Markets

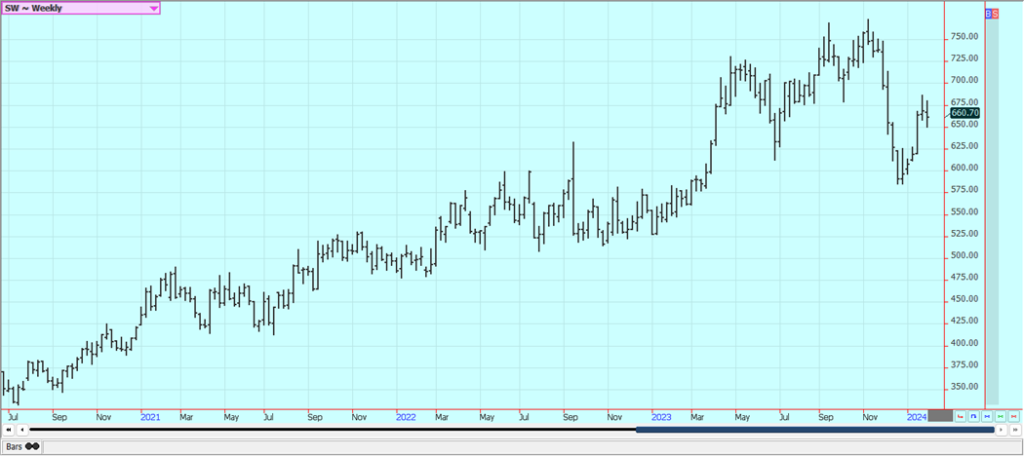

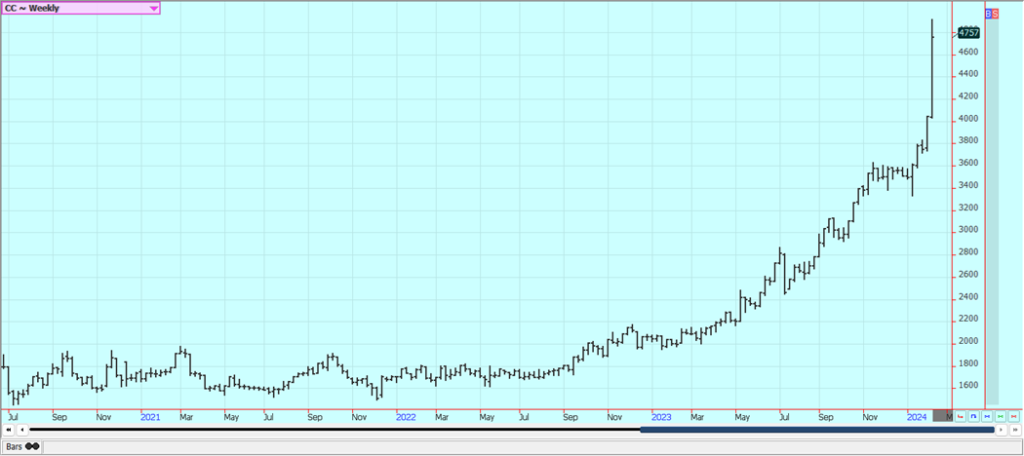

Both Cocoa Markets Were Sharply Higher and Entered the Stratosphere Last Week

Cocoa market in New York gained almost $1,000/ton last week and London was up over $700/ton. Price trends remain up on the daily and weekly charts. Futures have rallied sharply for the past month but exploded higher last week. The availability of Cocoa from West Africa remains restricted and projections for another production deficit against demand for the coming year are increasing.

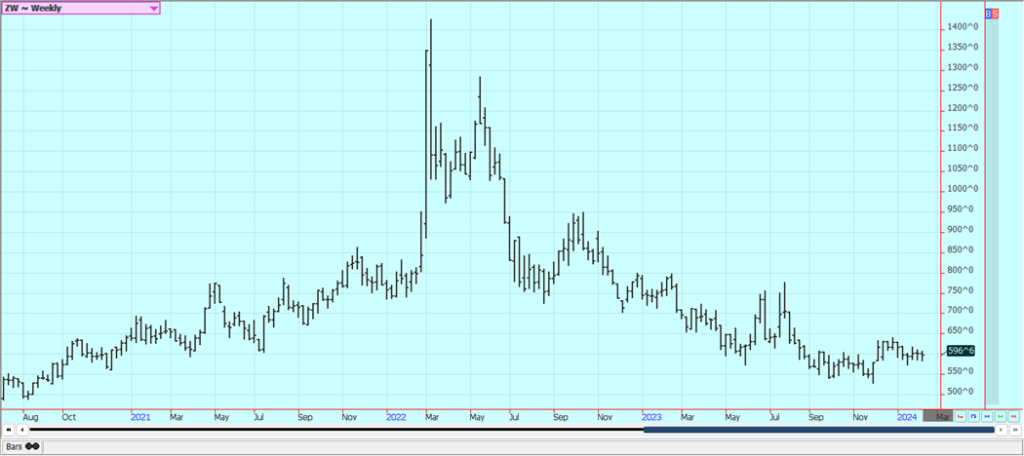

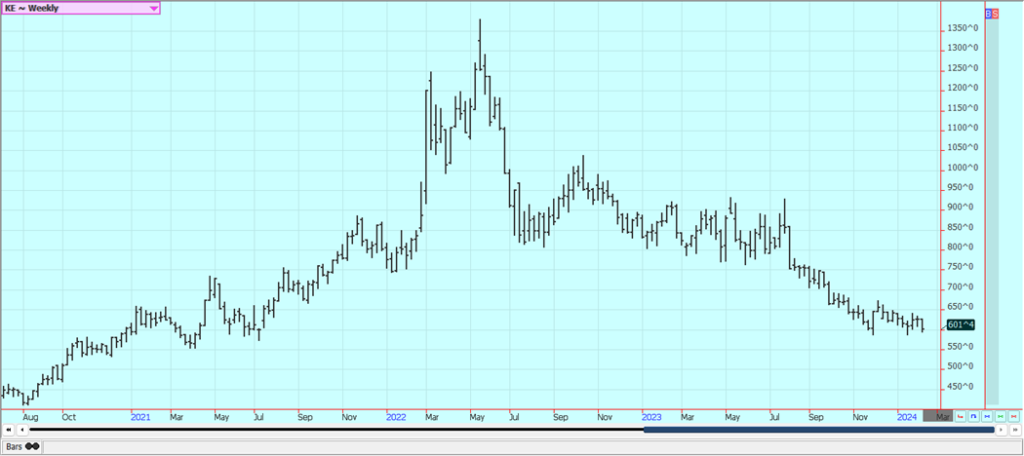

Wheat: Wheat was lower last week on big world supplies and low world prices. HRW futures was the weakest market. The weekly export sales report released last week was not strong and the weaker sales are due to strong competition from Rusia, Ukraine, and the EU as those countries look to export a lot of Wheat in the coming period.

EU offers were unchanged to help keep US offers from falling. Russian and Ukraine offers are weaker. Some support came from the bombings in the Red Sea that has interrupted commerce. It is warm in the US and Canada this week. Cooler temperatures are also forecast for next week. Black Sea offers are still plentiful and Russian prices appear to be weakening.

Weekly Chicago Soft Red Winter Wheat Futures

Weekly Chicago Hard Red Winter Wheat Futures

Weekly Minneapolis Hard Red Spring Wheat Futures

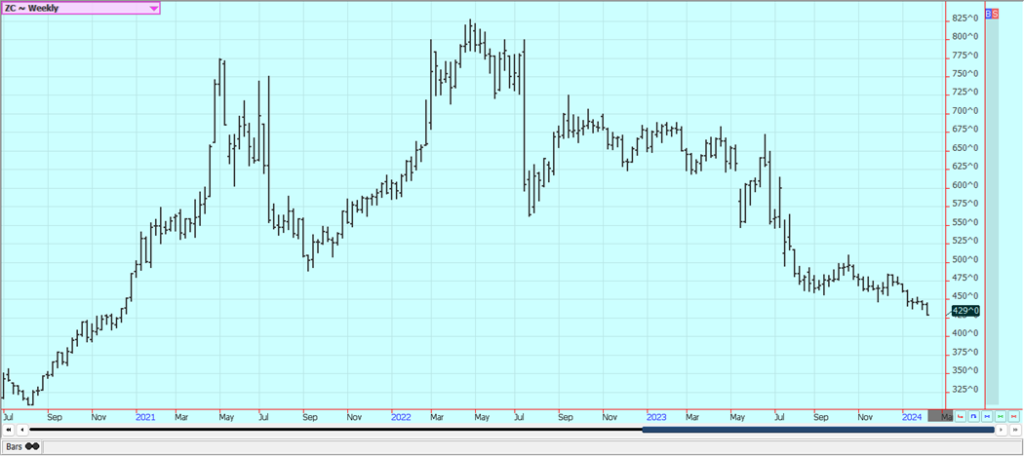

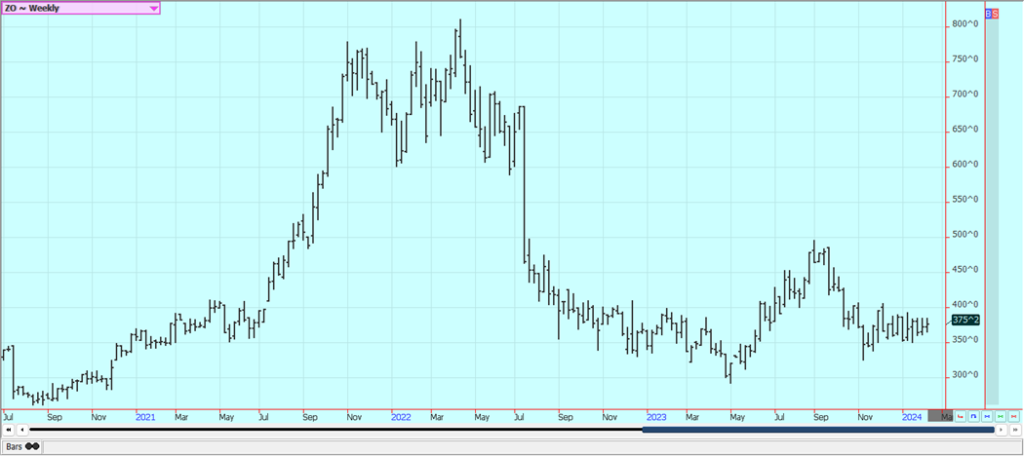

Corn: Corn closed a little lower last week and made new lows for the move in response to the WASDE reports with an increase of 10 million bushels in the ending stocks estimates. Oats were a little higher end remained in a trading range. The weather forecasts for Argentina are improving with more showers expected this weekend but coming after a hot and dry period first. On the other hand, more rain is forecast for central and northern Brazil and the Soybeans harvest could be delayed and that could mean less Corn planted area.

The planting progress reports to date indicate rapid progress so this concern is lessening. Soybean quality could be reduced as well. The market anticipates increased selling from US producers, but many have sold enough, and elevators and processors are reported to be full. Producers are looking for higher prices now as crops are in the bin for the Winter. Ideas of weak demand are keeping prices low. The market feels that there is more than enough Corn for any demand.

Weekly Corn Futures

Weekly Oats Futures

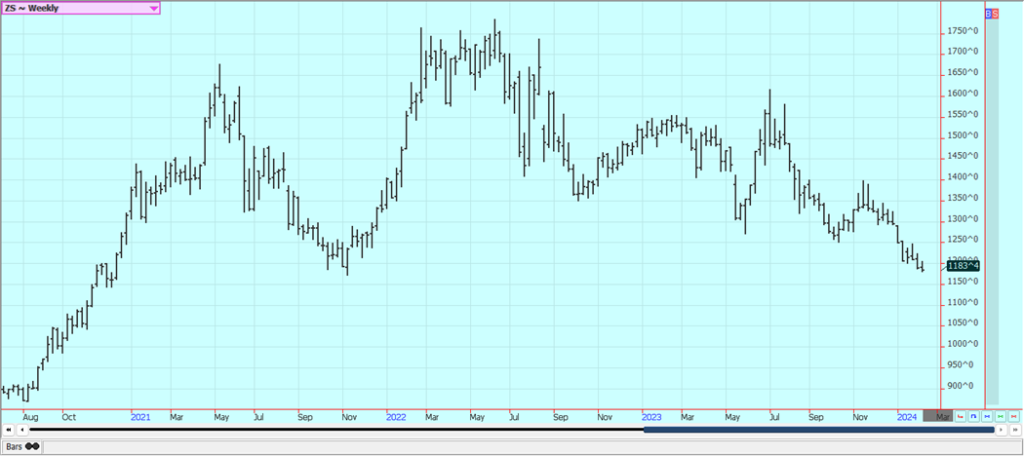

Soybeans and Soybean Meal: Soybeans was a little lower and Soybean Meal was lower in response to the USDA estimates, but Soybean Oil was higher on strong demand from the bio fuels sector. USDA left Brazil production estimates very high at 156 million tons and cut US export demand to push US ending stocks above 300 million bushels. The trade reacted and followed through on Friday.

Rains are in the forecast after the extreme weather seen over the next week in Argentina. Such rains would be beneficial for reproducing Corn and Soybeans. The precipitation keeps falling in Brazil and is expected to continue through this week. The rains could be detrimental to the quality Soybeans and the planting dates for Winter Corn. Support also came from reports of reduced Brazil production.

Weekly Chicago Soybeans Futures

Weekly Chicago Soybean Meal Futures

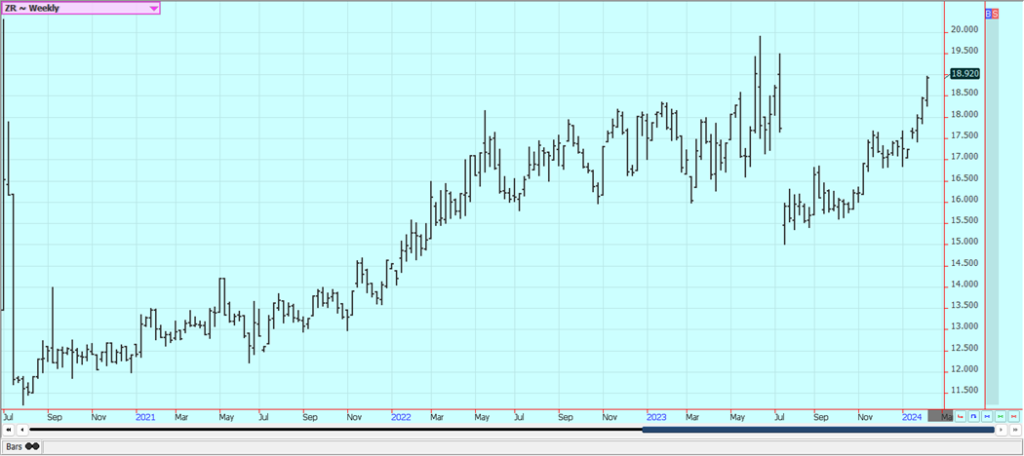

Rice: Rice closed higher last week and trends remain up on the daily and weekly charts. USDA cut ending stocks estimates for Long Grain and All Rice by 1.0 million tons on increased export demand. No big changes were noted for the world estimates.

However, the overseas markets feature less production in Brazil and India and it appears that the lack of offer from these markets is supporting prices here in the US. Warmer and wetter weather is expected this week and next on the Delta and Texas and soil moisture conditions for the next crop should improve.

Weekly Chicago Rice Futures

Palm Oil and Vegetable Oils: Palm Oil was higher last week on ideas of weaker production ideas against good demand. The fundamentals of average demand against a weaker supply outlook are still around to keep prices supported. Trends are mixed on the daily charts and on the weekly charts. Canola was ha little lower.

There are still forecasts for better rains in Argentina after a dry spell ends in a week or so and improving weather in Brazil. Current forecasts call for generally improved growing conditions in Brazil this week. The Canola crop is harvested, and it is in bins, so it will take some price movement to get new farm sales. Trends are trying to turn down on the daily and weekly charts in this market.

Weekly Malaysian Palm Oil Futures

Weekly Chicago Soybean Oil Futures

Weekly Canola Futures:

Cotton: Cotton closed higher last week and above strong resistance on the weekly charts in response to a reduction in ending stocks estimates from USDA. USDA found increased demand to lower ending stocks to 280 million bales from 290 million bales before. The demand news has been solid in this market for the last several weeks. The charts indicate that trends turned up in the second half of last week.

Reports indicate that the US cash market has been moderately active with some producer selling and mill fixing noted. The US economic data has been positive, but the Chinese economic data has not been real positive and demand concerns are still around. There are still many concerns about demand from China and the rest of Asia due to the slow economic return of China in the world market but recent demand from China is starting to put those concerns on the back burner.

Weekly US Cotton Futures

Frozen Concentrated Orange Juice and Citrus: FCOJ closed lower last week after making new highs for the move. The daily harts suggest once again that the market is finding a high area. USDA estimated production at 19.8 million boxes for lower Florida, much less than recent estimates but still well above a year ago. Prices had been moving lower on the increased production potential for Florida and the US and also in Brazil until a sharp rally came to the market.

That is lower Florida, much less than recent estimates but still well above a year and the rally came an end yesterday. There are no weather concerns to speak of for Florida or for Brazil right now. The weather has improved in Brazil with some moderation in temperatures and increased rainfall amid reports of short supplies in Florida and Brazil are around but will start to disappear as the weather improves and the new crop gets harvested. Historically low estimates of production in Florida due in part to the hurricanes and in part to the greening disease that have hurt production, but conditions are significantly better now with scattered showers and moderate temperatures.

Weekly FCOJ Futures

Coffee: New York and London closed higher on Friday and for the week on a lack of offer from producers as forecasts for good growing conditions through the month of February continue. The Dollar was a little higher yesterday and remains in an uptrend.

Robusta offers remain difficult to find and the lack of offer of Robusta remains the main bullish force behind the market action, and reports indicate that Brazil producers are reluctant sellers as well. Brazil weather continues to improve for Coffee production but is still not perfect. Rains continued to fall in parts of Brazil Coffee areas. Brazil weather is improving for the best crop production.

Weekly New York Arabica Coffee Futures

Weekly London Robusta Coffee Futures

Sugar: New York and London closed higher last week and the trends remain sideways on the daily charts but are trying to turn up. The market continues to see stressful conditions in Asian production areas. There are worries about the Thai and Indian production and talk that India could turn into an importer next year. Offers from Brazil are still active but other origins. are still not offering or at least not offering in large amounts except for Ukraine.

Weekly New York World Raw Sugar Futures

Weekly London White Sugar Futures

Cocoa: Both cocoa markets were sharply higher and entered the stratosphere last week. New York gained almost $1,000/ton last week and London was up over #700/ton. Cocoa price trends remain up on the daily and weekly charts. Cocoa futures have rallied sharply for the past month but exploded higher last week. The availability of Cocoa from West Africa remains restricted and projections for another production deficit against demand for the coming year are increasing.

The cocoa harvest seems to be coming and demand could be a problem with the current very high prices. Cocoa traders are worried about another short production year and these feelings have been enhanced by El Nino that is threatening West Africa crops with hot and dry weather. Ideas of tight cocoa supplies remain based on more reports of reduced arrivals in Ivory Coast and Ghana continue,

Weekly New York Cocoa Futures

Weekly London Cocoa Futures

__

(Featured image by 5671698 via Pixabay)

DISCLAIMER: This article was written by a third party contributor and does not reflect the opinion of Born2Invest, its management, staff or its associates. Please review our disclaimer for more information.

This article may include forward-looking statements. These forward-looking statements generally are identified by the words “believe,” “project,” “estimate,” “become,” “plan,” “will,” and similar expressions. These forward-looking statements involve known and unknown risks as well as uncertainties, including those discussed in the following cautionary statements and elsewhere in this article and on this site. Although the Company may believe that its expectations are based on reasonable assumptions, the actual results that the Company may achieve may differ materially from any forward-looking statements, which reflect the opinions of the management of the Company only as of the date hereof. Additionally, please make sure to read these important disclosures.

Futures and options trading involves substantial risk of loss and may not be suitable for everyone. The valuation of futures and options may fluctuate and as a result, clients may lose more than their original investment. In no event should the content of this website be construed as an express or implied promise, guarantee, or implication by or from The PRICE Futures Group, Inc. that you will profit or that losses can or will be limited whatsoever. Past performance is not indicative of future results. Information provided on this report is intended solely for informative purpose and is obtained from sources believed to be reliable. No guarantee of any kind is implied or possible where projections of future conditions are attempted. The leverage created by trading on margin can work against you as well as for you, and losses can exceed your entire investment. Before opening an account and trading, you should seek advice from your advisors as appropriate to ensure that you understand the risks and can withstand the losses.

Avant Devices Moves Toward Electric Wheelchair Kit Production with New Funding Drive

Murcia-based Avant Devices is seeking €260,000 in crowdfunding to launch mass production of its electric wheelchair conversion kit. The funds...

Legend Biotech: Growth Driven by CAR-T Innovation and Carvykti Expansion

Legend Biotech's stock reflects demand for innovative CAR-T cancer therapies. The US biotech focuses on commercializing Carvykti with partner Janssen...

Senegal’s Debt Strategy: Choosing Between Restructuring and Financial Innovation

Senegal’s upcoming choice of debt advisor, with Lazard reportedly leading the race, reflects a broader strategic decision. Rather than pursuing...

Pictet Raises $253 Million for Environmental Investment Fund

Pictet Group closed its Environment Co-Investment Fund I at $253 million, surpassing its $200 million goal. The Article 8 SFDR...

Virginia Cannabis Market Could Reshape Regional Competition

Virginia’s planned recreational cannabis market could reshape the Washington region’s economic landscape. With nine million residents, it may draw consumers...

|

|

|  |

|

|

-

Fintech1 week ago

Fintech1 week agoRevolut Updates Crypto Rules for Deposits and System Errors

-

Cannabis5 days ago

Cannabis5 days agoGermany Tightens Cannabis Reimbursement Rules: Approved Medicines Must Come First

-

Crowdfunding2 weeks ago

Crowdfunding2 weeks agoLemonaid Offers Shares to Consumers for the First Time

-

Crypto2 days ago

Crypto2 days agoBitcoin’s Price Drops as Investors Turn to Layer 2 Solutions