Featured

Cotton demand is still at low levels

Cotton closed lower for the week and trends are still sideways on the charts. Demand has improved over the last couple of weeks but remains at depressed levels. The export sales report showed better sales to China but not that much beyond that. Demand should stay week as long as the Coronavirus is a feature of life around the world. Shopping is hard to do and many people are still unemployed.

Wheat

Winter Wheat markets were lower last week and on Friday as USDA released its latest supply and demand and production reports. No changes were made to the US estimates and this was as expected by the trade. USDA increased ending stocks estimates for the new crop year to 319.4 million tons from 316.1 million tons and the estimates should be considered bearish. The larger world ending stocks estimates reflect larger production estimates in Russia and Australia. Less production is likely in Europe and Argentina due to drought. About half of Argentine growing areas are affected as was much of France. The next crop is being planted now in the northern parts of the world. Conditions are improved in the US after some rains fell in the Great Plains. The Midwest has had god rains although some areas in the southern Midwest have not gotten much rain recently. It is also too dry for planting in parts of Ukraine and southern Russia. There is still plenty of time for rains to start planting in the latter two areas.

Corn

Corn was little changed last week. USDA released its latest production and supply and demand reports and the reports should have been a little negative for prices at least for the US data. US Corn production was estimated at 14.900 billion bushels, a little higher than the average trade guess. The yield was higher than the average guess at 178.3 bushels per acre. Ending stocks were also higher than expected at 2.503 billion bushels. World data showed lower ending stocks estimates at 3.6.9 million tons. USDA estimated world ending stocks at 317.5 million tons last month. USDA has found less damage to crops in Iowa and northern Illinois due to the drought and derecho winds that hit both areas a month ago. That allowed for the higher yield, production, and ending stocks estimates. The world data implies that US export demand should remain strong for the foreseeable future. The lower ending stocks come from less ending stocks for the US and for China. The US has less production and China has less production and increased demand.

Soybeans and Soybean Meal

Soybeans and the products closed higher for the week. Soybeans were a leader on Friday due to the USDA reports and potentially bullish weather. USDA estimated US Soybeans production at 4.313 billion bushels and ending stocks at 460 million bushels. The production estimate was above the average trade guess but the ending stocks estimate was on the average trade guess. USDA is suggesting that demand will be there for any supply. Much of the demand until now has been from China. The trade generally expects China to shift its buying back to Brazil in the near future, but USDA suggests that China could continue to buy here a little longer than expected. World ending stocks estimates were neutral when compared to trade expectations but were lower than last month. That is due mostly to the lower US production estimates. Soybeans went higher despite the neutral data on funds and other speculators buying.

Rice

Rice was lower as USDA released bearish production estimates. The All Rice production estimate was 218.112 million cwt, ups significantly from last month. Long Grain was also up significantly at 159.097 million cwt. Ending stocks were up as well at 45.9 million cwt for All Rice and up significantly at 32.8 million cwt for Long Grain. USDA noted lower ending stocks estimates for Medium Grain. The report implies that the US will have plenty of Rice for any demand in the coming year. Reports indicate that export and domestic demand has not been real strong to start out the new crop year. Exporters and domestic mills are thought to be holding back on purchases for as long as possible due to the current relatively high prices. The USDA reports suggest that both sources of demand will be rewarded for their patience.

Palm Oil and Vegetable Oils

Palm Oil closed lower for the first time in three weeks. Demand reports from the private surveyors were down and this is becoming a bigger problem for higher prices. Production ideas are turning seasonally higher as trees enter a peak production period over the next few months, but the market appears to have priced itself out of the demand base. Most importers seem to have enough stocks on hand and the Coronavirus pandemic is keeping overall demand on the lighter side. Soybean Oil was a little higher and Canola was higher. Canola closed higher on reports of freezing temperatures last week in the Canadian Prairies. The freeze extended into parts of the Dakotas and Minnesota as well. It is possible that a significant part of the Canola crop got hurt during the freeze event. Farmers there have withdrawn from the market and speculators are buying. The rally in US Soybeans futures was also supportive to Canola futures as was late week weakness in the Canadian Dollar.

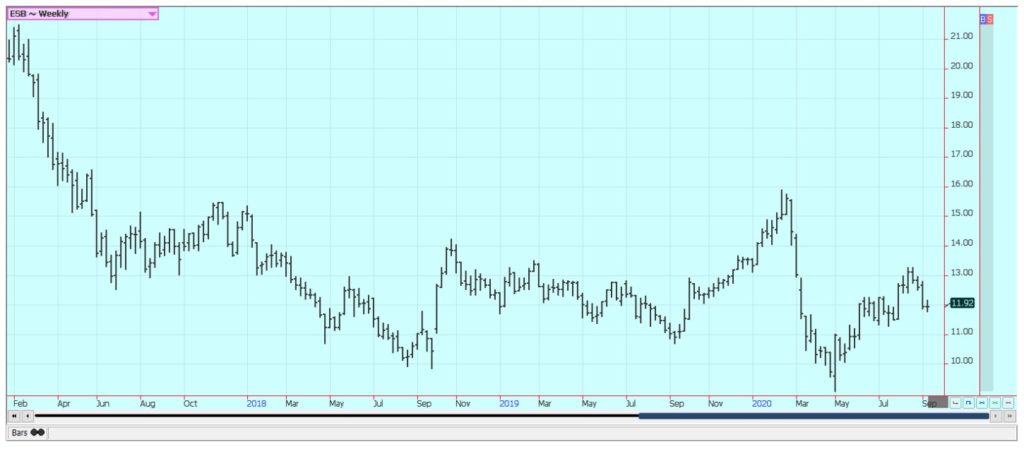

Cotton

Cotton closed a little lower for the week and trends are still sideways on the weekly charts. Demand has improved over the last couple of weeks but remains at depressed levels. The export sales report showed better sales to China but not that much beyond that. Demand should stay week as long as the Coronavirus is a feature of life around the world. Shopping is hard to do and many people are still unemployed. This is especially true for the US but it is true to some degree in just about all countries. US ending stocks were estimated at 7.2 million bales but came on the back of the lower production as export and domestic demand was trimmed. USDA estimated US Cotton production at just 127.06 million bales on Friday. Production was in line with trade expectations and below the 18 million produced last year. The supply losses are in the market now. However, the Harvest is still a ways down the road and the tropical season is active. There will be more chances to inflict more damage on the crops to help try to rally prices.

Frozen Concentrated Orange Juice and Citrus

FCOJ was lower. The daily and weekly charts show that trends are starting to turn down again. USDA left its Florida production estimate unchanged at 67.7 million boxes. This was about as expected by the trade. No hurricanes have hit Florida yet. The systems have all gone south into the Gulf of Mexico or north into the Carolinas. That usually means lower prices for futures but prices are already relatively cheap. The Coronavirus is still promoting consumption of FCOJ at home. Restaurant and food service demand has been much less as no one is really dining out. Florida production prospects for the new crop were hurt by an extended flowering period, but the weather is good now with frequent showers to promote good tree health and fruit formation. Import demand to the US should be minimal as US prices remain below those of Europe. Brazil has been too dry and irrigation is being used. Some showers are in the region now to help in Sao Paulo.

Coffee

Futures were lower last week in New York and in London. New York hit a wall of selling at the 135.00 area basis December futures. London has been the leader on the recent rally as demand for Robusta has improved with people staying at home. The demand from coffee shops and other food service operations is still at very low levels. Consumers are still drinking Coffee at home and the return of the Coronavirus outbreak will keep things that way. Reports indicate that consumers at home are consuming blends with more Robusta and less Arabica. Vietnam was dry during flowering time and is dry again. Production ideas are lower. The Brazil harvest is almost over but shipping has become difficult due to the widespread outbreak of the Coronavirus there. Even so, the ports are operating normally. Ideas are that production will be very strong this year as it is the on year for the trees. The strong production ideas are coming despite hot and dry weather seen in the country at flowering time.

Sugar

New York closed slightly lower and London was higher on speculative and fund related buying seen in London. Chart trends are down in both markets. UNICA noted less production of ethanol and Sugar from cane in its latest report and said that bad weather kept farmers out of the fields. Ethanol demand is down, anyway, so mills there are producing more Sugar in the mix. Ideas are that there is plenty of Sugar for the world market. India is thought to have a very big crop of Sugarcane this year but getting it into Sugar and into export position has become extremely difficult due to Coronavirus lockdowns. Thailand might have less this year due to reduced planted area and erratic rains during the monsoon season. There are reduced flows from rivers from China to hinder irrigation of the crops.

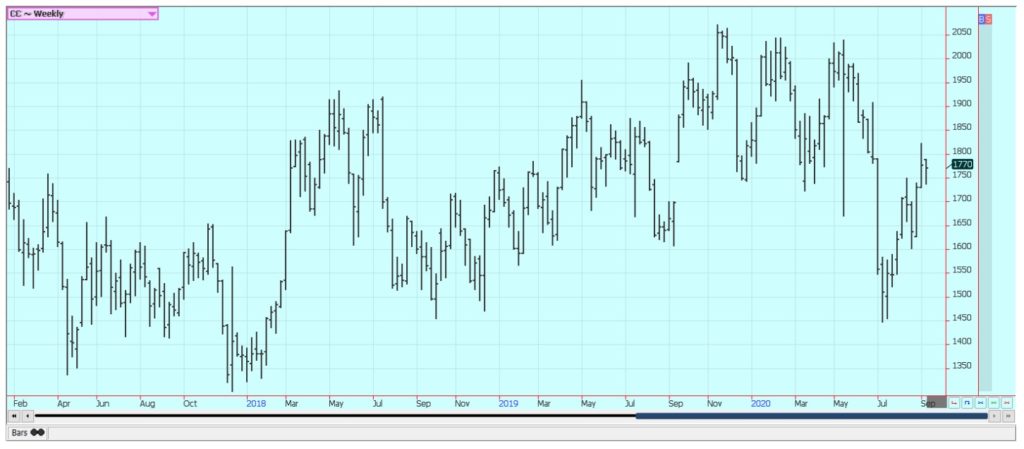

Cocoa

New York and London closed lower in correction trading. It was a rather narrow range week for both markets. The charts show that both markets are in sideways trends. The current crop features strong production but there are worries about the next crop. Nigerian traders told the wire services that the Nigerian rainfall has started and that crop conditions are much improved. There are a lot of demand worries as the Coronavirus is not going away and could be making a comeback in the US. Europe is still trying to open its markets again but the Coronavirus is still around and consumers are reluctant to buy. Ideas are that Southeast Asia also has good crops.

—

(Featured image by Trisha Downing via Unsplash)

DISCLAIMER: This article was written by a third party contributor and does not reflect the opinion of Born2Invest, its management, staff or its associates. Please review our disclaimer for more information.

This article may include forward-looking statements. These forward-looking statements generally are identified by the words “believe,” “project,” “estimate,” “become,” “plan,” “will,” and similar expressions. These forward-looking statements involve known and unknown risks as well as uncertainties, including those discussed in the following cautionary statements and elsewhere in this article and on this site. Although the Company may believe that its expectations are based on reasonable assumptions, the actual results that the Company may achieve may differ materially from any forward-looking statements, which reflect the opinions of the management of the Company only as of the date hereof. Additionally, please make sure to read these important disclosures.

ECSP Crowdfunding vs. eWpG Bonds: Overcoming SME Financing Limits

The ECSP Regulation limits annual crowdfunding per project promoter to €5 million, requiring a full prospectus for higher amounts, which delays...

Germany’s Cannabis Reform Shows Limited Risks but Calls for Regulatory Adjustments

Two years after Germany’s partial cannabis legalization, an evaluation finds no significant rise in consumption and some reduction in the...

Ortus Secures €97M Green Loan to Expand Solar Portfolio in Italy

Ortus Power Resources Italy secured a €97 million green, non-recourse loan to refinance 23 MW of operating solar plants and...

Foreign Exchange Markets Walk a Tightrope Amid Geopolitical Tensions and Policy Uncertainty

Foreign exchange markets remain fragile amid geopolitical tensions, monetary shifts, and persistent volatility. The dollar stayed a safe haven without...

Crypto Holds Steady as Tensions Rise and Regulatory Concerns Grow

Crypto markets remained cautious as a US ultimatum to Iran nears expiry. Bitcoin and Ethereum traded sideways despite strong ETF...

|

|

|  |

|

|

-

Business1 week ago

Business1 week agoMarkets Volatility, Geopolitics, and Signals of a Potential Trend Shift

-

Impact Investing7 days ago

Impact Investing7 days agoEU Taxonomy 2025: Progress in ESG Reporting, Gaps in True Sustainability

-

Africa2 weeks ago

Africa2 weeks agoBank Al-Maghrib Launches Reforms to Boost Credit via Non-Performing Loan Market

-

Fintech2 days ago

Fintech2 days agoToss Explores Blockchain Mainnet to Power Next-Generation Financial Services