Featured

Commodities Markets Are Mixed, with Corn Demand Slowly Improving

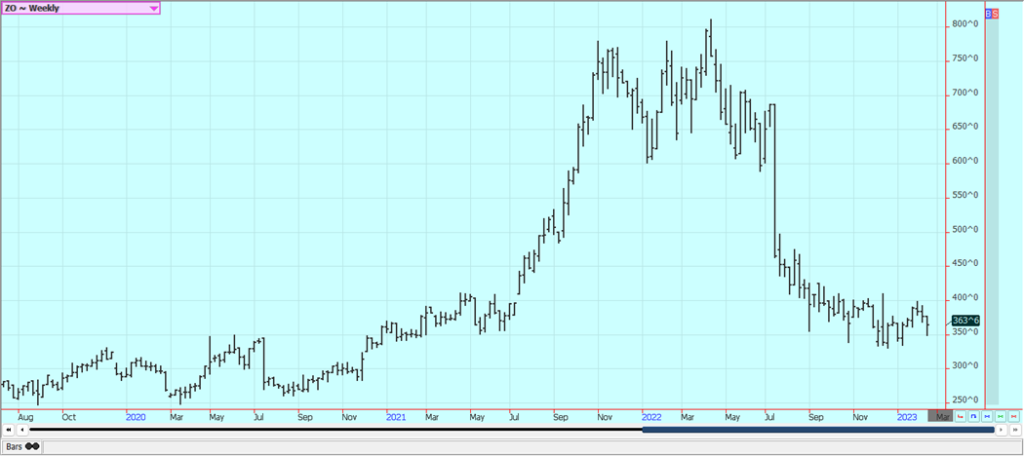

Corn and Oats closed lower last week, but Corn held well as demand is slowly improving. US prices are currently very competitive with those from South America and US demand has improved because of the price differentials. Prices from South America should now remain strong as countries there concentrate on Soybeans exports, so the US has a chance now to see export demand improve more than it has already.

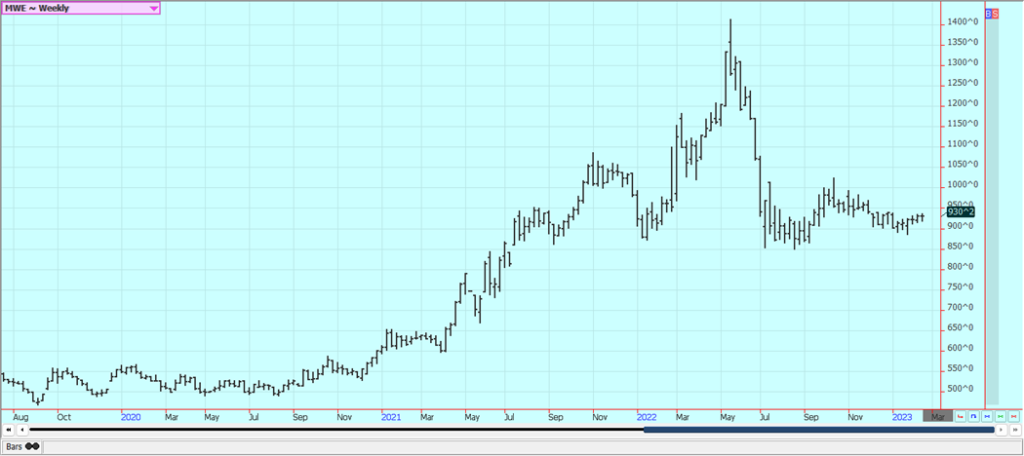

Wheat: Wheat markets were mixed last week, with SRW and HRW futures in Chicago a little lower but Minneapolis Spring futures unchanged for the week. News that Russia has launched a new offensive in Ukraine provided much of the support this week. Russia appears to be sending three divisions across the border to fight and it looks as though this could be a major operation for the Russian army. Wire reports now suggest that Russia has now committed almost its entire army to the war. Fears of deliveries of Wheat from the Black Sea will be cut significantly are surfacing again. Ideas are that both Australia and Russia are harvesting record to near-record Wheat crops this year. Russia is said to be plotting a huge new invasion of Ukraine that could prevent farmers in Ukraine from harvesting Wheat and planting Corn. Russia has a large production and is undercutting most world prices in the international market. However, Russian production estimates have dropped recently. The demand for US Wheat in international markets has been a disappointment all year and has been hindered by low prices and aggressive offers from Russia. Ukraine is also looking for new business for its crops and Russia is aggressive in the world market as it looks for cash to fund the war.

Weekly Chicago Soft Red Winter Wheat Futures

Weekly Chicago Hard Red Winter Wheat Futures

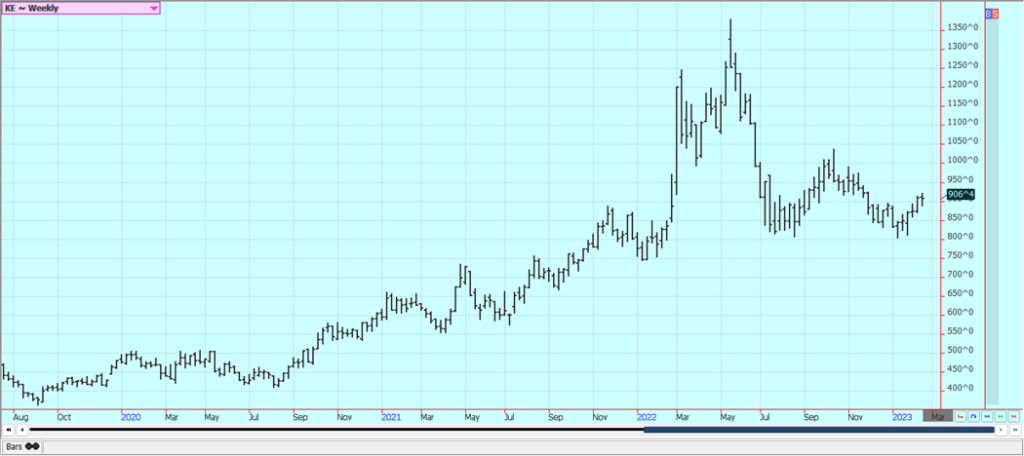

Weekly Minneapolis Hard Red Spring Wheat Futures

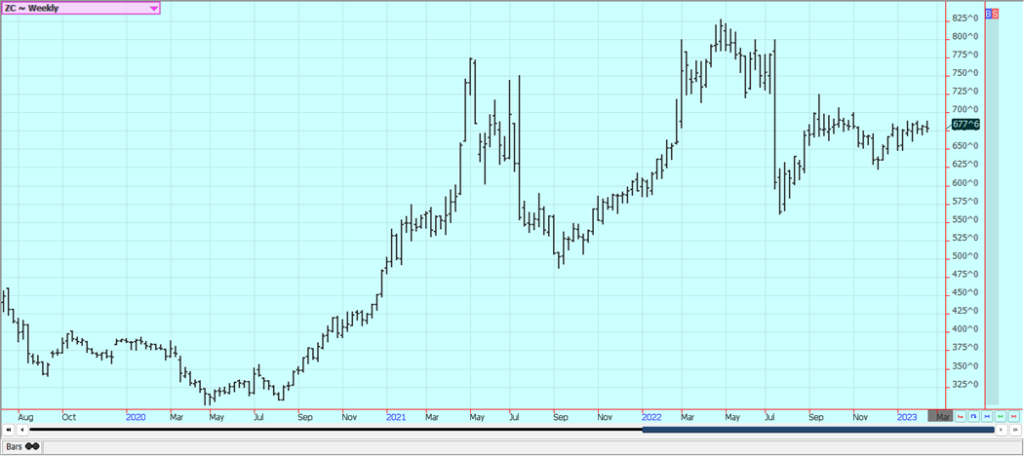

Corn: Corn and Oats closed lower last week, but Corn held well as demand is slowly improving. US prices are currently very competitive with those from South America and US demand has improved because of the price differentials. Prices from South America should now remain strong as countries there concentrate on Soybeans exports, so the US has a chance now to see export demand improve more than it has already. The export demand remains well behind the pace to make USDA objectives. Brazil has been hanging on for its Summer crop although losses are now being reported. Argentina has suffered through some extreme drought and losses could be large. The Brazil Winter crop is harvested and China has been buying the surplus. The Summer crop and the Argentine crop is developing under stressful conditions. The next Winter crop is going into the ground in good conditions, but it has been wet so the Soybeans harvest has been delayed and the Corn planting is becoming delayed as well. There are concerns about demand with the Chinese economic problems caused by the lockdowns creating the possibility of less demand as South America has much better crops this year to compete with the US for sales. China is now moving rapidly to open the economy and allow people to move around with no lockdowns so the demand could start to improve

Weekly Corn Futures

Weekly Oats Futures

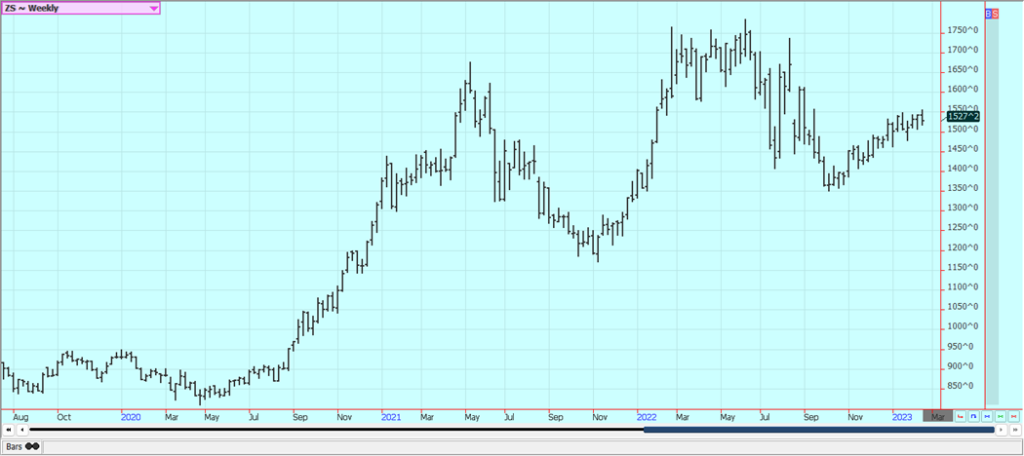

Soybeans and Soybean Meal: Soybeans and Soybean Meal were lower last week, but Soybean Oil closed a little higher. The market is weaker in anticipation of the South American harvest coming to export channels in the near term. It remains hot and dry in Argentina and southern Brazil and crop conditions are getting worse. However, the weather is becoming less important now as the harvest is already underway in central and northern Brazil and will spread south soon. Central and northern Brazil have seen harvest operations interrupted with too much rain. Soybean Meal saw strong weekly export sales as Argentina is having to withdraw from the market for Soy products sales due to the drought in the country and the fact that they have already sold a lot of Soybeans into the world market. They are now buying from Brazil. The harvest in Brazil is slowly expanding in central and northern areas. These areas have seen too much rain and the harvest has been slow. Production potential for the Brazil is called very strong even with potential problems and losses in the south. Argentine production ideas continue to drop with the drought as planting is delayed and the crops already in the ground are stressed. Ideas that Chinese demand will improve, but this could take a few more weeks as a very large part of the population now has Covid. This has delayed a robust economic return for the country.

Weekly Chicago Soybeans Futures:

Weekly Chicago Soybean Meal Futures

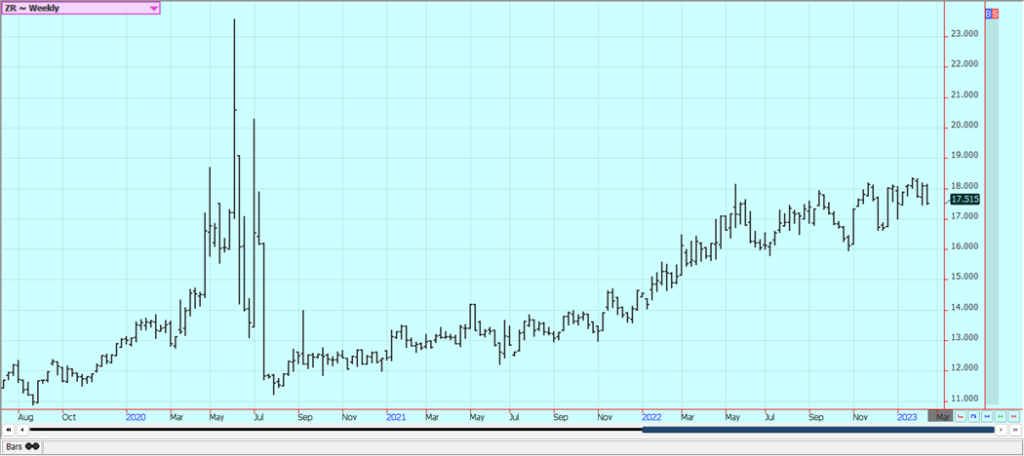

Rice: Rice was lower last week but held to the recent trading range. Reports indicate that the farmers have been selling and ideas are that they might dump on the market if they think a big crop is coming at the end of the new growing season that is now getting ready to start in southern growing areas. Demand has been good from domestic sources. Export demand has been uneven. Demand has been an issue for the market all year. There is not much going on in the domestic market right now although mills are milling for the domestic market in Arkansas and are bidding for some Rice. Markets from Texas to Mississippi are called quiet. Demand in general has been slow to moderate for Rice for exports and solid for domestic uses.

Weekly Chicago Rice Futures

Palm Oil and Vegetable Oils: Palm Oil closed higher last week on ideas of stronger demand due to the coming Ramadan holiday period and also on price action in Chicago Soybean Oil. Indonesia is now revoking some export permits to keep internal prices controlled and to support the bio fuels industry. The controls are expected to last through Ramadan. China has tried to relax some Covid restrictions so that the economy can start to function again. However, new outbreaks of the virus are being reported and infection rates are rapidly increasing but will start to decrease soon as most have now had Covid. There are still reports of too much rain in Malaysia. Canola was slightly lower last week in consolidation trading. Reports indicate that domestic demand has been strong due to favorable crush margins. Production was much improved this year on better weather during the Summer.

Weekly Malaysian Palm Oil Futures

Weekly Chicago Soybean Oil Futures

Weekly Canola Futures:

Cotton: Cotton was lower last week on what appeared to be chart-based speculative selling and still remains inside the trading range created since the beginning of November. Short-term trends are now down. Futures are still showing bad demand fundamentals as the weekly export sales reports have shown moderate sales at best. Some ideas that demand could soon increase as China could start to open its economy in the next couple of months as Covid outbreaks should start to weaken as people get vaccinated or immune. Covid is now widespread in China so the beneficial economic effects of the opening are being delayed but these effects should start to be felt as the people there achieve immunity over the next week or two.

Weekly US Cotton Futures

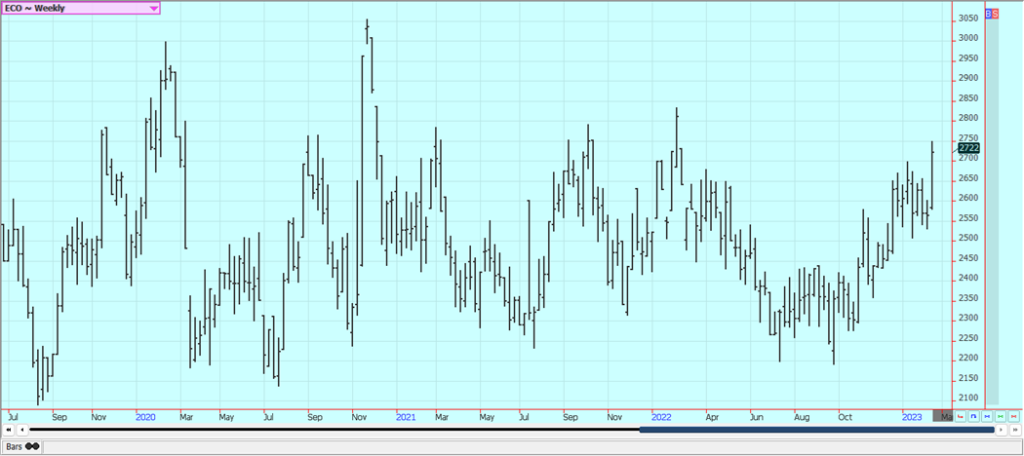

Frozen Concentrated Orange Juice and Citrus: FCOJ was lower last week, but rallied sharply on Friday to close well off the weekly lows after holding support near 128.00 on the weekly charts. Demand should start to weaken again as the northern Winter passes by. Historically low estimates of production due in part to the hurricanes and in part to the greening disease that have hurt production, but conditions are significantly better now with scattered showers and moderate temperatures. The weather remains generally good for production around the world for the next crop including production areas in Florida that have been impacted in a big way by the two storms seen previously in the state. Brazil has some rain and the conditions are rated good. Brazil continues to export to the EU and is increasing its exports to the US. Mexico is also exporting to the US. Even so, the Florida Dept of Citrus reported that inventories are still 40.6% below last year at 102.39 million pounds.

Weekly FCOJ Futures

Coffee: New York and London closed higher last week on higher differentials in Brazil. Producers are not offering right now and the market wants its coffee. Ideas of a big production for Brazil continue due primarily to rains falling in Coffee production areas now. Vietnam is estimated to have very good production this year due to a good growing season and less rain now as harvest expands again. There are ideas that the production potential for Brazil had been overrated. The weather in Brazil is currently very good for production potential but worse conditions seen earlier in the growing cycle hurt the overall production prospects as did bad weather last year.

Weekly New York Arabica Coffee Futures

Weekly London Robusta Coffee Futures

Sugar: New York and London closed a little lower last week in consolidation trading. Ideas are that the market has priced in production losses in India and Brazil and is providing remuneration for Indian and Thai exporters who want to sell. Thailand expects to export 9.0 million tons of Sugar in the current crop year, 7% more than last year. Ideas of better supplies coming might keep futures prices in check even with a rather tight nearby scenario. Good production prospects are seen for crops in central and northern areas of Brazil, but the south should turn dry again and so should some northern areas. There is concern that the rainy areas will stay too wet and delay the harvest and dilute the Sugar concentrations in the cane in central areas. The harvest is active in Thailand. Australian and Central American harvests are also active. European production is expected to be reduced again this year.

Weekly New York World Raw Sugar Futures

Weekly London White Sugar Futures

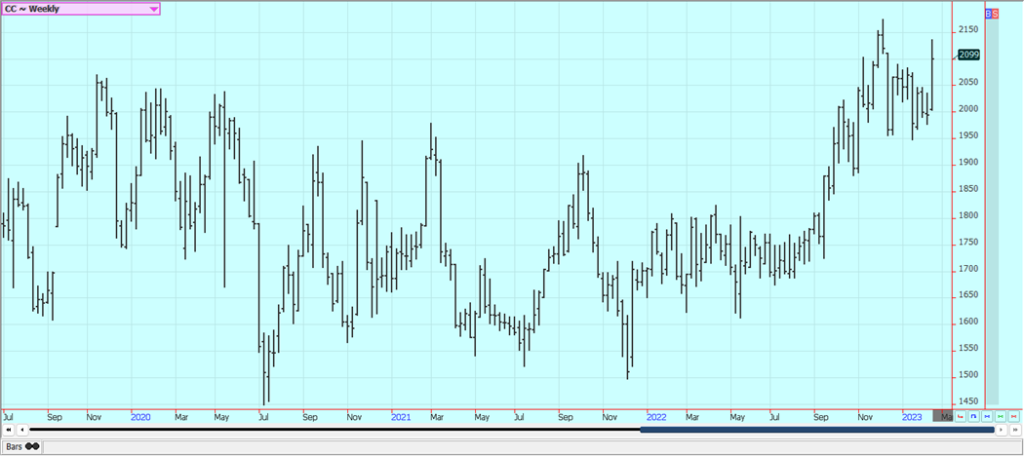

Cocoa: New York and London closed higher last week as West African exporters are not offering. Wire reports suggest that exporters are currently looking for Cocoa to make good on current contracts and are not entering into new contracts right now. Trends have turned up in both New York and London. The talk is that hot and dry conditions reported in Ivory Coast could curtail mid-crop production, but main crop production ideas are strong. Ghana has reported disease in its Cocoa to hurt production potential there. The rest of West Africa appears to be in good condition. Good production is reported for the main crop and traders are worried about the world economy moving forward and how that could affect demand. The weather is good in Southeast Asia.

Weekly New York Cocoa Futures

Weekly London Cocoa Futures

__

(Featured image by jorono via Pixabay)

DISCLAIMER: This article was written by a third party contributor and does not reflect the opinion of Born2Invest, its management, staff or its associates. Please review our disclaimer for more information.

This article may include forward-looking statements. These forward-looking statements generally are identified by the words “believe,” “project,” “estimate,” “become,” “plan,” “will,” and similar expressions. These forward-looking statements involve known and unknown risks as well as uncertainties, including those discussed in the following cautionary statements and elsewhere in this article and on this site. Although the Company may believe that its expectations are based on reasonable assumptions, the actual results that the Company may achieve may differ materially from any forward-looking statements, which reflect the opinions of the management of the Company only as of the date hereof. Additionally, please make sure to read these important disclosures.

Futures and options trading involves substantial risk of loss and may not be suitable for everyone. The valuation of futures and options may fluctuate and as a result, clients may lose more than their original investment. In no event should the content of this website be construed as an express or implied promise, guarantee, or implication by or from The PRICE Futures Group, Inc. that you will profit or that losses can or will be limited whatsoever. Past performance is not indicative of future results. Information provided on this report is intended solely for informative purpose and is obtained from sources believed to be reliable. No guarantee of any kind is implied or possible where projections of future conditions are attempted. The leverage created by trading on margin can work against you as well as for you, and losses can exceed your entire investment. Before opening an account and trading, you should seek advice from your advisors as appropriate to ensure that you understand the risks and can withstand the losses.

Virginia Cannabis Market Could Reshape Regional Competition

Virginia’s planned recreational cannabis market could reshape the Washington region’s economic landscape. With nine million residents, it may draw consumers...

Bitcoin’s Price Drops as Investors Turn to Layer 2 Solutions

Bitcoin fell toward $63,000 after leveraged liquidations erased recent gains, while geopolitical tensions between the US and Iran pressured risk...

Emily.AI: Personalized Oxygen Therapy Earns Global AI Recognition

Emily.AI, Quirónsalud’s explainable AI medical device, became a global finalist at the AI for Good Summit 2026 after competing with...

Advanced Blockchain Under Pressure Amid Crypto Market Shifts

The crypto market shows diverging trends: Advanced Blockchain faces heavy pressure despite restructuring, weak finances, and ongoing transformation, though analysts...

Cannabis Regulation in Germany and Switzerland Shows Early Benefits of Legalization Models

Germany and Switzerland’s cannabis reforms suggest regulated access can reduce criminalization without increasing consumption. Germany saw fewer cannabis-related prosecutions, while...

|

|

|  |

|

|

-

Crowdfunding2 weeks ago

Crowdfunding2 weeks agoSpanish Crowdfunding Market Reaches Record €761.6M in 2025, Driven by Real Estate and Crowdlending Growth

-

Cannabis3 days ago

Cannabis3 days agoGermany Tightens Cannabis Reimbursement Rules: Approved Medicines Must Come First

-

Crowdfunding1 week ago

Crowdfunding1 week agoLemonaid Offers Shares to Consumers for the First Time

-

Crypto4 hours ago

Crypto4 hours agoBitcoin’s Price Drops as Investors Turn to Layer 2 Solutions