Business

Farming weekly: News and reports

Farming weekly: What is new in the U.S. agriculture market? Report with detailed analysis and commentary.

Farming weekly: What is new in the U.S. agriculture market? Report with detailed analysis and commentary.

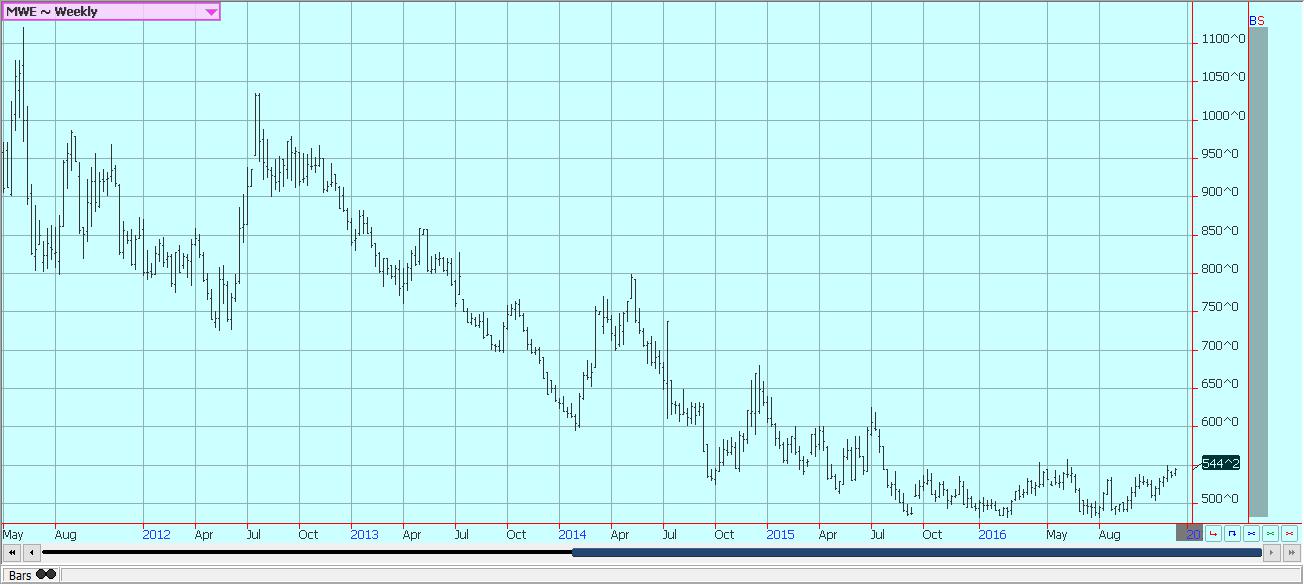

Wheat

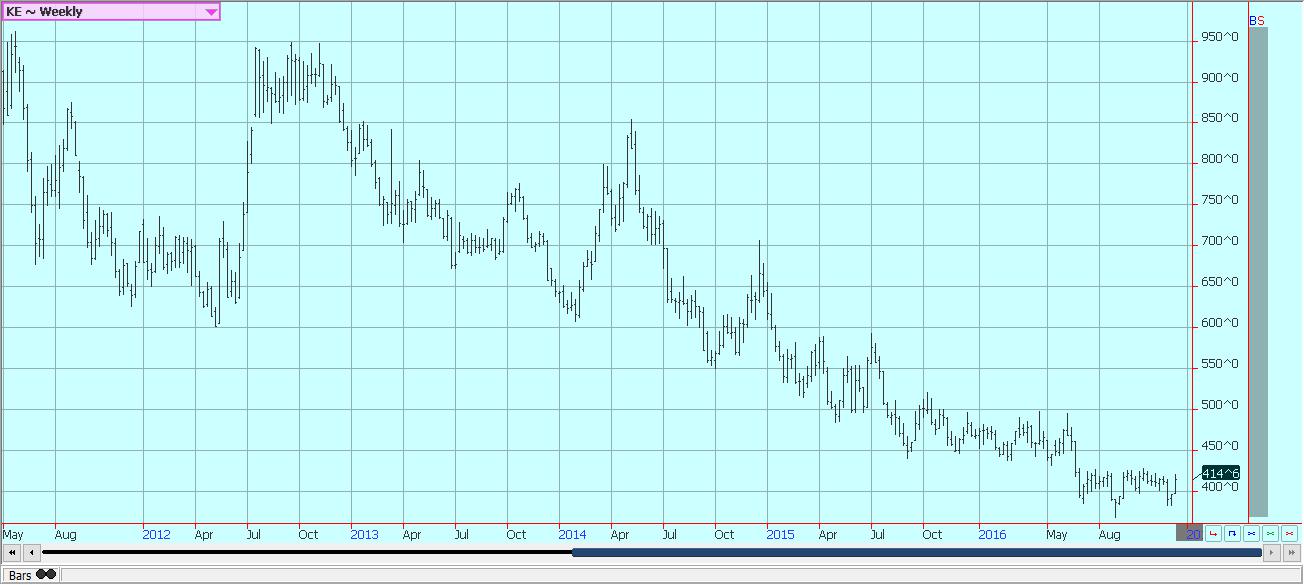

US markets moved a little higher last week despite continued strength in the US Dollar and in anticipation of a major cold outbreak for US Winter Wheat areas that occurred over the weekend. It got well below 0F over the weekend in many growing areas, and significant parts of the crop were at risk. Areas of southern Nebraska and western Kansas had little or no snow cover and were considered most at risk for loss. The crops in these areas had been poorly established due to the dry weather, and now are facing the cold. Crops in the Midwest were at risk as well, although most areas have at least some snow cover. It will be difficult to quantify any actual crop losses until the Wheat emerges from dormancy this Spring.

However, it is hard to think that at least some losses were inflicted on crop potential over the weekend. Western Kansas is the most important production area for HRW in the US, so the losses might become significant. Crop loss estimates will be seen this week once the temperatures start to moderate. USDA export sales last week were solid, especially considering the strength in the US Dollar since the US presidential elections and then the FED news of interest rate increases last month. The charts show that futures have staged a strong recovery in prices over the last couple of weeks and appear poised to head higher into the next year. Chicago shows some strong resistance starting at 420 March, but also shows the chance to move above a short term down trend line.

Weekly Chicago Wheat Futures © Jack Scoville

Weekly Kansas City Wheat Futures © Jack Scoville

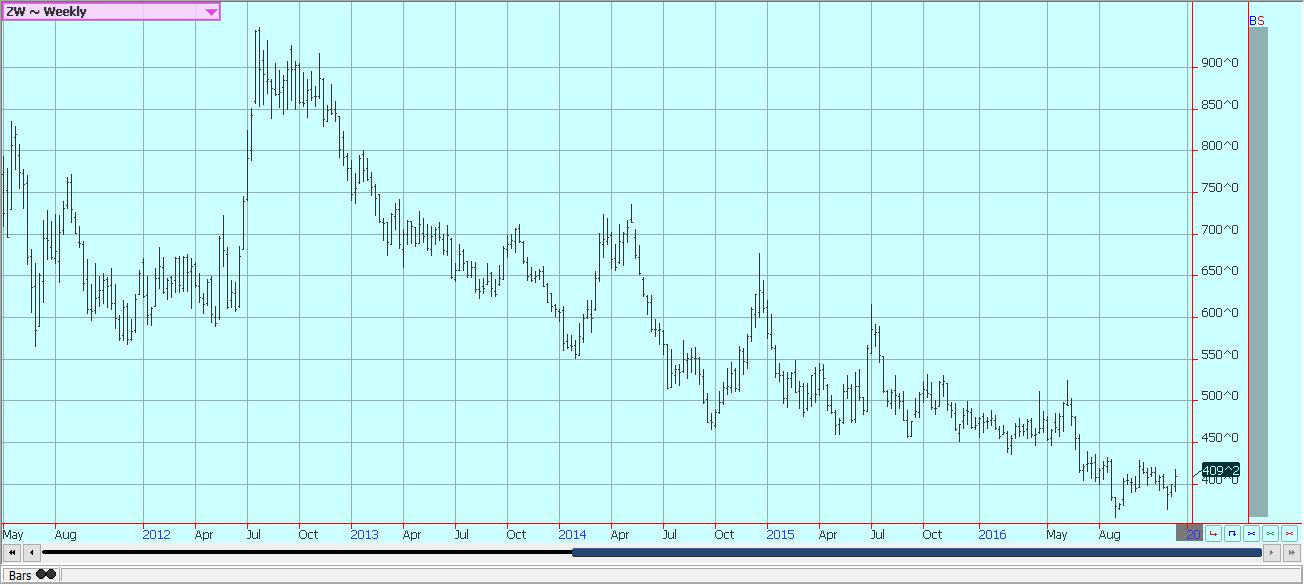

Weekly Minneapolis Wheat Futures

Corn

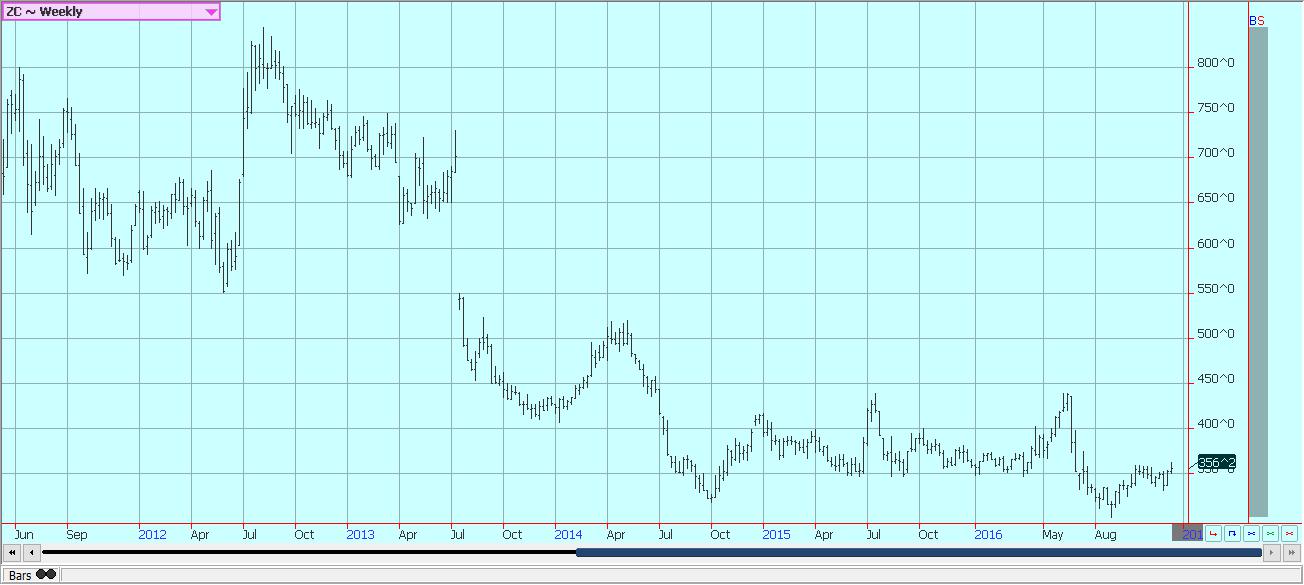

Corn closed near unchanged on Friday and higher for the week. The weekly charts still show that futures are in position to move higher. In fact, the market did move above resistance at about 360, but faded late in the week. There is enough demand to justify stronger prices. US farmers are still not selling Corn and have been selling Soybeans instead. Corn prices remain at unprofitable levels for them. They have the farm storage to be able to hold the Corn. The weekly export sales reports remain strong, and the domestic demand is stronger.

Corn for Ethanol demand remains very strong and above year ago levels. Margins for ethanol producers remain very strong, so continued strong Corn demand is expected from this sector. South America will remain quiet for the first part of next year. Prices in Brazil remain very high as traders oversold Corn into the cash and export market. The market remains tight and prices remain elevated. It will take some time for the market to replenish supplies and for prices to fall. It could be well into the coming Summer before South America starts to offer in a big way. Meanwhile, ideas are that the big Corn supplies held by US farmers will remain a problem on rallies. The Corn wijll have to move sooner or later, and history shows that rally attempts should not be real strong until the large farm holding of Corn is reduced and the crop gets used.

Weekly Corn Futures © Jack Scoville

Weekly Oats Futures © Jack Scoville

Soybeans and Soybean Meal

Soybeans and Soybean Meal were little changed last week. Demand for US Soybeans remained strong, but the market attention was more on the strength of the US Dollar and on crop conditions in South America. Ideas are that demand for US Soybeans can fade soon. However, farmers in the US have already sold about two thirds of the crop, according to some analysts, and farmers in South America are not really selling. The lack of offer in cash markets should help support the market. Farmers in South America remember last year and the drought that hit in the last part of the crop development cycle and are waiting to make sure they have good production before doing much contracting.

They are waiting despite favorable prices being offered in many domestic cash markets. Many are also concerned about the economics of South America, and in particular currency trends for the Real and the Peso. Most fear that these currencies will continue to fall and prefer to hold back on sales due to this reason alone. Meanwhile, the Brazil crop is mostly planted as of now. Conditions are reported to be mostly good in central and northern Brazil, but now it is turning a little too dry in northern Brazil. Argentina has also been dry. Rains are expected from south to north in Argentina and southern Brazil over the next couple of weeks to alleviate dryness concerns. Expectations for big crops in both countries are widespread, with some estimates ranging up to 106 million tons of Soybeans produced in Brazil this year. Last year, Brazil produced under 100 million tons.

Weekly Chicago Soybeans Futures © Jack Scoville

Weekly Chicago Soybean Meal Futures © Jack Scoville

Rice

World markets were mostly stable to higher last week. US futures markets moved lower and are now at some support areas. Speculators remain the primary sellers in Chicago and appear ready to try to force the market to test the lows made about a month ago at 912.5 basis the nearest futures contract. The US market has turned very quiet for the holiday period, and most farming operations are now shut down for the holidays. Most producers will not look at the market until early next year now. There is not much reason for them to consider prices at this time as cash market bids remain well below the cost of production for most sellers.

Domestic mills appear to have enough Rice in hand to meet projected demand into next year. Export sales last week were solid once again, but featured a sale of 25,000 tons of medium grain to Japan. Actual long grain demand was not real strong. The US is facing a big cut in planted area next year unless prices improve this Winter. Planting mix decisions will start being made next month, and most are now expecting a drop of 15% to 25% in planted area due to price. It just is not profitable to grow Rice in the US at current prices. Rice producers do have significant support from the farm programs, but even these are not enough to overcome the loss potential. We expect quiet markets the next couple of weeks, then a chance to try to rally prices again in January to encourage some farm selling.

Weekly Chicago Rice Futures © Jack Scoville

Palm Oil and Vegetable Oils

It was a higher week for world vegetable oils markets. Palm Oil found support from the monthly MPOB data that showed less than expected production and lower than expected ending stocks for the month. The trees there have been slow to recover from the El Nino droughts of last year. Price spreads for Palm Oil against Soybean Oil or other major vegetable oils remain historically tight due to the lack of supply. Meanwhile, there is a relative abundance of Soybean Oil, and US export sales of vegetable oils in general have been rather strong as the US is able to step in and fill a lot of the demand gap.

Demand for bio fuels remains very strong. The weekly demand data from DOE of the US government showed that demand remains elevated. Meanwhile, growing conditions in Southeast Asia are good for Palm Oil as showers are being reported in many production areas. South American growing conditions are expected to improve this week in Argentina and southern Brazil as some showers are in the forecast. Drier weather is expected farther to the north, but these areas have had good precipitation lately. Production should be good for vegetable oils as we move into the new year. Demand should hold strong as the demand for bio fuels and human consumption should hold together. The OPEC move to cut crude oil deliveries into the world market should support additional bio fuels production amid good prices.

Weekly Malaysian Palm Oil Futures © Jack Scoville

Weekly Chicago Soybean Oil Futures © Jack Scoville

Weekly Canola Futures © Jack Scoville

Cotton

Futures were a little higher last week as the holiday period gets underway. The US harvest is all but over now and offers into the cash market will be decreasing. The weekly charts show that the market held support and that the longer term uptrend remains intact. USDA weekly export sales were down on a week to week basis, but were still very strong at over 300,000 bales. The demand for US Cotton has held despite the strong US Dollar. Demand has come from diverse sources, with Vietnam, China, and Turkey all active buyers in last week’s report. This should be good news for the market and producers.

The situation in India remains difficult as the market has yet to open much due to the changes in monetization of the country. The government has changed bills and appears to be forcing more electronic transactions to open the economy and increase transparency. Trade in most agricultural markets has ground to a halt for a while and is now slowly starting to get better. The US has been able to sell more Cotton into the world market this year due to these developments, and even Pakistan has become a good buyer as they look to replace purchases normally made from India. Meanwhile, the holidays are here and trade could be limited in futures marklets for the next cuple of weeks.

Weekly US Cotton Futures © Jack Scoville

Frozen Concentrated Orange Juice and Citrus

FCOJ closed a little lower on Friday nd sharply lower for the week as an initial stream of polar air that moved into central parts of the US did not extend to Florida. The market is looking at stable production estimates and the potential for increased competition from Brazil. USDA left production estimates for Florida Oranges unchanged in its monthly reports. There are no frosts or freezes in the forecast for Florida, but it has turned cooler. Less Florida production and also less production in Brazil are the main market support factors. Brazil also suffers from the greening disease. The Florida harvest is moving forward, but harvest progress has been slow and progress is called behind normal. Irrigation has been used in Florida and is being used frequently at this time due to dry conditions. Fruit is moving to packing houses for the fresh trade. Increasing amounts are now moving to processors as the early and mid harvest expands. In Brazil, Sao Paulo state is getting good weather and crop conditions are called good.

Weekly FCOJ Futures © Jack Scoville

Coffee

Prices were as little higher last week in both New York and London. The offer side of the market is quiet. Differentials paid in Central America appear stable at weak levels. Little selling is being reported, but offers are available as the harvest starts to increase. There was some very unseasonal rains in Central America over the last couple of weeks that interrupted harvest and could have damaged the cherries. However, there have not been any reports of big damage seen by us until now. Differentials are also stable in Colombia. Brazilian producers have become quiet as the fear further weakness in the Real against the US Dollar. Coffee becomes a bank account when these fears get big enough. Roasters have become more withdrawn in the marketplace due to the recent surge in prices, and now due to the price weakness. They will probably start to buy again if a more stable price outlook appears. They are waiting for now and might not get real active until after the holiday season. The market in New York is trying to become more stable at this time, and London appears ready to work higher again.

Weekly New York Arabica Coffee Futures © Jack Scoville

Weekly London Robusta Coffee Futures © Jack Scoville

Sugar

Futures closed sharply lower and broke some important support areas on the charts. Technical analysts said Sugar futures entered bear market territory last week. It is possible that futures eventually move down to test more support at 1600 and 1500 in New York. Price action overall remains negative on worries about overall demand potential and on bigger than expected exports from Brazil. Demand news remains bearish for futures prices. China has imported significantly less Sugar in the last couple of months as it starts to liquidate massive supplies in government storage by selling them into the local cash market.

The government is currently offering another 300,000 tons into the domestic market. The Brazilian Real has moved sharply lower in the past couple of weeks and kept mills in a selling mode. There could be smaller crops coming from India and Thailand due to uneven monsoon rainfall in Sugar areas in both countries. India has said that its production and amounts in storage are sufficient and that there is no need for imports that had been expected earlier. The Sugar Association said Friday that the monetization program of the government has hurt domestic demand and that this will further prevent any imports. The weather in other Latin American countries appears to be mostly good as rains remain sufficient. Most of Southeast Asia has had good rains.

Weekly New York World Raw Sugar Futures © Jack Scoville

Weekly London White Sugar Futures © Jack Scoville

Cocoa

Futures markets were higher in recovery trading. Trends remain down in both New York and London, but prices have moved sharply lower in the last few weeks and some short traders might decide to book profits for the end of the year. Overall price action remains weak as the main crop harvest continues in West Africa under good weather conditions. Speculators are mostly done liquidating and some commercial buying has been noted. Reports indicate that consumptive demand is increasing at these lower price levels.

The demand from Europe is reported improved based on some corporate data released in the last few weeks. However, the Euro remains weak and new demand could be hurt. The next production cycle still appears to be bigger as the growing conditions around the world are generally improved. West Africa has seen much better rains this year and alternating warm and dry weather with the rains. There have been some reports of disease to crops in the wetter areas, but so far there is not a lot of market concern. Bigger production is expected this year in all countries. East Africa is getting enough rain now, and overall production conditions are now called good. Good conditions are still being reported in Southeast Asia.

Weekly New York Cocoa Futures © Jack Scoville

Weekly London Cocoa Futures © Jack Scoville

Dairy and Meat

Dairy markets were firm as good supply met very good demand. Butter and cheese manufacturers report strong demand, but expect demand to fall off now as the holiday season is here. Butter manufacturers are shifting from producing print butter to producing bulk butter. Most have good supplies on hand, but inventory has been moving. Even so, inventories are increasing. Cream demand has been strong in the domestic and world market, with Mexico and Canada showing buying interest. Cheese demand is being met with adequate to strong milk supplies and manufacturing is active. Fresh cheese markets are in balance at this time, but aged cheese inventories are said to be high.

Raw milk production has also been stronger, with only the Pacific Northwest reporting less production due to weather stress. Dried products prices are mixed to firm. Whey prices are strong, and whole milk prices are firm. NDM prices are mixed to firm. International markets are featuring higher prices due to reduced production. Production is less in Europe and Russia. Production is down in Australia, but has increased lately in New Zealand due to the uptick in prices. South American prices are firm as raw milk production goes into a seasonal decline.

US cattle and beef prices were higher last week in reaction to reports of higher beef prices and despite lower prices paid in cattle markets. Cash cattle markets traded at lower prices at the end of last week and in moderate volumes. However, prices paid in the cash markets were still above futures. The charts show that market could move higher. Demand is starting to improve overall as the wholesale market anticipates better demand in the new year. Australia has less to offer and very high prices. Herd culling has slackened in both Australia and New Zealand. Pasture conditions in both countries is better than a year ago on colder and wetter weather seen until now.

Pork markets have been firm, and live hog futures trends are higher. Pork demand has been stronger than expected and a primary ham consumption period is here with the holidays. Pork prices have trended higher in retail and wholesale markets. There has been a lot of featuring in supermarkets in the US. Pork demand should remain strong for the next couple of weeks as hams and other cuts will be featured for holiday buying. US export demand should start to improve on the lower prices. Packer demand has been improving as many packers expected reduced supplies of Hogs late in the Winter or in the Spring. The charts show that the market could remain higher.

Weekly Chicago Class 3 Milk Futures © Jack Scoville

Weekly Chicago Cheese Futures

Weekly Chicago Butter Futures © Jack Scoville

Weekly Chicago Live Cattle Futures © Jack Scoville

Weekly Feeder Cattle Futures © Jack Scoville

Weekly Chicago Lean Hog Futures © Jack Scoville

—

DISCLAIMER: This article expresses my own ideas and opinions. Any information I have shared are from sources that I believe to be reliable and accurate. I did not receive any financial compensation in writing this post, nor do I own any shares in any company I’ve mentioned. I encourage any reader to do their own diligent research first before making any investment decisions.

PayPal’s Slowdown: From Fintech Leader to Low-Growth Dividend Stock

PayPal has shifted from fintech leader to low-growth, value-style stock, losing over 25% in market value and trading at a...

Tilray (TLRY) Falls as Bearish Momentum Persists Despite Marketing Push

Tilray (TLRY) fell 3.32% to $4.44, remaining below key moving averages and signaling continued bearish pressure. Despite a £1 million...

ESG Gap Persists as Firms Struggle to Link Sustainability to Financial Value

KPMG’s Global Survey shows a major gap between ESG awareness and financial integration. While 72% of managers understand sustainability strategies,...

Bitcoin and Ethereum Slide as Market Pressure Builds Amid Strategy Concerns and Layer 2 Disruptions

Bitcoin fell below $60,000 with heavy ETF outflows, pressured by concerns over Strategy’s finances and its STRC stock decline. Ethereum...

AI Venture Builder Launches €600K Crowdfunding Round to Scale Secure AI Solutions

AI Venture Builder, an Italian-British firm developing AI applications and vertical startups, returns to CrowdFundMe with a equity campaign. After...

|

|

|  |

|

|

-

Crypto1 week ago

Crypto1 week agoCrypto Market Stays Stable as Bitcoin and Ethereum See Mild Declines

-

Crowdfunding2 weeks ago

Crowdfunding2 weeks agoSustainable Restoration of the Haus Hövener Garden in Brilon

-

Fintech3 days ago

Fintech3 days agoMollie Expands Across EEA With €350M Investment to Strengthen European Payments Network

-

Cannabis1 week ago

Cannabis1 week agoEurope’s Cannabis Shift: Rising Use, and New Risks

You must be logged in to post a comment Login