Markets

Ideas of Weaker Cotton Demand Due to Economic Problems in Asia Continue

Cotton closed higher last week on ideas of smaller US crops that should be seen in the USDA data that will be released in a couple of weeks. The export sales report was not strong at all and caused some selling late in the week. Ideas are around that Chinese economic data implies less US cotton demand for the coming year but demand from other buyers has been good. The weak demand from China could continue.

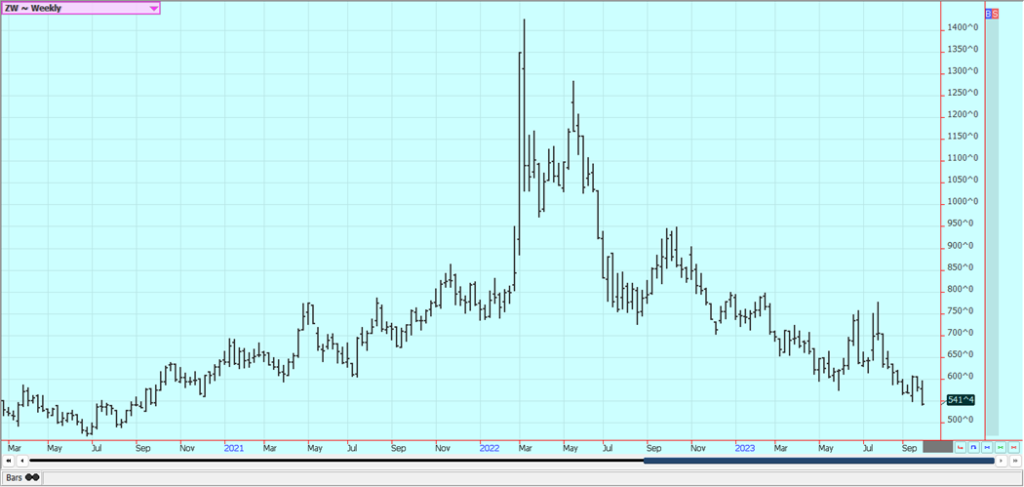

Wheat: Wheat markets closed lower and at a new low for the move last week in reaction to the USDA final production estimates and quarterly stocks report. Both reports were above trade expectations, with All Wheat production estimated at 1,812 billion bushels and stocks at 1.780 billion bushels.

There was a lot of business done to North African countries yesterday by Russia and EU countries, but nothing was reported to be done by the US. Russia is still exporting and offering Wheat into the world market at $270.00 per ton and is getting quite a bit of business. Ukraine and the EU countries are offering as well and are getting new business due to the higher Russian prices.

Demand has been poor for US Wheat as Russia’s production looks strong exports from Russia have not abated and Ukraine is still exporting, although mostly over land through the EU at higher costs.

Ukraine has lately shipped at least three loads of grain through the Black Sea after bombing a lot of Russian ships to allow for safe passage. Weather forecasts call for drier weather for Australia and Argentina, with production losses now expected for both countries.

Weekly Chicago Soft Red Winter Wheat Futures

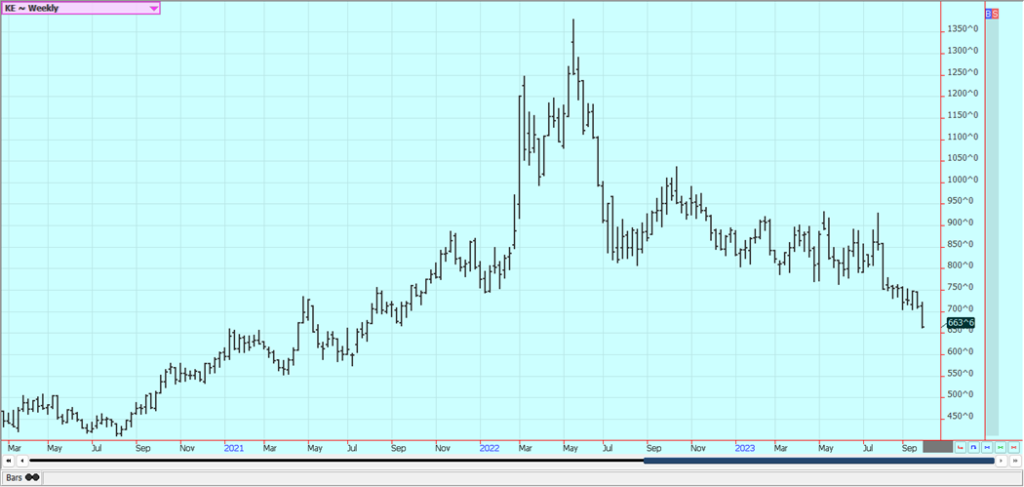

Weekly Chicago Hard Red Winter Wheat Futures

Weekly Minneapolis Hard Red Spring Wheat Futures

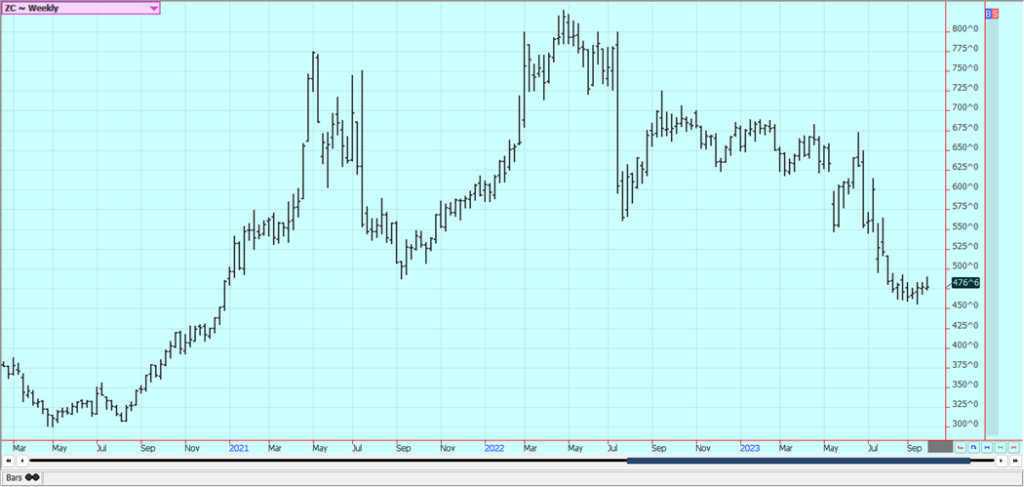

Corn: Corn and Oats were higher last week, with Corn just slightly higher after selling seen in response to the USDA stocks report. The report showed less-than-expected Corn stocks at 1.361 billion bushels, but futures were dragged lower anyway by higher-than-expected Soybeans and Wheat production and ending stocks.

The Corn harvest is underway with yield reports showing good and bad results with no real trend evident.

Farmers report no real sales of Corn as they wait for higher prices. Weather forecasts remain mostly dry but with moderate temperatures for the Midwest for the next week. The harvest is coming so moisture needs are less, and many producers report that Corn is shutting down early and that the harvest could start sooner than normal.

Demand for US Corn in the world market has been very low and domestic demand has been weak due to reduced Cattle and other livestock production. The Brazil Corn harvest is underway so export prices for Corn from Brazil are relatively cheap and Brazil is getting the business. That could change in the coming year is the growing conditions deteriorate in Brazil as is possible in an El Nino year.

Weekly Corn Futures

Weekly Oats Futures

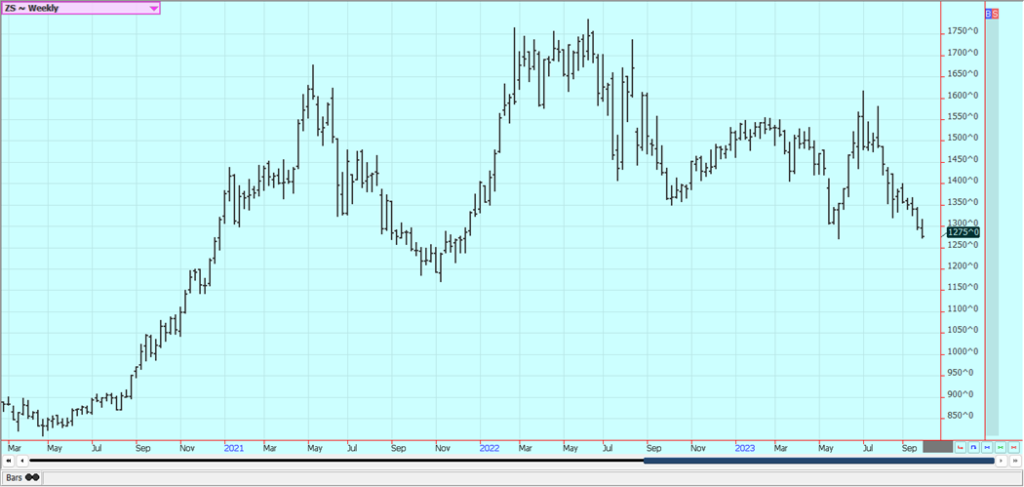

Soybeans and Soybean Meal: Soybeans and the products closed lower last week, with later week selling seen in response to the USDA stocks report. The report showed larger-than-expected ending stocks for the previous crop year at 268 million bushels and forced USDA to revise its 2022 production estimate to 4.270 billion bushels.

Those could be the last reports the market will see for a while as USDA is shutting down with the rest of the government today and will not be releasing any reports.

Initial yield results for the new crop show that production and yields are above and below APH data with no real trend showing just yet. The data has been called disappointing to traders as production appears to be less than expected so far this crop year.

Weather forecasts call for dry conditions and near to above-normal temperatures for the Midwest for the first half of the week, then dry and cool conditions. Ideas are that the top end of the yield potential is gone and severe damage is becoming possible in some areas.

Brazil’s basis levels are still low, and the US is being shut out of the market for most importers, but the US is price competitive now. Brazil is still selling a lot of Soybeans to China and other countries.

Weekly Chicago Soybeans Futures

Weekly Chicago Soybean Meal Futures

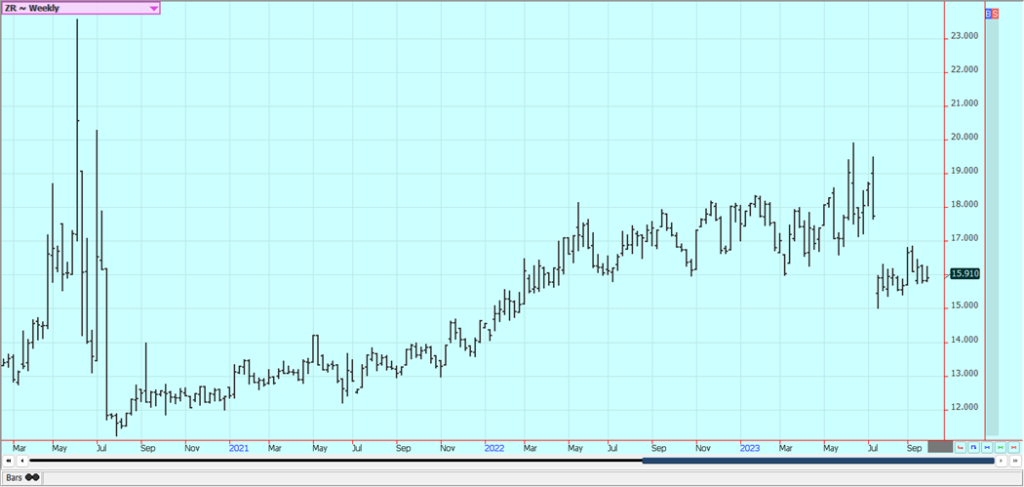

Rice: Rice closed a little higher last week but gave back most of the gains made in selling seen late in the week. The harvest is still active in Arkansas and Mississippi, but winding down in Texas and Louisiana. Ideas are that production will be less in this and coming reports. Yields are called average to below average in Texas and average so far in Arkansas as the harvest moves forward.

The quality has been uneven with some crops affected by the extreme heat seen during the growing season. India will not allow Rice exports except for Basmati for now because not enough rain in some production areas. Northern areas are too wet and southern areas are too dry.

Weekly Chicago Rice Futures

Palm Oil and Vegetable Oils: Palm Oil was higher last week on hopes for improved demand and smaller monthly ending stocks. Traders still think that El Nino will cause big production problems down the road and are holding out hopes for rallies in the future.

Canola was lower with Chicago price action and as the harvest has become more active. Drier weather is generally forecast for the Prairies and the crops have been stressed, but some rain is falling now to maintain crop conditions. Speculators were selling as the trends were turning down again.

Weekly Malaysian Palm Oil Futures

Weekly Chicago Soybean Oil Futures

Weekly Canola Futures:

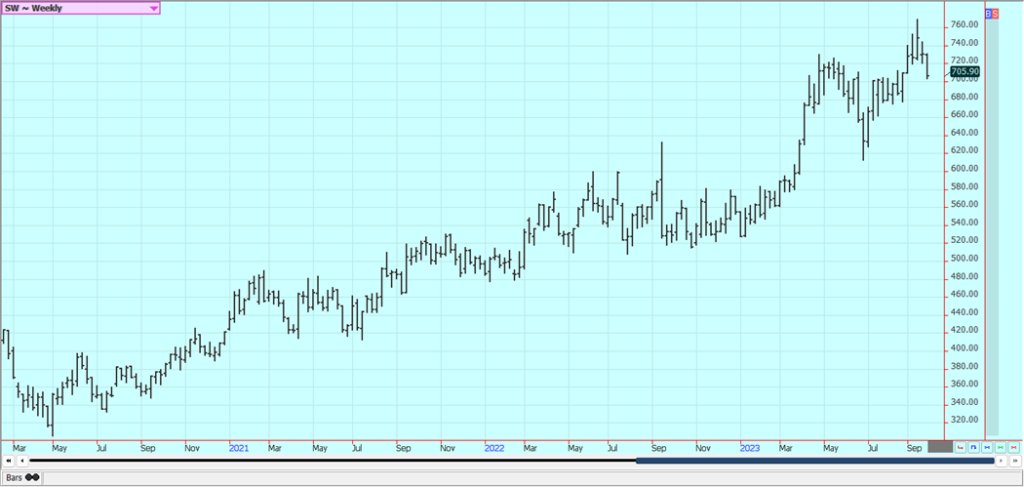

Cotton: Cotton closed higher last week on ideas of smaller US crops that should be seen in the USDA data that will be released in a couple of weeks. The export sales report was not really strong at all and caused some selling late in the week. Ideas are around that Chinese economic data implies less US cotton demand for the coming year but demand from other buyers has been good.

The weak demand from China could continue as China does not want to buy anything from the US for political reasons. Ideas of weaker demand due to economic problems in Asia continue and Chinese economic data continues to show weakness.

There are still many concerns about demand from China and the rest of Asia due to the slow economic return of China in the world market. However, there are also production concerns about Australian and Indian Cotton as both countries are likely to suffer the effects of El Nino starting this Fall.

Weekly US Cotton Futures

Frozen Concentrated Orange Juice and Citrus: FCOJ closed higher last week but could not hold the best gains of the week or the breakout higher that was completed early in the week. It was a disappointing week of price action for those looking for the market to keep marching higher in terms of price.

The market has been dynamic as traders are wary about selling futures due to the hurricane season that could bring a storm to damage crops in Florida again.

Futures have stalled out in the last week as the hurricanes are missing Florida and are instead landing farther north up the coast. Reports of short supplies in Florida and Brazil are around. Futures are also being supported by forecasts for an above-average hurricane season that could bring a storm to damage the trees once again.

Historically low estimates of production due in part to the hurricanes and in part to the greening disease that has hurt production, but conditions are significantly better now with scattered showers and moderate temperatures. Florida Citrus Mutual said that inventories of FCOJ are now 44.5% less than last year.

Weekly FCOJ Futures

Coffee: New York and London closed lower last week as the higher US Dollar has improved the offers from Brazil and Vietnam. Demand for Robusta and lower quality Arabicas has improved due to the recent price strength in Robusta, but the Vietnam harvest is now underway and growers there are reported to be excited to sell into higher prices seen currently.

The lack of offers from Asia, mostly from Vietnam but also Indonesia remains a main feature of the market, but the offers are starting to improve with the Vietnam harvest underway and the US Dollar moving higher.

Offers from Brazil and other countries in Latin America should be increasing but prices are considered a little cheap to create much selling interest from producers and the differentials offered have been very high. The Brazil harvest moving quickly and this fact has pressured prices. It is hot and dry in Brazil right now.

Weekly New York Arabica Coffee Futures

Weekly London Robusta Coffee Futures

Sugar: New York and London closed lower last week. There are still forecasts for rain in Brazil after a spell of very hot and dry conditions, but the market continues to see stressful conditions in Asian production areas. The Brail rains could still be a few weeks off but the rainy season should be under way soon.

Chart trends are turning down with the price action so far this week. The Asian dryness is still the main feature. Many growing areas in India have been dry, and exports have indicated that production has suffered.

The government there now says it will have more than enough production for the domestic demand but will limit exports to help control inflation. There are also worries about the Thai and Indian production potential due to El Nino. Offers from Brazil are still active but other origins are still not offering, and demand is still strong. Brazil reports very good harvest conditions but the weather in Southeast Asia is currently dry.

Indian production is less this year and Pakistan also has reduced production and the monsoon has been uneven so far in both countries. Thailand production is also down a lot this year and many Asian countries are worried about El Nino impacting future production. European beet producers are reported to be less interested in planting this year due to environmental regulations imposed by the EU.

Weekly New York World Raw Sugar Futures

Weekly London White Sugar Futures

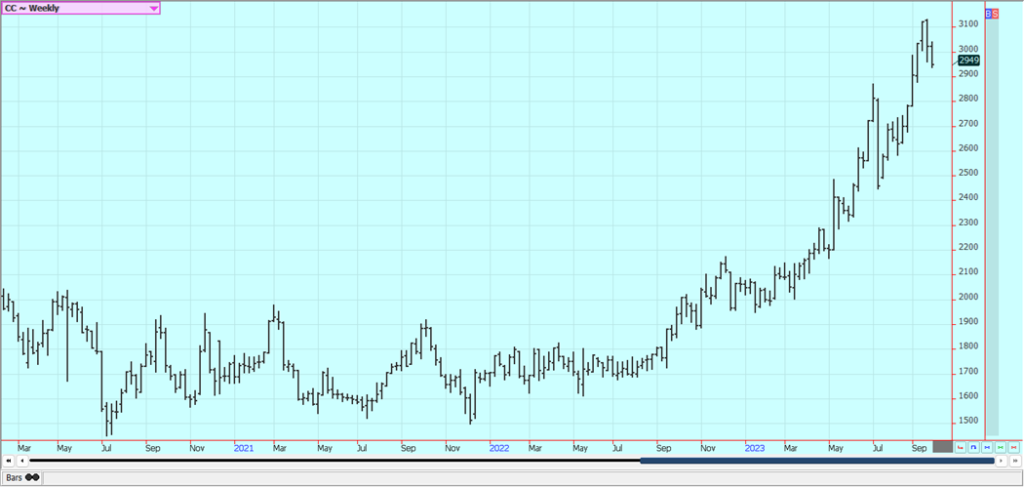

Cocoa: New York and London closed lower last week as the main crop harvest comes into focus. Futures seem to be high enough in price for now and some speculators are taking money off the table. The charts suggest that a correction is underway and it is possible that futures and cash prices have gotten a little too high for the demand side of the market despite production losses seen during the growing season.

The supply and demand situation remains bullish. Reports of diseases in West Africa that are hurting production continue. The diseases are from too much rain falling earlier in the growing season. Ideas of tight supplies remain based on more reports of reduced arrivals in Ivory Coast and Ghana continue.

Midcrop production ideas are lower now with diseases reported in the trees due to too much rain that could also affect the main crop production. Ivory Coast exports are down 10% so far this marketing year at 1.305 million tons. The Cocoa grind in Ivory Coast is up 9% in August.

Weekly New York Cocoa Futures

Weekly London Cocoa Futures

__

(Featured image by Karl Wiggers via Unsplash)

DISCLAIMER: This article was written by a third party contributor and does not reflect the opinion of Born2Invest, its management, staff or its associates. Please review our disclaimer for more information.

This article may include forward-looking statements. These forward-looking statements generally are identified by the words “believe,” “project,” “estimate,” “become,” “plan,” “will,” and similar expressions. These forward-looking statements involve known and unknown risks as well as uncertainties, including those discussed in the following cautionary statements and elsewhere in this article and on this site. Although the Company may believe that its expectations are based on reasonable assumptions, the actual results that the Company may achieve may differ materially from any forward-looking statements, which reflect the opinions of the management of the Company only as of the date hereof. Additionally, please make sure to read these important disclosures.

Futures and options trading involves substantial risk of loss and may not be suitable for everyone. The valuation of futures and options may fluctuate and as a result, clients may lose more than their original investment. In no event should the content of this website be construed as an express or implied promise, guarantee, or implication by or from The PRICE Futures Group, Inc. that you will profit or that losses can or will be limited whatsoever. Past performance is not indicative of future results. Information provided on this report is intended solely for informative purpose and is obtained from sources believed to be reliable. No guarantee of any kind is implied or possible where projections of future conditions are attempted. The leverage created by trading on margin can work against you as well as for you, and losses can exceed your entire investment. Before opening an account and trading, you should seek advice from your advisors as appropriate to ensure that you understand the risks and can withstand the losses.

Morocco’s Budget Execution June 2026: Deficit Narrows to 20.2 MMDH

Morocco’s Finance Law execution at end-June 2026 shows a reduced budget deficit of 20.2 billion dirhams, down from 24.9 billion...

Tilray Brands Hits Multi-Year Lows as Cannabis Investors Await Regulatory Clarity

Tilray Brands shares have fallen 57% this year amid cannabis sector weakness and uncertainty over US regulatory reform. While potential...

Ethereum Between ETF Inflows, Price Risks and a Strong July

Ethereum faces mixed signals as ETF inflows and a strong July performance support recovery, while technical resistance and downside risks...

Mercedes-Benz Accelerates EV Decarbonization With Recycled Aluminum

Mercedes-Benz expands its partnership with Hydro to accelerate supply chain decarbonization. Future electric vehicles will use Hydro CIRCAL aluminum containing...

Evotec and BioGaia Boost Biotech, while Vitrolife Disappoints

European stocks moved on earnings and broker actions. Evotec, BioGaia, Plus500, Pharming, Inwido, Amundi and Julius Baer rallied on upgrades,...

|

|

|  |

|

|

-

Cannabis4 days ago

Cannabis4 days agoGermany’s Cannabis Clubs Enter New Phase as Legal Harvests Begin

-

Cannabis2 weeks ago

Cannabis2 weeks agoAli G Makes Surprise Wimbledon Appearance with Cannabis-Themed Satire

-

Impact Investing6 days ago

Impact Investing6 days agoBiodiversity Becomes a Key Driver of Value and Resilience in Real Estate

-

Markets2 weeks ago

Markets2 weeks agoOil Surge, Weak Stocks, and a Potential Turn for Gold