Featured

Coffee Prices Have Stayed Firm as the Current Brazil Harvest Starts to Wind Down

New York and London closed higher last week on the adverse weather for Brazil Arabica Coffee areas. Prices have stayed firm as the current Brazil harvest starts to wind down. The freeze threat in Brazil has passed but the damage has been done. The government in Brazil estimates that 11% of the Coffee areas were affected. Temperatures are warmer with near to above normal readings expected

Wheat: Wheat was higher as USDA cut its production estimates more than expected by the trade and on fund buying as trends have turned up again on the daily and weekly charts for all three markets. The FSA said that farmers enrolled 48.808 million acres of Wheat into subsidy programs including preventing plant of 282,229 acres/ Dry weather in southern Russia as well as the northern US Great Plains and Canadian Prairies remains a supportive feature in the market. Trends in Winter Wheat markets are still up. Crop size estimates in Russia have been reduced and are now well below the latest USDA estimates. The Russian weather has been good for production in northern and western areas but is still trending dry in southern areas and into Kazakhstan. Some showers are no in the forecast for the drier areas over the next week, then showers and cooler temperatures are in the forecast. The weather in China and Europe is wet and there is potential for reduced quality in Europe. Europe is expecting top yields as are parts of eastern Europe and northern Russia. It has been very cold in South America and the winter crops are in trouble in Brazil and Paraguay. US White Winter Wheat production is also being hurt by hot and dry weather, but a cold front could bring some relief in several days.

Weekly Chicago Soft Red Winter Wheat Futures

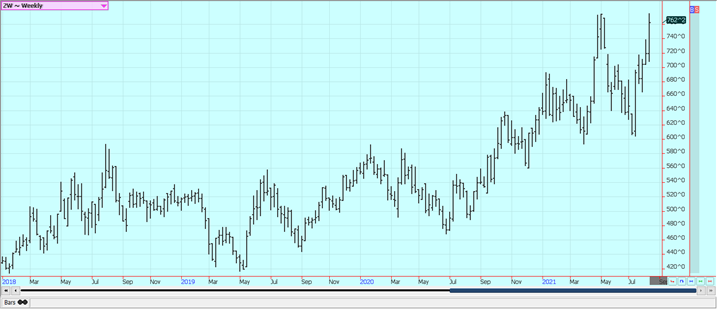

Weekly Chicago Hard Red Winter Wheat Futures

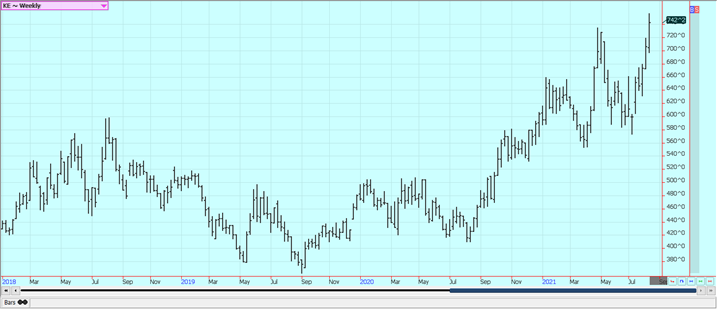

Weekly Minneapolis Hard Red Spring Wheat Futures

Corn: Corn was mixed on Friday and higher for the week in reaction to the USDA reports released on Thursday. Trends are up on the charts in reaction to the USDA reports. USDA reduced yields and production estimates much more than the trade had expected. Production in Brazil was also cut significantly. USDA also said that farmers enrolled 90.309 million acres into subsidy programs and included 620,458 acres of prevent plant. Demand has improved in the past week, and the weather remains a feature of the trade. Some forecasts call for improved weather, especially in the eastern belt. The growing conditions in the US are highly variable and not likely to produce trend line or record yields. It is still too dry in many areas of the west and drier weather is expected in the east. It should stay hot in the west and cool in the east. Ideas are that Brazil Corn production could be less than 85 million tons so reduced production estimates are expected in coming reports. Oats were higher as well. The uncertain weather in the northern Great Plains and Canadian Prairies remains the best support for the market. Canadian Oats areas and those in the northern Great Plains remain too hot and dry. Some rain is now in the forecast but is too little and too late to materially help crops.

Weekly Corn Futures

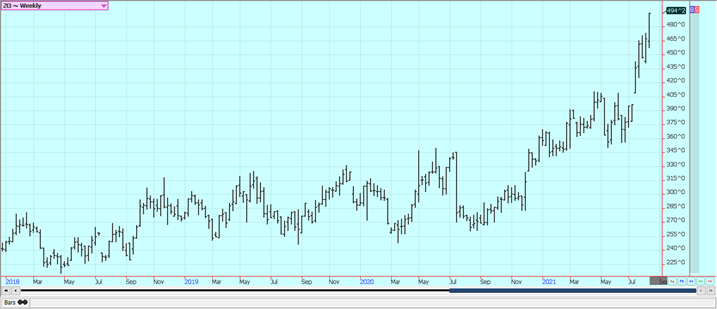

Weekly Oats Futures

Soybeans and Soybean Meal: Soybeans and products were higher last week in response to positive demand news and the USDA reports that showed production in line with trade estimates. Chart trends remain sideways in all three markets. US weather is still a feature in the market as it remains hot in the west and is dry in just about all areas now. Eastern Midwest areas should be cooler and parts of central Illinois turned too wet again after some big rains on Thursday night. Soybeans conditions in central production area started the year too wet and have suffered. Minnesota and nod the Dakotas are hot and dry but could get some showers this week. FSA said that US farmers enrolled 85.267 million acres of Soybeans in crop subsidy programs including prevent plant on 316,367 acres..

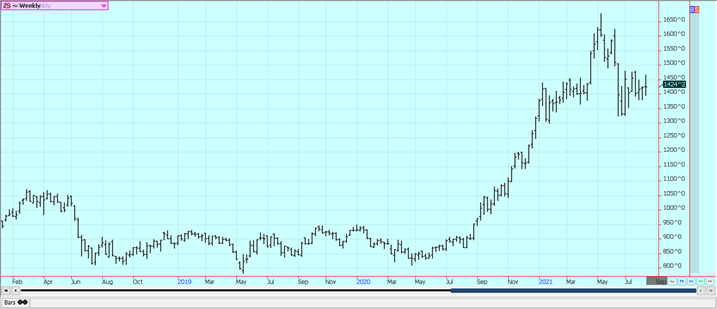

Weekly Chicago Soybeans Futures:

Weekly Chicago Soybean Meal Futures

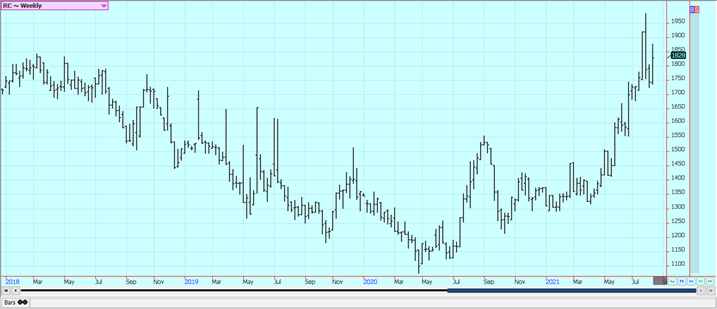

Rice: Rice closed about unchanged on Friday and higher in reaction to the USDA reports. USDA cut its production estimate and ending stocks estimates. The harvest is now expanding through southern growing areas and as traders got ready for the USDA reports that will be released later this morning. Initial yield reports and quality reports have not been real good. Smut has been reported in Texas but the smut is coming off the grain in the cleaning process. The trends are mixed in the market. Traders expect average to weak production. The harvest got started in Texas and southern Louisiana but has been slow in these areas due to rain showers in the region. Both areas have been wet and cloudy this season and average at best yields are expected. Initial reports from Texas suggest that average yields are very optimistic. The harvest pace is expected to be slow due to ongoing showers in both regions. Ideas of average yields at best are also heard in Arkansas and Mississippi. The market expects smaller production this year due to reduced planted area and some weather extremes seen through the growing season to date. Growing conditions have been mixed at best with many areas getting too much rain. Asian prices are mostly steady this week.

Weekly Chicago Rice Futures

Weekly Malaysian Palm Oil Futures: Palm Oil closed higher Friday and for the week. Futures are still a trading range market on ideas of tight supplies due to labor problems. There are just not enough workers in the fields due to Coronavirus restrictions. Production has also been down to more than offset the export losses so prices have trended higher. Canola closed higher last week as damaging weather continues in the Canadian Prairies and northern Great Plains. Production ideas are down due to the extreme weather seen in these areas. It remains generally dry and warm in the Prairies. Some showers in the forecast for this week have no chance to be very beneficial as the Prairies crops are in big trouble now due to previous hot and dry weather and the rains are coming too late.

Weekly Palm Oil Futures

Weekly Chicago Soybean Oil Futures

Weekly Canola Futures:

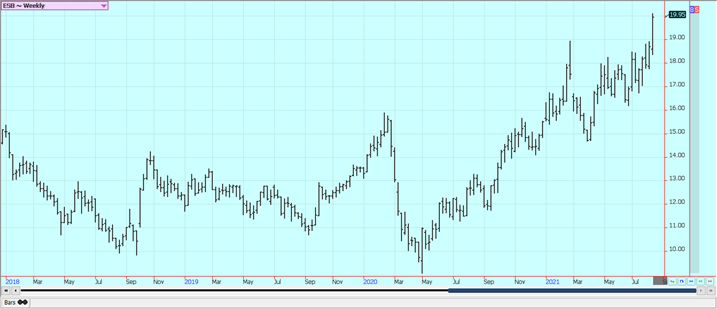

Cotton: Futures were higher last week, with much of the buying in response to the USDA reports. Actual US production and ending stocks estimates were far less than trade expectations and the reason for the rally. Prices can continue to climb in the coming days. Showers are falling in Texas and throughout the major growing areas of the south. Ideas of strong demand continue but the weekly reports have shown more like an average demand. The demand is expected to be strong from Asian countries as world economies recover from Covid lockdowns. Analysts say the demand is still very strong and likely to hold at high levels for the future. However, the expansion of the Delta variant has given pause to the better demand ideas due to fears of economies here and around the world starting to partially lockdown again. Production ideas are being impacted in just about all areas due to the weather extremes. It has been very hot in parts of Texas and the Delta and Southeast have had drenching rains at various times in the last couple of months.

Weekly US Cotton Futures

Frozen Concentrated Orange Juice and Citrus: FCOJ closed higher Friday but a little lower for the week as Florida weather remains non-threatening and the cold weather has passed in Brazil. Freezing temperatures have been reported in Sao Paulo in the last couple of weeks. Weather conditions in Florida are rated mostly good for the crops. The Atlantic is more active and a system is threatening western parts of the state this weekend. Some Orange groves reported excessive rain from this event but little if any wind damage. Mexican crop conditions in central and southern areas are called good with rains, but earlier dry weather might have hurt production. Northeastern Mexico areas are too dry, but the rest of northern and western Mexico are rated in good condition. Demand news has been bad with Nielsen reporting a third month of declining sales. The sales are now the weakest since the Pandemic began and are likely to head lower as the world and the US emerge from the pandemic.

Weekly FCOJ Futures

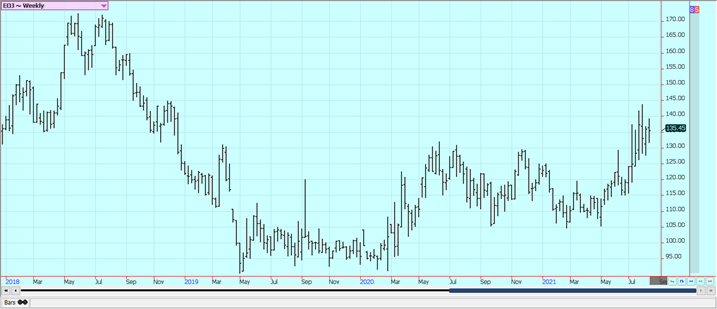

Coffee: New York and London closed higher last week on the adverse weather for Brazil Arabica Coffee areas. Prices have stayed firm as the current Brazil harvest starts to wind down. The freeze threat in Brazil has passed but the damage has been done. The government in Brazil estimates that 11% of the Coffee areas were affected. Temperatures are warmer with near to above normal readings expected. It is flowering time for the next crop and the flowers were frozen and will drop off the trees. It is also harvesting time and the crop is now 89% harvested. The current outlook calls for 10 days of dry weather which will not support the flowering either. Improved showers are now in the forecast for Southeast Asia. Little demand is showing for Vietnamese Coffee as containers to ship the Coffee are hard to find. Good conditions are reported in northern South America and good conditions reported in Central America. Colombia is having trouble exporting Coffee due to protests inside the country. Conditions are reported to be generally good in parts of Africa, but Ivory Coast and Ghana have been a little dry.

Weekly New York Arabica Coffee Futures

Weekly London Robusta Coffee Futures

Sugar: New York and London were higher again as the temperatures have moderated in Brazil. Chart trends are up in both markets. The freeze and drought damage is there and UNICA last week noted less second-half July production because of all the damage that the cane crops have sustained. Ideas are now that the Brazil processing and exporting season will end very early due to the freezes. Ideas are that the damage from previous freezes and drought episodes should show up in processing data for August as well. London has been the weaker market but has firmed a bit lately with the problems in Brazil and trends in this market could now be turning up. There is plenty of White Sugar available in India for the market and monsoon rains are promoting good conditions for the next crop. Thailand is expecting improved production. Ethanol demand is returning to the market as more world economies open up after the pandemic, but renewed Ethanol demand is now in doubt with weaker Crude Oil futures and covid pandemic fears as the Delta variant spreads.

Weekly New York World Raw Sugar Futures

Weekly London White Sugar Futures

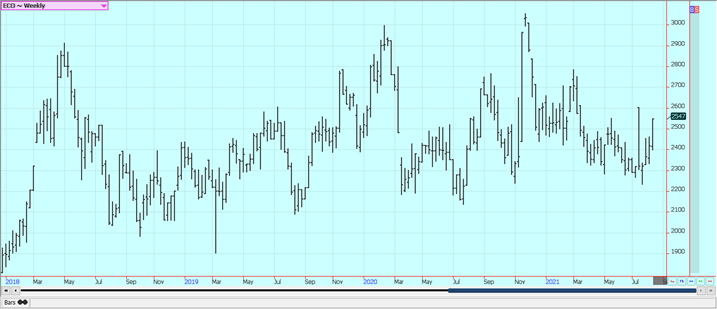

Cocoa: New York and London closed higher last week and trends remain up in both markets. London was the stronger market. Ivory Coast has forward sold 1.4 million tons of beans and has stopped selling for the next crop on fears of less supplies. The grind data was released recently and showed a strong recovery from the Covid times. World economies are starting to reopen after Covid and the open economies are giving demand the boost. Ports in West Africa are filled with Cocoa right now. The weather has had below to rains in West Africa and crop conditions are rated good. Ivory Coast arrivals are now 2.11 million tons, up 4.8% from last year. Ivory Coast processed 452,000 tons of beans by the end of July, down 3.6% from last year.

Weekly New York Cocoa Futures

Weekly London Cocoa Futures

—

(Featured image by gedsarts via Pixabay)

DISCLAIMER: This article was written by a third party contributor and does not reflect the opinion of Born2Invest, its management, staff or its associates. Please review our disclaimer for more information.

This article may include forward-looking statements. These forward-looking statements generally are identified by the words “believe,” “project,” “estimate,” “become,” “plan,” “will,” and similar expressions. These forward-looking statements involve known and unknown risks as well as uncertainties, including those discussed in the following cautionary statements and elsewhere in this article and on this site. Although the Company may believe that its expectations are based on reasonable assumptions, the actual results that the Company may achieve may differ materially from any forward-looking statements, which reflect the opinions of the management of the Company only as of the date hereof. Additionally, please make sure to read these important disclosures.

Futures and options trading involves substantial risk of loss and may not be suitable for everyone. The valuation of futures and options may fluctuate and as a result, clients may lose more than their original investment. In no event should the content of this website be construed as an express or implied promise, guarantee, or implication by or from The PRICE Futures Group, Inc. that you will profit or that losses can or will be limited whatsoever. Past performance is not indicative of future results. Information provided on this report is intended solely for informative purpose and is obtained from sources believed to be reliable. No guarantee of any kind is implied or possible where projections of future conditions are attempted. The leverage created by trading on margin can work against you as well as for you, and losses can exceed your entire investment. Before opening an account and trading, you should seek advice from your advisors as appropriate to ensure that you understand the risks and can withstand the losses.

Youth Cannabis Use in Colorado Is Falling — But the Full Story Is More Complex

The 2026 Colorado survey shows teen cannabis use fell to 10 percent in 2025, down from 21 percent in 2015....

Morocco’s Growth Holds at 4.6% as Agriculture Offsets Economic Pressures

Morocco’s economy grew 4.6% in Q1 2026, driven by a strong agricultural rebound offsetting declines in industry. Services expanded moderately...

Abivax Shares Surge as New Trial Data Eases Safety Concerns Over Ulcerative Colitis Drug

Abivax shares surged nearly 36% after positive updated trial results for its ulcerative colitis drug obefazimod reassured investors following earlier...

El Dorado Raises $9M to Expand Cross-Border Fintech Platform

El Dorado, a Latin American fintech improving cross-border financial services, raised a $9 million Series A led by Paradigm with...

Bitcoin Stalls Near $60K as Strategy Moves, ETFs Outflow, and EU MiCA Rules Take Effect

Bitcoin hovers near $60,000 with ETF outflows, while Strategy boosts reserves, sells BTC, and raises dividends to reassure investors. Ethereum...

|

|

|  |

|

|

-

Biotech1 week ago

Biotech1 week agoGalicia Launches €805M Biotechnology Strategy to Drive Innovation and Competitiveness (2026–2030)

-

Crypto2 weeks ago

Crypto2 weeks agoBitcoin and Ethereum Markets Steady as Strategy and Bitmine Expand Holdings Amid World Cup Crypto Activity

-

Impact Investing5 days ago

Impact Investing5 days agoESG Gap Persists as Firms Struggle to Link Sustainability to Financial Value

-

Crowdfunding2 weeks ago

Crowdfunding2 weeks agoTemotiva Launches Crowdfunding Campaign to Advance Preventive Mental Health