Featured

The Market Will Have Enough Coffee When the Next Harvest Comes

New York and London closed mostly higher Friday as the US Dollar moved sharply lower but nearby months were lower on signs of less demand for Brazilian Coffee. Brazil sold 3.57 million bags of Coffee in October, down 4.3% from the previous year. Weather conditions are good in Brazil and the rest of Latin America and supplies available to the market should keep increasing.

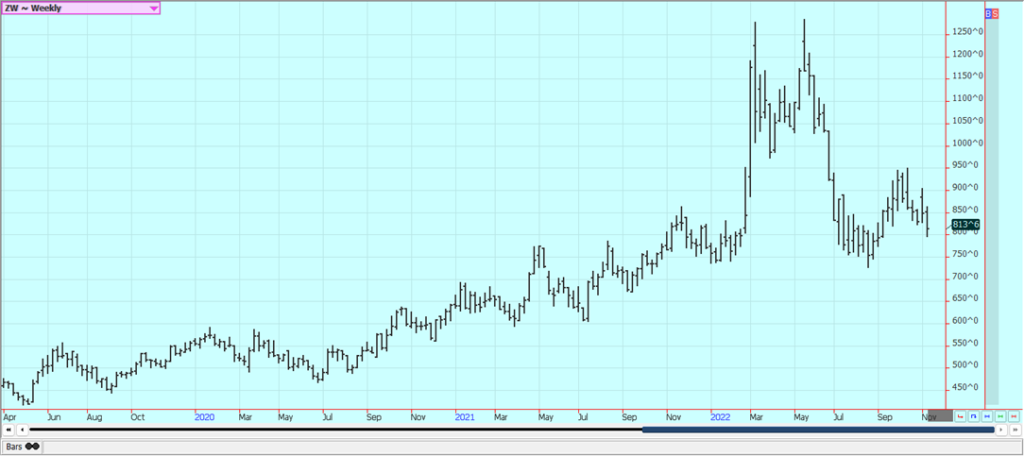

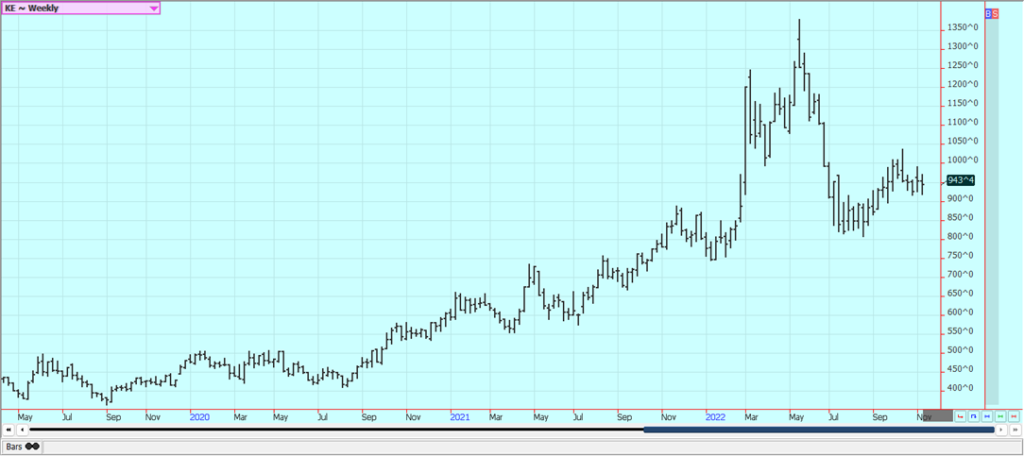

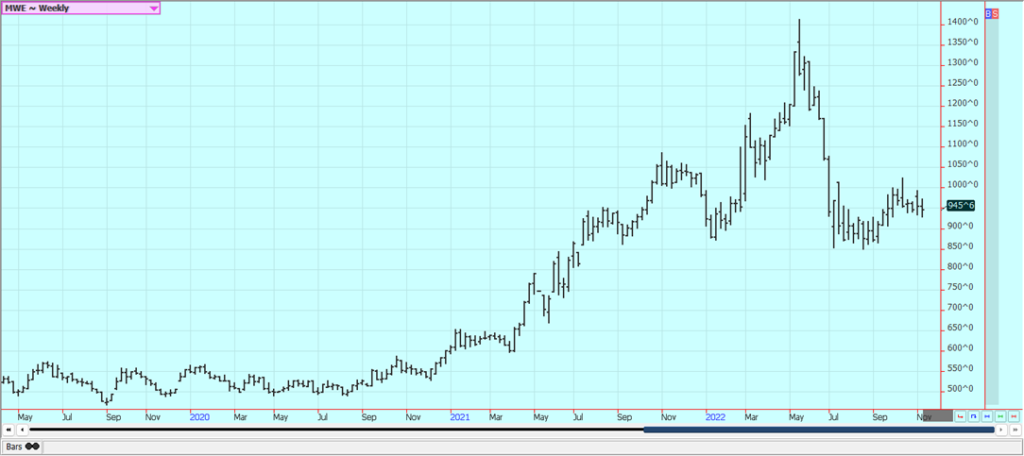

Wheat: Wheat markets were a little lower last week in part on follow-through selling in response to the USDA report and in part on ideas that a new Russia-Ukraine export agreement will be reached and exports from both countries will be likely and will likely increase in the volume. The US Dollar was sharply lower last week and trends have turned down for now on the daily charts. A cut in demand and an increase in ending stocks was seen but the increase in ending stocks was only 10 million bushels and smaller than expected. The reduced pace of export sales for the US were bearish. The demand for US Wheat still needs to show up and right now there is no demand news to help support futures.

Weekly Chicago Soft Red Winter Wheat Futures

Weekly Chicago Hard Red Winter Wheat Futures

Weekly Minneapolis Hard Red Spring Wheat Futures

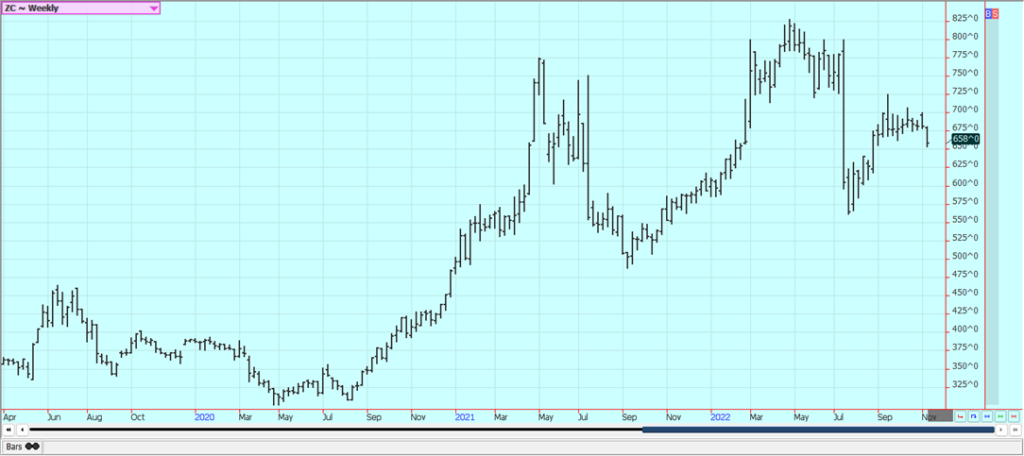

Corn: Corn and Oats closed lower last week, with Corn lower on selling from the lack of export demand. USDA increased yields and production a little and increased demand a little to produce only a minor increase in ending stocks estimates. Domestic demand was increased while export demand was left unchanged. Weak demand for US Corn remains a big problem for the market and USDA was expected to cut demand and raise ending stocks in its coming WASDE reports. The US Dollar index was sharply lower last week and lost about 4,500 points. The Mississippi river is low due to the dry conditions seen in most of the central parts of the US Barge traffic has been reduced. The cash market has been strong in the Gulf but weak in the Midwest river areas due to the low river levels. There are increasing concerns about demand with the Chinese economic problems caused by the lockdowns creating the possibility of less demand as South America has much better crops this year to compete with the US for sales. Export demand in general has been slow so far this year and was slow in the weekly export sales report.

Weekly Corn Futures

Weekly Oats Futures

Soybeans and Soybean Meal: Soybeans and the products were higher on Friday and mixed for the week, with Soybeans and Soybean Oil higher and Soybean Meal lower. News on Friday that China was relaxing Covid restrictions supported the market on Friday. China will now require eight days in quarantine instead of two weeks or more. The US Dollar Index lost 1,500 points Friday and 2,500 points on Thursday for a dramatic turnaround. USDA increased yields in its reports on Wednesday and left demand alone. Ending stocks were higher than the trade anticipated at 220 million bushels. Export demand for the US is heating up and the new demand could not come at a better time. Domestic demand should be increasing for Soybeans as the crush spreads got richer and provided crushers with a big profit margin for their crushing Export demand has suffered due to the lack of good buying by China, but China has been a very active buyer this week. Ideas are that Brazil is off to a very good start. The Mississippi river is low due to the dry conditions seen in most of the central parts of the US but some rain fell in the basin last week and river levels should work a little higher. Barge traffic has been reduced but could increase with the improved river flows. The trade is worried about demand due to a lack of Chinese interest. Brazil is still offering its old crop Soybeans, and South America as a whole is expected to produce a very big crop later this year for harvest next Spring as the weather outlook is positive for crops. However, the third year of La Nina as predicted by meteorologists could cut the production potential. US production ideas remain strong after mostly good weather in August.

Weekly Chicago Soybeans Futures:

Weekly Chicago Soybean Meal Futures

Rice: Rice was a little higher last week and closed at new highs for the move. USDA on Wednesday cut export demand by 4.0 million cwt but increased domestic demand by 1.0 million cwt for an overall increase of 2.0 million cwt. The supply side showed reduced yields and production. The Dollar Index was sharply lower on Thursday and Friday and trends have turned down for now on the daily charts. The Dollar Index lost about 4,500 points in the two days. Some new Rice producer selling might be found soon as futures and basis are now getting close to being profitable for producers to sell. Shipping delays were caused by the low river levels on the Mississippi and as the harvest pressure continued. Some rain has fallen in the basin in the last week so barge traffic on the Mississippi might get better. Demand in general has been slow for Rice for both exports and domestic uses but export demand was improved last week. The weekly charts show that trends are up.

Weekly Chicago Rice Futures

Palm Oil and Vegetable Oils: Palm Oil futures were higher on Friday and little changed for the week. Futures rebounded from lower levels on Friday on news that China had relaxed some Covid restrictions so that quarantines now need to be eight days instead of at least two weeks. The MPOB data released on Thursday showed the largest stocks in three years as production improved more than exports did. Ideas are that supply and production will be strong, but demand ideas are now weakening and the market will continue to look to the private data for clues on demand and the direction of the futures market. Demand reports for the current month were stronger yesterday. Canola was closed on Friday yesterday but was lower for the week as the US Dollar moved sharply lower. Reports indicate that domestic demand has been strong due to favorable crush margins. The Canola growing conditions were much improved and production estimates are higher for the year.

Weekly Malaysian Palm Oil Futures

Weekly Chicago Soybean Oil Futures

Weekly Canola Futures:

Cotton: Cotton was mixed to a little higher on Friday and for the week as USDA raised production estimates in its reports on Wednesday. Support came on Friday from the news that China had relaxed its quarantine policy to eight days from at least two weeks before. But, cities are still getting shut down there and the economy is still weak. The Chinese moves could serve to limit the damage a little bit and help support some demand ideas for US Cotton. The recent USDA supply and demand reports showed that US demand was left unchanged and ending stocks trended higher at 300,000 bales. Economic data releases sent the US Dollar sharply lower to help demand ideas as well. There are hopes that China is about to open again despite its zero-tolerance Covid policies. Chinese demand is especially a problem as parts of Wuhan and Shanghai in China got locked down again last week. Trends are now mixed on the charts. Production in the US is very short. The trade is still worried about demand moving forward due to recession fears and Chinese lockdowns but is also worried about total US production potential. It is possible that the continued Chinese lockdowns will continue to hurt demand for imported Cotton for that country and that a weaker economy will hurt demand from the rest of the world.

Weekly US Cotton Futures

Frozen Concentrated Orange Juice and Citrus: FCOJ was lower Friday and for the week last week. Daily and weekly charts show that a downtrend could have started late last week in this market. Historically low estimates of production due in part to the hurricane and in part to the greening disease has hurt production. The weather remains generally good for production around the world for the next crop but not for production areas in Florida that have been impacted in a big way by the storm. Brazil has some rain and conditions are rated good. Mostly dry conditions are in the forecast for the coming days.

Weekly FCOJ Futures

Coffee: New York and London closed mostly higher Friday as the US Dollar moved sharply lower but nearby months were lower on signs of less demand for Brazilian Coffee. Brazil sold 3.57 million bags of Coffee in October, down 4.3% from the previous year. Weather conditions are good in Brazil and the rest of Latin America and supplies available to the market should keep increasing. Ideas are that the market will have enough Coffee when the next harvest comes in a few months. Ideas of a significant recovery in world production next year remain the main cause for any selling. There are still reports of improving growing conditions and increasing availability of Coffee in Brazil. More showers and rains are in the forecast in Brazil’s Coffee areas for this week. The rest of South America and Central America are reported to be in good condition. Vietnam has scattered showers in Coffee areas.

Weekly New York Arabica Coffee Futures

Weekly London Robusta Coffee Futures

Sugar: New York and London closed higher last week as the overall tight supply situation continues. Trends are still up in both markets. The move came even as Brazil crushed 85% more Sugarcane in the second half of October qt 31.5 million tons. The weather in Brazil remains good for the next crop. More ideas that supplies of White Sugar would soon be increasing for the market could limit the upside for the London market. The world Sugar market is expected to be in a big surplus production next year. Ideas of a world surplus in the coming year are hurting the prices in both markets, but supply remains tight for now. Brazil Sugar offers are likely to drop in volume with the return of Lula as president of Brazil. He is much more environmentally focused than the previous president was and is likely to return the ethanol and biofuels mandates to previously higher levels. Indian exporters are now selling into the world market and have been aggressively looking to sign sales contracts. India has had a very good production year and estimated Sugar production is now at 36.5 million tons with 9.0 million tons available for export.

Weekly New York World Raw Sugar Futures

Weekly London White Sugar Futures

Cocoa: New York and London closed lower on Friday as the US Dollar moved sharply lower for the second day. The weekly charts show that New York closed higher for the week but London closed lower. Chart trends are mixed on the daily charts in New York while chart trends have turned down on the daily charts in London. Trends remain up in both markets on the weekly charts and both markets are being supported by reports of reduced arrivals in Ivory Coast ports. Good production is reported and traders are worried about the world economy moving forward and how that could affect demand. Supplies of Cocoa are as large as they will be now for the rest of the marketing year. Reports of scattered showers along with very good soil moisture from showers keep big production ideas alive in Ivory Coast. The weather is good in Southeast Asia.

Weekly New York Cocoa Futures

Weekly London Cocoa Futures

__

(Featured image by Alexas_Fotos via Pixabay)

This article may include forward-looking statements. These forward-looking statements generally are identified by the words “believe,” “project,” “estimate,” “become,” “plan,” “will,” and similar expressions. These forward-looking statements involve known and unknown risks as well as uncertainties, including those discussed in the following cautionary statements and elsewhere in this article and on this site. Although the Company may believe that its expectations are based on reasonable assumptions, the actual results that the Company may achieve may differ materially from any forward-looking statements, which reflect the opinions of the management of the Company only as of the date hereof. Additionally, please make sure to read these important disclosures.

Futures and options trading involves substantial risk of loss and may not be suitable for everyone. The valuation of futures and options may fluctuate and as a result, clients may lose more than their original investment. In no event should the content of this website be construed as an express or implied promise, guarantee, or implication by or from The PRICE Futures Group, Inc. that you will profit or that losses can or will be limited whatsoever. Past performance is not indicative of future results. Information provided on this report is intended solely for informative purpose and is obtained from sources believed to be reliable. No guarantee of any kind is implied or possible where projections of future conditions are attempted. The leverage created by trading on margin can work against you as well as for you, and losses can exceed your entire investment. Before opening an account and trading, you should seek advice from your advisors as appropriate to ensure that you understand the risks and can withstand the losses.

Blockchain Adoption Accelerates as SwissChain and Amundi Launch Tokenized Financial Solutions

SwissChain Holding SA has digitized its share certificates using blockchain, improving transparency, efficiency, and ownership tracking while maintaining Swiss legal...

Cocoa Markets Steady as Weak Demand and Rising Supply Signal Potential Surplus

New York and London markets higher range trading, with mixed short term trends. Strong West African harvests and favorable rains...

Global Markets on Edge as Iran Conflict, Inflation Pressures, and Financial Risks Intensify

Iran conflict threatens economy disruptions beyond energy to agriculture and goods. Rising PPI signals persistent inflation, risking stagflation reminiscent of...

The Iran War Tests Bitcoin and Crypto Market Resilience

The Iran war has driven oil prices higher and disrupted crypto markets. Bitcoin rose despite volatility, while mining activity declined....

Italy’s Pharmaceutical Sector Drives Innovation, Sustainability, and European Leadership

Italy’s pharmaceutical sector invests €4 billion annually, including €2.3 billion in R&D and €1.7 billion in industrial technologies, up 21%...

|

|

|  |

|

|

-

Fintech6 days ago

Fintech6 days agoPayPay Targets Global Expansion After Landmark IPO

-

Cannabis2 weeks ago

Cannabis2 weeks agoNew Global Survey Shows Growing Cannabis Acceptance in Poland

-

Crypto1 day ago

Crypto1 day agoThe Iran War Tests Bitcoin and Crypto Market Resilience

-

Crypto1 week ago

Crypto1 week agoOil Surge and Iran War Lift Bitcoin as Crypto Sentiment Improves