Featured

The price to earnings ratio: When cheap means crap

There are key differences between earnings growth and price-earnings. Knowing them could spell success or failure to investors in stock market.

Everyone loves cheap, especially investors. But when cheap becomes crap, cheap becomes expensive. In the stock market, investors are seduced by low-quality stocks looking cheap and promising at first sight. The moment of happiness lasts until they realize that the stock’s performance is moderate at best. And low-quality stocks often result in capital losses and dividend cuts.

A notorious dazzler

Dividing price by earnings is a common metric to determine a stock’s valuation. Unfortunately, “common” does not equal “correct.” In an open market, whenever something looks cheap, something is rotten. The stock market is one of the most open markets, thus cheap means something must be very rotten.

Don’t believe? Let’s have a look what “cheap” really means.

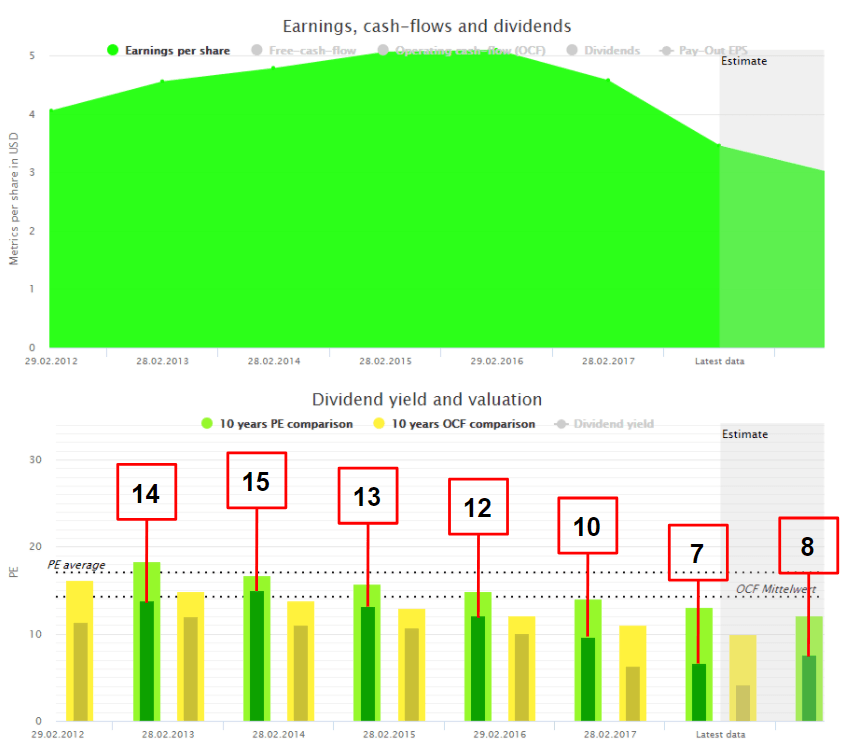

How cheap looks like

These charts show the relationship between earnings growth and price-earnings. As earnings decline, the stock price declines even faster, leading to a contraction of the price-earning-ratio. The stock becomes “cheap” because the company is in serious “earnings” trouble, and the market does not believe in fast recovery.

(Source: DividendStocks.Cash)

The stock price tumbled from above $70 in 2014 to less than $23 now. A painful capital loss for anybody invested. If you “took the chance” and bought in 2017 when the price-earnings-ratio was “only” 10, you still lost about 50 percent. Sole consolation: when all earnings are gone, there is no price-earnings-ratio anymore.

No price-earnings-ratio — then what?

Long-term investors should always invest in high-quality stocks, but the price-earnings-ratio has no clue about quality. That’s the problem, and that’s why we need other metrics. Which one, I’ll tell another time.

P.S.: The same goes for the price-to-book-ratio.

—

DISCLAIMER: This article expresses my own ideas and opinions. Any information I have shared are from sources that I believe to be reliable and accurate. I did not receive any financial compensation in writing this post, nor do I own any shares in any company I’ve mentioned. I encourage any reader to do their own diligent research first before making any investment decisions.

Morocco’s Growth Holds at 4.6% as Agriculture Offsets Economic Pressures

Morocco’s economy grew 4.6% in Q1 2026, driven by a strong agricultural rebound offsetting declines in industry. Services expanded moderately...

Abivax Shares Surge as New Trial Data Eases Safety Concerns Over Ulcerative Colitis Drug

Abivax shares surged nearly 36% after positive updated trial results for its ulcerative colitis drug obefazimod reassured investors following earlier...

El Dorado Raises $9M to Expand Cross-Border Fintech Platform

El Dorado, a Latin American fintech improving cross-border financial services, raised a $9 million Series A led by Paradigm with...

Bitcoin Stalls Near $60K as Strategy Moves, ETFs Outflow, and EU MiCA Rules Take Effect

Bitcoin hovers near $60,000 with ETF outflows, while Strategy boosts reserves, sells BTC, and raises dividends to reassure investors. Ethereum...

Cannabis Dominates Global Drug Use: Trends, Risks, and Shifting Markets

Cannabis remains the world’s most widely used illicit drug, with 256 million users in 2024, surpassing all others combined. Growth...

|

|

|  |

|

|

-

Biotech1 week ago

Biotech1 week agoNew Gene Therapies Transform Rare Disease Care, but Gaps Remain

-

Biotech2 hours ago

Biotech2 hours agoAbivax Shares Surge as New Trial Data Eases Safety Concerns Over Ulcerative Colitis Drug

-

Crowdfunding7 days ago

Crowdfunding7 days agoIthaca: Climate Road Trip RPG on Climate Resistance

-

Fintech2 weeks ago

Fintech2 weeks agoFintech and AI: Adoption Grows, but Profits Favor Agile Innovators

You must be logged in to post a comment Login