Featured

The Rally Potential for Soybeans Might Not Be that Great Unless Demand Improves

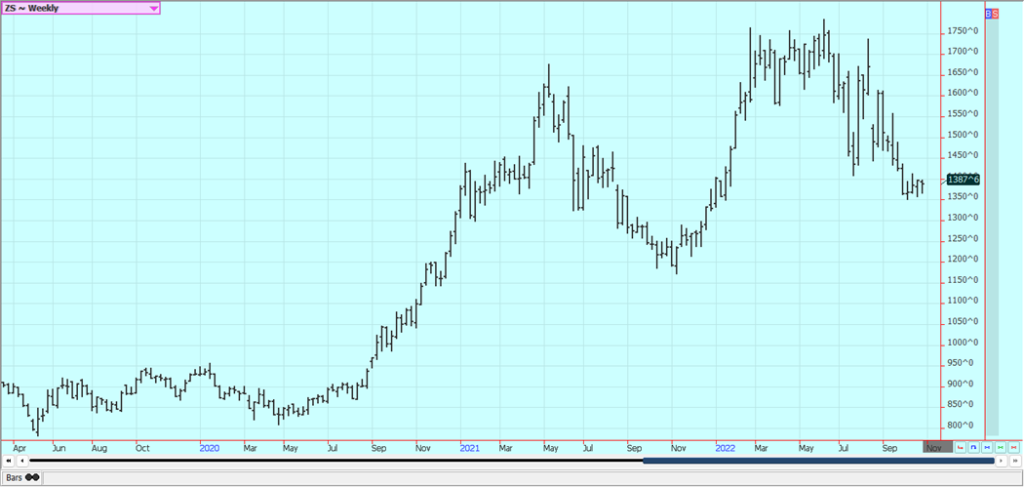

Soybeans closed a little lower and the products were higher as the weekly export sales report for Soybeans was strong. Domestic demand should also be increasing for Soybeans as the crush spreads got richer and provided crushers with a big profit margin for their crushing. The US is now more than 80% done with the harvest and a turn to higher prices becomes more possible.

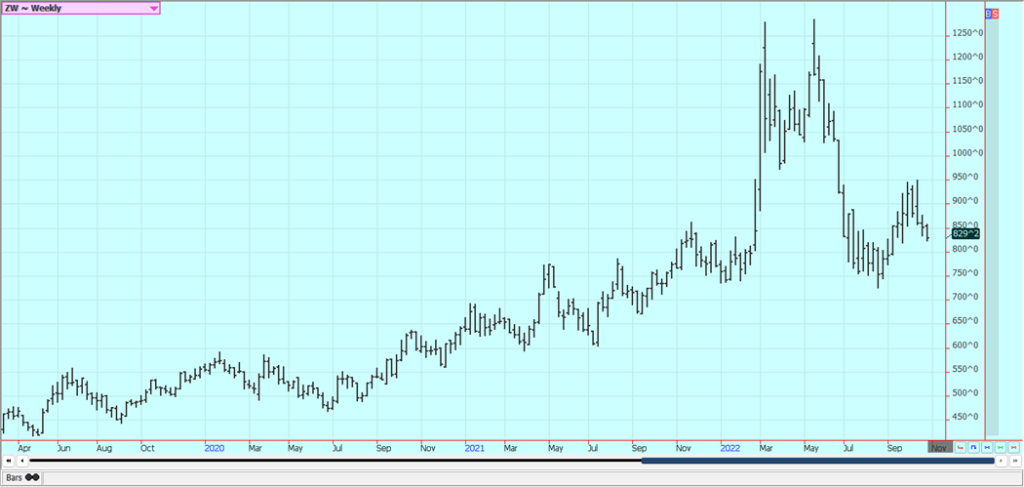

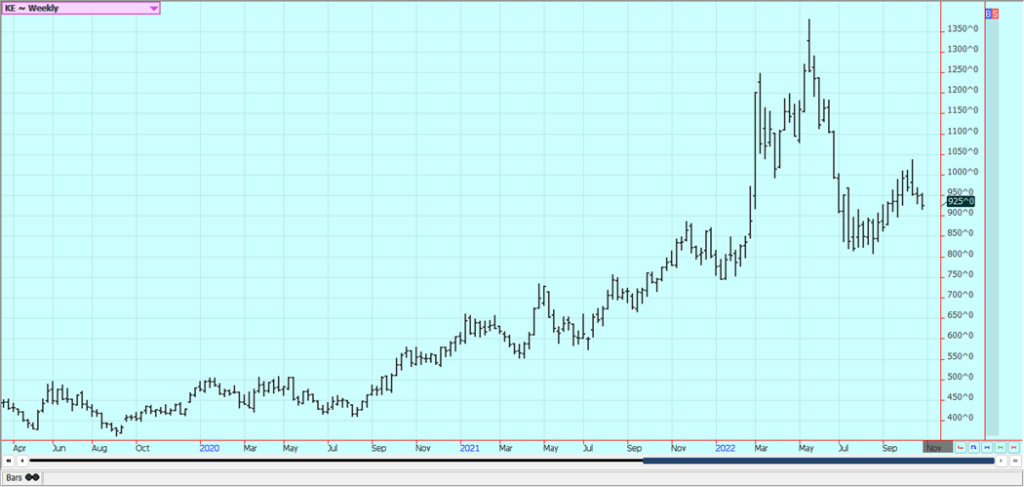

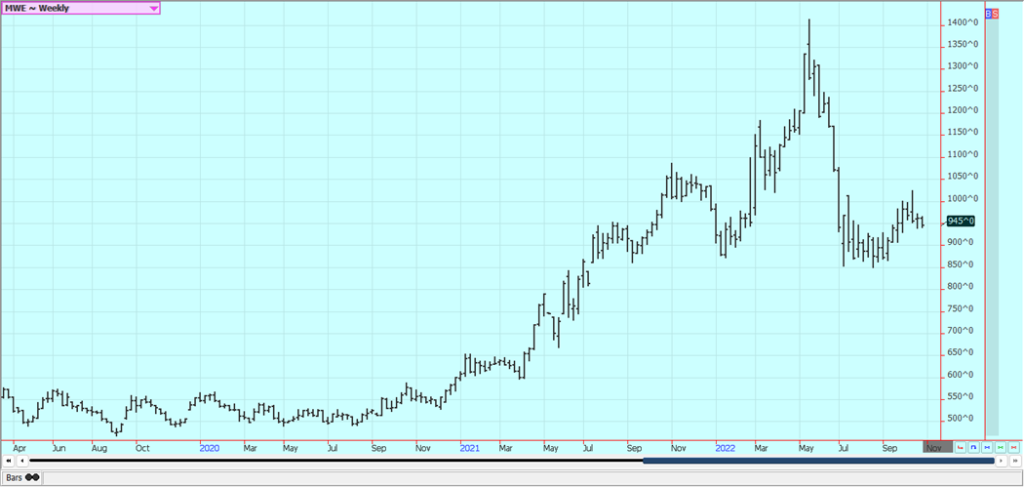

Wheat: Wheat markets were a little lower last week and trends started to turn down again in the Winter Wheat markets. Trends are sideways in Minneapolis as the Spring Wheat Harvest is over. The weekly export sales report showed stronger sales but the sales were not enough to turn trends up as export demand has generally been poor until now. Ideas are that weak demand can continue due in part to the stronger US Dollar. Russia is looking to export more and wants Ukraine to export less and to only countries, it defines as poor. Russia still appears to be losing the war and could do something rash to try to hold things together. The demand for US Wheat still needs to show up and right now there is no demand news to help support futures. The US central and southern Great Plains have been too hot and dry although there are some showers in the western Great Plains now. Conditions are called good for the development of Winter Wheat in the Midwest.

Weekly Chicago Soft Red Winter Wheat Futures

Weekly Chicago Hard Red Winter Wheat Futures

Weekly Minneapolis Hard Red Spring Wheat Futures

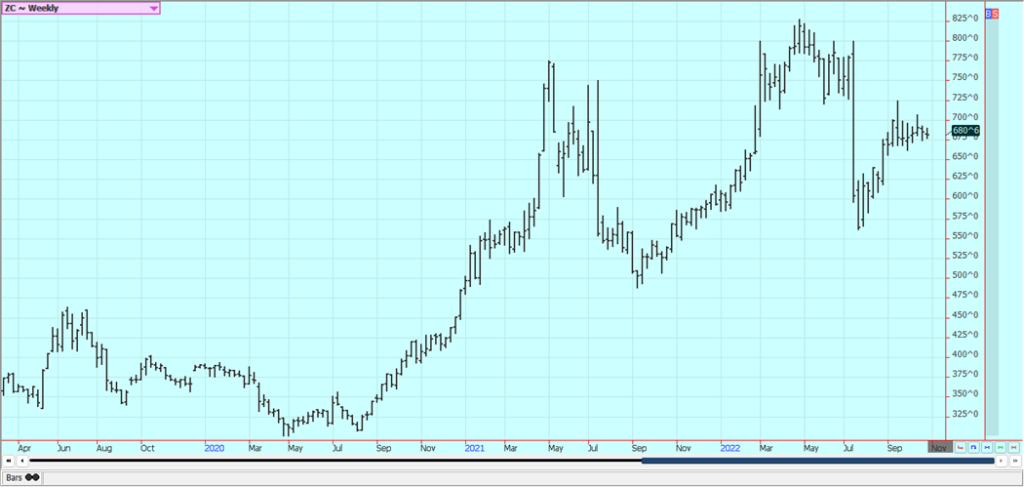

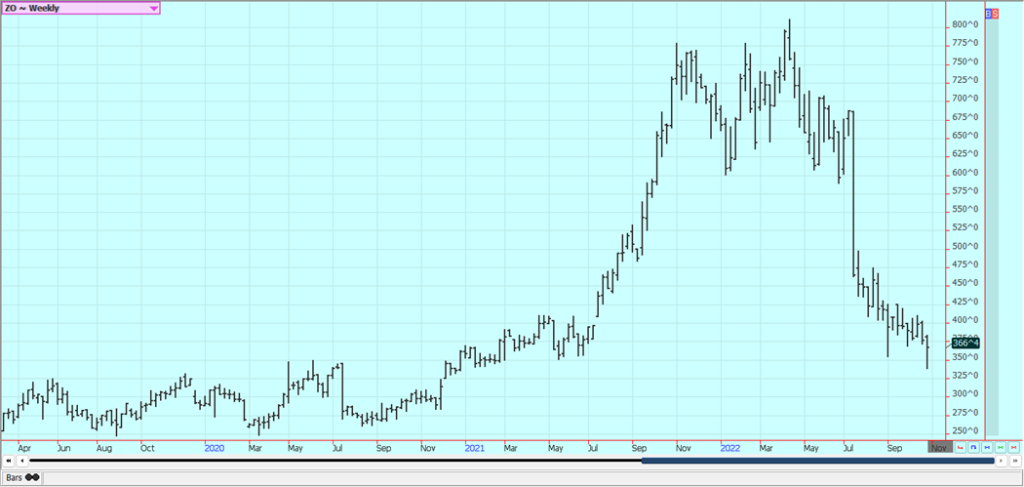

Corn: Corn and Oats closed a little lower last week in range trading. The weekly export sales report showed poor sales and was considered bearish for prices. Futures continue to hold support areas on the charts but fail at resistance areas. The Mississippi river is low due to the dry conditions seen in most of the central parts of the US and there are no forecasts for an improvement soon even with rain in the forecast for today. Barge traffic has been reduced. The cash market has been strong at the Gulf but weak in the Midwest river areas due to the low river levels. The demand side will need to be watched as Corn demand needs to hold to keep lower ending stocks estimates in play. There are increasing concerns about demand with the Chinese economic problems caused by the lockdowns creating the possibility of less demand as South America has much better crops this year to compete with the US for sales. Export demand in general has been slow so far this year.

Weekly Corn Futures

Weekly Oats Futures

Soybeans and Soybean Meal: Soybeans closed a little lower and the products were higher as the weekly export sales report for Soybeans was strong. Domestic demand should also be increasing for Soybeans as the crush spreads got richer and provided crushers with a big profit margin for their crushing. The US is now more than 80% done with the harvest and a turn to higher prices becomes more possible. The rally potential might not be that great unless demand improves, and the US Dollar turns lower. Ideas that Brazil is off to a very good start. The Mississippi river is low due to the dry conditions seen in most of the central parts of the US and there are no forecasts for an improvement soon. Barge traffic has been reduced. The trade is worried about demand due to a lack of Chinese interest caused by the Covid lockdowns there and in part by the stronger US Dollar. Brazil is still offering its old crop Soybeans, and South America as a whole is expected to produce a very big crop later this year for harvest next Spring as the weather outlook is positive for crops. However, a third year of La Nina as predicted by meteorologists could cut the production potential. US production ideas remain strong after mostly good weather in August. Basis levels are weaker in the Midwest but are strong at the Gulf. There are still Chinese lockdowns and there are fears that China has been importing less as a result. However, Chinese data showed huge imports from all sources in September. President Xi has been elected to a third term in China and has stocked the ruling body with his associates so there are fears that nothing will change soon there.

Weekly Chicago Soybeans Futures:

Weekly Chicago Soybean Meal Futures

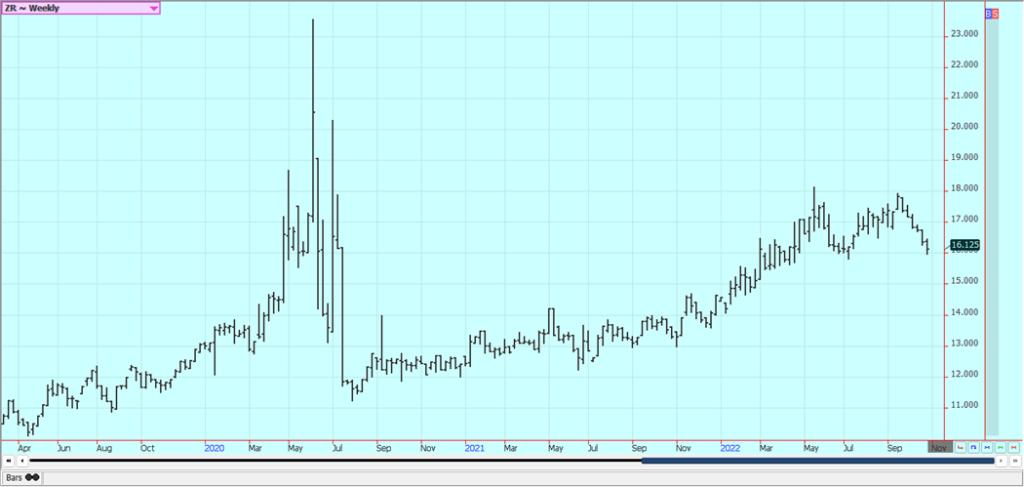

Rice: Rice was a little lower again yesterday in part on shipping delays caused by the low river levels on the Mississippi and as the harvest pressure continued. Demand, in general, has been slow for Rice for both exports and domestic uses but export demand was improved this week at 39,500 tons. The weekly charts show that trends are down. Harvest progress is almost complete in Arkansas, the largest Rice producing state, and yields and quality are reported to be very strong. Mississippi is at harvest with much more mixed results. Producers are done with harvesting in Texas as well as in southern Louisiana. Yield reports have been generally good in Louisiana and quality reports are generally good. Yield and quality have been up and down in Texas.

Weekly Chicago Rice Futures

Palm Oil and Vegetable Oils: World vegetable oils prices were mixed last week, with Canola and Soybean Oil trading higher and Palm Oil lower. Palm Oil was lower on reports of light export demand. Ideas are that supply and production will be strong, but demand ideas are now weakening and the market will continue to look to the private data for clues on demand and the direction of the futures market and that data has been weaker so far this month. Export data has been strong this month from private sources and MPOB reported improved demand last month. Production was also higher and ending stocks were up more than 10% to 2.315 million tons. Canola was higher last week. The Canola harvest is about over. Reports indicate that domestic demand has been strong due to favorable crush margins. The Canola growing conditions are much improved and production estimates are higher for the year.

Weekly Malaysian Palm Oil Futures

Weekly Chicago Soybean Oil Futures

Weekly Canola Futures:

Cotton: Cotton was lower last week and made new lows for the move as traders continue to worry about demand. The weekly export sales report showed very low sales and parts of Wuhan and Shanghai in China got locked down again. Trends are down on the charts. Traders are worried about a global recession and demand in that recession and also about Chinese demand due to the lockdowns there. Production is very short. The harvest is appearing in the market, and the market has responded to it sideways to lower prices. The trade is still worried about demand moving forward due to recession fears and Chinese lockdowns but is also worried about total US production potential. It is possible that the continued Chinese lockdowns will continue to hurt demand for imported Cotton for that country and that a weaker economy will hurt demand from the rest of the world.

Weekly US Cotton Futures

Frozen Concentrated Orange Juice and Citrus: FCOJ was lower last week, with nearby months weaker than deferred months. It seems that the bullish production estimate from USDA is now part of the market price. The market has been holding firm on supply-side fundamentals. USDA estimated Florida production at 28 million boxes in its latest production reports and these are historically low estimates of production due in part to the hurricane and in part to the greening disease that has hurt production in recent years. The weather remains generally good for production around the world for the next crop but not for production areas in Florida that have been impacted in a big way by the storm. Brazil has some rain and the conditions are rated good. More showers are in the forecast for the coming days. Florida damage is expected to be very big, with many trees lost as well as fruit lost. Mexican areas are showing mixed trends, with dry weather in some northern areas but better weather to the south.

Weekly FCOJ Futures

Coffee: New York and London closed sharply lower on Friday and for the week, with ideas of a significant recovery in world production next year as the main cause for the selling. There are still reports of improving growing conditions and increasing availability of Coffee in Brazil. The crop conditions are called good so producers have been selling although they are out of the market now due to the weaker prices. More showers and rains are in the forecast in Brazil’s Coffee areas for this week. The rest of South America and Central America are reported to be in good condition. Vietnam has scattered showers in Coffee areas.

Weekly New York Arabica Coffee Futures

Weekly London Robusta Coffee Futures

Sugar: New York and London closed lower last week on more ideas that supplies of White Sugar would soon be increasing for the market. In fact, the world Sugar market is expected to be in a big surplus production next year. UNICA on Wednesday reported increased crushing and Sugar production from increased offers of Sugarcane in its reports released yesterday. Center-south mills crushed 27.7 million tons of Sugarcane in the period, an increase of 40.5% from the previous year. That made Sugar production 1.8 million tons, an increase of 59%, and Ethanol production 1.4 billion liters, up 10.7%. Ethanol demand has been soft but ideas are that it can increase with recently higher Crude Oil futures. Ideas of a world surplus in the coming year are hurting the prices in both markets, but supply remains tight for now. Indian exporters are still waiting for a government announcement on its export policy before offering much to the market. This announcement is expected within a week now. India has had a very good production year and estimated Sugar production is now at 36.5 million tons with 9.0 million tons available for export.

Weekly New York World Raw Sugar Futures

Weekly London White Sugar Futures

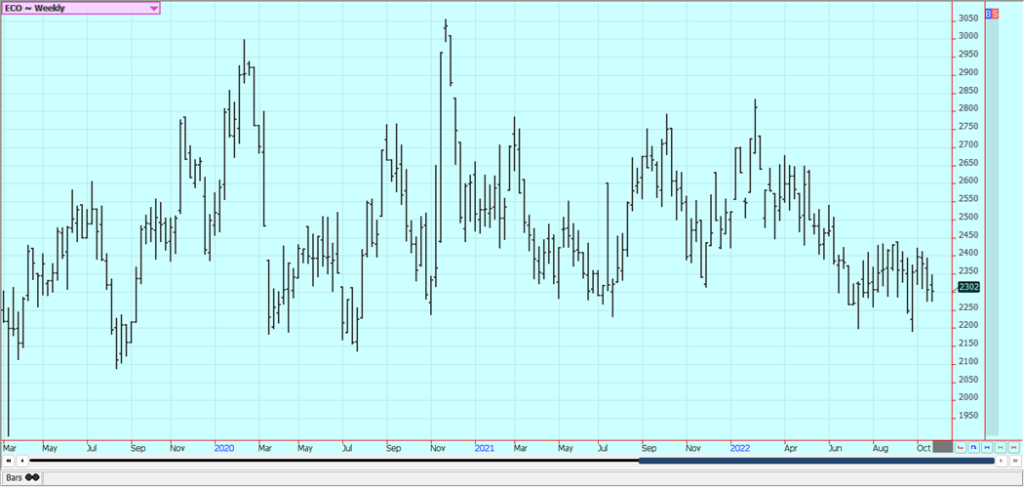

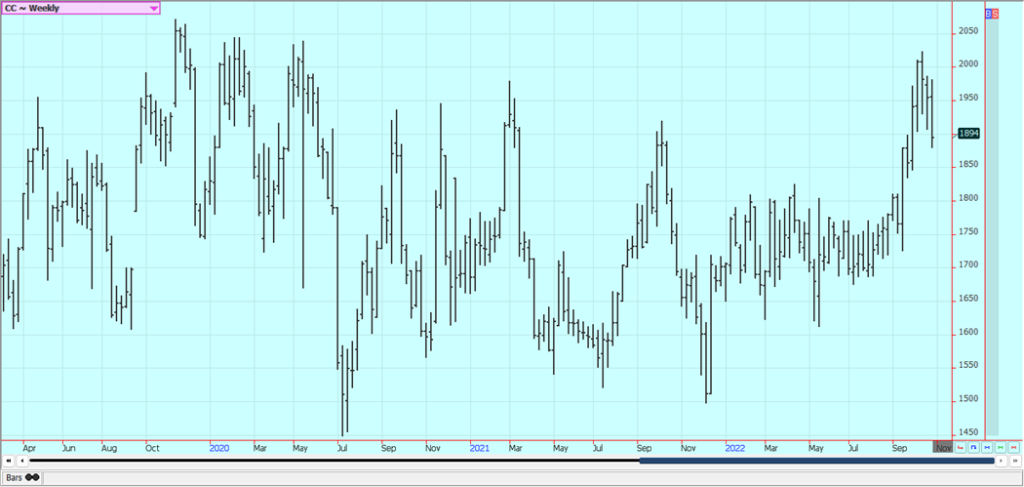

Cocoa: New York was about unchanged and London closed lower last week, price trends are trying to turn down in London as New York holds to a sideways trend. The grind reports were released in the last two weeks and showed strong demand. Good production is reported and traders are worried about the world economy moving forward and how that could affect demand. Supplies of Cocoa are as large as they will be now for the rest of the marketing year. Reports of scattered showers along with very good soil moisture from showers keep big production ideas alive in Ivory Coast. Ideas are still that good production is expected from West Africa as a whole for the year. The weather is good in West Africa. The weather is good in Southeast Asia.

Weekly New York Cocoa Futures

Weekly London Cocoa Futures

__

(Featured image by pnmralex via Pixabay)

This article may include forward-looking statements. These forward-looking statements generally are identified by the words “believe,” “project,” “estimate,” “become,” “plan,” “will,” and similar expressions. These forward-looking statements involve known and unknown risks as well as uncertainties, including those discussed in the following cautionary statements and elsewhere in this article and on this site. Although the Company may believe that its expectations are based on reasonable assumptions, the actual results that the Company may achieve may differ materially from any forward-looking statements, which reflect the opinions of the management of the Company only as of the date hereof. Additionally, please make sure to read these important disclosures.

Futures and options trading involves substantial risk of loss and may not be suitable for everyone. The valuation of futures and options may fluctuate and as a result, clients may lose more than their original investment. In no event should the content of this website be construed as an express or implied promise, guarantee, or implication by or from The PRICE Futures Group, Inc. that you will profit or that losses can or will be limited whatsoever. Past performance is not indicative of future results. Information provided on this report is intended solely for informative purpose and is obtained from sources believed to be reliable. No guarantee of any kind is implied or possible where projections of future conditions are attempted. The leverage created by trading on margin can work against you as well as for you, and losses can exceed your entire investment. Before opening an account and trading, you should seek advice from your advisors as appropriate to ensure that you understand the risks and can withstand the losses.

The TopRanked.io Weekly Digest: What’s Hot in Affiliate Marketing [++ KuCoin Affiliate Program Review]

X now allows people to block certain topics from their feed. This week, we're going to tell you how to...

Hotel Stay Project Supports Wildlife Conservation in Japan

Iwate Prefecture launched a project linking hotel stays to conservation through Morioka Zoological Park Zoomo. A themed room at Yunomori...

Bitcoin Leads Modest Crypto Rebound Amid Mixed Signals

Bitcoin rose 2 percent to above 77000 as ETFs saw 15 million inflows and April gains of 12.2 percent. Ethereum...

Major Pharma Advances: EU Approvals, Vaccine Progress, and Breakthrough Clinical Results

Johnson & Johnson has EU approval for nipocalimab for generalized myasthenia gravis, showing superior control and sustained benefits. Sanofi reported...

Agential Cannabis 2026 to Drive APAC Market Growth and Global Industry Collaboration

Agential Cannabis 2026 will take place September 23–24 in Bangkok, bringing global experts together to advance the APAC medical cannabis...

|

|

|  |

|

|

-

Business1 week ago

Business1 week agoThe TopRanked.io Weekly Digest: What’s Hot in Affiliate Marketing [uMobix Affiliates Review 2026]

-

Biotech2 weeks ago

Biotech2 weeks agoBeeline Medicines Launches with $300M to Advance Precision Therapies for Autoimmune Diseases

-

Crypto2 days ago

Crypto2 days agoCrypto Markets Steady as US Bitcoin Reserve Plans and MegaETH Debut Take Focus

-

Fintech1 week ago

Fintech1 week agoFintech Investment Rebounds in 2025 Amid Cautious Optimism for 2026