Business

Coffee producers in Brazil, Vietnam not selling much due to perceived low prices

Rainy season could impact coffee quality and yields, while sugar prices closed higher again in New York.

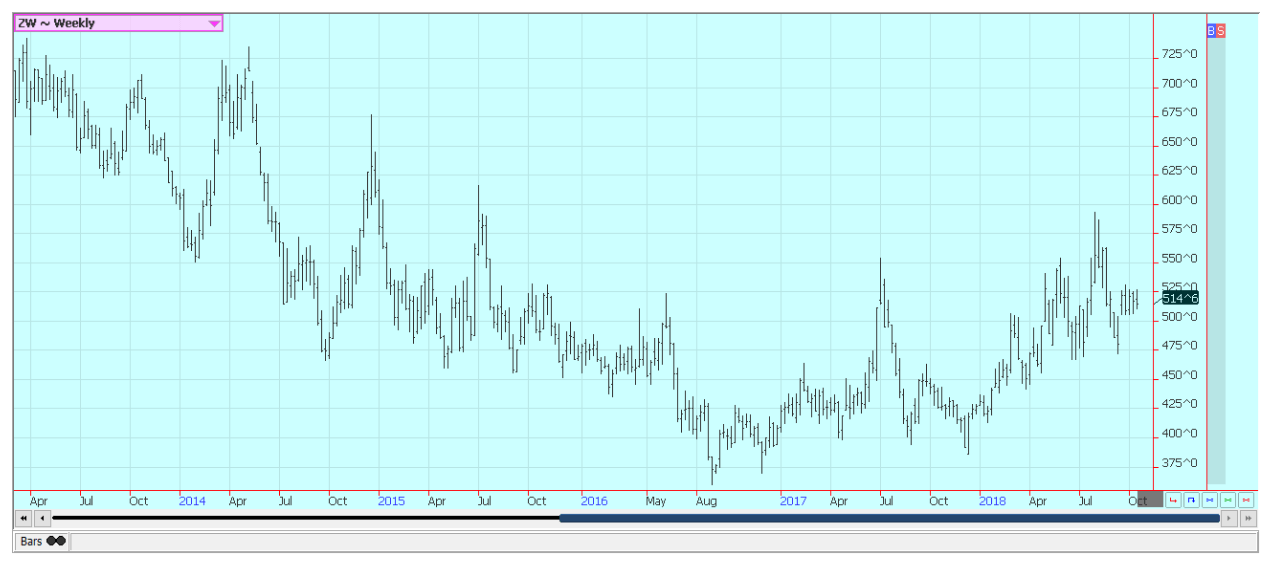

Wheat

Wheat was lower last week as the market still looks for more demand to go with the reduced world production. World crop reports continue to indicate less production and tightening supplies. There will be quality and yield losses in Canada to go with the reduced crops from other major exporters around the world. Firm prices extend from Russia to Australia on reduced world production.

It remains very dry in Australia, and yield and production estimates continue to drop well below those estimated by USDA. It is reported to be wet and cold in Siberia, but planting conditions are reported to be improved near the Black Sea.

The Spring wheat harvest in Siberia has been delayed. The problem is that these production problems have not translated into new demand for U.S. wheat. Bullish traders think it is just a matter of time before world buyers turn to the U.S. as the other major exporters would be out of wheat for export, but the buyers are still looking everywhere they can for other origins and are trying to avoid U.S. wheat.

The weather in the U.S. is improved for planting the next Winter wheat crop as much of the Great Plains has seen rains, and soil moisture conditions are thought to be very good.

Weekly Chicago Soft Red Winter Wheat Futures © Jack Scoville

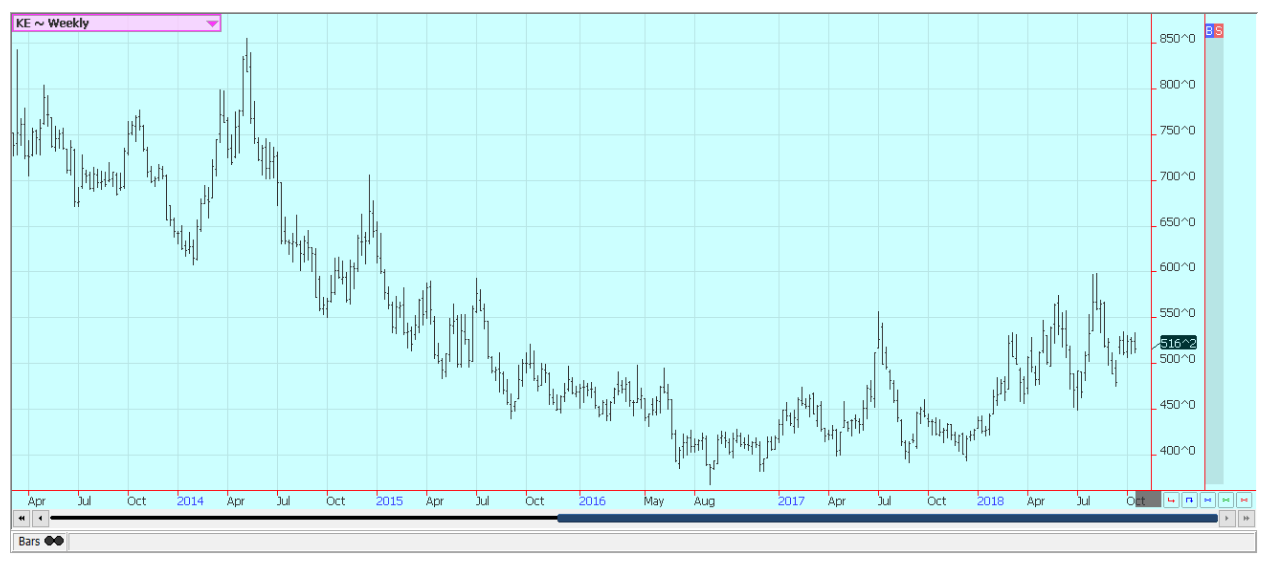

Weekly Chicago Hard Red Winter Wheat Futures © Jack Scoville

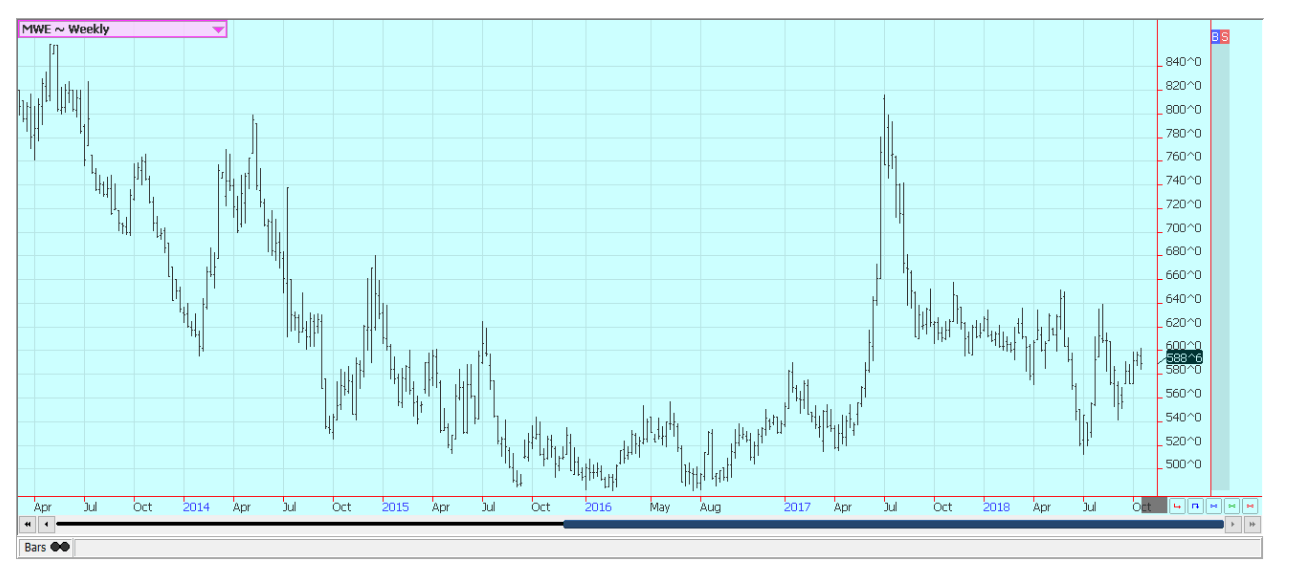

Weekly Minneapolis Hard Red Spring Wheat Futures © Jack Scoville

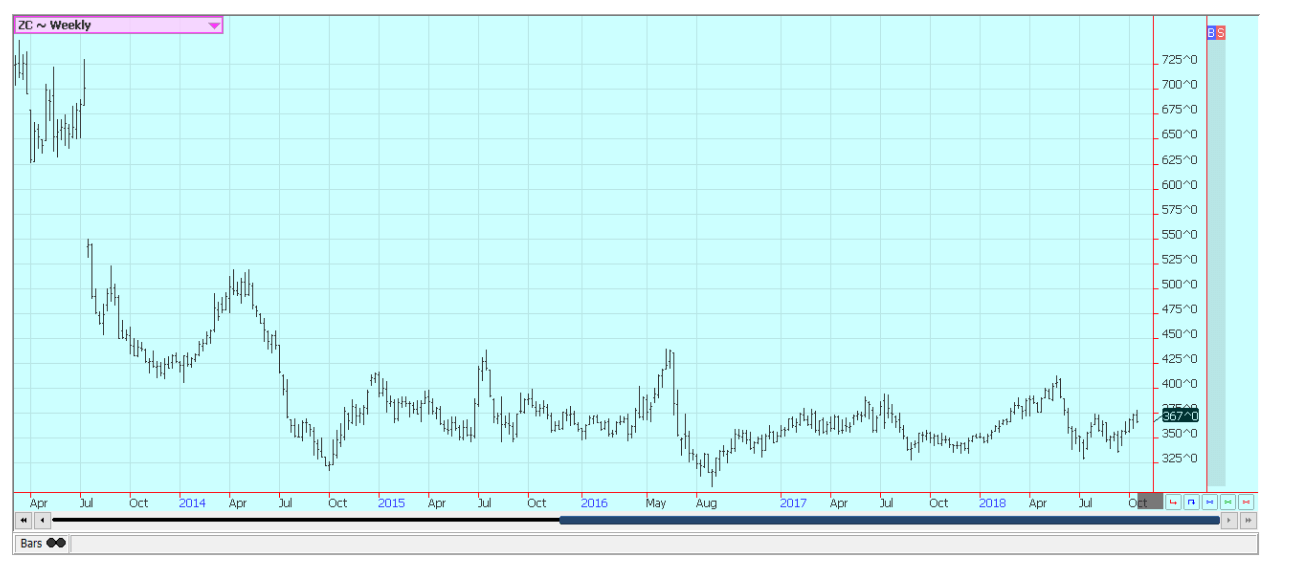

Corn

Corn was lower for the week and faded after making new highs for the move. Demand was a problem as the weekly export sales report was very bad on Thursday and as ethanol use was lower as well. The charts show that December futures made initial targets for the move before backing off late in the week. Chart patterns remain bullish and point to moves to just under 400 December over time. The support came from short covering from funds and other speculators who had expected larger yield and production estimates.

The harvest continues to roll along with at least some work going on in parts of the Midwest. Rain started to delay harvest progress most of last week, but conditions are mostly dry and cool and the harvesters should be running. Some producers in Iowa said that corn was starting to lose quality due to the harvest delays and reports of diseases and perhaps mold. Harvest data as reported by producers still suggest that the crop can be another very big one.

Weekly Corn Futures © Jack Scoville

Weekly Oats Futures © Jack Scoville

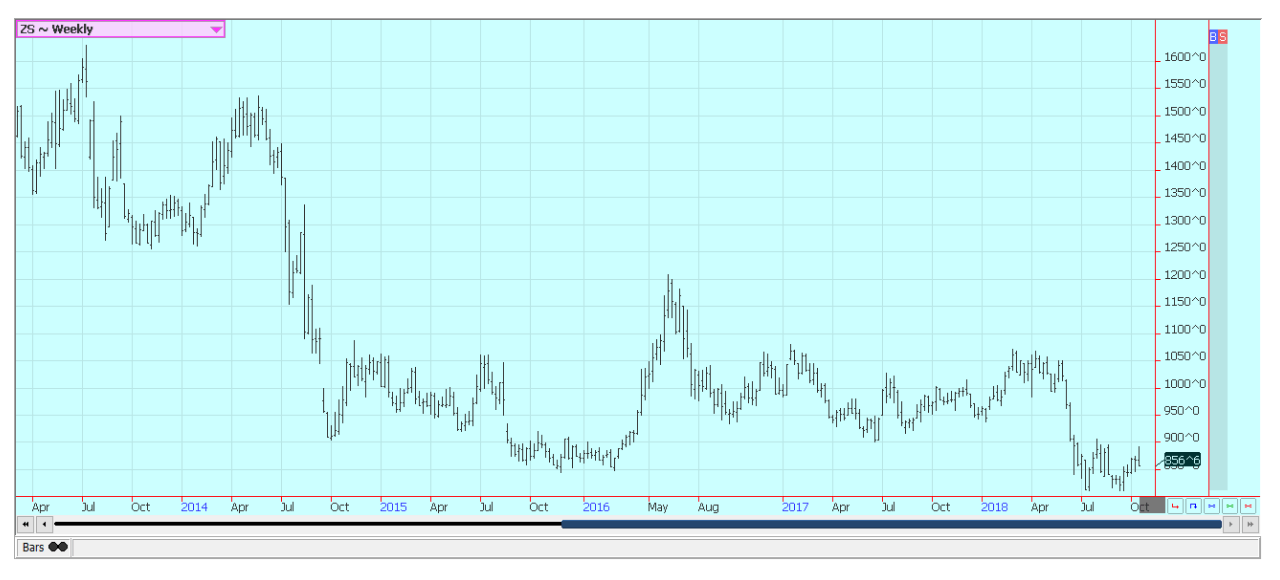

Soybeans and soybean meal

Soybeans were slightly lower last week, and Soybean Meal was a little higher. Selling came on weak demand as ween in the export sales report and from news that Commerce Secretary Ross had said that negotiations with China on a new trade program had stalled. The stalled negotiations implied that little would be done before the midterms.

Futures were supported by disease reports as wet Soybeans were getting molded and were sprouting in some areas along with some spillover support from the recent USDA reports. The reports indicated less production than expected, but it is still expected to be a huge crop, and the US might have trouble getting it moved to the point where ending stocks are small enough to make a difference in prices. Current ending stocks estimates are still more than ample, and the weekly export sales report was poor.

Brazil is still doing all the business with China despite the wide disparity in prices, and the rest of the world should not be able to make up for the lost business with China for the US. US producers are still trying to harvest, but have been shut down by rains for several days. Some producers in Iowa and to the west are reporting yield losses and quality losses from the rains that have caused some sprouting and mold to form. Freezing temperatures were seen in northern and western areas and should prove beneficial for harvest progress and the cold could help preserve quality in some cases. Futures appear to have made seasonal lows, but ideas are that upside potential is no more than $9.00 per bushel right now.

Weekly Chicago Soybeans Futures © Jack Scoville

Weekly Chicago Soybean Meal Futures © Jack Scoville

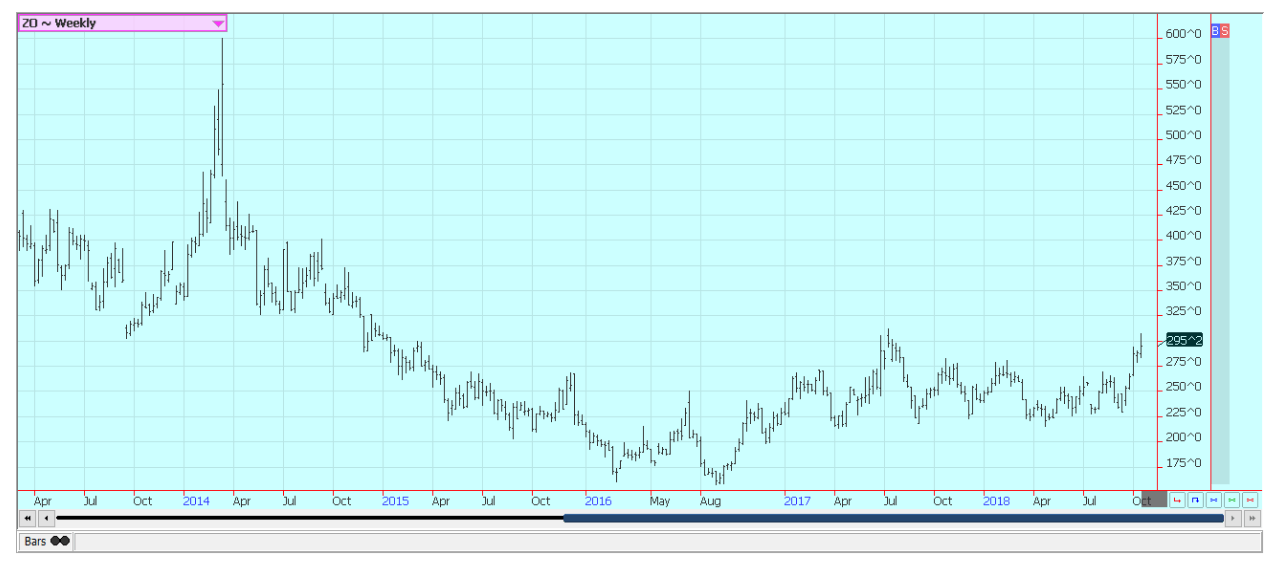

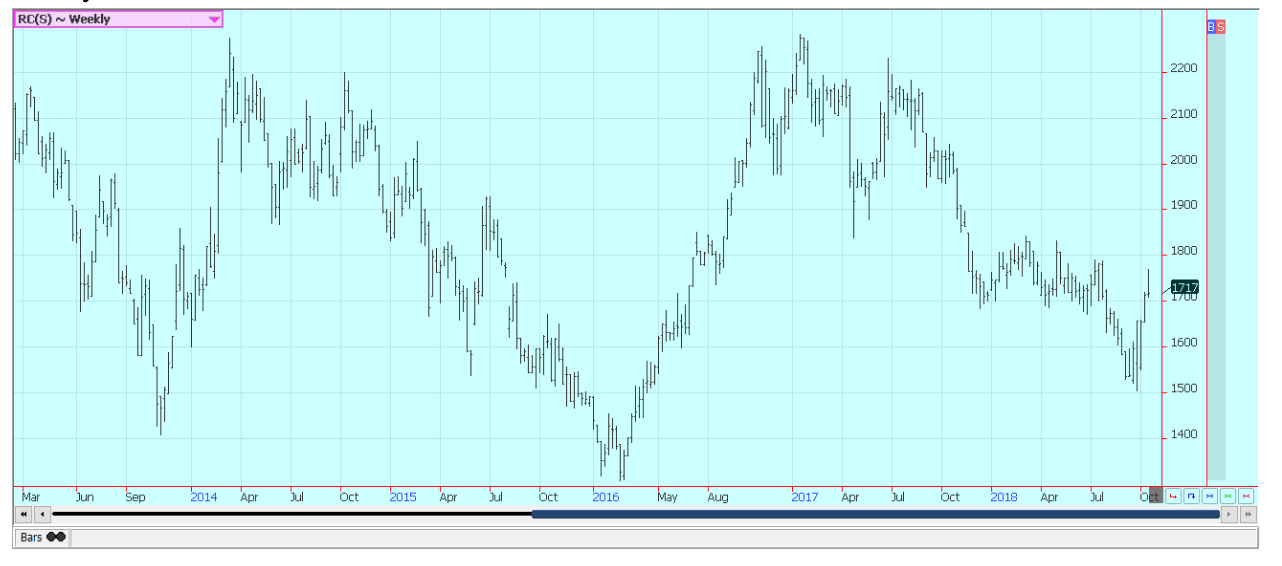

Rice

Rice was higher and closed at the upper end of the weekly range. The chart patterns suggest that nearby futures can run to $11.50 per hundredweight and then to $12.00 per hundredweight in the short to medium term. The harvest is coming to a close in many parts of the Mid South, although there was still a little left to do in Mississippi and Arkansas, and as Texas and Louisiana still were waiting to harvest the second crop. Farmers think prices are too cheap and are still concentrating on harvesting in most areas. Others are storing crops and waiting or doing other activities.

Good to excellent yields have been reported in Texas and Louisiana so far, and good to very good yield reports are being heard in Mississippi and Arkansas. Cash prices are somewhat weaker as mills and elevators fill up. Milling yields have been acceptable to very good. Export demand has been good, and was especially strong last week as futures moved lower. Good export demand is expected to continue.

Weekly Chicago Rice Futures © Jack Scoville

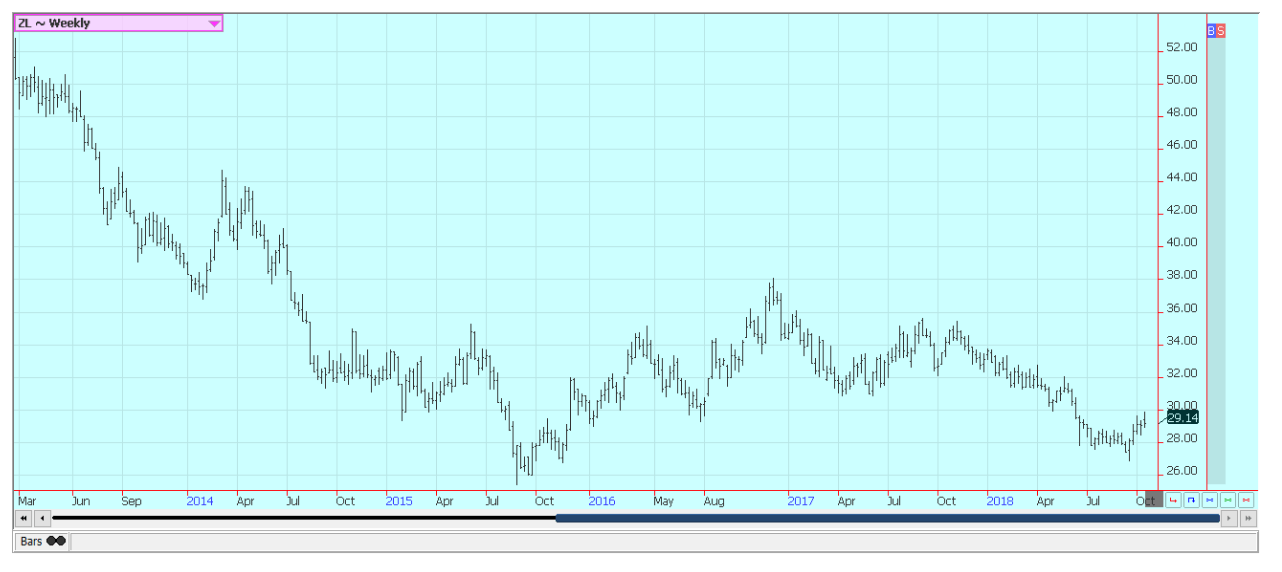

Palm oil and vegetable oils

World vegetable oils prices were mostly higher again last week. Palm Oil was higher as the front month futures contract rolled forward with the expiration on October futures. Daily charts show that price action is actually weak even though weekly charts show futures in a small trading range.

The private export surveyors reported a slower pace to exports for the first half of the month, and this has been the primary negative for prices. The market is anticipating strong production for the short term as the weather is good for the trees. However, both Malaysia and Indonesia are watching long term trends as El Nino is expected to develop. Indonesian supplies are already less as demand from China has been strong.

The weather could hurt production potential down the road. Soybean Oil closed slightly higher and is trying to confirm a seasonal low on the weekly charts. The market is expecting better demand as world petroleum prices have moved higher. Support is also coming from less offer from South America and on higher Canola prices.

Canola was unchanged on slow harvest progress amid wet and cold weather and reports of slow demand. Farmers have had a tough time getting into the fields due to rains, especially in the west. The weather is now cold, but drier, and farmers are back harvesting again. Progress to date has been significantly behind normal, so the trade will want to hear yield reports again to see if there are new losses. Yield reports so far are said to be below expectations and ideas are that StatsCan has overestimated production potential this year.

Weekly Malaysian Palm Oil Futures © Jack Scoville

Weekly Chicago Soybean Oil Futures © Jack Scoville

Weekly Canola Futures © Jack Scoville

Cotton

Cotton was slightly lower for the week on demand concerns. Export sales for the last few weeks have been poor and show no real signs of improvement for now. News that Commerce Secretary Ross has said that negotiations with China had stalled hurt prices along with less demand from other buyers such as Vietnam and Turkey. Export demand needs to improve soon for prices to rally significantly this year, but any increase in demand has to come with no purchases from China for a while.

The trade in India remains optimistic that a good crop is coming and that they will not need to import very much Cotton this year. China has been active in India buying and will buy as much as possible there to make up for production losses inside of China. USDA estimated production down in India and Pakistan due to bad weather during the growing season, so India might not be able to cover all the Chinese demand.

Hurricane Michael ripped into Georgia two weeks ago and then into the Carolinas and brought devastating winds and rain to growing areas in Georgia. Social media showed pictures of widespread devastation in Cotton fields, with many plants blown over and destroyed and Cotton on the ground. Chart trends remain down.

Weekly US Cotton Futures © Jack Scoville

Frozen concentrated orange juice and citrus

FCOJ was lower last week on a big increase in Florida oranges production as estimated by USDA and as the Oranges harvest is underway. USDA estimated all oranges production at 79 million boxes, with improvements shown in both the early and mid categories and the Valencia categories. Good weather continues in Florida and as prospects for a much improved crop from a year ago continue. Chart trends are down as futures stayed below some important resistance on the weekly charts.

Overall growing conditions in Florida are good to very good, and there is no storm development in the Atlantic at this time, or at least nothing that would impact the state. Florida producers are seeing good sized fruit, and work in groves maintenance is active. Irrigation is being used when needed, and producers expect a good crop. Packing houses are open to process fruit for the fresh market, and one major processor is open in the state to take packing house eliminations.

Weekly FCOJ Futures © Jack Scoville

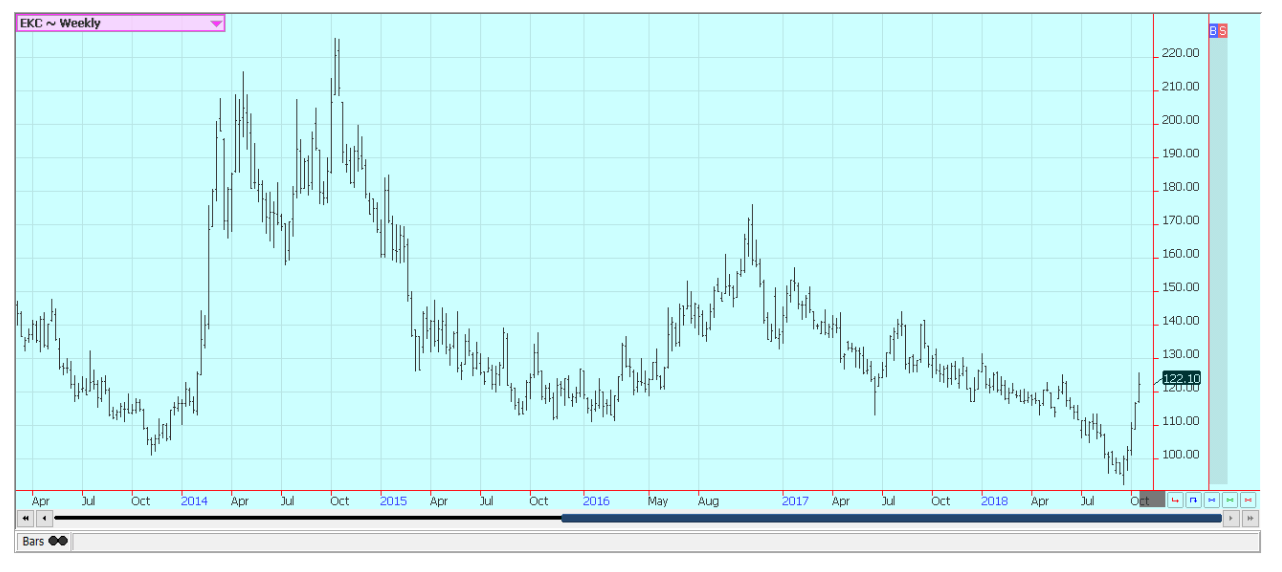

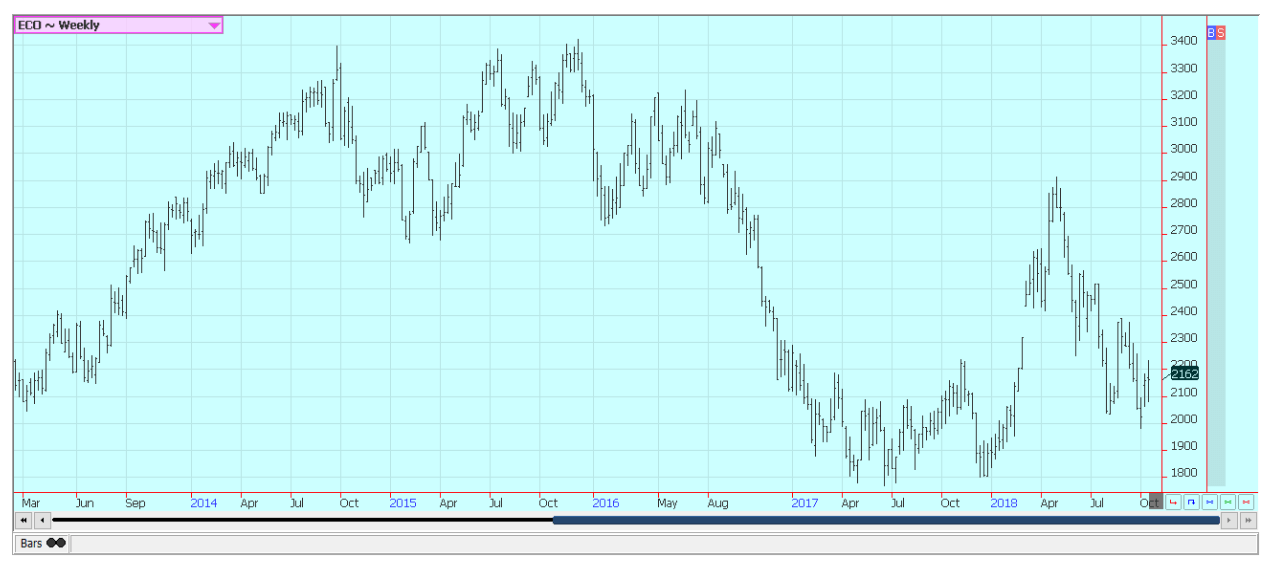

Coffee

Futures were higher again last week in New York, but closer to unchanged in London. Trends are still up in both markets, and weekly charts show that futures had their best few weeks of upside action in years. It has been primarily a short covering rally as funds and other speculators have been buying out short positions due to trend changes in the Brazilian Real. The Real has found support as the right wing candidate for president in Brazil won the first round of elections and leads for the second round over the workers party candidate.

Ideas of strong production in Brazil and Vietnam have been keeping futures under selling pressure. Vietnam is getting close to its next harvest, and ideas are that producers there need to sell more of the previous crop to create new storage space. Producers in both countries are not selling much due to perceived low prices. Some problems with too much rain have been noted in Central America. Drier conditions are wanted for harvesting, but big rains are being reported in most of the region instead. The rains could eventually impact quality and yields and could make processing and drying of the beans very difficult.

Weekly London Robusta Coffee Futures © Jack Scoville

Weekly New York Arabica Coffee Futures © Jack Scoville

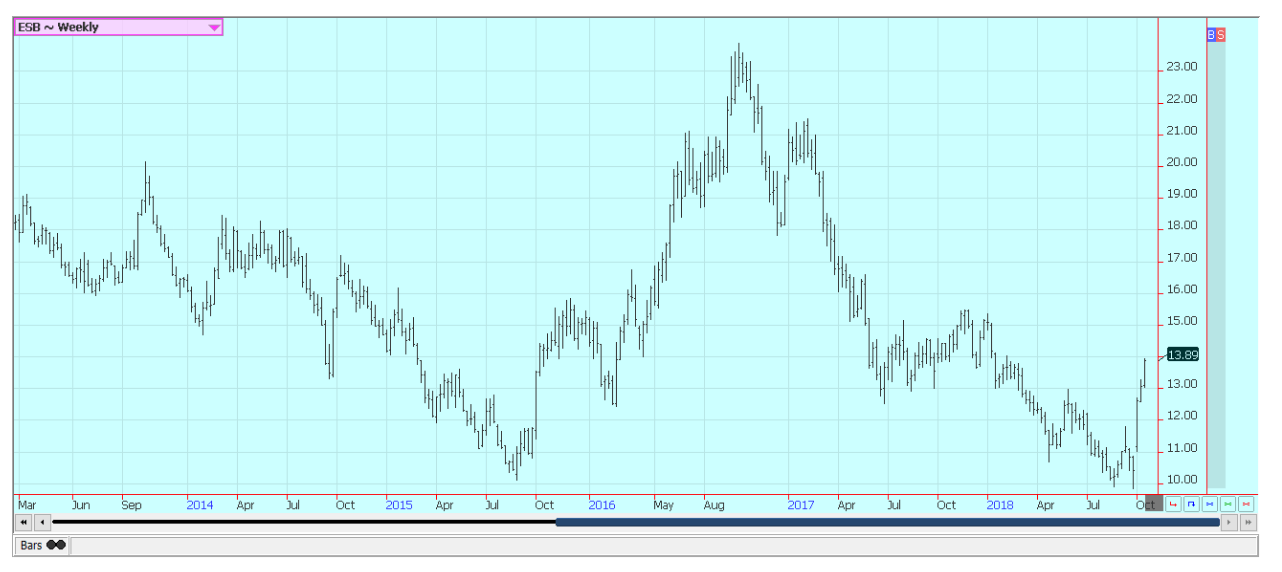

Sugar

New York closed higher again last week and moved very close to strong resistance near 1400 NY March. London was higher as well. Both markets are showing that medium term lows have been made on the weekly charts. Sugar was supported by reduced selling in Brazil due to the presidential elections that were held last week and ideas of increasing inflation in the US. The Real has been gaining on the US Dollar as a result and this has served to limit export interest in Brazil.

Ideas of big world production are bearish and have been the reason for the selling, but now there are doubts on just how much production will be seen this year in India. Wire reports indicate that pests have invaded Sugarcane fields and are eating and destroying the crop. There is no indication of losses yet, but the implication of the reports is that the losses could be significant.

Northwest India had been experiencing hot and dry weather that could cut yields. Dry conditions continue in Brazil, the EU, and Russia, but conditions are mostly good in Ukraine. Very good conditions are reported in Thailand. Brazil producers are worried about Cane production, and the market still talks about less production there this year. The dry weather in much of Europe and in southern Russia near the Black Sea has hurt Sugarbeets production potential in these areas.

Weekly New York World Raw Sugar Futures © Jack Scoville

Weekly London White Sugar Futures © Jack Scoville

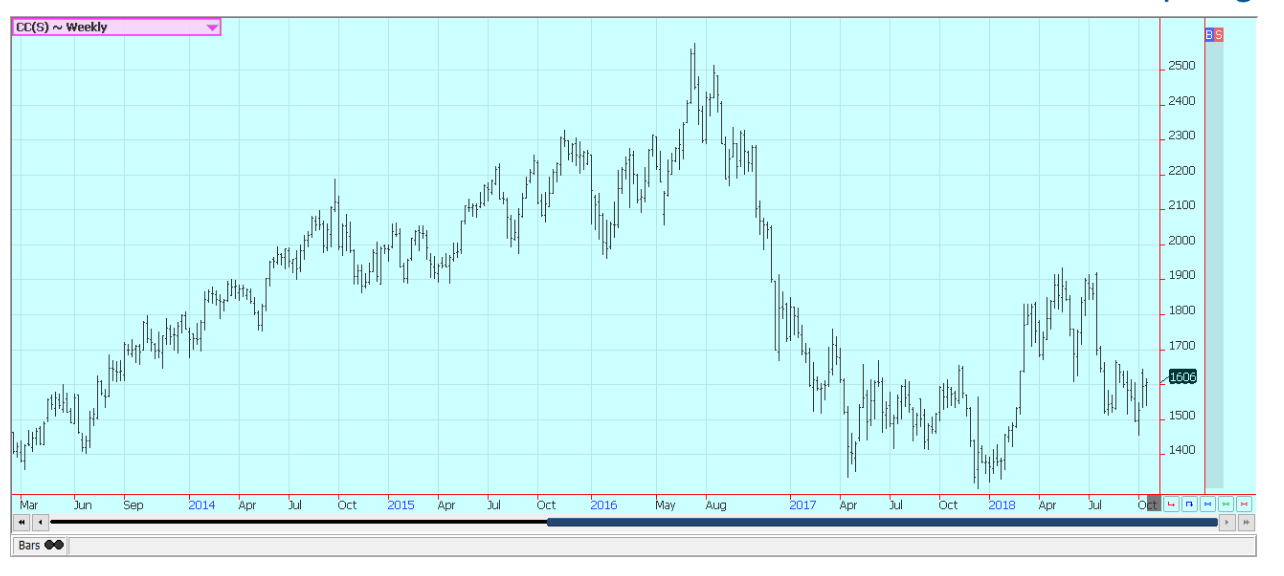

Cocoa

Futures closed near unchanged in New York and a little higher in London as the new main crop harvest comes to market in West Africa. Trends remain down on the weekly charts for New York, but are now more like sideways in London. The recovery has been impressive as it is time for offers from the West Africa harvest to start increasing.

The outlook for strong production in the coming year has been enough to keep the prices weak, but there are some disease concerns for West Africa as a lot of humid air has promoted some concerns that Black Pod Disease could spread. In fact, initial harvest reports from Nigeria indicate reduced yields due to too much rain as the main crop was maturing. The main crop harvest is in its earliest stages in some parts of West Africa. Main crop production ideas for Ivory Coast and Ghana are high, but are being reduced in Nigeria. Conditions also appear good in East Africa and Asia. Demand is said to be improving as offers from the new harvest start to increase. The grind data released last week was strong and provided some support for futures markets.

Weekly New York Cocoa Futures © Jack Scoville

Weekly London Cocoa Futures © Jack Scoville

—

DISCLAIMER: This article expresses my own ideas and opinions. Any information I have shared are from sources that I believe to be reliable and accurate. I did not receive any financial compensation for writing this post, nor do I own any shares in any company I’ve mentioned. I encourage any reader to do their own diligent research first before making any investment decisions.

Why 2026 Could Mark a Turning Point for Sustainability

Amid geopolitical crises and climate pressures, companies must seek alternative strategies, as sustainability becomes a key driver of value. By...

Dow Jones Rebounds as Markets Shrug Off Iran Conflict

A shortened trading week saw the Dow Jones rebound from a 10 percent correction, closing between key BEV levels. Outlook...

Iran War Drives Oil Surge and Rising Financial Risks

The war continues pushing oil prices higher, with Brent above 140 while futures lag. Energy stocks weakened despite highs. Headline...

TopRanked.io Weekly Affiliate Digest: What’s Hot in Affiliate Marketing [Bovada Affiliate Program]

This week, we're mashing up 80s tech with 2020s private messaging apps. Why? Because Big Tech just dropped a big...

Euro Stablecoins Struggle to Compete with Dollar Dominance in Crypto Markets

Euro stablecoins remain marginal despite the euro’s global importance, with minimal trading volume compared to dollar rivals like USDT and...

|

|

|  |

|

|

-

Business2 weeks ago

Business2 weeks agoGlobal Markets on Edge as Iran Conflict, Inflation Pressures, and Financial Risks Intensify

-

Business3 days ago

Business3 days agoTopRanked.io Weekly Affiliate Digest: What’s Hot in Affiliate Marketing [Bovada Affiliate Program]

-

Biotech1 week ago

Biotech1 week agoNHS Funds Breakthrough CAR-T Therapy Breyanzi for Lymphoma Treatment in Spain

-

Fintech6 days ago

Fintech6 days agoCrypto Lending Hits $30 Billion, Becomes Key DeFi Pillar

You must be logged in to post a comment Login