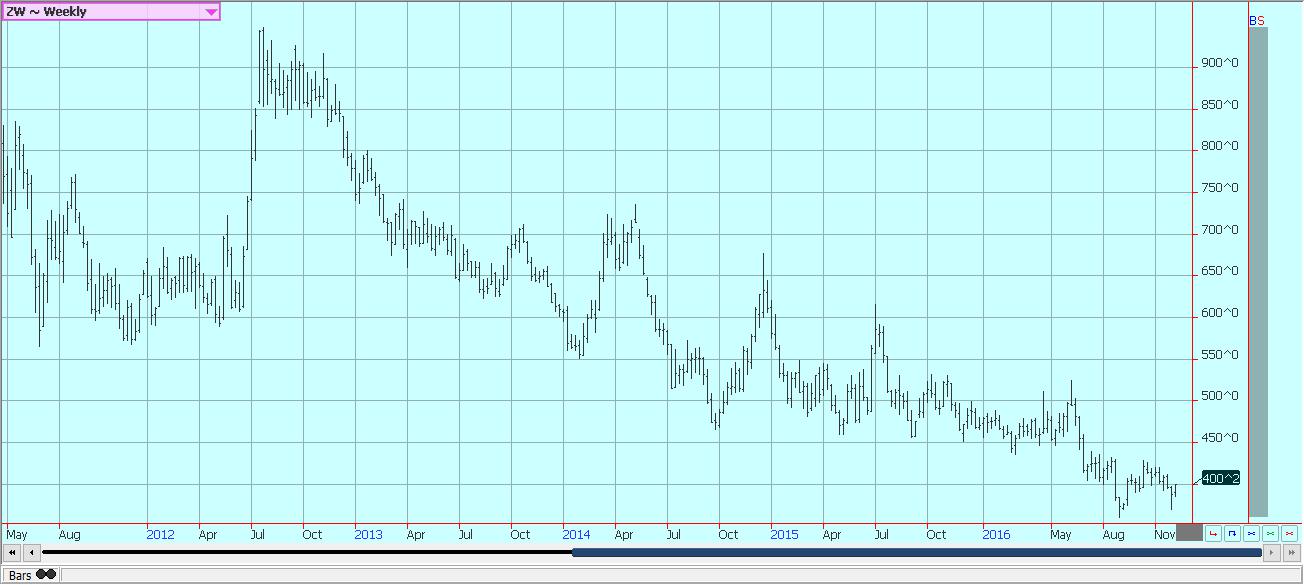

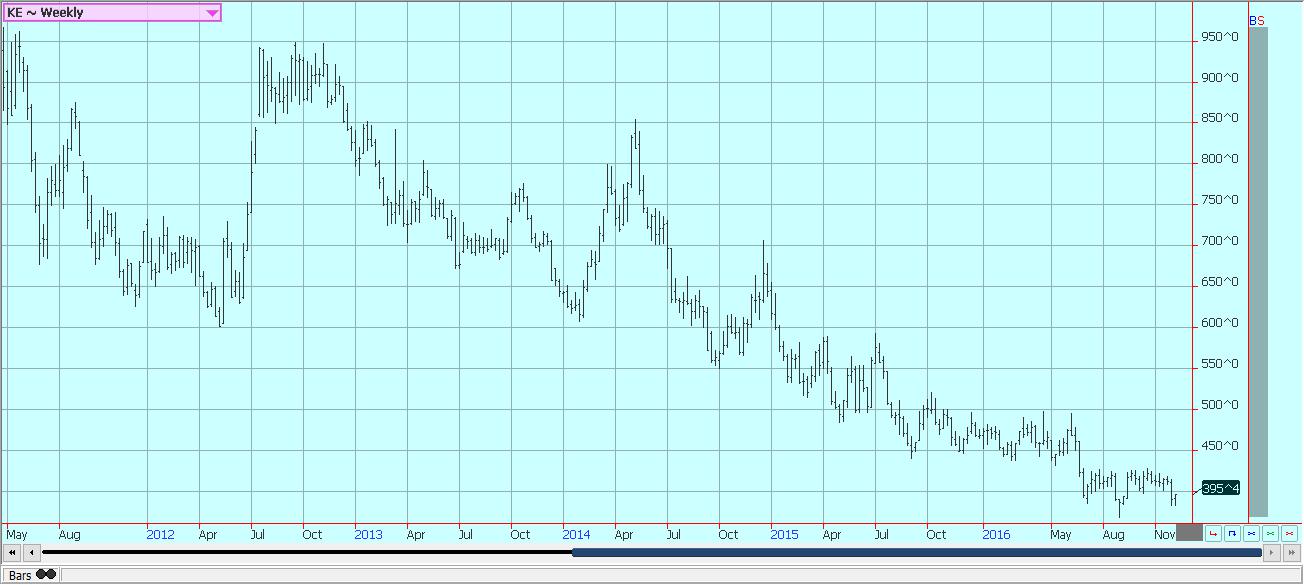

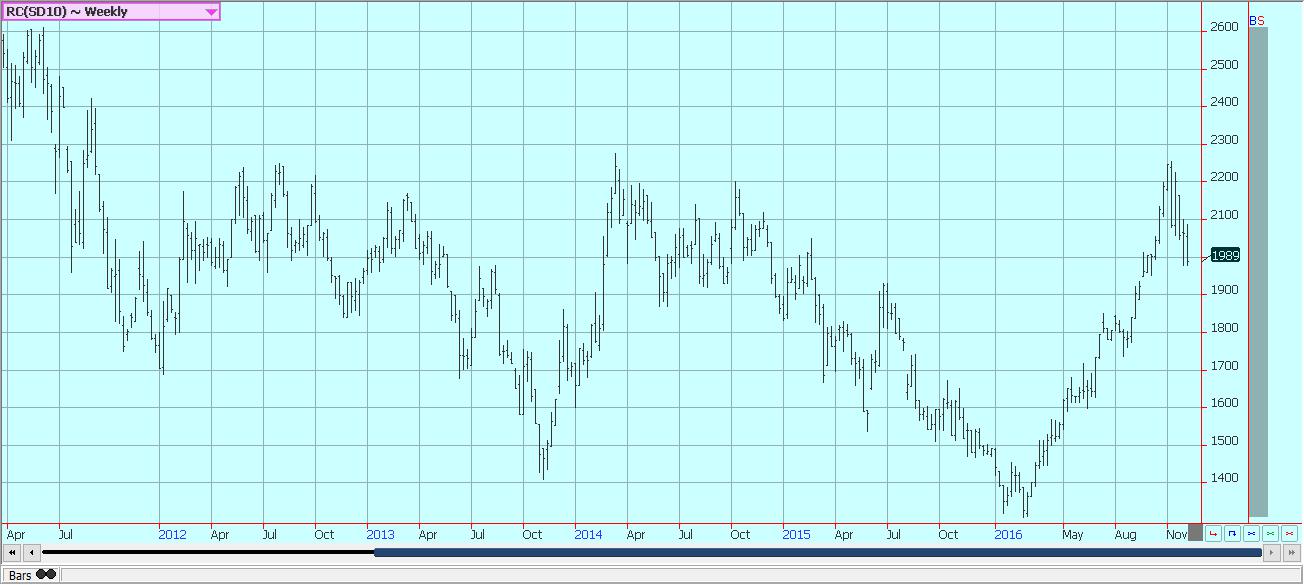

Weekly Kansas City Wheat Futures © Jack Scoville

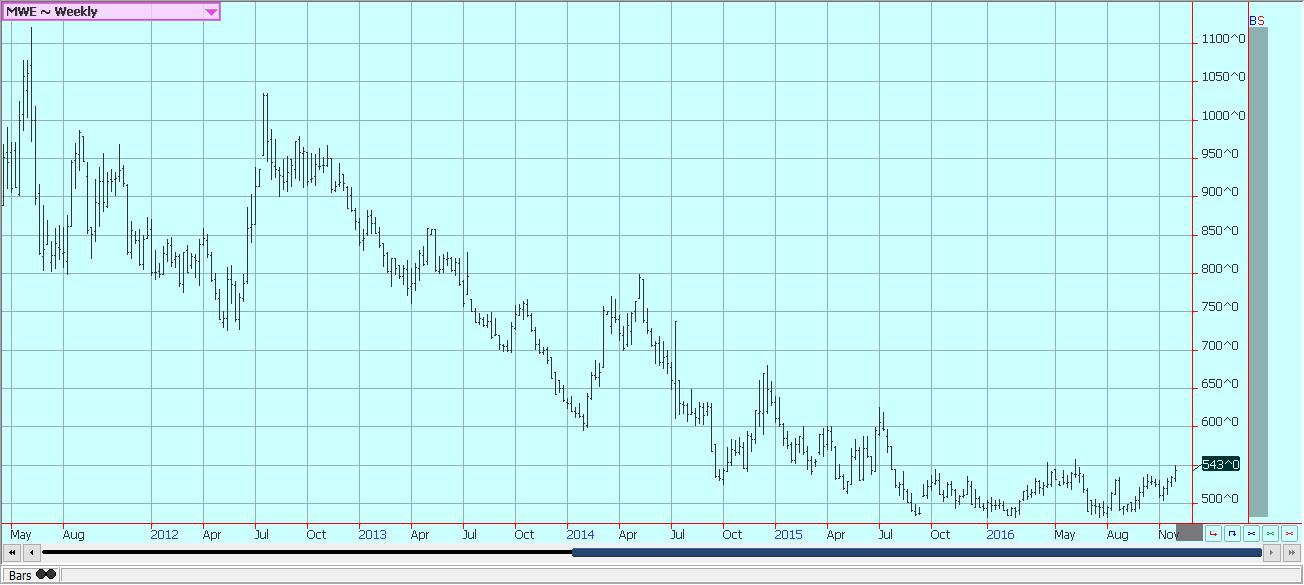

Weekly Minneapolis Wheat Futures © Jack Scoville

Corn

Corn closed higher on Friday and higher for the week. The weekly charts show that futures are in position to move higher. The daily charts show that futures remain locked in a sideways trend. The monthly USDA estimates were considered neutral to negative for prices by the trade. The reports were released on Friday and showed no changes for the US supply and demand estimates. World ending stocks estimates were above the average trade guess due to stronger than expected production in China.

China has made changes to its Corn support program and no longer buys at a high fixed price. However, the changes were announced too late for farmers who had already bought inputs and planted the Corn. The US export sales pace remains strong on a weekly basis and should stay strong into next year, or until some Corn becomes available for export in South America. That might take a little longer than normal as South America, especially Brazil, remains short of Corn due to bad growing conditions last year.

US domestic markets remain mostly quiet, but reports indicate that supplies in temporary storage are disappearing. These ideas should help keep a firmer tone under the futures market. The market will need to bid up for Corn from producers as prices remain relatively cheap and below the cost of production for many. It might be easier for futures prices to continue sideways to higher in the short to medium term.

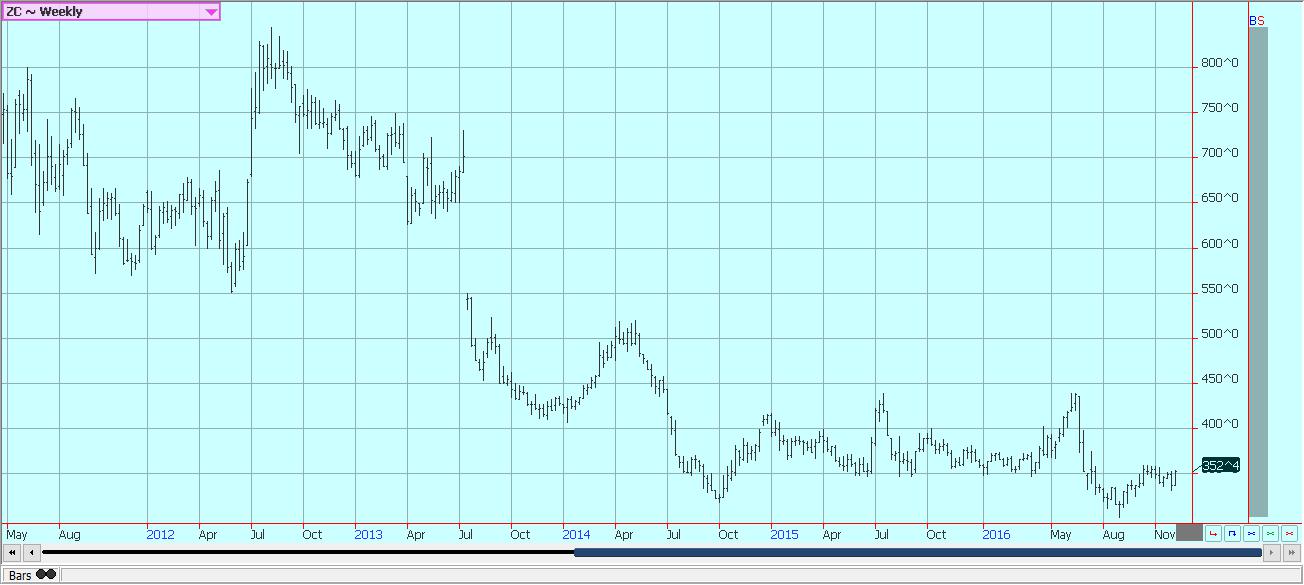

Weekly Corn Futures © Jack Scoville

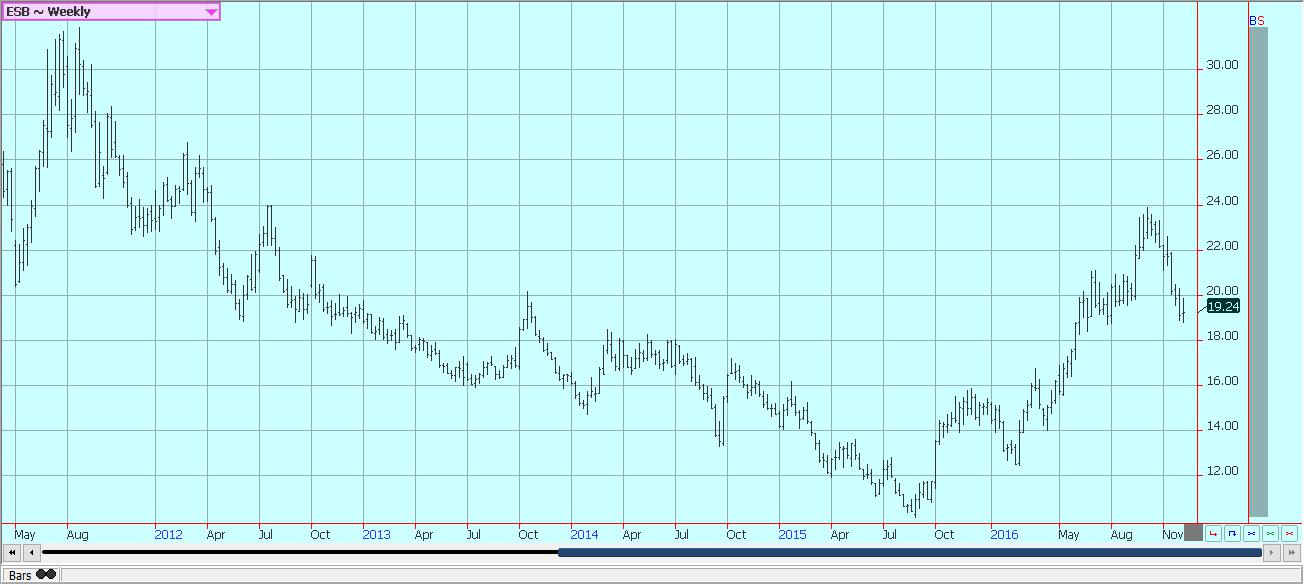

Weekly Oats Futures © Jack Scoville

Soybeans and soybean meal

Soybeans and Soybean Meal were higher last week. USDA issued its monthly supply and demand estimates on Friday and made no important changes to the ideas for Soybeans and Soybean Meal. US demand remains very strong with another strong export sales report last week. However, the market seems to has stalled on the daily and weekly charts. There are concerns that demand will soon shift to South America, and the focus of the market is starting to turn in that direction in any case.

China is buying in South America as well as the US as it fills in its pipeline for the first part of next year. Crops have been progressing well in northern Brazil and there is some talk that Soybeans could show up at ports for export by the end of January. This would be a very early start to the export season if true. It is possible that Soybeans will be available by then, but US demand should only be fading at that point. It will take some time before the bulk of the demand can be covered by both Brazil and Argentina. The US has more time to enjoy strong sales and shipments. Domestic demand has been strong as NOPA and USDA crush data has generally been stronger than expected. USDA had been expected to cut US ending stocks slightly due to the increased crushing pace, but left all data alone for the month. It did increase South American ending stocks estimates for the coming year despite unchanged production.

Some concern is noted in the trade about dry conditions fin Argentina. It should be dry there again this week, but some rain is in the forecast for next week. Either way, the crop is still being planted and raion needs are less right now. The market will get much more interested in South American weather next month as flowering spreads from north to south. The region has the potential for a big crop this year, but the crop is not yet made. La Nina years often produce droughts in southern Brazil and northern Argentina, so the market will closely watch the weather. Conditions are good to very good in Brazil and adequate in Argentina right now.

Weekly Chicago Soybeans Futures © Jack Scoville

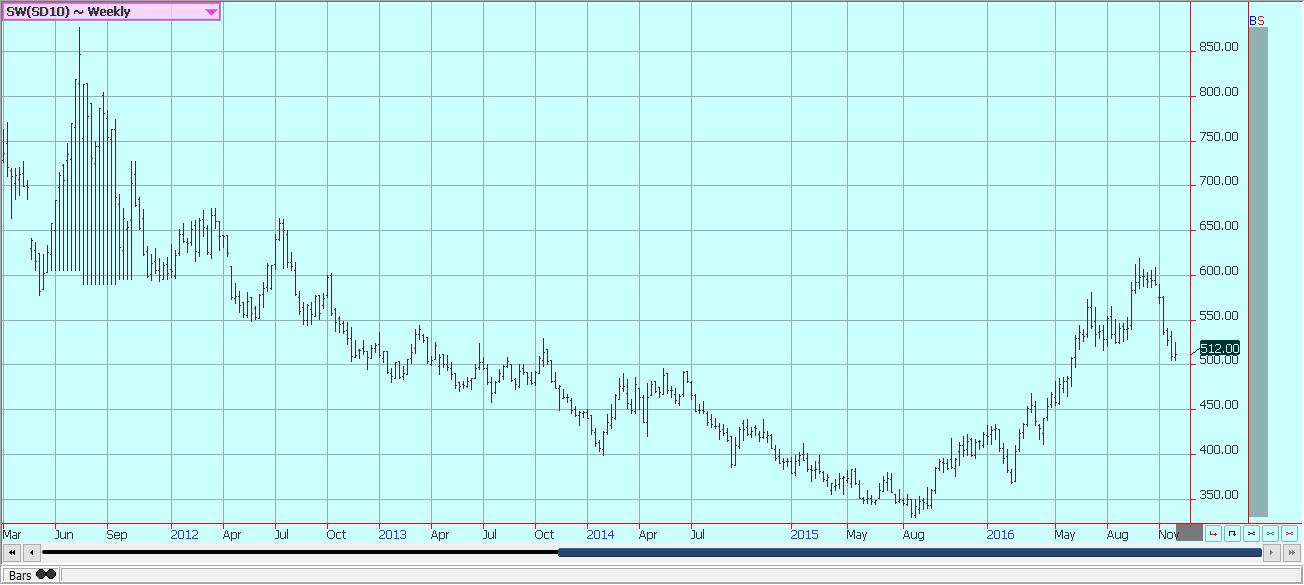

Weekly Chicago Soybean Meal Futures © Jack Scoville

Rice

World markets were mostly stable to higher last week. USDA released its monthly supply and demand estimates on Friday and made no changes of significance to the US data. It did trim world ending stocks levels due to smaller supplies in some Asian countries including China. Chinese ending stocks were reduced by about 1.0 million tons. The futures market is showing the potential for prices to rally during the holiday period, with objectives of 1050 and about 1100 seen on the weekly charts. Producers in the US are not selling, but mills and exporters have been quiet as well. The domestic cash market is likely to stay quiet through the holidays.

World traders are watching India. The new monetary regime has served to paralyze the agricultural markets for the short term. The country might experience a short term lull in exports that could create some buying interest for Southeast Asian or US Rice. There was some increased movement in the markets in India last week, but the situation remains far from normal. It should start to slowly loosen up as time goes on. The US market is starting to look ahead to next year. Current low prices are well below the cost of production for virtually all US producers and educed planted area is expected next year. Acreage could drop 15% on a year to year basis unless prices and market conditions improve.

Weekly Chicago Rice Futures © Jack Scoville

Palm Oil and vegetable oils

It was a lower week for world vegetable oils markets. Only Palm Oil managed to close with a fractional gain for the week. It was a disappointing week of price action, and lower prices are possible this week. Palm Oil got new data from MPOB on Monday. The trade had expected weaker production and weaker demand. Palm Oil demand has been falling due to market reforms in both India and China, two large traditional buyers of Palm Oil. Exports from the private surveyors in Malaysia have been dropping for the last couple of months and Indonesian demand has been on the wane as well. The demand loss has caused the rally in Palm Oil futures to stall in the last week.

Trends are still up on the weekly charts, but the weak close last week implies that the current leg of the rally might be running out of steam. Soybean Oil and Canola posted losses last week. Soybean Oil was weaker despite positive demand reports. South Korea bought 20,000 tons of US Soybean Oil last week, and, on Friday USDA increased its biofuels demand and cut ending stocks in line with the modified targets set by the EPA. However, the market is concerned about the new energy nominee for the government. The nominee is known to favor petroleum and has shown disdain for biofuels and alternative fuels development. The new administration could work to roll back a lot of the mandates in the near term and hurt demand potential overall.

Weekly Malaysian Palm Oil Futures © Jack Scoville

Weekly Chicago Soybean Oil Futures © Jack Scoville

Weekly Canola Futures © Jack Scoville

Cotton

Futures were lower last week and were lower on Friday in response to the latest USDA supply and demand estimates. USDA increased production and ending stocks in the reports, but left its average form prices about unchanged. Demand was unchanged overall, but featured less domestic demand and more export demand. The world data featured more production and greater ending stocks. The reports were considered bearish as the ending stocks estimates were above trade ideas. The weekly classing report showed that the crop is still featuring good quality as the harvest starts to wind down. The price action last week was not strong, but prices held above most important resistance areas. Speculators in general are very long and might look to lighten these positions, so more selling is possible this week.

The situation in India remains one of only slow market activity. The government monetary moves have made business difficult as many producers have not been selling until more clarity about the overall economic situation is seen. The market has started to open a little more, but activity remains well below normal. Pakistan and India are having another war of words over Kashmir, and Pakistan is moving to ban Indian imports including Cotton. The demand from China is quiet at the moment as the domestic market absorbs its own harvest. Southeast Asia was the strongest buyer in the USDA weekly export sales report, with Vietnam the best buyer overall at over 100,000 bales. Export demand for US Cotton should remain strong.

Weekly US Cotton Futures © Jack Scoville

Frozen concentrated orange juice and citrus

FCOJ closed mixed on Friday, with nearby months a little lower and deferred months a little higher. USDA left production estimates for Florida Oranges unchanged in its monthly reports. This was mostly in line with trade ideas. It did reduce juice yields and that should support prices. The freeze season is here as very cold temperatures have invaded central parts of the US. There are no frosts or freezes in the forecast for Florida, but it has turned cooler.

Less Florida production and also less production in Brazil are the main market support factors. Brazil also suffers from the greening disease. The Florida harvest is moving forward, but harvest progress has been slow and progress is called behind normal. Irrigation has been used in Florida and is being used frequently at this time due to dry conditions. Fruit is moving to packing houses for the fresh trade, with only small amounts moving to processors. In Brazil, Sao Paulo state is getting good weather and crop development is called good.

Weekly FCOJ Futures © Jack Scoville

Coffee

Prices were lower once again last week in New York and in London. The weakness in London came on less demand for Robusta against Arabica, but also on news that the Vietnamese Coffee was starting to flow to ports and that production appeared to be solid. New York saw some selling pressure as trends remain down on the charts. New York has moved through swing targets on the daily charts and initial swing targets on the weekly charts. It has additional swing targets of about 122.00 on the weekly charts.

Differentials paid in Central America appear stable at weak levels. Differentials are also stable in Colombia. Brazilian producers are said to be more active sellers and as exports remain very strong at over 3.0 million bags for last month. The market has turned weaker as futures adjust to increased supply potential. Roasters have become more withdrawn in the marketplace due to the recent surge in prices, and now due to the price weakness. They will probably start to buy again if a more stable price outlook appears. They are waiting fow now and might not get real active until after the holiday season.

Weekly New York Arabica Coffee Futures © Jack Scoville

Weekly London Robusta Coffee Futures © Jack Scoville

Sugar

Futures closed higher last week as New York held a support area about 1900 on the weekly charts. Futures started to slide again late last week, and it is possible that a harder test of support will be seen this week. Price action overall remains negative on worries about overall demand potential and on bigger than expected exports from Brazil. Demand news remains bearish for futures prices. China has imported significantly less Sugar in the last couple of months as it starts to liquidate massive supplies in government storage by selling them into the local cash market.

The Brazilian Real has moved sharply lower in the past couple of weeks and kept mills in a selling mode. There could be smaller crops coming from India and Thailand due to uneven monsoon rainfall in Sugar areas in both countries. India has said that its production and amounts in storage are sufficient and that there is no need for imports that had been expected earlier. The weather in other Latin American countries appears to be mostly good as rains remain sufficient. Most of Southeast Asia has had good rains.

Weekly New York World Raw Sugar Futures © Jack Scoville

Weekly London White Sugar Futures © Jack Scoville

Cocoa

Futures markets were lower again. Trends are down in both New York and London. Overall price action remains weak as the main crop harvest continues in West Africa under good weather conditions. However, some buying did appear last week as prices have moved to levels not seen in a long time. Speculators are mostly done liquidating and some commercial buying has been noted. Reports indicate that consumptive demand is increasing at these lower price levels. The demand from Europe is reported improved based on some corporate data released in the last few weeks.

However, all eyes were on the Italian referendum last weekend and its results as European demand needs to stay stronger and improving for demand to stay stronger at this time. The next production cycle still appears to be bigger as the growing conditions around the world are generally improved. West Africa has seen much better rains this year and alternating warm and dry weather with the rains. There have been some reports of disease to crops in the wetter areas, but so far there is not a lot of market concern. Bigger production is expected this year in all countries. East Africa is getting enough rain now, and overall production conditions are now called good. Good conditions are still being reported in Southeast Asia.

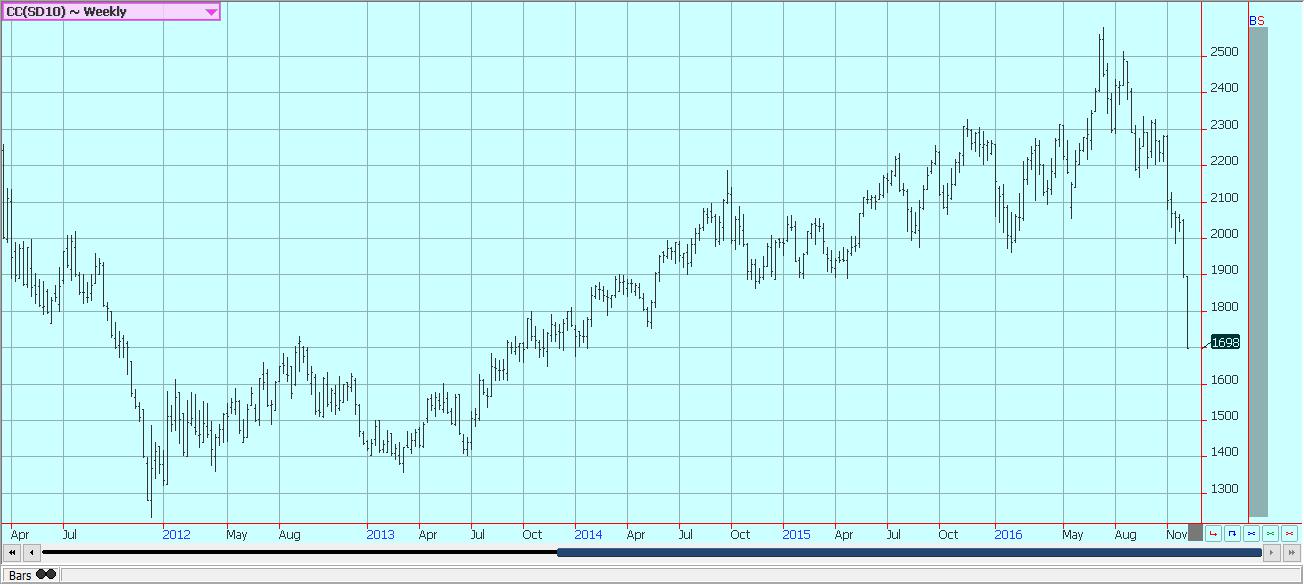

Weekly New York Cocoa Futures © Jack Scoville

Weekly London Cocoa Futures © Jack Scoville

Dairy and meat

Dairy markets were firm as good supply met very good demand. Butter and cheese manufacturers report strong demand, but expect demand to fall off now as the holiday season is here. Butter manufacturers are shifting from producing print butter to producing bulk butter. Most have good supplies on hand, but inventory has been moving. Cream demand has been strong in the domestic and world market, with Mexico and Canada showing buying interest. Cheese demand is being met with strong milk supplies and manufacturing is active.

Fresh cheese markets are in balance at this time, but aged cheese inventories are said to be high. Raw milk production has also been stronger, with only the Pacific Northwest reporting less production due to weather stress. Dried products prices are mixed to firm. Whey prices are strong, and whole milk prices are firm. NDM prices are weak. International markets are featuring higher prices due to reduced production. Production is less in Europe and Russia. Production is down in Australia, but has increased lately in New Zealand due to the uptick in prices. South American prices are starting to firm as raw milk production goes into a seasonal decline.

US cattle and beef prices were higher last week in reaction to reports of higher beef prices and despite lower prices paid in cattle markets. Cash cattle markets traded at lower prices at the end of last week and in moderate volumes. However, prices paid in the cash markets were above futures. The charts show that market could move higher. Demand is starting to improve overall as the wholesale market anticipates good holiday demand and also better demand into the new year. Australia has less to offer and very high prices. Herd culling has slackened in both Australia and New Zealand. Pasture conditions in both countries is better than a year ago on colder and wetter weather seen until now.

Pork markets have been firm, and live hog futures trends are higher. Pork demand has been stronger than expected and a primary ham consumption period is here with the holidays. Pork prices have trended higher in retail and wholesale markets. There has been a lot of featuring in supermarkets in the US. Pork demand should remain strong for the next couple of weeks as hams and other cuts will be featured for holiday buying. US export demand should start to improve on the lower prices. The charts show that the market could remain higher.

Weekly Chicago Class 3 Milk Futures © Jack Scoville

Weekly Chicago Cheese Futures © Jack Scoville

Weekly Chicago Butter Futures © Jack Scoville

Weekly Chicago Live Cattle Futures © Jack Scoville

Weekly Feeder Cattle Futures © Jack Scoville

Weekly Chicago Lean Hog Futures © Jack Scoville

–

DISCLAIMER: This article expresses my own ideas and opinions. Any information I have shared are from sources that I believe to be reliable and accurate. I did not receive any financial compensation in writing this post, nor do I own any shares in any company I’ve mentioned. I encourage any reader to do their own diligent research first before making any investment decisions.

Temenos to Acquire Additiv to Boost AI Wealth Management

Temenos is acquiring Zurich fintech Additiv to strengthen its digital wealth management and expand AI-driven financial orchestration. Additiv’s platform connects...

EFPIA Warns Limited SPC Reform Could Weaken EU Pharma Competitiveness

EFPIA supports the EU Biotechnology Law and a 12-month SPC extension but warns the current proposal is too limited. A...

EU Approves €23B Italian Renewable Energy Plan to Boost Climate Goals

The European Commission approved Italy’s €23 billion aid scheme to boost renewable energy and meet 2030 climate goals. Supporting wind,...

Institutional Bitcoin Buying and LiquidChain Presale Signal Market Optimism

Institutional Bitcoin buying, like Strategy’s 1,550 BTC purchase, signals confidence, stabilizes prices, and may trigger bullish momentum. Meanwhile, infrastructure projects...

The German Biotech Industry Faces Funding Crunch Despite Market Stability

German biotech held steady in 2025 but faces ongoing financing pressures, according to EY-Parthenon and BIO Deutschland. Total capital fell...

|

|

|  |

|

|

-

Biotech1 week ago

Biotech1 week agoArgentina Expands Flu Vaccine Production Through PAHO Partnership

-

Biotech1 day ago

Biotech1 day agoThe German Biotech Industry Faces Funding Crunch Despite Market Stability

-

Crypto1 week ago

Crypto1 week agoCardano in Decline as Hoskinson Distances Himself Amid Growing Uncertainty

-

Cannabis2 weeks ago

Cannabis2 weeks agoHemp Boom to Bust: America’s Regulatory Reset and Europe’s Warning

You must be logged in to post a comment Login