Business

Palm oil moves higher on improved demand ideas

Weekly charts closed strongly for palm oil and vegetable oils as stock and demand rise due to a trade shift in the US-China dispute.

Wheat

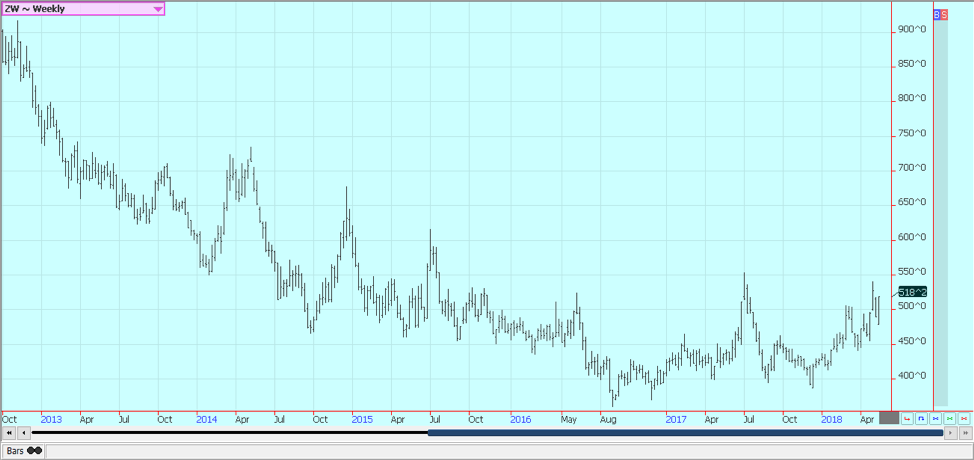

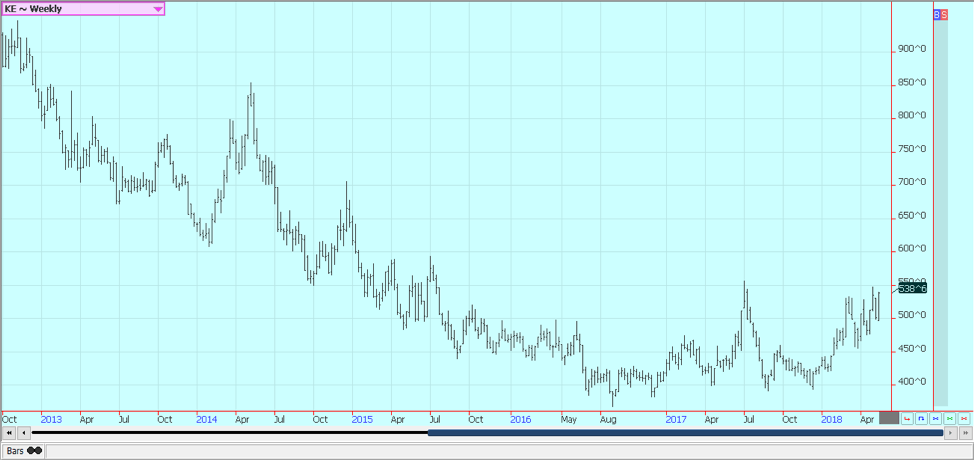

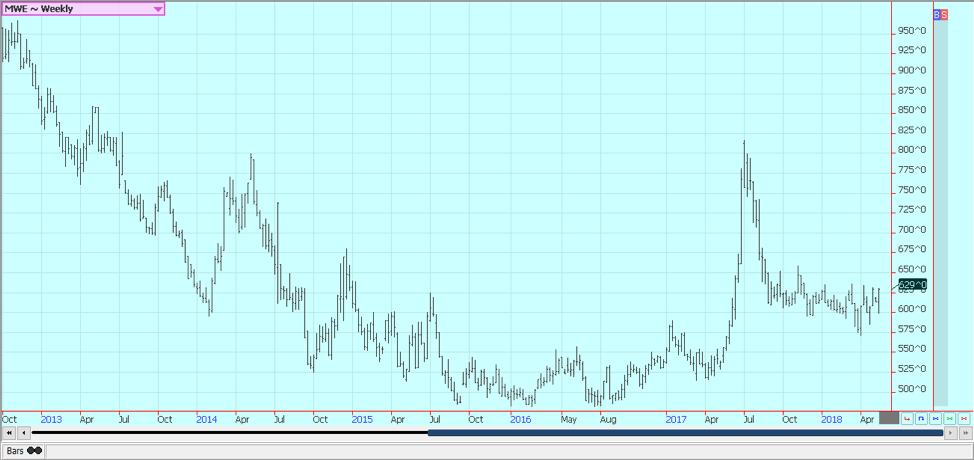

Wheat markets were higher on uncertain production prospects at home and increasingly in other producing countries. The dry conditions in the western Great Plains, although Oklahoma saw a big jump in condition ratings last week due to some rains. Kansas also saw better ratings due to rains, but Texas did not get rain and conditions remained very poor. New crop ratings will be released tonight. Spring wheat planting has been slow, especially in South Dakota, and final planting dates for insurance purposes are coming at or before the end of the month.

There are now reports of dry weather in Canada, and hot and dry weather in the Indian Subcontinent and north into Kazakhstan and then east into parts of China. Australia is also reported to be dry. Some very beneficial rains fell in the Black Sea growing areas, but mostly in Ukraine as Russian areas remain dry. Black Sea prices remain the cheapest but have been trending higher lately.

There had been talks of the potential for significant yield losses if rains did not appear in the short term. Demand remains the big problem for wheat traders, and the weekly export sales report once again showed weak demand. The competition from eastern Europe and the Black Sea area remains very tough, and US prices are currently above the competition.

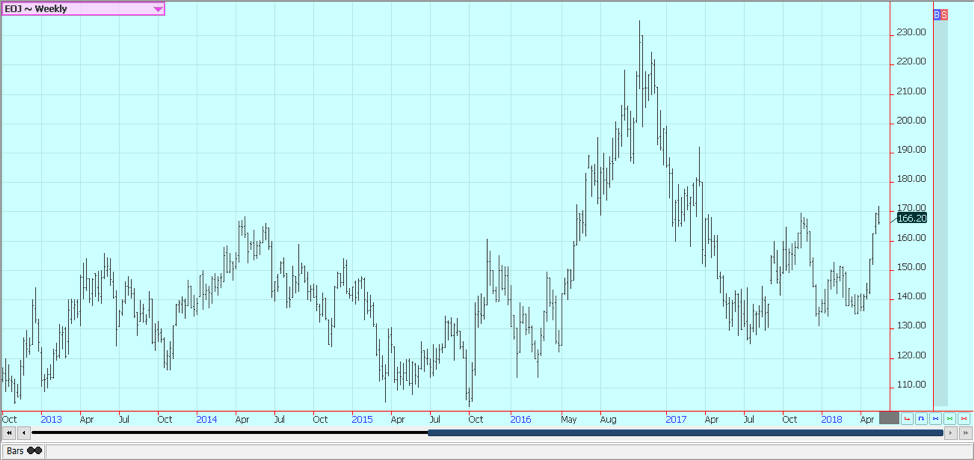

Weekly Chicago Soft Red Winter Wheat Futures © Jack Scoville

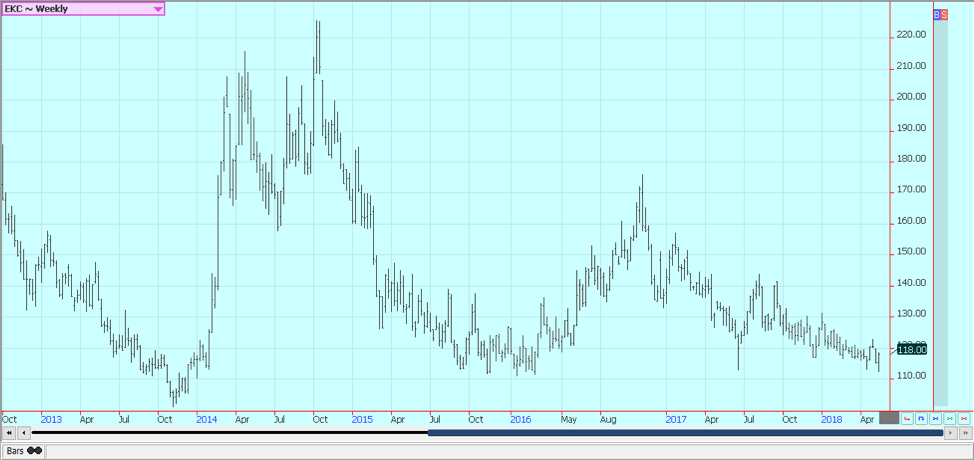

Weekly Chicago Hard Red Winter Wheat Futures © Jack Scoville

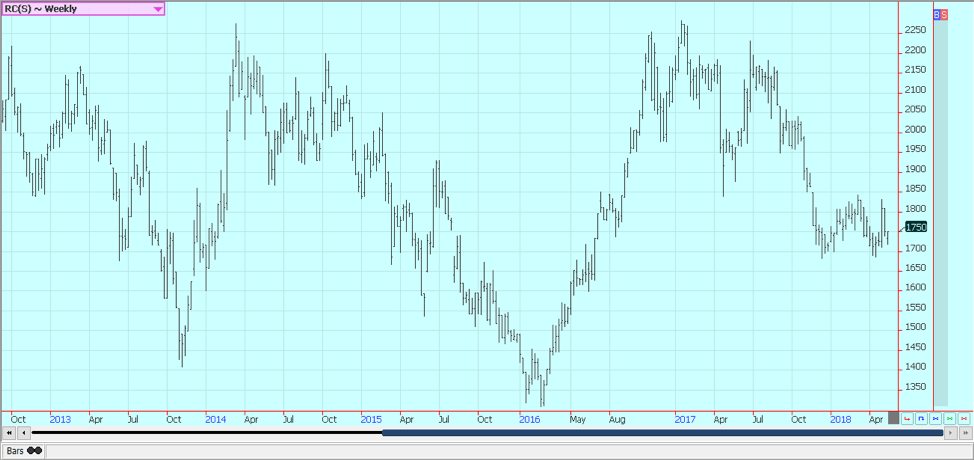

Weekly Minneapolis Hard Red Spring Wheat Futures © Jack Scoville

Corn

Corn closed higher on demand ideas and worries that some of the areas in the northwestern part of the Corn Belt might not get planted. Producers in most areas have been active and have been able to get most or all of the corn planted on intended area. This is not true, however, for parts of Wisconsin, Minnesota, and the Dakotas, where planting remains very far behind.

Quit dates for insurance purposes com in some cases by the end of this week and in others at the end of the month, so it is getting to crunch time for producers to get corn planted. The export sales report last week was strong and showed that demand for US corn remains intact. There is not a lot of corn available from other world sellers right now, and US corn is enjoying a significant price advantage over the competition.

Strong sales should remain a feature for a couple more months and maybe longer, depending on the production of the winter corn crop in Brazil. The Safrinha crop is in trouble in parts of Parana and Mato Grosso at a key time in its development cycle. It is pollination and kernel fill time, but the weather has already turned hot and dry. It could be that the rainy season has ended early. If so, yield potential will shrink dramatically as the development of the crop will be sharply reduced.

Weekly Corn Futures © Jack Scoville

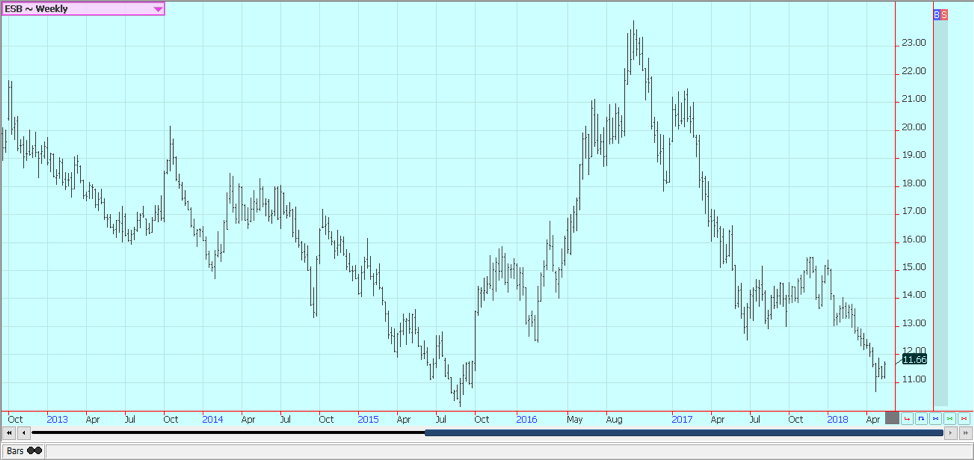

Weekly Oats Futures © Jack Scoville

Soybeans and soybean meal

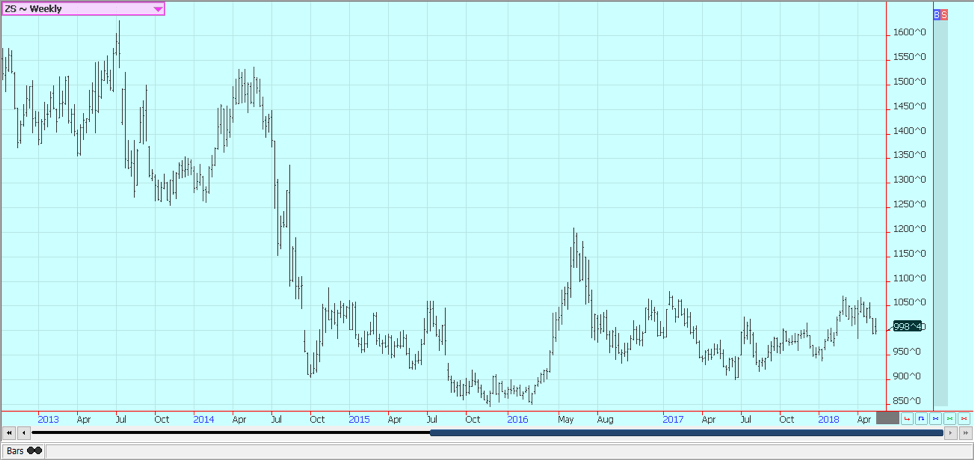

Soybeans were slightly higher and the products were lower last week. The US and China have continued talks to try to resolve the trade dispute. An agreement was found on some issues in the first round of meetings, but there are still a lot of issues that need to be resolved, and the differences are said to be big on some of these. Demand is still an issue with traders as the tariff threats with China remain alive, but there are still hopes that the issues with China can be resolved before any punitive tariffs are enacted.

There are very high-level meetings scheduled between the two sides this week. The trade also hopes for a peaceful solution to the NAFTA talks to keep Mexican and Canadian demand alive. China still prefers Brazilian soybeans due to the tariff threats and as the new crop Brazil harvest is now available, and the US stands to lose demand in coming weeks from that buyer and maybe others as Brazil expands market share. Farmers in much of the southern Midwest are planting soybeans. Planting of corn and soybeans will increase in the north this week.

Weekly Chicago Soybeans Futures © Jack Scoville

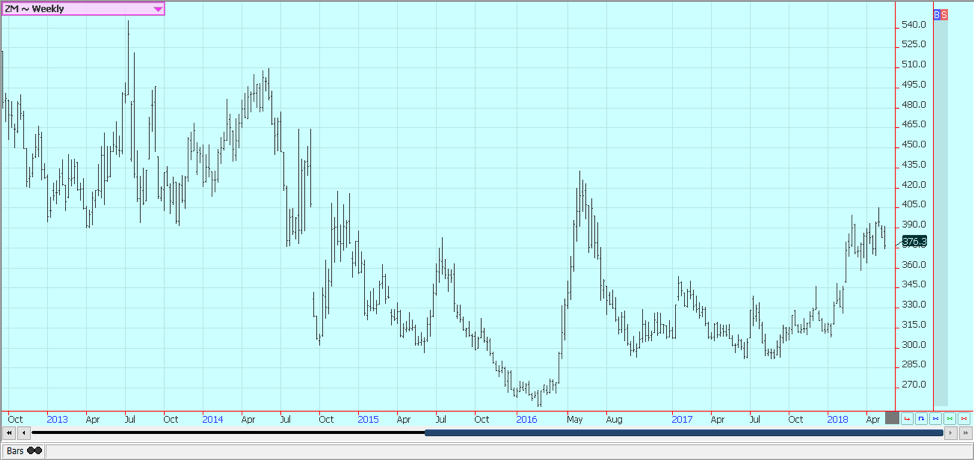

Weekly Chicago Soybean Meal Futures © Jack Scoville

Rice

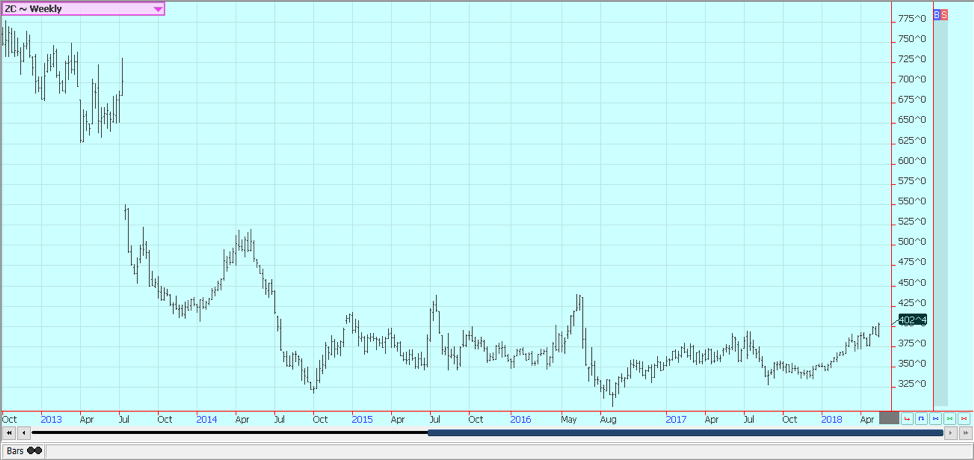

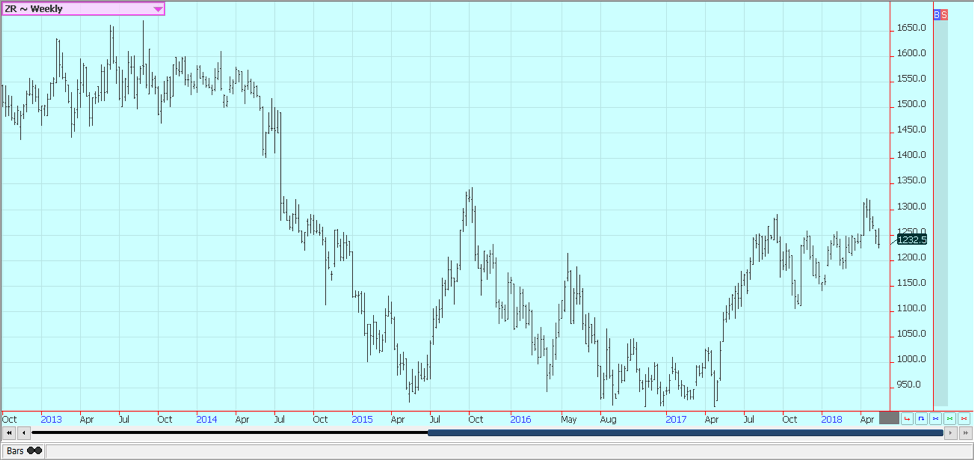

Rice was lower for the week and made new lows for the move on ideas that demand is waning and the crop is starting to progress. Ideas are that domestic demand is now about covered and that export demand could be less with the NAFTA problems with Mexico and on weakening export sales report in recent weeks from USDA. Sources in Arkansas say that planting has been active on warmer weather and that crops are finally starting to emerge. Some producers switched to soybeans for some of the areas due to price and the bad weather.

Planting is also about done along the Gulf Coast. It remains very dry in Texas and producers are having to flush crops more than normal. There are worries that are starting to be heard about yield potential for the state. Ideas are that little old crop rice is available in the cash market, and the situation is not likely to improve before the new crop becomes available late this Summer as farmers are mostly sold out. Farmers have planted more rice this year, but the increase in planted area is not considered burdensome.

Weekly Chicago Rice Futures © Jack Scoville

Palm oil and vegetable oils

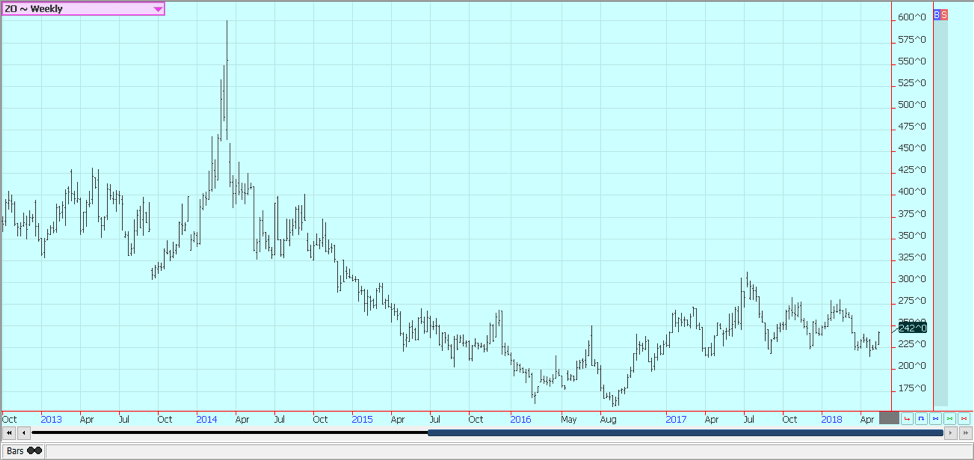

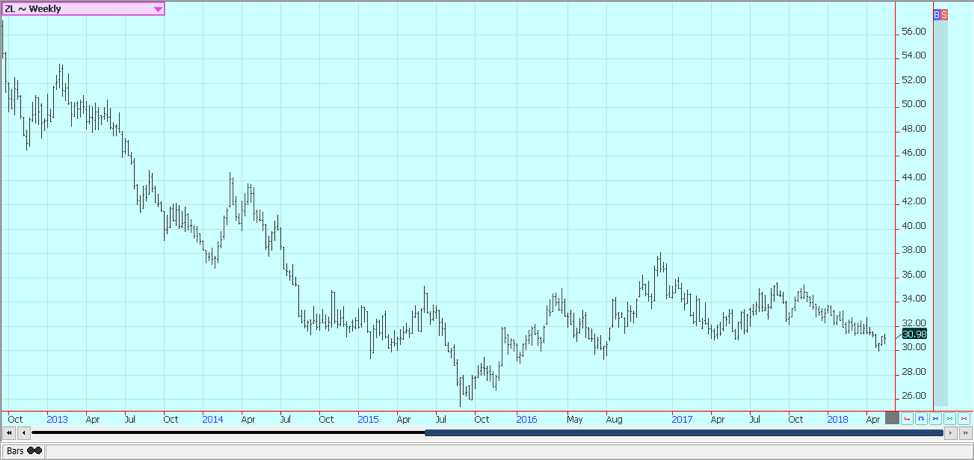

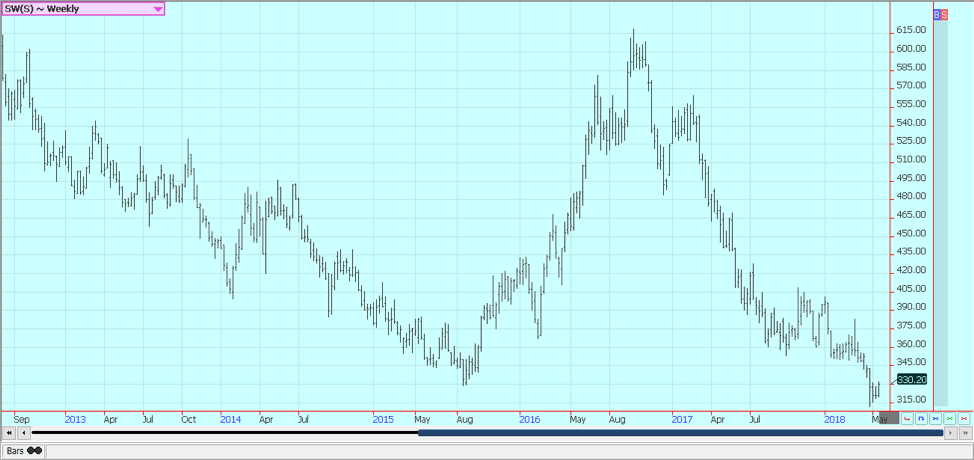

World vegetable oils prices were a little higher again last week. Palm oil moved higher as the market hopes for increased demand. The US-China trade dispute could shift some of the demand to palm oil, especially since the soybeans and soybean meal market has been under pressure in China. China has been importing mostly from Indonesia and India is out of the market for now. China has been crushing a lot of soybeans and has been producing its own soybean oil.

A weaker currency has also supported improved demand ideas. The weekly charts show that palm oil trends have turned down again as the weaker demand is being met by reports of better production. A downtrend can continue. Soybean oil was locked in a sideways trend all week but managed to close higher. Canola found some support from the trade war. Farmers were active planting, although some parts of the Prairies have turned very dry. Offers from farmers were down last week as they plant and wait for higher prices.

Weekly Malaysian Palm Oil Futures © Jack Scoville

Weekly Chicago Soybean Oil Futures © Jack Scoville

Weekly Canola Futures © Jack Scoville

Cotton

Cotton was higher for the week and once again tested previous highs on the weekly charts near 8800. Further weakness now could mean that the market has made an important top. It is still a weather market due to the poor weather in Texas and on there are still ideas of tight available supplies. It has also been hot and dry in India and Pakistan and also in China.

There are ideas that the US is now running short of high-quality cotton to deliver to the exchange and to overseas buyers. Demand remains strong in export markets as the weekly export sales report showed strong volumes again last week. Chart trends are mixed on daily charts and on weekly charts. New crop planting has been slow, but not unusually slow when compared to last year and the five-year average.

The weather in the western Great Plains is still mostly dry. Forecasts call for mostly dry weather for the next couple of weeks, and producers in the western Great Plains are likely to wait for better rains before planting more cotton. Planting conditions have improved in Oklahoma and Kansas due to recent precipitation. Farmers in the Delta and Southeast have seen too much rain and have had delays as soils dry out. The overall planting pace is likely to remain slow.

Weekly US Cotton Futures © Jack Scoville

Frozen concentrated orange juice and citrus

FCOJ was lower. FCOJ is in a weather market as dry conditions are reported in production areas of Brazil. However, some drought busting rains have been reported in Florida in the past week, and the situation in the state should be much improved as the rainy season appears to be underway. These rains have been big and could be interrupting the last of the harvest in the state.

The market is still dealing with a short crop against weak demand. Florida producers are seeing marble sized to golf ball sized fruit. Conditions are reported as generally good. Irrigation is being used, but less now after the rains. Brazil also could use more rain as Sao Paulo has been hot and dry. Generally good conditions are reported in Europe and northern Africa.

Weekly Frozen Concentrated Orange Juice Futures © Jack Scoville

Coffee

Futures in New York were higher for the week on strong commercial buying that started to fade late in the week in anticipation of the Brazil harvest that is about to get started. However, speculators were not willing sellers, and origin selling was quiet in the futures markets. London was little changed. Ideas are that at least 55 million bags of coffee will be harvested. CONAB said the total could be about 68 million bags, and a consensus of trade guesses puts production at about 59 million bags.

The weather is dry in Arabica areas, but there have been some showers in Conillon areas. Origin is still offering in Central America and is still finding weak differentials. Good business is getting done and exports are active. Traders anticipate big crops from Brazil and from Vietnam this year and have remained short in the market.

Robusta remains the stronger market as Vietnamese producers and merchants are not willing to sell at current prices and are willing to wait for a rally. Vietnamese cash prices were weaker last week with good supplies noted in the domestic market. The weather there is good for the next production as there are now rains.

Weekly New York Arabica Coffee Futures © Jack Scoville

Weekly London Robusta Coffee Futures © Jack Scoville

Sugar

Futures were higher in both markets for the week. Both markets are trying to form bottoms on the daily and weekly charts. Ideas of big world supplies against average at best world demand keeps the overall tone of the market weak, but the market acts sold out and in need of new sellers. The Brazil season is off to a big start, causing the selling interest as the market now expects even more sugar to be available.

There has been little in the way of positive news for traders in the last year as production estimates have climbed and demand estimates have not. The fundamentals remain little changed, and there does not seem to be much, for now, that can shake the market out of its current trend. Ideas that sugar supplies available to the market can increase in the short term have been key to any selling. India is back to export sugar this year after being a net importer for the last couple of years. Thailand has produced a record crop and is selling. Brazil still has plenty of sugar to sell.

Weekly New York World Raw Sugar Futures © Jack Scoville

Weekly London White Sugar Futures © Jack Scoville

Cocoa

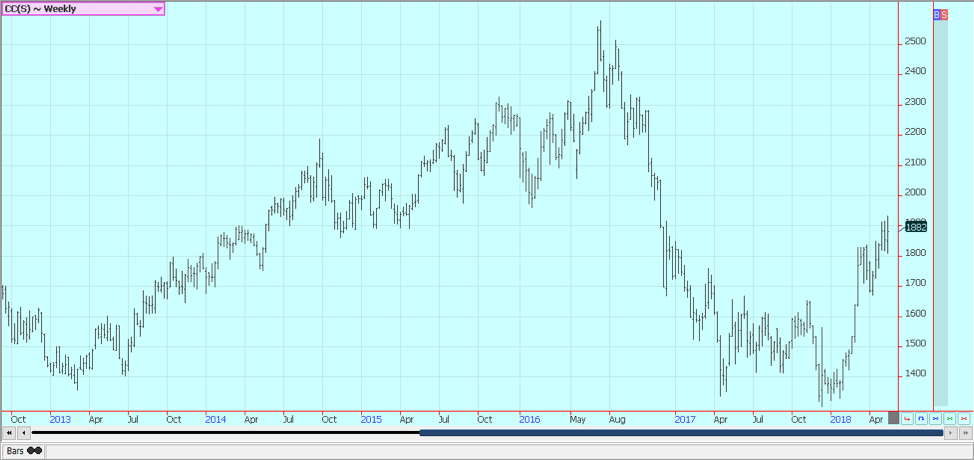

Futures were much lower in New York, but higher London last week. The spread between New York and London has now begun to correct back to more normal levels as New York is losing its steam to move higher but as London continues to rally. The widespread is due to the fund buying in New York, and also due to the need to pay higher to attract African supplies.

Asian supplies are now less available since Asian grinding capacity has increased, so New York has space for African Cocoa. Ideas that world production has been largely sold remain part of the rally. Showers and more seasonal temperatures have been seen in the last few weeks to improve overall production conditions in West Africa. The mid-crop harvest is active.

Weekly New York Cocoa Futures © Jack Scoville

Weekly London Cocoa Futures © Jack Scoville

—

DISCLAIMER: This article expresses my own ideas and opinions. Any information I have shared are from sources that I believe to be reliable and accurate. I did not receive any financial compensation in writing this post, nor do I own any shares in any company I’ve mentioned. I encourage any reader to do their own diligent research first before making any investment decisions.

The TopRanked.io Weekly Digest: What’s Hot in Affiliate Marketing [LiveChat Affiliates Review]

Quick Disclosure: We’re about to tell you how LiveChat Affiliates run a top-notch affiliate program. And we really mean it....

German SMEs Face Tighter Bank Lending, Turn to Alternatives

Access to bank loans for German SMEs is tightening despite strong financing needs. About 37.8 percent face restrictive lending, driven...

Bitcoin Stalls as Geopolitical Risks and Crypto Industry Tensions Persist

Bitcoin is moving sideways near $72,000 amid ongoing Iran tensions, while ETF inflows remain strong. Quantum security debates continue. Ethereum...

Geopolitical Tensions and Trade Disruptions Reshape Global Commodities Markets

Geopolitical tensions and disrupted trade routes, especially around the Strait of Hormuz, are reshaping global commodities markets. Agriculture faces supply...

Germany Sees 413 Cannabis Cultivation Clubs Two Years After Partial Legalization

Two years after partial cannabis legalization in Germany, 413 cultivation clubs have been established nationwide. Lower Saxony leads in clubs...

|

|

|  |

|

|

-

Africa4 days ago

Africa4 days agoForeign Exchange Markets Walk a Tightrope Amid Geopolitical Tensions and Policy Uncertainty

-

Markets2 weeks ago

Markets2 weeks agoCotton Prices Rise Amid War Tensions, Weather Risks, and Supply Concerns

-

Fintech2 days ago

Fintech2 days agoGerman SMEs Face Tighter Bank Lending, Turn to Alternatives

-

Biotech1 week ago

Biotech1 week agoGilead Sciences Advances Growth Strategy with Focus on HIV, Oncology, and Innovation

You must be logged in to post a comment Login