Featured

The bear market is not over, but investors can still find opportunities

Week 8 of the lockdown and everyone is trying to reopen and trying to come up with the cure. But pandemics are rarely one, and historically have come in waves. April lived up to its reputation as the best month of the year as stock markets enjoyed a sharp recovery. That brought out the bulls declaring the bear is over and long live the new bull. But is it? Probably not.

To open, or not to open, that is the question. Do we get a vaccine soon, or will it really take up to 18 months? Closing the economy was controversial. And opening it up is also a source of controversy and heated debate. There are those who believe it was foolhardy to shut down the economy in the first place, that we should have followed the Swedish model who kept their economy open. A quick check, however, reveals that Sweden’s case rate is 1.7 times higher than their fellow Scandinavian countries and their death rate is 5.4 times higher. There is even a comparison with Canada and the U.S. where Sweden’s case rate is 1.5 times higher than Canada, but compared to the U.S., the U.S is worse—1.6 times higher than Sweden. However, when it comes to deaths, Sweden’s death rate is 3.2 times higher than Canada and almost 1.4 times higher than the U.S. At these rates, calculated on the basis of per million of population, Sweden is doing worse than everyone except the U.S. when it comes to the number of cases per million population. (Source: www.worldometers.info/coronavirus)

That doesn’t carry everywhere and Sweden on that basis is outperforming the U.K., France, Spain, and Italy. Still, some have described the shutting down of the economy as possibly the “most inept stupidity in all of human history.” While they note that the Spanish flu of 1918–1920 did not cause this much damage to the economy, there was a steep post-war recession from August 1918 to March 1919, followed by an even steeper depression from January 1920 to July 1921 that was triggered in no small part by the Spanish flu.

But keep in mind that 1918–1920 populations were lower, just over 50% of the population were primarily in agriculture in a rural setting, and the economy wasn’t as interlocked as it is today, nor was the service economy as large as it is today, nor was the consumer as dominant. The service economy back then was only about 25% of the economy. Today it is 85%. What was the most stable part of the economy has now become the most unstable.

So, what will the coronavirus COVID-19 pandemic bring us? For starters, Q1 advance GDP fell 4.8% which was higher than the consensus of 4%. Some are expecting Q2 GDP to be even worse with a decline of up to 25%. Personal income for March fell 2% and personal spending fell a sharp 7.5% when the expectation was for only a decline of 5%.

Opening the economy is fraught with danger as another spike could occur. Pandemic flus tend not to come in “one and done.” They come in waves. The Spanish flu occurred in three waves: the first in the spring of 1918, the second in the fall of 1918, and the third and final wave in the winter of 1918. The second wave was the deadliest in terms of the number of cases and deaths. Will a vaccine make a difference and prevent or at least slow a second wave? Gilead Science’s remdesivir drug appears to at least shorten the time it takes for COVID-19 patients to recover, from 15 days to 11. There was also a trend to fewer deaths using the drug. Thoughts of opening the economy, plus the potential of remdesivir, helped spark a huge stock market rally. However, to put remdesivir in perspective, the sample size is small and its potential use is still months away. The drug appears to speed up recovery, but it is not a vaccine.

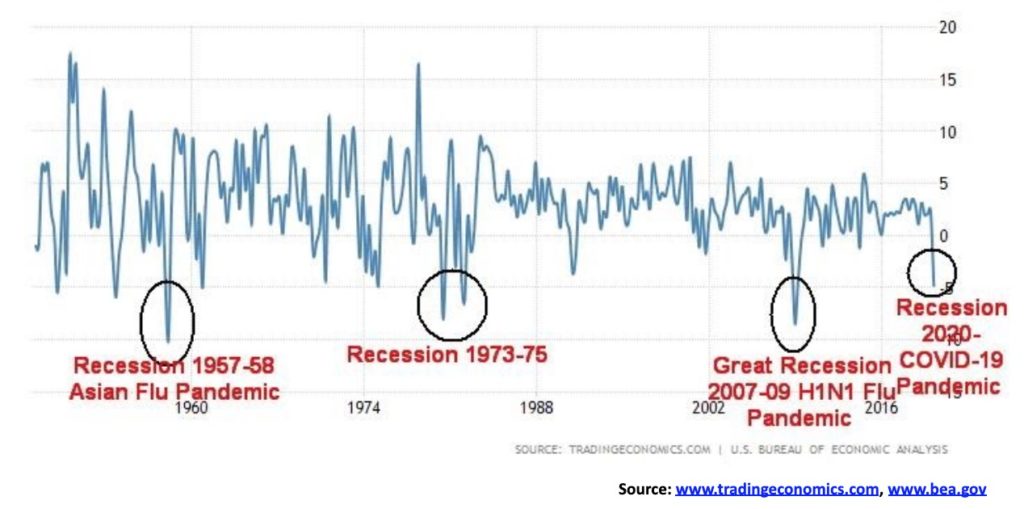

History shows that all pandemics come in waves. The Black Death of the 14th century was recorded over a period of years from 1346–1353; the bubonic plagues of the 17th century reoccurred over most of that century, popping up in different parts of the Western world with deadly effect; the smallpox plagues that destroyed the native populations of North America started in the 16th century but were still breaking out into the 19th century . Going back even further, the first recorded plague of the 5th century BC in Athens had three waves: 430, 429, and 427–426. The great plague of Antonine reoccurred over a number of years from 165–180 AD and played a major role in starting the decline of the Roman Empire. The Great Plague of Justinian occurred mostly over a 2-year period from 541–542 AD and played a major role in plunging the Western world into the Dark Ages. Even the Asian flu of 1957–1958 took place over part of a 2-year period and then reoccurred in the early 1960s.

Closing the economy is one thing. But closing it, then opening it, and then finding you have to close it again could prove to be even more costly than closing it and keeping it closed. But the economic pressure to reopen is huge, given that we are already reading of the potential for scores of bankruptcies and sharply rising unemployment, particularly in the retail, service, hospitality, and tourism sectors. Government largesse to bail out the economy is exploding. Already U.S. government debt to GDP has hit 116% with budget deficits estimated to be almost 12% of GDP and the possibility of rising to 20% of GDP. The same is playing out in Canada, the EU, Japan, and China. How will all this debt be paid back? It won’t. One can only hope when we come out of this the economy grows, thereby lowering the debt to GDP ratio to more reasonable levels. And for the thousands, nay, millions who have been thrown out of work, will there be a job to come back to?

The huge loss of jobs has large economic consequences. Those who lose their job may now have trouble paying rent, mortgages, and other debt, including student loans. Not everyone will be rescued by programs to help them out nor will the financial help offered necessarily cover all their expenses. This in turn could lead in some instances to evictions, mortgage defaults, and bankruptcies. It could also lead to greater income inequality as a huge part of society falls further behind those who have the high-end jobs in finance, health care, technology, and more who are able to secure their jobs. It is estimated that one in four workers will be out of work which has a significant economic impact.

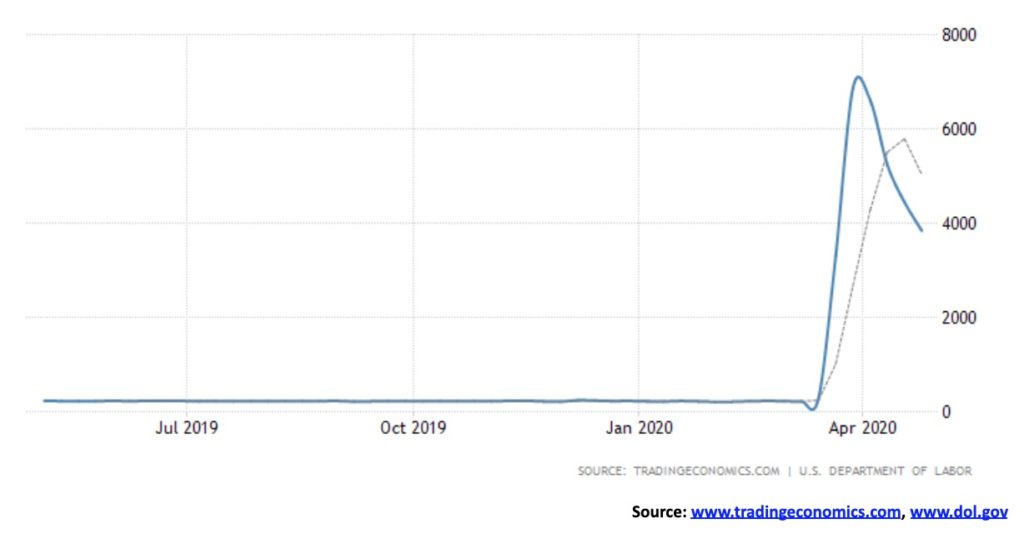

The job losses march on. The U.S. reported another 3.8 million initial claims this week bringing the six-week total to over 30 million, equating to one in every six workers. The 4-week average is over 5 million. Coupled with those that are currently unemployed, we could discover that upwards of 1 in 4 workers are unemployed. That’s for U3 the official unemployment. We’d hate to think what Shadow Stats’ unemployment number is going to be. Previously it was over 20%. Could it be over 40% now? The April jobs numbers will be released next Friday, May 8, 2020.

Job losses are worldwide, not just limited to the U.S. and Canada. According to a United Nations labour body study. the equivalent of about 305 million full-time jobs could be lost in Q2. But many workers are in what is known as the “informal economy,” especially in developing countries in Africa, Latin America, South Asia, and parts of Eastern Europe. How will they be impacted? Many could have their livelihoods destroyed. There are an estimated 1.6 billion workers in the “informal economy.” That is almost half the globe’s workforce of 3.3 billion. Poverty could rise sharply, ending years of steady progress in eradicating poverty. And that in turn could play into the destabilization of many countries.

Next, we could see further crackdown by autocratic governments taking advantage of the destabilization triggered by the pandemic. We are seeing that in a host of countries, including ones who were already being run by autocratic rulers. The list includes China, Hungary (an EU member), Serbia, Togo, Bolivia, Guinea, Azerbaijan, Cambodia, Thailand, Russia, and India. No fewer than 84 countries have enacted emergency laws vesting them with extra powers. Will the powers be relinquished when the crisis is over? The record isn’t good. Few have been like South Korea, Taiwan, or Norway who have set up systems to track, trace, and quarantine. But they have safeguards. Would Western countries such as the U.S. and Canada accept them when there are already many claiming the government is going too far? It’s no surprise that there are now further crackdowns on journalists, human rights activists, and even medical people who dare speak out.

And then there is the debt. They talk about the fight against COVID-19 in the same terms that they talk about war. The result is that governments around the world are borrowing at levels last seen during the war years of 1939–1945. Billions and trillions of dollars are being spent in an effort to prevent the economy from completely collapsing. But with factories, shops, restaurants, offices and much more closed, economic activity has come to a screeching halt. Canada has estimated that they will run a deficit of $250 billion which is 12.7% of GDP. The U.S. is expected to spend even more, upwards of 15% of GDP which would come to about $3.3 trillion. Some believe the U.S. deficit could get as high as $4 trillion. The IMF believes government debt in the Western nations could climb by over $6 trillion in 2020. This is larger than what was spent during the 2008 financial crisis. It could get higher because, just as they move to close one hole, another one bursts open.

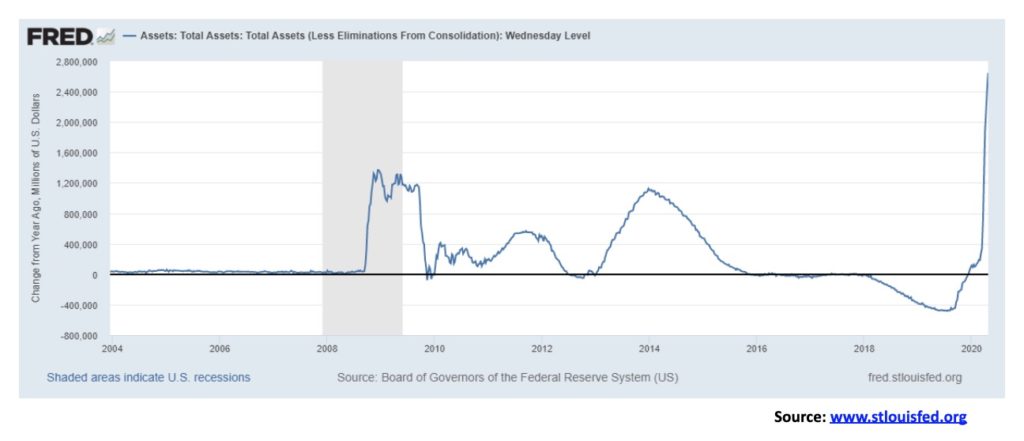

The Federal Reserve’s balance sheet is exploding (as is the Bank of Canada’s) as a result of purchasing U.S. government treasuries and almost unlimited amounts of corporate bonds and other financial instruments in an effort to keep the economy alive. Actually, more like life support, although we are not sure it has been intubated yet. The Fed’s balance sheet now stands at $6.6 trillion and rising. That’s up $2.8 trillion since September 2019. This is growth at over twice the rate that was seen during the 2008 financial crisis.

With the Fed purchasing huge amounts of the debt, the debt is actually owned by the citizens. Well, not exactly as the shareholders of the Fed are large private banks. But the Bank of Canada is an independent crown corporation of the Canadian government under the Minister of Finance. So, in effect, you are paying yourself back. Except you will never pay it back. And by purchasing your own debt you help keep interest rates low so that the cost of servicing the debt is ultimately what matters. In 2019 only 1.8% of the U.S.’s GDP was spent on interest. That is less than what it was some 20 years ago. Governments that can print their own money not only help keep interest rates low but help keep inflation low. Given that oil prices have also collapsed, that should add to keeping both interest rates and inflation low.

The worry instead might be deflation, particularly if the corporate bond market implodes and bankruptcies amongst consumers mount. In an overleveraged economy, the act of deleveraging the economy is quite deflationary. The Fed may not have to worry about inflation, but deflation could become a problem. Others believe that with the government printing more and more money it will eventually be hyperinflationary. It also potentially becomes a problem for the currency and could eventually spark a sharp fall in the value of the U.S dollar. The U.S. dollar is the world’s reserve currency which gives the U.S. advantages that other countries don’t have. The biggest one is that other central banks primarily hold their reserves in U.S. treasuries. Other countries like Italy don’t have this luxury. Even if the U.S. has a debt to GDP the same as Italy, Italy is far worse off than the U.S. This is because Italy, unlike the U.S., lives in the eurozone and it is merely a part of it, similar in some respects to a U.S. state.

As a result of the COVID-19, coupled with trade wars (as Trump once again hints at a round of tariffs against China) and the busting of supply chains around the world, we could see the world move to deglobalization and balkanization. You would have three main areas: North/South America anchored by the U.S., Europe anchored by Germany, the U.K. and even Russia and Asia anchored by China. There would be outliers such as Africa and even Australia.

Against this backdrop it is amazing that the stock markets have recovered from the COVID-19 crash in March 2020. But the stock markets look ahead. The stock markets, we suspect, are looking at a recovery starting in the third quarter and getting better in the fourth quarter. But, as we noted earlier, pandemics have a history of coming in waves. A resumption in the fall would set the markets in for a nasty surprise. And while there is some hope with the remdesivir drug, remember it is still in the testing stage and has a lot more tests to pass to become FDA approved. And, remdesivir is not a vaccine.

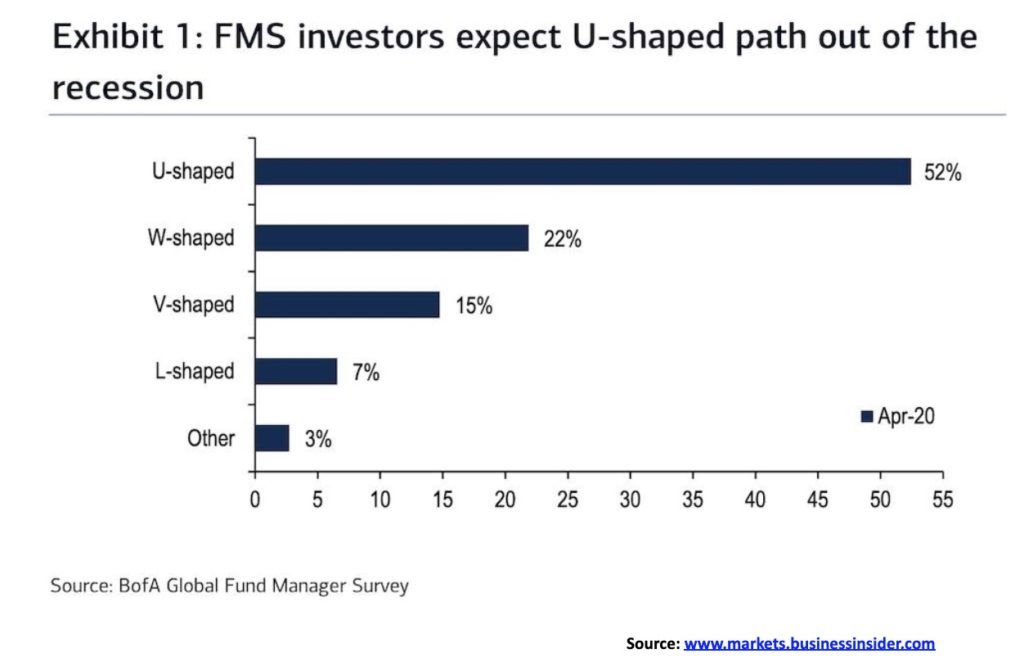

It is not a surprise that many fund managers expect a recession in 2020. IMF consensus for 2020 is for the U.S. to contract 3%. For Canada it is 3.2%. But many economists expect the worst to be during the second quarter. Fund managers were carrying in April the highest cash levels seen since the 9/11 terrorist attacks, some 5.9%, exhibiting a high level of fear. While the expectation is that earnings will be weak going forward, they believe that GDP will nonetheless bounce back relatively quickly. According to a Bank of America survey, some 52% of fund managers expect the recovery will be U-shaped. Another 15% are even more optimistic looking for a V-shaped recovery. Only 7% are expecting an L-shaped recovery.

Optimism before the storm? The economy is not like a light that you can just switch on after the shock of turning it off. As China is discovering coming out of its black hole of February/March, the consumer is not spending, instead he is saving, supply chains are broken, and the corporate debt that was already a burden has become an even bigger burden. The question is, even if we open up tomorrow, will people flock back to the restaurants and pubs, to the theatres and the cinemas, the galleries and museums, to the trains, planes, and cruise ships? The answer is, probably not as caution and trepidation rule. Globalization is fractured, the world’s two biggest economies are sniping at each other, and people are just praying they have a job to come back to while they try to find the funds to pay the May rent. COVID-19 broke the economy. Like Humpty Dumpty falling off a wall, putting it back together is going to take months and that is presuming another wave doesn’t hit.

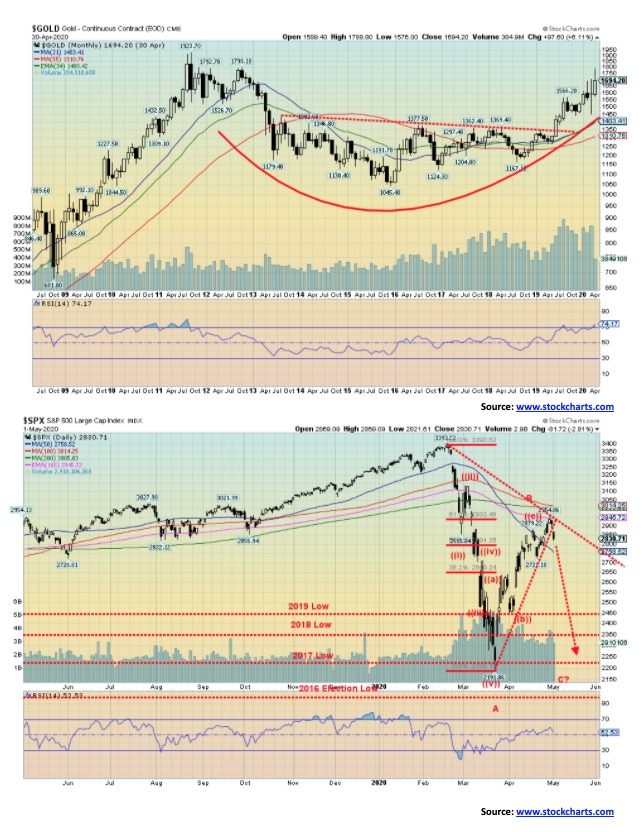

Some long-term perspective. The S&P 500 broke an uptrend line from the 2010 low. It also broke the uptrend from the 2009 low, but we chose the 2010 low as it better represented what has taken place since that time. The rebound rally ran into resistance at around the 21-month MA, and just above the 34 month EMA. It also ran into a resistance at around a series of tops seen in 2018 and 2019 before the market burst out to the final (so far) top in February 2020. As we know, it didn’t hold and the market plunged, eventually taking out both the 2019 and 2018 lows. The S&P 500 just failed in closing under the 2018 low on a monthly basis which would have been another bearish sign. The market appeared to find support around the 55-month MA. That level is currently at 2,575 so another break under that level would be bearish indeed and signal to us that the secular bear is truly underway.

Below is the Dow Jones Industrials (DJI) monthly chart for the same time period. As with the S&P 500, it broke down below its uptrend line from the 2010 low. And, as well, the DJI broke under the 2019 and 2018 low and just missed breaking under the 2017 low. The rebound has not been as strong as the S&P 500 as the DJI only came up to the 34-month EMA, failing to hit the 21-month MA so far at least. The DJI also plunged under the 55-month MA more so than the S&P 500. These points are all important as they show us that this market is weak, given it broke key year lows and has failed to break back over thus far key MAs. That leads us to conclude that the next wave down is most likely underway. A breakdown under the 55-month MA, currently at 22,855, would signal to us that a more serious bear is underway.

Our final monthly chart is gold, which is exhibiting the opposite of what the stock indices are telling us. Gold broke out of a massive monthly base and in the process is trading over multiple yearly highs—2013, 2014, 2015, 2016, 2017, 2018, and 2019. And we are very close to breaking over the 2012 high. Yes, it is getting into overbought territory, but as we saw with the stock indices that condition can prevail for a number of months.

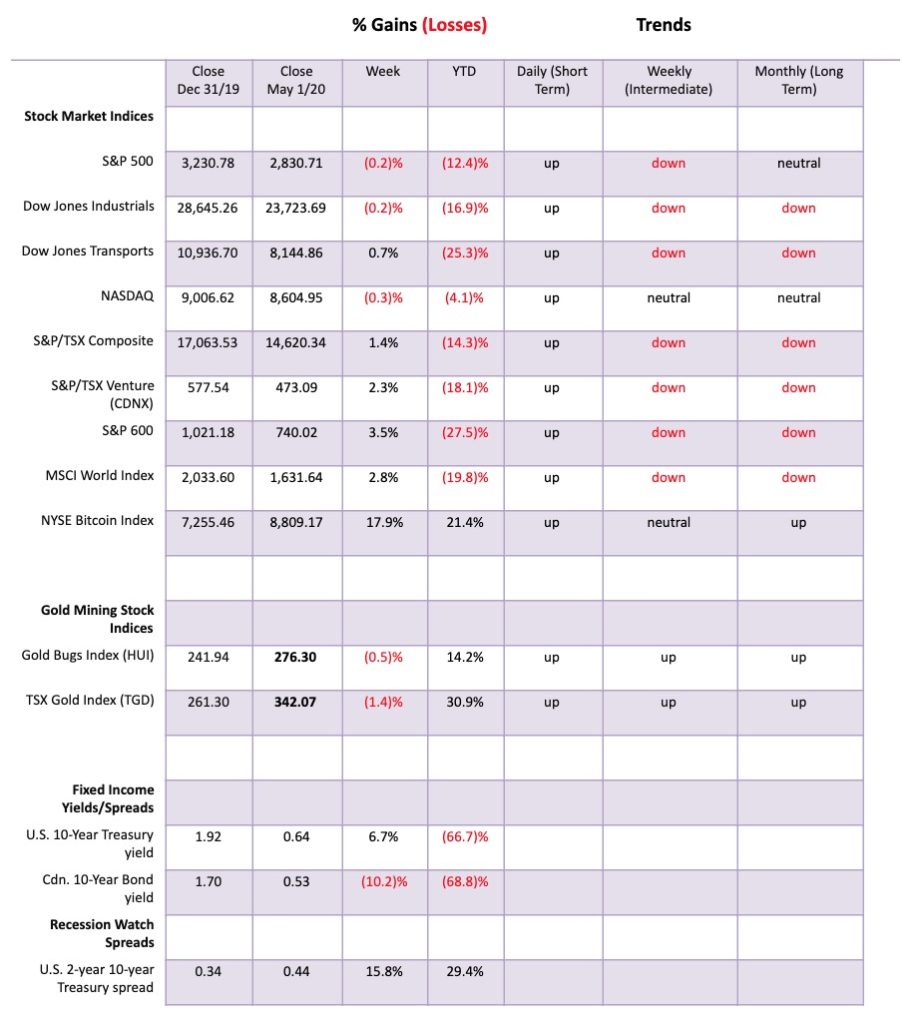

April lived up to its reputation as the best month of year with S&P 500 gaining 12.6%, the best gain ever seen for April. Overall, the S&P 500 gained 30% from the March 23 low on a close basis. So, what does May bring? Well there is the old saying “sell in May, and go away.” Or the other one “buy when it snows, sell when it goes.” There wasn’t much snow this year. May ranks as the 9th month for the Dow Jones Industrials (DJI), the 8th month for the S&P 500. September remains the worst month. So, our expectations for May shouldn’t be too high, especially after a record April.

This past week the S&P 500 looked like it was just going to keep going higher, but then Trump threatened tariffs against China and everything fell apart on Friday. The S&P 500 fell 2.8% and closed the week on a losing note, down a small 0.2%. So, it chalks up as a reversal week with a lower close. With the job numbers out this coming Friday things might not get any better. We may be starting our C wave to the downside. Other indices were as follows: the DJI was down 0.2%, the Dow Jones Transportations (DJT) bucked the trend and gained almost 0.7%, the NASDAQ was off 0.3%, and the S&P 600 (small cap) was a star, gaining 3.5%. Elsewhere, the TSX Composite had a 1.4% gain and the TSX Venture Exchange (CDNX) gained 2.3%. Overseas, the London FTSE was down 0.5%, the Paris CAC 40 was up 4.1%, the German DAX gained 5.1%, China’s Shanghai Index (SSEC) was up 1.8%, while the Tokyo Nikkei Dow (TKN) gained about 1%. A very mixed week, but then the overseas exchange did not bear the full brunt of Friday’s decline in the U.S. markets.

We are seeing quite an argument online between those who are bullish and those who are bearish. The bulls seem quite convinced that we have entered the new great bull market and that it was shortest bear in history. We confess we don’t share their enthusiasm. They cite the massive amounts of money being spent to keep the economy alive, along with the potential for a cure for the COVID and that the economy will rebound quickly once they take the lockdown shackles off. As we show later, they point out amongst other things that Semi-Conductors and retail are leading the way. As well, they note the strength recently in the S&P 600—thus the small caps are also leading the way. They also don’t believe the earnings drop will last very long either. But the conclusion is “don’t fight the Fed.” And, it seems, don’t fight the desire of President Trump to be re-elected. A collapsing stock market doesn’t favour his re-election.

But the bears want their say as well. The reality is, income is taking a big hit with potentially record unemployment. The massive amount of monetary stimulus being provided by the Fed and the Treasury (and, here in Canada, the government and the BofC) is designed only to ensure that things kind of/sort of stay in place until a recovery gets underway. The question is, how long will this last, and how many will go bankrupt before things come back together? Bailouts, we might note, are not a substitute for income. People may be able to pay their rent (although many won’t be able to), but they will default on loans, student loans, and more. That in turn could create a big headache for the banking system. As companies slash dividends, another source of income could dry up. The biggest danger is in the energy sector as companies go bankrupt and slash their dividends. Many could be caught out in the housing market especially speculators in the condo markets and we could suddenly see a huge number of houses and condos being dumped on the market. And, since they will need to get liquid and get out, a housing crash could follow. Even the optimists are expecting a 5–10% correction. Interest rates may fall to zero, but their credit card interest rate won’t. The Fed and BofC may be buying back bonds, but the banks are parking it in reserves as they tighten credit conditions and they won’t be any mood to lend the funds out. Loan loss reserves will rise sharply. Finally, the bulls will argue this time it is different. No, the only thing that is different is how this bear will play out.

The S&P 500 shattered a number of yearly lows—2018 and 2019 and came perilously close to taking out the 2017 low. The rebound rally has recouped just under the Fibonacci 61.8% retracement level, reaching to just under the converging 100- and 200-day MA. In a bear market rally that is pretty normal. Unless we can firmly take out the 200-day MA (currently 3,005) this market is not in a bull market. It remains in a bear. Only above 3,100 do we stand a chance of testing the February high of 3,393. A break under 2,225 would suggest to us that the bear is resuming. A break under 2,450 and the lows should be tested. Under 2,370 new lows are possible. This has been a bear market rally, not the start of new bull market.

Here is the S&P 600 the small cap index. The SML gained 40% from its March low. However, it retraced only about 50% of the February/March decline that saw the index lose almost 45%. The SML fell well short of its 100- and 200-day MA. It remains in a bear market. Only above 915 could a better bull market get underway. Above 935 new highs are possible. Maybe it will on another try, but in the interim the SML remains in a bear market and there is little sign here a new bull is emerging.

Here is the S&P 600 the small cap index. The SML gained 40% from its March low. However, it retraced only about 50% of the February/March decline that saw the index lose almost 45%. The SML fell well short of its 100- and 200-day MA. It remains in a bear market. Only above 915 could a better bull market get underway. Above 935 new highs are possible. Maybe it will on another try, but in the interim the SML remains in a bear market and there is little sign here a new bull is emerging.

The NASDAQ is the bulls’ great hope. Unlike the other indices, the NASDAQ held above its 2018 and 2019 low. It touched down to the 2019 low but didn’t break it. So, for many the NASDAQ remains in a bull market. The NASDAQ on this rally also regained back above its 200-day MA, suggesting it is in a bull market. We have noted that technology should be a big winner in the COVID bear market. Biotech might be another winner for finding a vaccine. So, the NASDAQ holding numerous technology and biotech stocks could have winners and as a result outperform the other indices. Nonetheless, the NASDAQ does appear to be turning back down. A break of 8,200 would suggest that the rally is over. The NASDAQ did recover well over 61.8% of its February/March decline but it did not take out 9,100 a point that might have suggested to us that it could make new highs. Despite the big gain, RSI only regained to about 55, a level considered neutral and often seen as a turning point for the market.

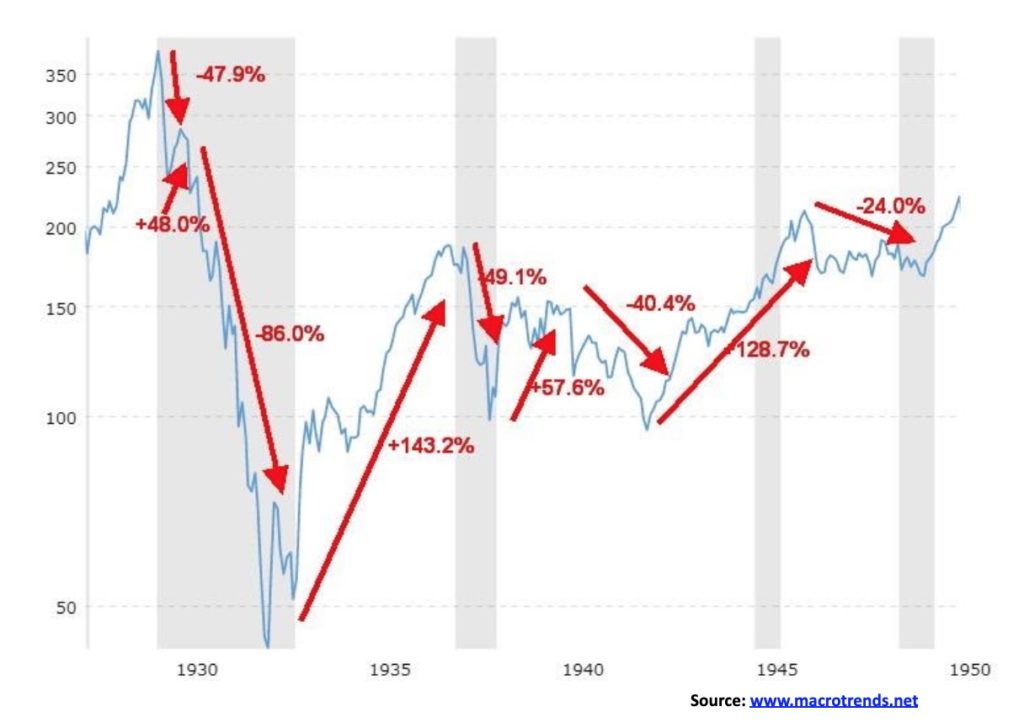

Last week we showed the gyrations of the 1966–1982 secular bear market. Above is the 1929-1949 secular bear market. The 1929 high was not finally taken out for good until 1954 a period of 25 years. A reminder that, after 30 years Japan’s Nikkei Dow has still not taken out its 1990 high. A very long bear market. For the sake of comparison, we might like to think about the March 2020 crash as comparable to the 1929 crash. The first phase down lasted 71 days and saw the DJI lose 47.9%. The rebound rally lasted 155 days and saw the DJI gain 48%. Is the current crash and recovery occurring over a shorter period of time? The COVID-19 crash saw the DJI lose 38.4% over a period of only 40 days. The rebound has seen the DJI gain almost 36% in only 37 days. It is difficult to believe that all that would be compressed into only 77 days vs. 226 days back in 1929–1930. But anything is possible. On a proportional basis we’d hate to speculate on the C wave down seeing the DJI fall 64% to 69% in a period of only 170 days to up to 422 days. We doubt that, but anything is possible.

Here is another great hope for the bulls—the Semi Conductor Index (SOX). The Sox recouped almost 75% of its bear collapse, but so far at least it fell just short of telling us that new highs are possible. That point would come above 1,806. For now, a break back down below 1,500 would suggest to us the bear market rally is over.

The bulls have noted that the retail sector appears to be recovering nicely following its crash. Above is the SPDR S&P Retail ETF (XRT). XRT lost 43% during the market crash. Since then it has recouped 46.5% at the recent high of $38.43. Retail is the great bull hope. But the retail sector has been shattered because of the lockdown. Don’t expect it to return anytime soon. XRT fell well short of its 200-day MA near $40.60. And well short of telling us that new highs are possible. Only above $41.30 are new highs possible. To the downside, the breakdown point is seen at $34 and $32.50. Retail should continue to exist, but how much of it will now be online? Shopping malls may become a relic. As with many other charts, this appears to us as a bear market rally. Nice rally but the 200-day MA is still a few dollars away.

One of our favourite indicators is the McClellan Summation Index ratio adjusted (RASI). Despite the powerful rally seen from the March low, the RASI is only up to zero—not exactly a level that would be considered bullish. A move above 500 is bullish as some of the best moves for the S&P 500 came after the RASI crossed 500. What this appears to suggest to us is that we should fail here and return to at least test the March lows or even see new lows.

This is the S&P 100 Bullish Percent Index (BPOEX). The S&P 100 is the largest cap stocks contained in the S&P 500. We note that there appears to be a divergence with the S&P 100 making new highs while the BPOEX made a lower high. If that’s correct, then the next move could be down for the S&P 100.

We suppose that, given the steepness of the decline in March and despite the rebound into April, it should not be expected that the number of stocks trading over their 200-day MA would be high. But this is not conducive to a bull market, either. It may be suggesting that the rally since the March low has been led by a select few and does not have broad acceptance. Only a bit over 20% of the stocks in the S&P 500 are trading over their 200-day MA. So, this indicator remains bearish. We’d be more excited if it were up to 50%. But then the S&P 500 itself is not trading over its 200-day MA (currently near 3,000). Shown above is a monthly chart and we are using the 10-month MA as a key zone. The S&P 500 is trading below its 10-month MA as is the percentage of stocks trading above its 200-day MA. The chart appears to us more as a potential failure than as bullish.

The TSX Composite managed to buck the trend for a reversal and lower close this past week, gaining 1.4% on the week. Still, it appears it may have broken an uptrend line and could be poised for further losses. There is some support at 14,300, but below that level a decline to 14,000 and 13,750 could be swift. Of the 14 sub-indices, 8 were up on the week and 6 were down. Leading the way to the upside was Energy (TEN) with a hefty 11.1% gain, thanks to higher oil prices. Other gainers were Income Trusts (TCM) +2.8%, Consumer Discretionary (TCD) +3.5%, Financials (TFS) +2.8%, Industrials (TIN) +0.1%, Materials (TMT) +0.8%, Real Estate (TRE) +1.9%, and, Utilities (TUT) +0.8%. Losers were led by Consumer Staples (TCS) -4.3%, Golds (TGD) -1.4%, Health Care (THC) -1.1%, Telecommunications (TTS) -0.5%, Metals & Mining (TGM) -0.9% even as they made new highs, and Information Technology (TTK) -0.6%. The TSX Composite rose to just under the 61.8% Fibonacci, suggesting that it may have made its high for this move. A move higher and over 16,375 would suggest to us that new highs are probable. There is considerable resistance between 15,600 and 16,200. The breakdown zone is seen at 13,900. Under 12,500 new lows are possible.

We continue to highlight the potential for the TSX Venture Exchange (CDNX). This weekly chart shows the huge swings it goes through. After topping back in 2006, the CDNX collapsed 80% into the financial crisis of 2008. After that, it embarked on a huge upswing, gaining 263%. Another fall was seen into 2015, this time losing 81% The next rally made lower highs once again but did gain 101%. The fifth and final wave down saw the CDNX lose 65% into the March 2020 low. We now believe we could be embarking on a new bull market. No, it is not as yet confirmed. We have some work to do. A break over 700 could set in motion a run to next major resistance just above 1,000. A move above that level could set in motion a runaway move. Still, just a move to 70 could see numerous stocks double. A move to 1,000 could set up triples and more. It has been a long decline, but we like the look of the five waves fall (ABCDE) so the March low could prove to be the low for a number of years to come. Things do not look dire everywhere.

The U.S. 10-year treasury note yield rose to 0.64% this past week, up from 0.60% the previous week. A break over 0.75% would suggest to us that the decline in rates could be over. Over 0.80% we could see the 10-year rise to 1.00% and even up to 1.20%. These days that might be considered a disaster as, given the huge amounts required to finance the COVID-19 collapse, it could raise the bond interest bill substantially. With U.S. government debt at $24.9 trillion and climbing rapidly, higher interest rates are not a good idea. The expectation is that the U.S. government debt could hit as high as $30 trillion before the COVID is over. Debt it seems doesn’t matter when it comes time to try and save the economy. And that is about all it does—keep things in place. The Fed will be a huge purchaser of the debt and their balance sheet will continue to explode upwards. It currently stands at $6.6 trillion and climbing. But, as we have noted, with the nonfarm payrolls expected to be down 21 million this Friday and an unemployment rate of 16%, adding to the debt is just a number.

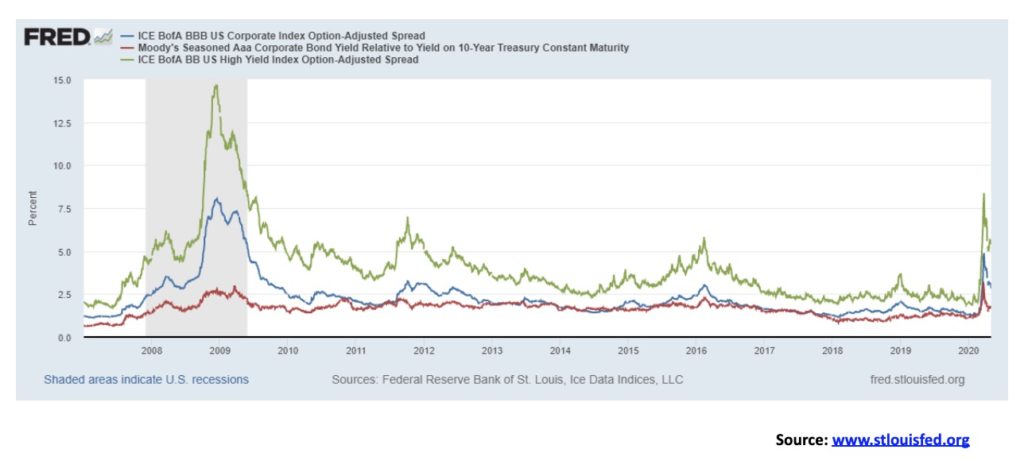

With continued thoughts of the potential for an improving economic picture and gobs of money being thrown at the economy by the Fed, credit spreads continue to narrow after spiking earlier. After peaking at 10-year plus 281 bp, the spread for Aaa bonds has fallen to 174 bp over. The BBB bonds—the lowest investment grade—have fallen from 465 bp over to 282 bp over. And finally, for BB bonds—the highest junk status—the spread has fallen to 837 bp over to 539 bp over. It is still early in this recession, however, and we note that during the 2007–2009 recession the peak didn’t come until later in the cycle. We believe the same thing is at play now.

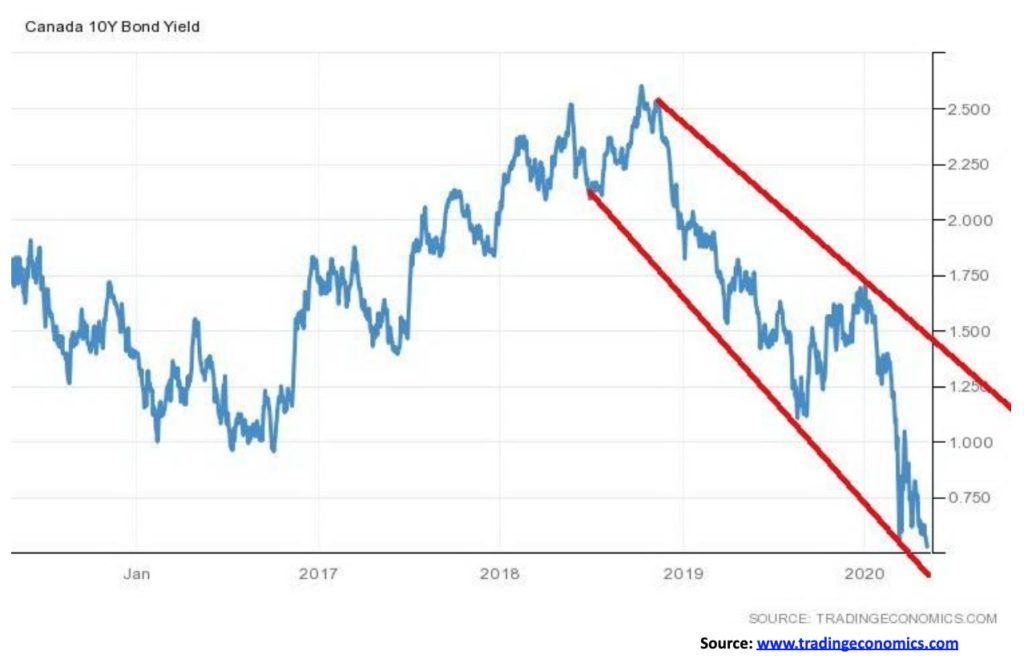

A welcome to Tiff MacKlem, the new Bank of Canada (BofC) governor. MacKlem is a financial veteran, currently Dean of the Rotman School of Management and with a long history with the BofC and the Department of Finance. He’ll have his work cut out for him as on Friday the April job numbers will be out and they won’t be pretty. Canada is expected to have lost 2,750,000 jobs in April and the unemployment rate could be 16%. The Government of Canada 10-year bond (CGB) has fallen to 0.53%, a record low. Canada has in all likelihood entered a recession. Mr. MacKlem is taking over from the former governor Stephen Poloz at an interesting time. Poloz’s term was up and the Liberal government decided that a new person at the helm would be helpful. The governor of the BofC is Canada’s equivalent to the Chair of the Federal Reserve Jerome Powell.

The US$ Index broke briefly under what might be a double top this past week in closing at 99.10. Since it wasn’t conclusive, a further decline this coming week would confirm the breakdown. Otherwise, we could go up once again. Triple tops are rare so we would expect any rally now would take out the possible double top near 101. The US$ Index needs to break down under 99 to tell us we are headed to test the major breakdown line near 95. The US$ Index was down 1.3% this past week. Currencies were up with the euro gaining 1.4%, the Swiss franc up 1.2%, the pound sterling gaining 1.0%, and the Japanese yen up 0.6%. The Canadian dollar gained a small 0.3%. Weak economic numbers are likely to help spur the U.S. dollar lower. On Friday we will get the April job numbers and the consensus expectation is a loss of 21 million jobs and an unemployment rate of 16%. With a plethora of economic numbers out this coming week, it could weigh heavily on the U.S. dollar.

Gold continues to trade in a possible corrective manner after making multi-year highs in April at $1,788. As we note further along, gold could be moving into weak seasonals often seen into April/May. With a high at $1,788, we just missed taking out the 2012 high of $1,798. Gold is being fueled by the endless rounds of QE coming from the Fed as a result of bailing out the economy. Given the 2012 high, we knew going in that $1,800 could prove to be resistance. The head and shoulders pattern that formed with the March 2020 low broke out at $1,680 and projects up to potential targets at $1,935 to $1,950. That would imply new all-time highs above the 2011 high of $1,923. That gold could make new all-time highs should not be a surprise given gold has already made new all-time highs in numerous currencies including the Canadian dollar and the euro. Given the potential for weak seasonals into April/May, the question is, how low might we go? Support is seen down to $1,660, but a break under that level would set up a test of $1,565/$1,575. Below that there would be support at around $1,545, but the next good support is the March low of $1,450. Below $1,450 gold’s bull market could be over.

We were unable to obtain our usual source for the COT but we did find some numbers. The commercial COT this past week was at 22%, slipping from 23% the previous week. Long open interest fell almost 2,000 contracts but short open interest was down even more close to 12,000 contracts. That is at least somewhat bearish going forward. The large speculators (hedge funds, managed futures, etc.) COT was at 92% which is quite bullish.

We read both bullish and bearish reports for gold going forward. Bank of America is on record calling for $3,000 gold, quite a call coming from a mainstream source. This past week we learned that the Bank of Nova Scotia (BNS) is closing their precious metals desk. That was a bit of shock as BNS has been in precious metals actively since 1997 after having purchased Mocatta Bullion, a company that dated back to 1684. BNS was a major bullion bank and had been the first non-British bank to chair the London gold fixing. But controversy swirled around the London fixing and BNS, like other bullion banks, was the subject of lawsuits both in Canada and internationally after being accused of price fixing. That still leaves CIBC and RBC as active precious metals dealing desks here in Canada. We view the closing of the BNS dealing desk as bullish for metals.

But we are also well aware of bearish outlooks for gold despite what appear to be sound fundamentals. We are aware that we are approaching the 23.5-year cycle low due in a wide range from 2020 to 2027. The narrower range would be the 7.83 cycle low last seen in 2015 and due 2023–2024. If that’s correct, then we should still have some time on our side for a major run to the upside to our potential targets of $1,935–$1,950 and even BofA’s targets of $3,000. As noted, a breakdown under $1,450 the March 2020 low would suggest that we are in the throes of heading for our 7.83 year and 23.5-year cycle low. How low could it go? Well, it could certainly test the 2015 low of $1,045.

Like gold, silver prices faltered this past week. Silver was down 2.1%. Silver continues to frustrate and act like it is in a bear market. Given that it made new multi-year lows in March, maybe it is. The rebound rally took us back to the 50-day MA, but thus far it has been unable to break out above it. It now appears poised to break down further. A break of the recent low at $14.56 would set up a test of the previous low at $13.90 and once again the 2015 low near $13.50. A break under $13.50 would set up a test of the March low and possibly even new lows. A break of $12.75 would almost certainly set up new lows. The breakout to the upside remains elusive. Right now, we need a break above $16 once again to suggest at least a test of $17. A break above $17.25 would suggest to us that we could see new highs above $18.90.

We read bullish and bearish reports on silver. Gold as well. We try to absorb each of them equally and until we see clear signs that we are breaking out we can’t be dismissive of the bearish reports. Unlike gold, silver did not make new highs in 2019. In fact, it wasn’t even close. And then when the March 2020 collapse came silver made new multi-year lows, taking out the 2015 low.

We have noted in the past silver’s long cycle of possibly 18.5 years. Silver, like gold, started free trading after the gold window was closed. Silver made a significant low in January 1976. The next major low was January 1993, 17 years later fitting nicely into the range of 15–22 years for the 18.5 year low. The next major low was November 2008, 15 years and 10 months later. Again, that fit in to the 15–22-year range for the 18.5 year low. The next one is due 2023 to 2030 so it would appear we still have time on our side for a run to the upside. It looks even better if 2015 was the 18.5-year cycle as that came 22 years after the 1993 low. Silver’s shorter cycle is 7 years and the range is 5–9 years. If 2008 was the 18.5-year cycle low, then 2015 fit the 7-year cycle nicely. The next 7-year cycle low would be due 2020 to 2024. Could the March 2020 low be the 7-year cycle low? That would be confirmed only if we broke above the high of the last cycle at $21.23 that was seen in July 2016. For starters, a move over $19 would at least be quite encouraging.

Like gold, we didn’t see a silver COT from our usual source. However, we did obtain some numbers and the commercial COT for silver was 39% this past week. Over the week long open interest fell a small 300 contracts and short open interest was down about 2,800 contracts. The large speculators COT was at 70%. There has been improvement in the commercial COT but it is not yet what we would call really bullish.

Thanks to my friend and colleague Mike Ballanger, writing in his weekly missive the GGM Advisory, for pointing out a potentially interesting anomaly in the markets. We can’t hope to write with Mike’s often hilarious take on the markets, but we can flesh things out a bit. Gold traditionally follows a somewhat predictable pattern of seasonals. Strength is usually seen starting in November/December that runs into February. That period of strength is often followed by a period of choppiness with either an upward or downward bias. Weakness into March, strength into April, weakness into May even June, strength into July, weakness into August then a strong period of strength into October followed by the final weakness once again into November/December where the cycle starts all over again. No, it doesn’t follow it every year like clockwork and periods of strength and weakness can vary irrespective of whether it is a bull or bear market.

In 2008 there was a crash into November. Strength was classically seen into a top in February 2009. We then had a bouncy downward bias descent into a low in late April/early May before we began another ascent into June. In 2015 we had a nasty descent into a final low in December 2015 followed by a strong rally into March 2016. What followed was a choppy period that saw the final low made in late May 2016 before we began the final ascent into a top in July 2016. The pattern continues so far, this past year. We made an important low in November 2019 followed by a good rally into March 2020. Gold crashed along with the stock market in March 2020, then snapped back rather nicely, topping in April 2020. Since that top we have begun what appears as once again a choppy descent where, with any luck, the previous patterns hold up and we find a low sometime in May 2020 but certainly no later than June 2020. We should then begin another ascent if the previous seasonal patterns hold true. Will we see new highs? We are encouraged by the fact that we made a higher high in April, signalling to us that the bigger trend appears to be up.

The gold stocks had a pause this past week that hopefully refreshes. It has been quite a run from those March crash lows. The TSX Gold Index (TGD) is up 98% from the March low while the Gold Bugs Index (HUI) is up 94%. Nice moves. On the year, the TGD is now up almost 31% while the HUI lags up 14%. However, this past week both paused with the TGD off 1.4% while the HUI was down a small 0.5%. Friday saw quite a strong turnaround for the gold stocks as the TGD made a slightly lower low then a higher high from the previous day and closed up 4.6% on the day. We can’t help but notice that institutional buying has come into the market and analysts who normally don’t talk much about gold are taking notice and calling for it to move higher. The result is we are seeing more fund buying for portfolios than we normally do and the talk from the fund managers and portfolio managers is more positive than it usually is. Is this a warning sign that the market might be becoming overheated? After all, when the non-gold-bug managers are jumping into the market, should we instead be turning tail and bailing out? Probably not, at least not yet. What appears to be a large head and shoulders bottom suggests a potential move as high as 385/390. Well, we are getting close. But we may go through a bit of a pullback first in keeping with our note about seasonals. The TGD is fine as long as we can stay above 275. A drop under 300 would suggest that our pullback is bit steeper than expected. Corrections of 10% or more, even in a bull move, are not unusual for gold stocks. A look at the 2008–2011 bull market for gold and the gold stocks reveals that the TGD had no fewer than six corrections ranging from 12% to 24% before making its final high in September 2011. The bull rally was underway in with the final low in October 2008. Altogether, the TGD gained 187% from October 2008 to September 2011.

Our first level of support is at 320 and below that at 300. New highs would suggest we could be in the throes of making the move towards the targets of 385/390.

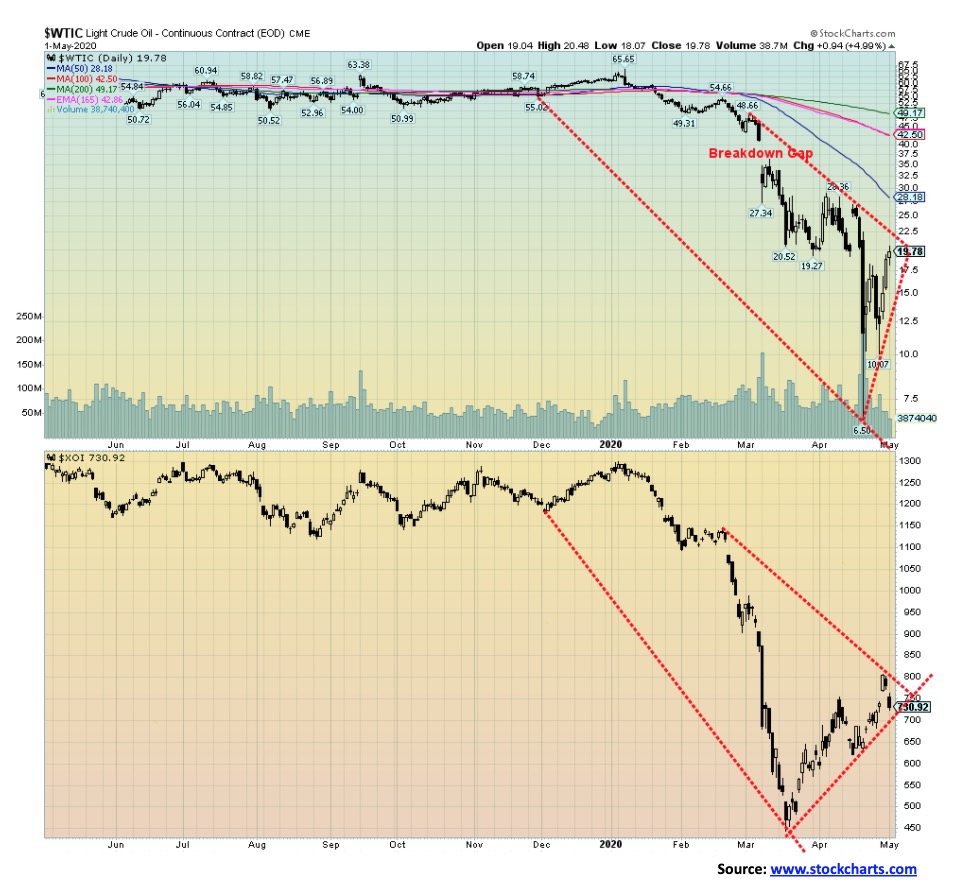

The oil bear is over! Okay, let’s not get too excited. But, for a change, it was a pretty good week for oil and the energy stocks. Oil was emboldened by more seeming to step up to the plate and cut production and by the excitement of potentially positive news on the coronavirus front. Relief rally? That could be, as we ended the week at the top of a channel. So, this coming week we either have to break out or, like an illusion, it will just go poof and down we go again. WTI oil was up almost 20% on the week although natural gas (NG) didn’t follow as it was strangely flat on the week. The energy stocks responded positively with the Arca Oil & Gas Index (XOI) up 4.4% and the TSX Energy Index (TEN) up 11.1%. The energy stocks followed the markets down on Friday although oil prices held up, closing near $20. Pretty good considering at one time earlier in the month oil went negative.

We confess we are not quite sure why (although we do have our suspicions), but the Fed’s spigot of money may be turned on for shale producers as well. The industry should be allowed to retrench, bankrupt, and merge in order to survive. What is the point of continuing to allow shale producers to pump into a market already with too much supply? But the oil and gas industry is huge and powerful and has a big ear in Washington with politicians and the money men. They could take the money and run and still leave behind huge unemployment in the industry. Even the American Petroleum Institute was baffled and was quoted as saying, “You can’t have capitalism on the way up and socialism on the way down.”

We knew dividends were coming. Royal Dutch Shell (RDS.A) announced a dividend cut. Cuts to production were announced by Conoco Phillips (COP) totalling 420 thousand BPD. Huge losses were reported by Chevron (CVX) and Exxon (XOM). Chevron was also cutting some 400 thousand BPD. Oasis Petroleum (OAS), announced the shutting of its Bakken oil fields. Many of these same companies that operate in OPEC countries will also be cutting production. Even Norway was prepared to cut production. Apparently, Chesapeake Energy (CHK) is filing for chapter 11 bankruptcy. Russia is trying to cut back as well but faces logistical problems with its old wells, many of which are unable to actually be capped.

Altogether, it is estimated that the oil and gas industry is poised to lose over $1 trillion in revenue in 2020. Banks are preparing for huge losses from the sector and have even set up special units to deal with bad energy loans.

WTI oil is at downtrend line resistance. A firm break above $22 could suggest a run to the 50-day MA near $28. But we figure that would be about it. To the downside, the break point is under $10, suggesting a test of the lows and single figures once again.

—

(Featured image by Austin Distel via Unsplash)

DISCLAIMER: This article was written by a third party contributor and does not reflect the opinion of Born2Invest, its management, staff or its associates. Please review our disclaimer for more information.

This article may include forward-looking statements. These forward-looking statements generally are identified by the words “believe,” “project,” “estimate,” “become,” “plan,” “will,” and similar expressions. These forward-looking statements involve known and unknown risks as well as uncertainties, including those discussed in the following cautionary statements and elsewhere in this article and on this site. Although the Company may believe that its expectations are based on reasonable assumptions, the actual results that the Company may achieve may differ materially from any forward-looking statements, which reflect the opinions of the management of the Company only as of the date hereof. Additionally, please make sure to read these important disclosures.

Morocco’s Growth Holds at 4.6% as Agriculture Offsets Economic Pressures

Morocco’s economy grew 4.6% in Q1 2026, driven by a strong agricultural rebound offsetting declines in industry. Services expanded moderately...

Abivax Shares Surge as New Trial Data Eases Safety Concerns Over Ulcerative Colitis Drug

Abivax shares surged nearly 36% after positive updated trial results for its ulcerative colitis drug obefazimod reassured investors following earlier...

El Dorado Raises $9M to Expand Cross-Border Fintech Platform

El Dorado, a Latin American fintech improving cross-border financial services, raised a $9 million Series A led by Paradigm with...

Bitcoin Stalls Near $60K as Strategy Moves, ETFs Outflow, and EU MiCA Rules Take Effect

Bitcoin hovers near $60,000 with ETF outflows, while Strategy boosts reserves, sells BTC, and raises dividends to reassure investors. Ethereum...

Cannabis Dominates Global Drug Use: Trends, Risks, and Shifting Markets

Cannabis remains the world’s most widely used illicit drug, with 256 million users in 2024, surpassing all others combined. Growth...

|

|

|  |

|

|

-

Africa2 weeks ago

Africa2 weeks agoEgypt’s Net Foreign Assets Rise as External Position Continues Gradual Strengthening

-

Markets2 days ago

Markets2 days agoOil Surges on U.S.–Iran Tensions as Global Markets Show Diverging Trends and Rising Risk Fears

-

Markets1 week ago

Markets1 week agoCocoa Market Faces Mixed Trends Amid Rising Supply and Weak Demand

-

Africa6 days ago

Africa6 days agoBank of Africa Expands Sino-African Trade Partnerships in Beijing