Business

Rice exports see solid demand due to competitive US prices

Demand from the mills is said to be quiet, but exports are going strong, with US prices deemed competitive in Latin America and the Caribbean Basin.

Wheat

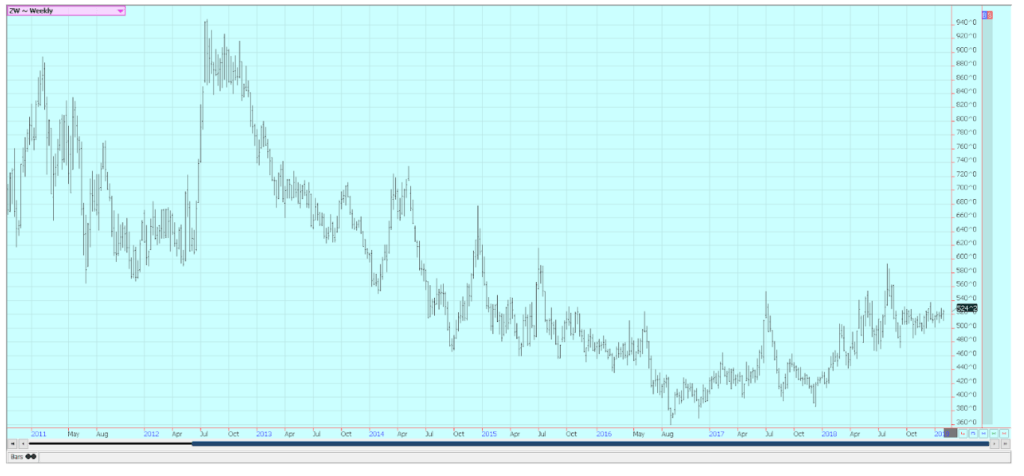

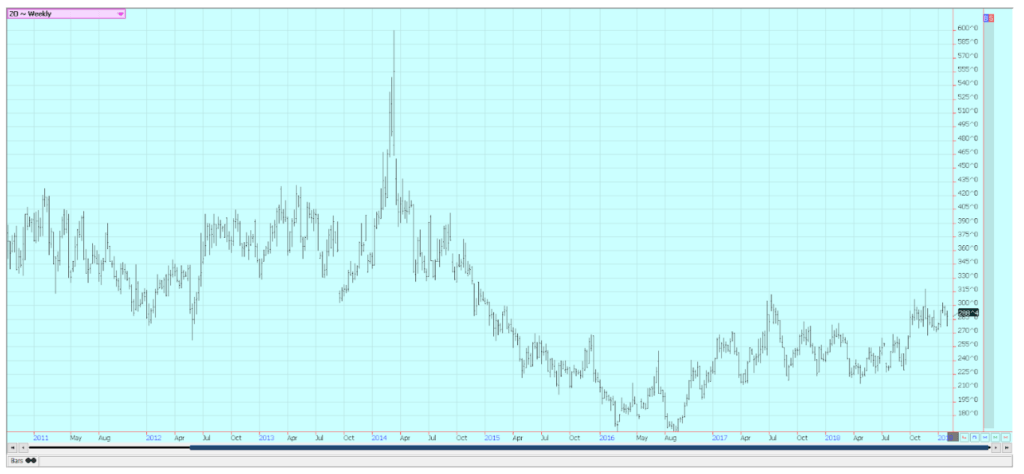

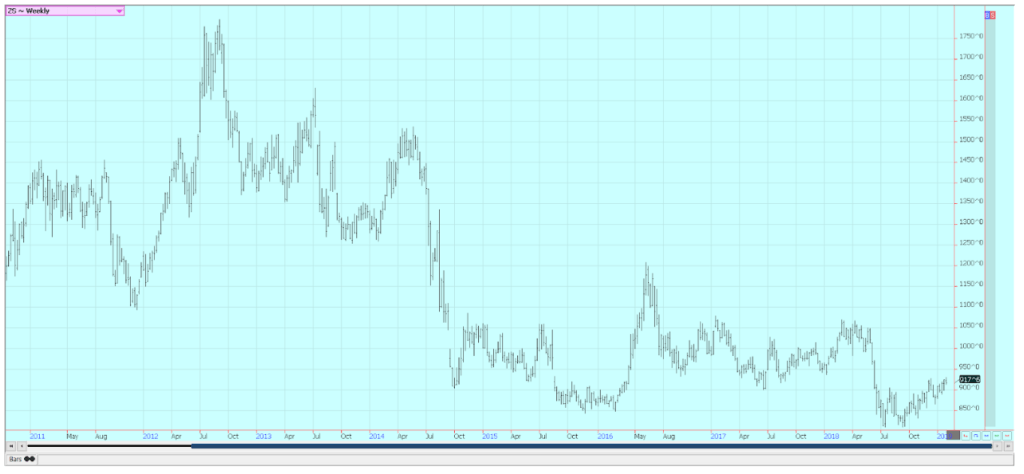

Winter Wheat markets were mixed again last week after a good rally on Friday pulled Chicago SRW and Minneapolis Spring markets higher, but left HRW with slight losses. Futures rallied on Friday on news that Ethiopia had tendered for 450,000 tons of world Wheat and that US Wheat would be considered and would be price competitive. Traders were waiting for demand news or at least some signs of improved demand. The only demand news released by USDA was the weekly export sales report from December 20, and this news was too old to affect prices. USDA said it would catch up with the weekly reports by the end of the month. The China meetings last week in Washington apparently ended on a positive note, and there is hope for some demand from that country as well as others as US Wheat remains competitively priced. They were also keeping an eye on the weather as extreme and record cold that invaded the US Midwest last week. The SRW crop could be at risk, especially in areas ill little or no snow cover. Some early estimates said that up to 20% of that crop could have been lost or damaged. There are no reports of damage so far from the Great Plains. USDA said that the January reports will be released with the February reports on February 8. The Wheat Seedings report could easily show that not all of the Winter Wheat got planted in the Midwest and Great Plains due to wet conditions in the Fall planting period. The price action has been positive and implies that higher prices are possible in the short to medium term. However, prices are working in a range for now.

Weekly Chicago Soft Red Winter Wheat Futures © Jack Scoville

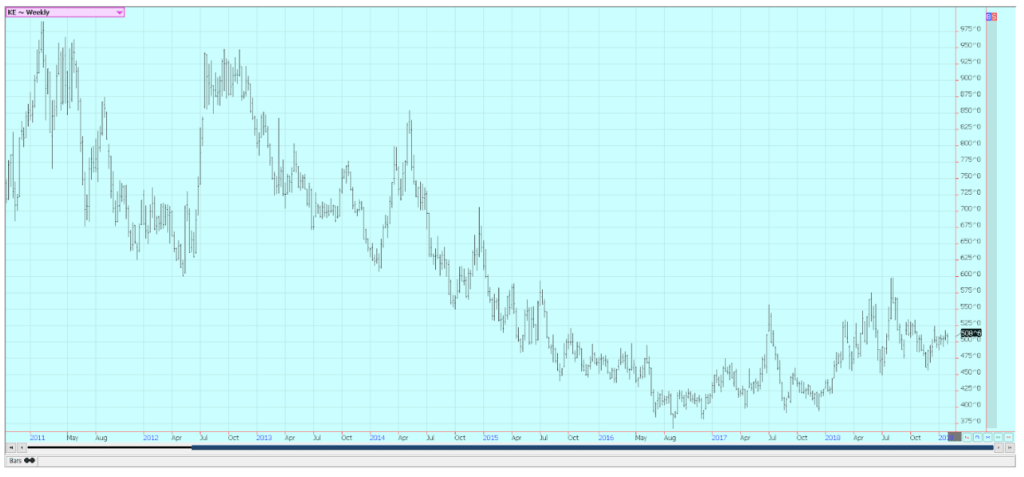

Weekly Chicago Hard Red Winter Wheat Futures © Jack Scoville

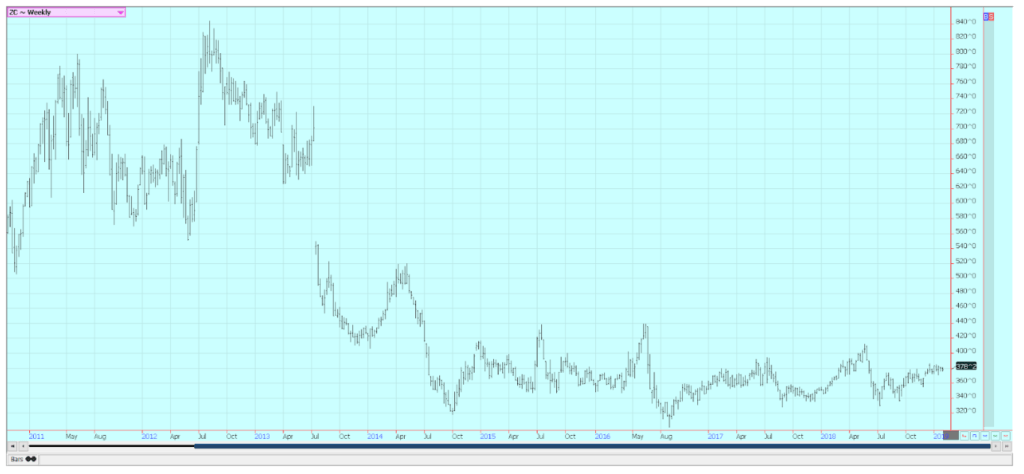

Weekly Minneapolis Hard Red Spring Wheat Futures © Jack Scoville

Corn

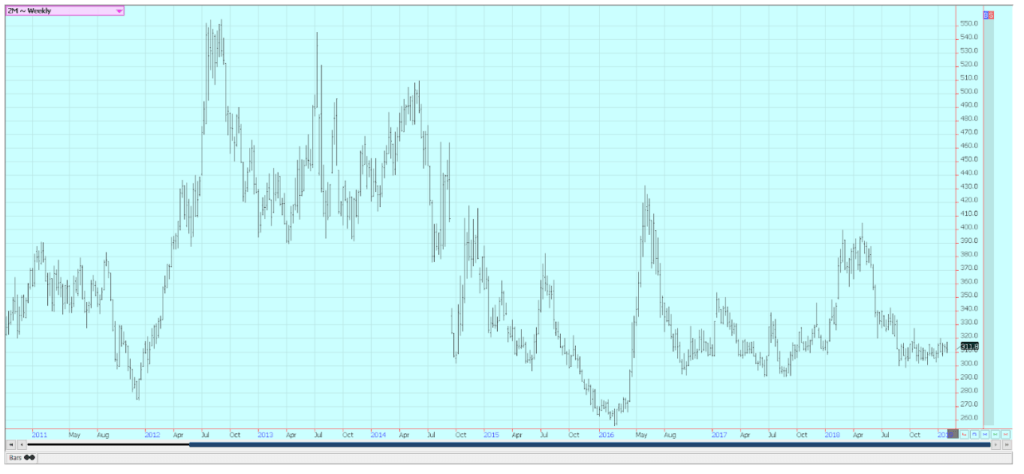

Corn was higher on Friday, but a little lower for the week as the market. Oats were also lower for the week. The first weekly export sales report since the government shutdown was released and it showed strong demand. The report was from December 20 and was considered too old to do much for prices. USDA will catch up on the rest of the weekly reports by late this month. USDA will issue the January reports along with the February reports on Friday. The Corn data for last year is expected to show reduced production. Demand could be a little weaker as well, especially with the current weakness in the ethanol market. It remains dry and hot in central and northern Brazil, but the weather patterns are starting to change and feature at least some showers in important Winter Corn growing areas. The Soybeans harvest is expanding in Mato Grosso and Parana, and farmers will be ready to plant the winter Corn once the Soybeans are out. The harvest pace and planting pace have been ahead of normal there and also in Parana. The Corn market still finds increased selling interest when prices try to get close to the 390 March area, and has been able to find support near 370 March. Trends are currently sideways on the daily charts and sideways on the weekly charts.

Weekly Corn Futures © Jack Scoville

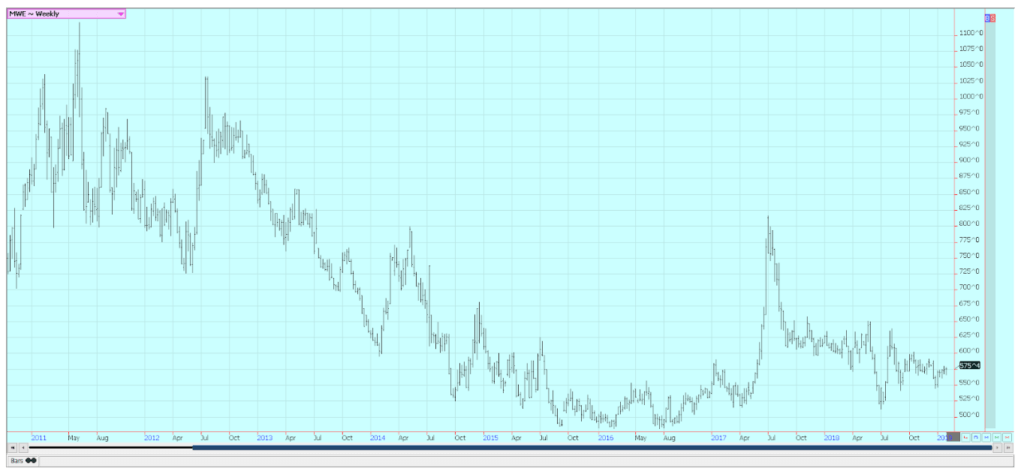

Weekly Oats Futures © Jack Scoville

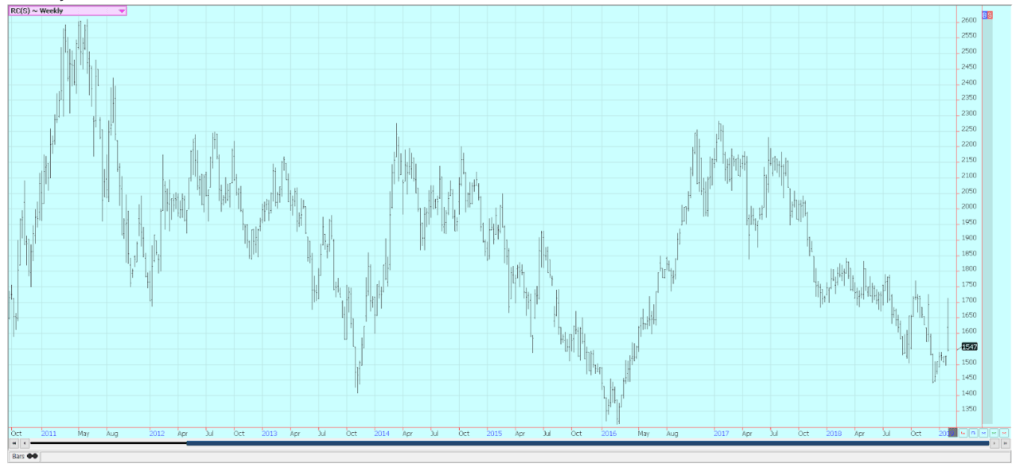

Soybeans and soybean meal

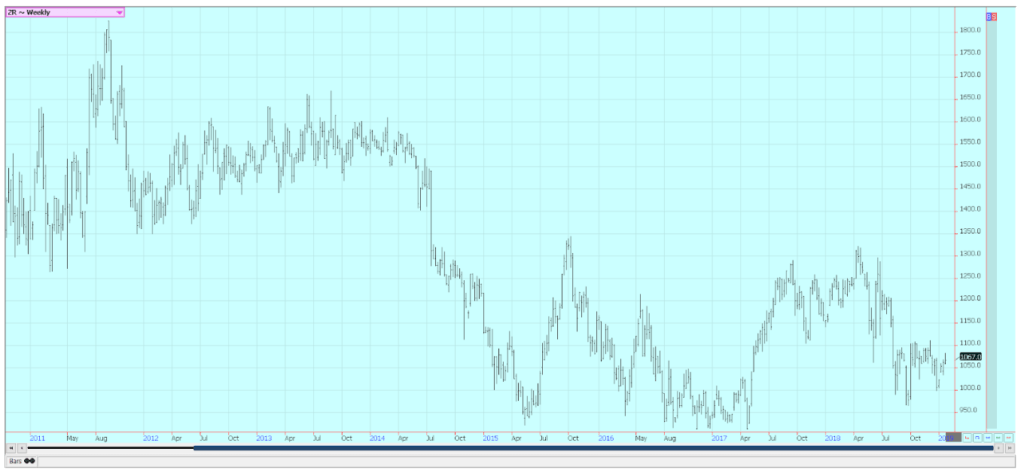

Soybeans and Soybean Meal were lower last week as movement was seen in the US-China trade dispute. There was apparently good progress made at the talks, and word was leaked that any deal now would include a commitment from China to buy another five million tons of US Soybeans. There was talk that China had already bought at least one million tons. This news allowed Soybeans to rally for most of Friday, but late selling took the market well off the highs and futures closed near the lows of the day. Trends are sideways on the weekly charts for these markets, and the fundamentals of big supplies might keep rallies in check. US Soybean Meal supplies should be increasing as crushers look to produce Soybean Oil due to higher prices in that product, and Soybean Meal trends are starting to turn down. There are plenty of Soybeans to sell from the US and South America. USDA released its first weekly export sales report since the shutdown and announced part of the sale of about 5.0 million tons to China that were made in the last month. It will catch up with the weekly reports by late this month. It will release the January reports along with the February reports on Friday. Soybeans remain a weather market. South American weather remains too wet in Argentina and southern Brazil and too dry in western Parana and parts of Mato Grosso and Mato Grosso do Sul. These weather trends are finally starting to change, but it is too late to help most Soybeans in Brazil. There have been reports of losses in the early harvest areas of western Parana and Mato Grosso. Private Brazil production estimates range from about 110 million tons to about 115 million tons.

Weekly Chicago Soybeans Futures © Jack Scoville

Weekly Chicago Soybean Meal Futures © Jack Scoville

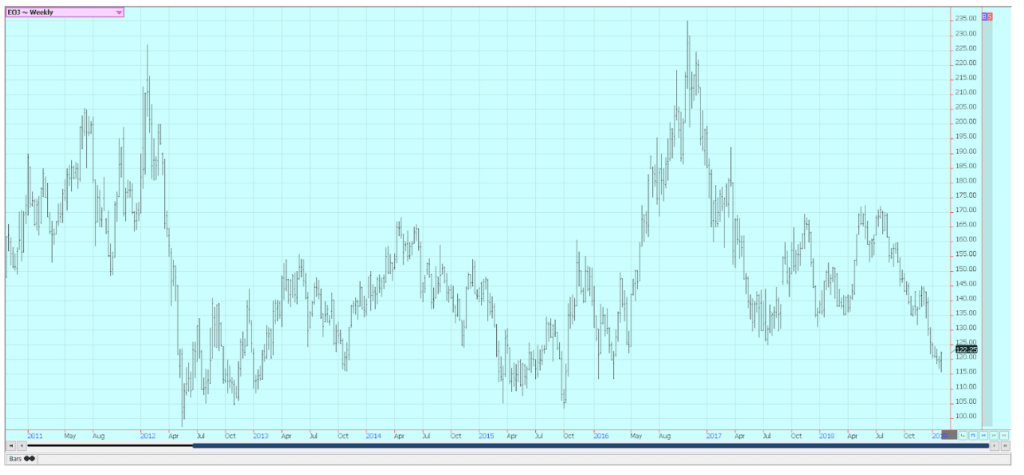

Rice

Rice was a little higher Friday and slightly lower for the week in very quiet trading. Weekly charts show that futures are near strong resistance areas, and the quiet tone in the cash market is reflecting the lack of farmer interest in selling. Demand from the mills is said to be quiet, but export demand should be solid as US prices are competitive into Latin America and the Caribbean Basin. Basis levels remain generally firm in Arkansas, but are weak in Texas. The Arkansas market needs a little Rice and is not getting much offer from the producers. Basis levels have shown some weakness near the Gulf coast due to light demand. Producers do not seem interested in further sales at this time, and prices are too cheap for them right now. South American weather has not been good for growing Rice, and internal prices there have not interested producers. Ideas are that production will be less in Mercosur again this year. The weather is a problem in the US as it has been too wet near the Gulf Coast for producers to begin fieldwork.

Weekly Chicago Rice Futures © Jack Scoville

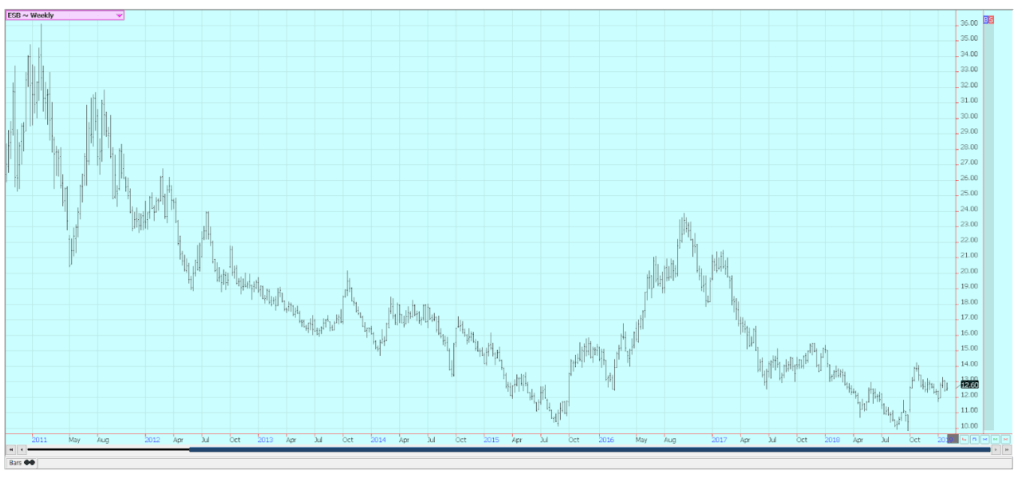

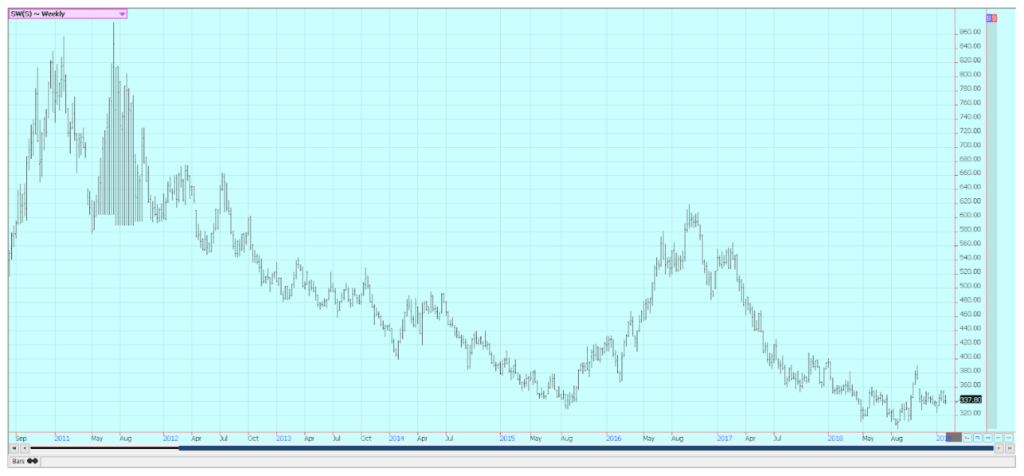

Palm oil and vegetable oils

World vegetable oils prices were mostly a little lower on reports and ideas that demand is improving. Only Palm Oil managed to close with slight gains on ideas of stronger demand. Exports from Malaysia have improved, and production should be starting a seasonal decline. Malaysian export taxes are 0%, and Indian import taxes are currently very low and allow for imports at profitable prices. Trading interest in Palm Oil will be limited this week due to the Lunar New Year holiday. Daily charts show and weekly charts show futures mostly in up trends, especially for Palm Oil and Soybean Oil. Canola is the weaker market as the Canadian Dollar has been strong and due to worries about Chinese demand. Soybean Oil closed slightly lower despite Palm Oil strength and better demand ideas. Domestic and export demand is thought to be stronger due to biofuels demand as Soy bean Oil is cheaper into some areas than Palm Oil.

Weekly Malaysian Palm Oil Futures © Jack Scoville

Weekly Chicago Soybean Oil Futures © Jack Scoville

Weekly Canola Futures © Jack Scoville

Cotton

Cotton was a little lower last week and trends are sideways on the daily and the weekly charts. Weak overall demand continues to impact the US market, but word of smaller supplies is providing the support. USDA showed good export demand on its first weekly export sales report since the shutdown, but the data was deemed too old to offer any support to prices. USDA will catch up with the weekly data by late this month and will release the January data along with the February data at the end of this week. Ideas are that Cotton production can be reduced as some of the crop was left in the fields well into the Winter season. US producers report that there is still a lot of Cotton out in the fields to be harvested, and the quality of the fiber is going down. At least some of the unharvested crop might have to be abandoned. World production and supplies are going still lower due to bad weather in the growing season for major producers around the world, including India, Pakistan, and Australia. India and Pakistan are expected to import more Cotton this year to cover the short domestic production. China had problems with its growing weather, too, and has been forced to import a lot of Cotton this year. Demand for US Cotton has been disappointing. China has not bought any US Cotton this year and has been active in other markets, especially India. The US has had disputes this year with other major importers such as Turkey, and this could impact demand for the US. US prices are down and China might start to look at the US crop, but there have been worries about the quality of the US crop due to some extreme growing conditions in Texas and the Southeast over the Summer and Fall. Ideas are that the quality worries have kept some importers of US Cotton away from the market.

Weekly US Cotton Futures © Jack Scoville

Frozen concentrated orange juice and citrus

FCOJ was higher on Friday, and higher for the week in reversal trading. Trends are now sideways on the weekly charts. A reversal higher often happens at this time of year. The market has absorbed speculative long liquidation and producer selling through the Winter as no freeze has developed. Longer range forecasts show that there is little chance for a freeze to develop this month, and then it will be getting to be too late for a freeze to be seen in the state of Florida. The Oranges harvest is active in Florida as the weather is warm and mostly dry. The fruit is abundant, but arrivals to packinghouses and processors are reported behind last year. Florida producers are seeing small sized to good sized fruit, and work in groves maintenance is active. Irrigation is being used in all areas. Packing houses are open to process fruit for the fresh market, and all processors are open in the state to take packing house eliminations and fresh fruit. Mostly good conditions are reported in Brazil, and some beneficial rains should be seen this week.

Weekly FCOJ Futures © Jack Scoville

Coffee

Futures were lower on Friday and lower for the week in both New York and London. New York failed once again to turn trends up, but prices still held the recent trading range. Weekly chart trends are sideways in London. Brazil should be getting past the gut slot of its harvest, and the strong export pace from the country should start to turn down. Brazil had a big production year for the current crop, but the next crop should be less as it is the off year for production. Ideas are that the current production of 62 or 63 or more million bags can become about 52 million bags next year. El Nino is fading, but remains in the forecast, and Coffee areas in Brazil could be affected by drought that could hurt production even more. Many areas are dry now, but showers are in the forecast for this week. Vietnam is active in its harvest. Selling will be less this week due to the Lunar New Year holiday. Production in Vietnam is estimated less than 30 million bags due to uneven weather during the growing season.

Weekly New York Arabica Coffee Futures © Jack Scoville

Weekly London Robusta Coffee Futures © Jack Scoville

Sugar

Both markets moved lower on Friday, but a littler higher for the week. The weekly charts in both markets show mixed trends and the market appears to be searching for a direction at this time. Petroleum futures appear to have made some short term lows at this time, and petroleum futures strength seems to be helping change the tone in Sugar. Brazil has been using a majority of its Sugarcane harvest to produce ethanol this year instead of Sugar. Unica reported that In the season from April 1 through Jan. 16, the mills crushed 562.7 million tons of cane, down 3.6% from the same period a year earlier. Sugar production fell nearly 27% to 26.4 million tons, and ethanol output rose almost 20% to 30.2 billion liters. The production mix for the season through Jan. 16 was 35.5% sugar to 64.5% ethanol. A year earlier, the mix was 46.9% sugar and 53.1% ethanol. There are doubts on just how much production will be seen this year in India. Northwest India had been experiencing hot and dry weather that could cut yields. It has not announced a reduction in its export goal of 5.0 million tons this year, but it appears that the country will not export nearly that much. Some industry sources told wire services that exports could be only half of the target. The government is now exploring ethanol use for the surplus. Dry conditions continue in northern Brazil and there are frequent rains in Rio Grande do Sul. Very good conditions are reported in Thailand, but the next production could be less as farmers might switch to other crops due to low prices for Sugarcane. Thailand has crushed 45.1 million tons of Sugarcane this year, from 34.6 million last year. It has produced 4.5 million tons of Sugar, from 3.4 million tons last year.

Weekly New York World Raw Sugar Futures © Jack Scoville

Weekly London White Sugar Futures © Jack Scoville

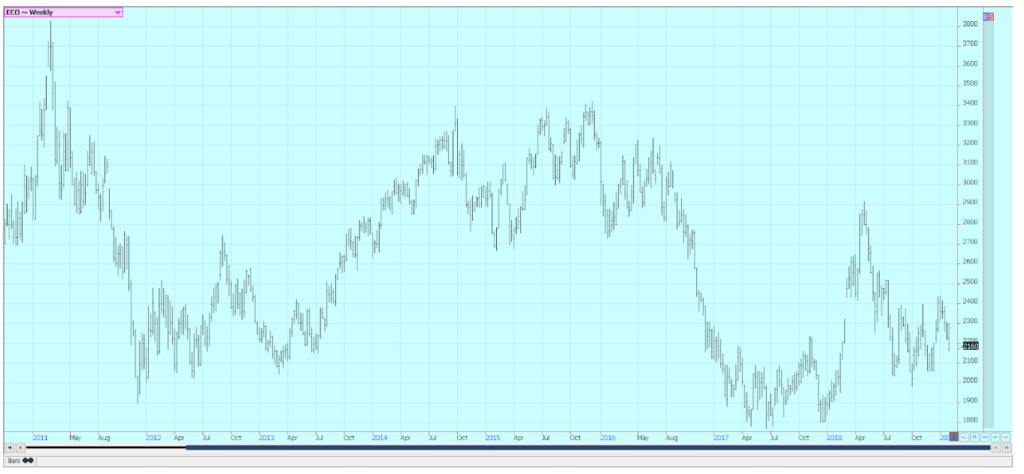

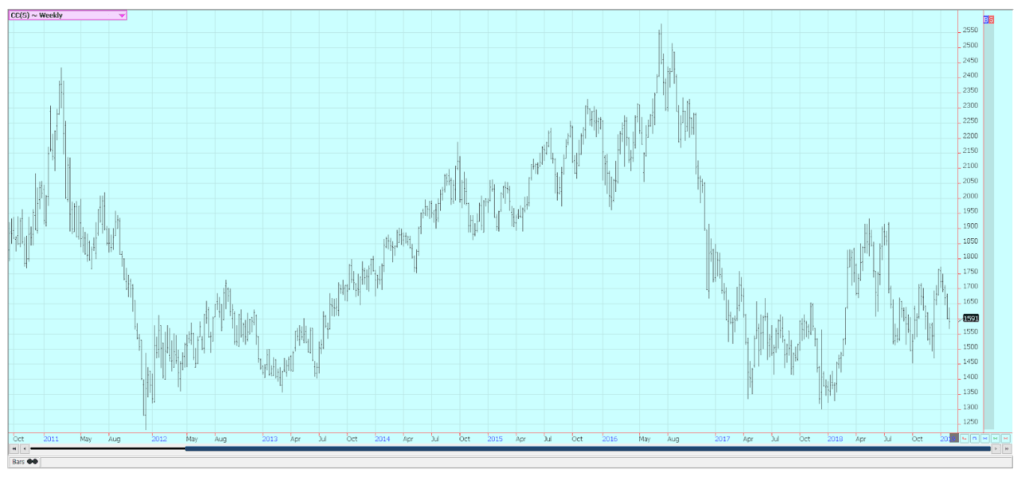

Cocoa

Futures closed lower for the week in New York and lower in London as the new main crop harvest continues in West Africa. Trends are down. The outlook for strong production in the coming year is still around, and ports are said to have plenty of Cocoa on offer. The main crop harvest is active in West Africa. Harmattan winds and hot and dry conditions have moved into West Africa. The winds have stayed to the north of primary production areas so far this season. These conditions can take moisture out of the soil very rapidly and cause some very significant stress on the trees. Conditions appear good in East Africa and Asia. Demand is said to be improving as offers from the new harvest start to increase.

Weekly New York Cocoa Futures © Jack Scoville

Weekly London Cocoa Futures © Jack Scoville

—

DISCLAIMER: This article expresses my own ideas and opinions. Any information I have shared are from sources that I believe to be reliable and accurate. I did not receive any financial compensation for writing this post, nor do I own any shares in any company I’ve mentioned. I encourage any reader to do their own diligent research first before making any investment decisions.

Wyrmgold Launches Crowdfunding Campaign for Believe in me! (please)

Wyrmgold has launched a Gamefound campaign for Believe in me! (please), a darkly humorous board game where 2–4 players compete...

Fintech and AI: Adoption Grows, but Profits Favor Agile Innovators

AI is becoming standard in financial services, but adoption doesn’t guarantee returns. While most institutions use AI, many remain stuck...

AseBio 2025 Report Highlights Growth and Future Potential of Spanish Biotechnology

AseBio presented its 2025 report on the Biotech Act, highlighting opportunities for Spanish biotechnology while urging greater ambition, funding, and...

Bitcoin and Ethereum Markets Steady as Strategy and Bitmine Expand Holdings Amid World Cup Crypto Activity

Bitcoin trades sideways around $66,000 while ETFs see $64 million outflows. Strategy bought 1,587 BTC for $100 million and increased...

SBTi Net-Zero Standard 2.0 Enhances Corporate Climate Action

The Science Based Targets initiative (SBTi) has released Corporate Net-Zero Standard Version 2.0, a major update to its global framework...

|

|

|  |

|

|

-

Crowdfunding1 week ago

Crowdfunding1 week agoHistoric KiHa 2101 Railcar Restored in Japan Through Community Effort

-

Impact Investing6 days ago

Impact Investing6 days agoEU Approves €23B Italian Renewable Energy Plan to Boost Climate Goals

-

Biotech2 weeks ago

Biotech2 weeks agoEarly Use of Tirzepatide Shows Strong Results in Type 2 Diabetes Study

-

Biotech2 days ago

Biotech2 days agoAdvances in Biomarkers and Targeted Therapies Transform Kidney Care in Autoimmune Disease