Business

Indonesia and Brazil are low on coffee supplies

The Robusta market is relatively strong compared to Arabica.

Latest news in the agriculture market: The New York coffee market is important to watch as futures are trying to break down trends that have been in place on the daily charts since last November.

Wheat

US markets were higher as inclement weather and poor growing conditions continued in the US and in some areas around the world. Minneapolis could not hold early week gains and finished lower for the week on reports of increased producer selling interest in the US and Canada. Futures gapped higher to start the week but spent the last part of the week moving a little lower and traders tried to fill the gap at the end of the week.

Trends are up on the weekly charts in all three markets. The harvest is complete in Texas and Oklahoma, and reports continue to be mixed. Results indicate that the protein levels are not strong in these areas. Yields are lower as well. The Kansas crop harvest is very active. Yield reports were mixed, but protein levels were considered generally satisfactory.

It is dry in the Dakotas and Montana and the southern Prairies, while other parts of the northern Prairies have seen too much rain. winter wheat production is expected to be slightly higher than last month, but spring Wheat production estimates are expected to be sharply lower. All wheat production estimates are expected to be less due to the Spring Wheat losses. The Midwest has seen plenty of rain, and yields, in general, should be strong. Russia is cutting back production expectations a bit and there are questions about Ukraine and Europe wheat production. Australia has been hot and dry and production estimates are falling. Some now suggest that the crop there could be less than 20 million tons. World production will be less than previous expectations. The weekly charts show the potential for Wheat prices to move significantly higher.

Weekly Chicago Soft Red Winter Wheat Futures © Jack Scoville

Weekly Chicago Hard Red Winter Wheat Futures © Jack Scoville

Weekly Minneapolis Hard Red Spring Wheat Futures © Jack Scoville

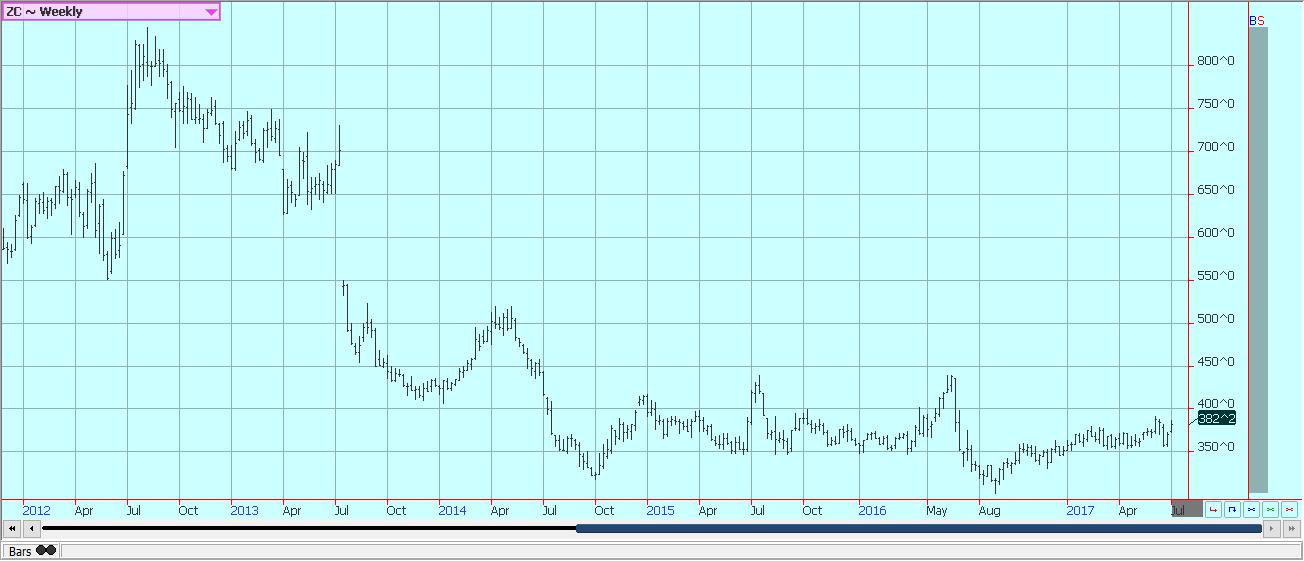

Corn

Corn was higher and oats were lower last week. Weather problems and difficult growing conditions continue to support both markets. Trends are up on the daily and weekly charts for corn, and the weekly charts imply that rallies to 403 and 430 basis the nearby contract are possible.

Crop progress remains generally good but is uneven due to the spread out planting seen at the start of the year. Pollination is starting on some fields, but other areas might not move to pollination until the end of the month. Ideas are already that the top edge of yield potential is gone, although the potential for very good production is still very much there. But, the weather must stay good and so far the weather has been variable at best. Variable and potentially stressful conditions are expected to return with hotter temperatures in western areas.

Weekly Corn Futures © Jack Scoville

Weekly Oats Futures © Jack Scoville

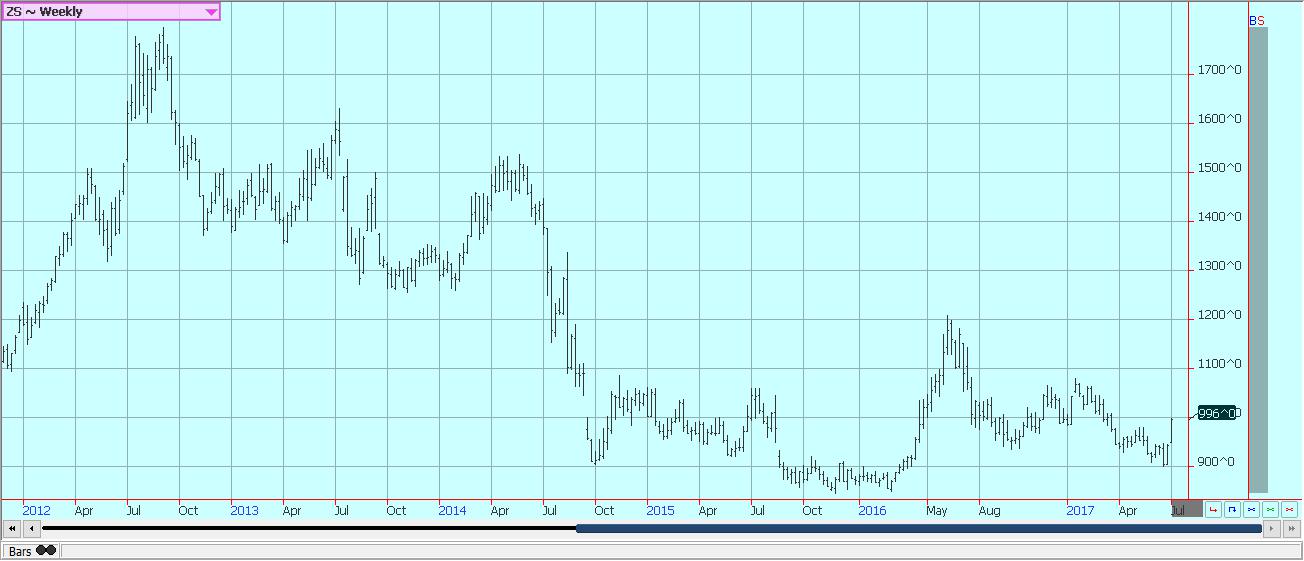

Soybeans and soybean meal

Soybeans and soybean meal were higher last week as hot and dry weather is forecast to move into western production areas from the Great Plains. Parts of Iowa and Minnesota had already been dry and topsoil moisture levels are low, so the hot and dry forecast is coming at a bad time for these areas.

The weather has been very warm to promote growth, but soybeans in many areas remain short and some crops are not canopied yet. Crop ratings are not as high as expected but could show some deterioration in the data that will be released on Monday afternoon. However, USDA might not reflect the more difficult conditions in its supply and demand estimates on Wednesday as it will most likely combine the new planted and harvested area estimates with trend line yields. Demand for US soybeans remains strong, with solid export sales on a weekly basis that run above trade and USDA expectations. The export sales report last week was relatively weak as prices have moved higher now.

Weekly Chicago Soybeans Futures © Jack Scoville

Weekly Chicago Soybean Meal Futures © Jack Scoville

Rice

Rice closed higher last week and closed at the weekly highs after holding support areas on the charts. The price action suggests that futures prices can continue to move higher. The potential for smaller US crops this year continues to support the move higher. The weather in most growing areas should improve this week on forecasts for warmer and drier conditions in the Delta and Gulf coastal areas. Many parts of the Delta and along the Gulf Coast remain too wet and this weather has affected production potential.

There are ideas that USDA has overestimated planted area in Arkansas. Texas is in good to very good condition. California has good looking crops, but the crops were planted late so top yields are not likely. Crops are in flood in the south and going into the flood in the north. The crop condition improved on a week to week basis but remains slightly behind the conditions of last year.

Weekly Chicago Rice Futures © Jack Scoville

Palm oil and vegetable oils

World vegetable oils markets were mostly higher last week, but soybean oil struggled due to domestic demand developments. EPA announced its proposed annual biofuels mandates, and the mandate for soybean oil based bio fuels was reduced due to what it called domestic market reality. The move by EPA implies that demand can drop for soybean oil in the coming year. Ethanol mandates remained high. The weekly charts for the various vegetable oils markets remain the weakest of all agricultural futures markets.

Weekly Malaysian Palm Oil Futures © Jack Scoville

Weekly Chicago Soybean Oil Futures © Jack Scoville

Weekly Canola Futures © Jack Scoville

Cotton

Cotton was lower and made new lows for the move on the weekly charts. Trends remain down on the charts. It is possible now that the market is in an extended trend lower that could last at least through the rest of the year. However, the current growing conditions are less than favorable in some areas. The growing weather in half of the US is generally good and crop conditions are reported to be good by producers and observers. These areas include parts of Texas, the Delta, and the Southeast.

Warmer temperatures have arrived to support the development and there has been enough rain. Texas and the desert Southwest and into California has seen extreme heat and mostly dry weather and dryland crops are suffering. The US and maybe the world will produce much bigger crops this year, with US crops bigger due as much to increased planted area as yield potential. On the other hand, China has been too dry. Central Asia has been dry, but conditions are rated as good. Overall, the market expects more production in the world against stagnant demand.

Weekly US Cotton Futures © Jack Scoville

Frozen concentrated orange juice and citrus

FCOJ closed lower last week but remains in a trading range on both the daily and weekly charts. Selling has abated with the Valencia harvest coming to a close. It is hurricane season, and an above average year is expected in the Atlantic. A system is currently in the Atlantic but is expected to remain a tropical depression as it moves west. It would not be a threat to crops if it comes onshore, but the exact course is not certain. The Pacific has also been active. Florida weather has shown improvement as rains continue in the state.

The demand side remains weak and there are plenty of supplies in the US. Brazil has been exporting FCOJ to the US to cover the short Florida crop. Domestic production remains very low due to the greening disease and drought. Trees now are showing the fruit of varying sizes and overall conditions are called good because of the irrigation and the recent rains. Brazil crops remain in mostly good condition.

Weekly FCOJ Futures © Jack Scoville

Coffee

It was a higher week in New York as that market tried to form what could be an important low. The New York market action is important to watch as futures are trying to break down trends that have been in place on the daily charts since last November. The cash market remains very slow with almost no interest seen from roasters as they see the big US supplies and think that prices will remain cheap. Offers are less and seen at high prices from Robusta countries such as Vietnam. Indonesia and Brazil are also very low on supplies. The Robusta market is still relatively strong compared to Arabica and due to the short supplies available to the market as it works to curb demand through the higher prices.

Weekly New York Arabica Coffee Futures © Jack Scoville

Weekly London Robusta Coffee Futures © Jack Scoville

Sugar

Futures in both London and New York were higher last week, and both markets now appear ready for a more two-sided trade for the coming weeks. Frequent reports of increased supplies to the market that has pressured prices in the last few weeks, but this could now be part of the price. Production conditions have been better this year in Brazil, and a better harvest is anticipated in the next couple of months as the Sugarcane harvest moves to its peak. UNICA showed a big increase in processing of cane

Production in India and Thailand is expected to improve in the coming year as both countries anticipate better monsoons than the failed monsoons of last year. It is raining in parts of India now as the monsoon arrived a few weeks ago, and most Sugarcane areas appear to be getting good rains. India is now ready to increase import tariffs due to the outlook for increased local production. The Indian weather service estimates that the monsoon will be within the normal range. Thailand also hopes for an improved monsoon season this year and is getting rains now.

Weekly New York World Raw Sugar Futures © Jack Scoville

Weekly London White Sugar Futures © Jack Scoville

Cocoa

Futures markets were lower last week and both markets are showing the potential for prices to work lower in the next few weeks. The overall market situation remains generally bearish, although fundamentals could change in the longer term. Harvest activities in West Africa are completed. Ivory Coast said last week that it had already sold more that 1.0 million tons of the next crop. That means that there is less offer in the cash market as much of this cocoa has already been sold. The demand from Europe is reported weak overall, and the North American demand has been weaker. However, chocolate prices are falling in Germany and should be falling in other parts of the world now to help move product and to get the market flowing again as input costs are much lower now.

Weekly New York Cocoa Futures © Jack Scoville

Weekly London Cocoa Futures © Jack Scoville

Dairy and meat

Dairy markets were higher last week, and longer term trends remain up. However, price action in all three markets was weak at the end. Butter prices have been the strength of the market on reports of very good demand for the next six months and tightening supplies due to hotter weather. Cheese prices have been relatively weak.

US cattle and beef prices were lower and trends in cattle futures remain down. The beef market has been much weaker in the last couple of weeks and has been racing live cattle prices lower. Feedlots are very current with supplies and are pulling cattle ahead in order to take advantage of the high prices. However, ideas are that more supplies are coming as weight per carcass is higher and more cattle is coming to the market.

Pork demand remains stronger than expected, but packers have been pulling back from the market as they sense increasing supplies are coming. Demand also starts to work lower as most of the Summer buying is done. There are big supplies out there for any demand. The charts show that the market could work lower.

Weekly Chicago Class 3 Milk Futures © Jack Scoville

Weekly Feeder Cattle Futures © Jack Scoville

Weekly Chicago Lean Hog Futures © Jack Scoville

Weekly Chicago Cheese Futures © Jack Scoville

Weekly Chicago Butter Futures © Jack Scoville

Weekly Chicago Live Cattle Futures © Jack Scoville

—

DISCLAIMER: This article expresses my own ideas and opinions. Any information I have shared are from sources that I believe to be reliable and accurate. I did not receive any financial compensation in writing this post, nor do I own any shares in any company I’ve mentioned. I encourage any reader to do their own diligent research first before making any investment decisions.

TopRanked.io Weekly Affiliate Digest: What’s Hot in Affiliate Marketing [Bovada Affiliate Program]

This week, we're mashing up 80s tech with 2020s private messaging apps. Why? Because Big Tech just dropped a big...

Euro Stablecoins Struggle to Compete with Dollar Dominance in Crypto Markets

Euro stablecoins remain marginal despite the euro’s global importance, with minimal trading volume compared to dollar rivals like USDT and...

Gilead Sciences Advances Growth Strategy with Focus on HIV, Oncology, and Innovation

Gilead Sciences focuses on developing treatments for HIV, cancer, and inflammatory diseases, driven by blockbuster drugs like Biktarvy. Growth relies...

Casablanca Stock Exchange Profits Surge in 2025 as Growth Momentum Strengthens

In 2025, Casablanca Stock Exchange profits rose 40% to MAD 50.9 billion. Net income grew 22.3%, driven by strong industrial...

Credibur Scales Rapidly: €2 Billion in Structured Debt Facilities in Six Months

Infrastructure fintech Credibur has added over two billion euros in structured debt facilities within six months. Its platform connects lenders,...

|

|

|  |

|

|

-

Impact Investing6 days ago

Impact Investing6 days agoItalian Unlisted Banks Lag on ESG Sustainability

-

Crypto2 weeks ago

Crypto2 weeks agoThe Iran War Tests Bitcoin and Crypto Market Resilience

-

Crypto3 days ago

Crypto3 days agoEuro Stablecoins Struggle to Compete with Dollar Dominance in Crypto Markets

-

Crypto2 weeks ago

Crypto2 weeks agoCrypto Markets Volatile as Bitcoin Hovers, Solana Eyes AI Integration

You must be logged in to post a comment Login