Featured

The Weekly Export Sales Report for Rice Showed Poor Demand

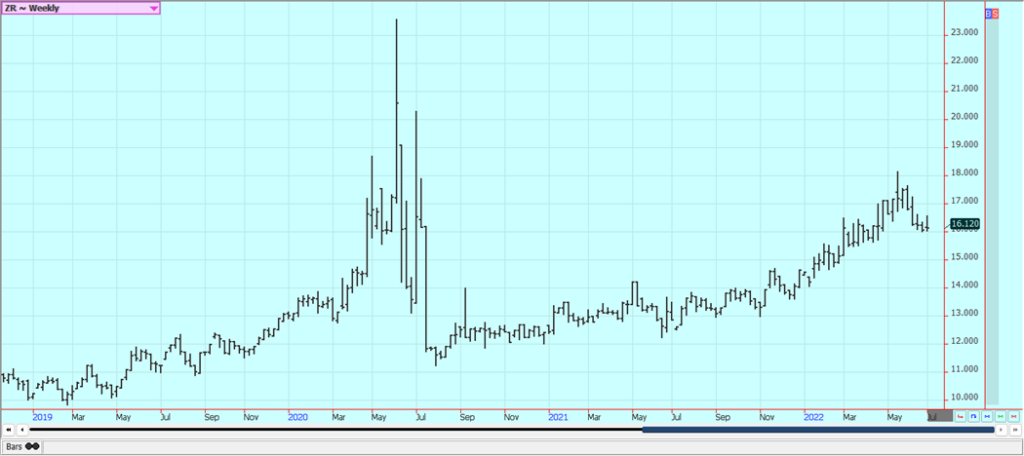

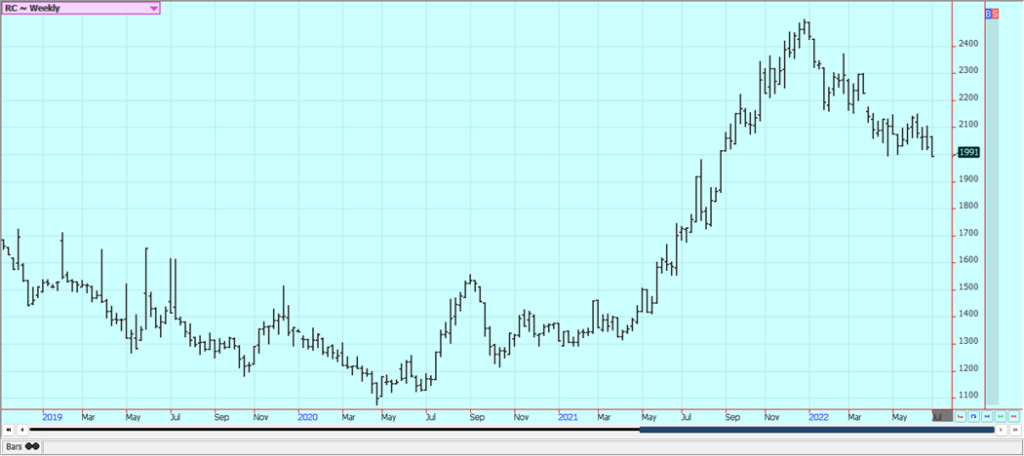

Rice was lower on Friday but higher for the week and sideways trends held together in response to the USDA reports. USDA said that 2.343 million acres of all Rice were planted and that current stocks are now 56.6 million cwt. Both levels are below those of a year ago and should have been considered neutral to positive for prices. The speculators have been the best sellers lately

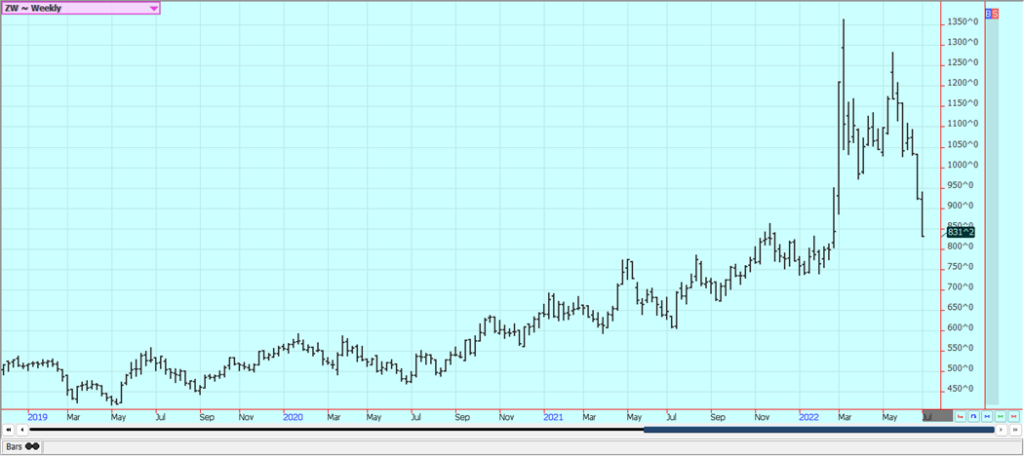

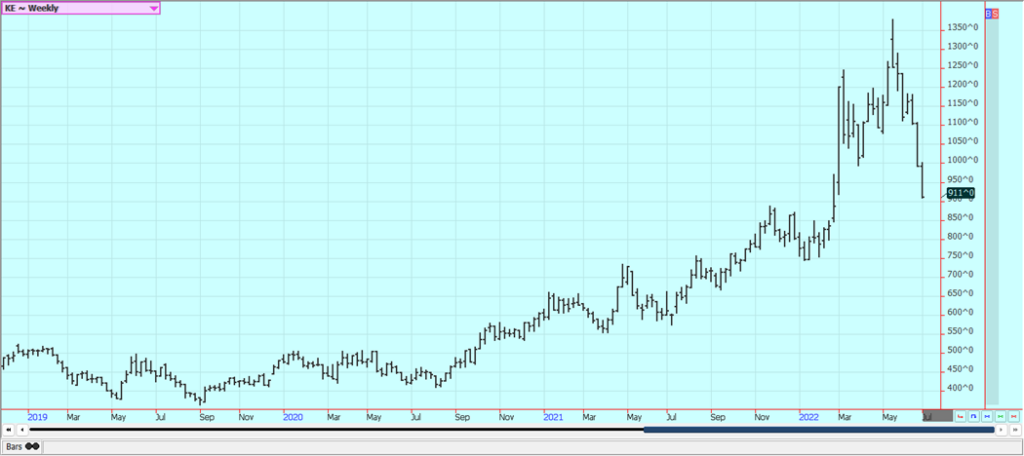

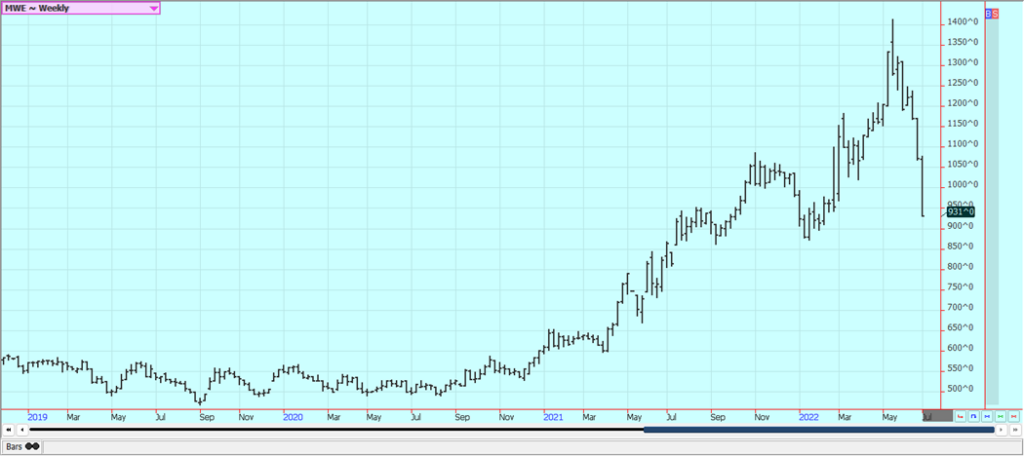

Wheat: Wheat markets were much lower last week as the Winter Wheat harvest is expanding through the Great Plains and Midwest. Trends are down in all three markets. Futures had a negative reaction to the quarterly stocks reports and also the planted area reports. Both showed figures that were little above trade expectations with the quarterly stocks just above the trade guess at 660 million bushels and the planted area reports also just above the average trade guess at 47.1 million acres. The weekly export sales report sowed bad demand for US Wheat once again. Futures should form a harvest low earlier in the harvest due to the small crop size. Yield reports have been weakening in Kansas despite recent rains that have helped kernel size and test weight. Hot and dry weather is back for this week to southern areas while northern areas have more moderate weather. It is turning warmer and drier farther north to give hope to Spring Wheat farmers that they can plant crops. Europe is too hot and dry and India and Pakistan are both past major heat waves and dry conditions.

Weekly Chicago Soft Red Winter Wheat Futures

Weekly Chicago Hard Red Winter Wheat Futures

Weekly Minneapolis Hard Red Spring Wheat Futures

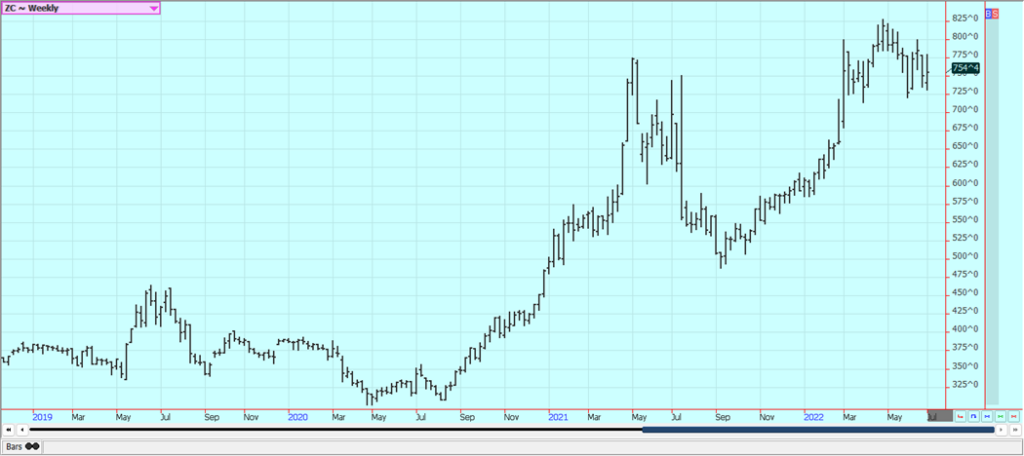

Corn: Corn closed lower in response to the USDA reports and on some outlooks for less hot and still dry weather for the next few weeks. The reports showed more supplies on hand at 4.346 billion bushels and more planted area at 89.9 million acres than trade expectations. The weekly export sales report showed poor demand. Corn has emerged under what is considered good conditions but it has been hot in the Midwest. More moderate temperatures are forecast for the weekend and into next week, but then some forecasts call for hot and dry weather to return while others suggest more normal rainfall. Continued hot and dry weather could hurt yields down the road. Stress could start to develop if the hot and dry weather returns as forecast. Many think the top end of the yield has been taken off the Corn crop due to the delayed planting but others look at the crop condition rating and expect improved yields.

Weekly Corn Futures

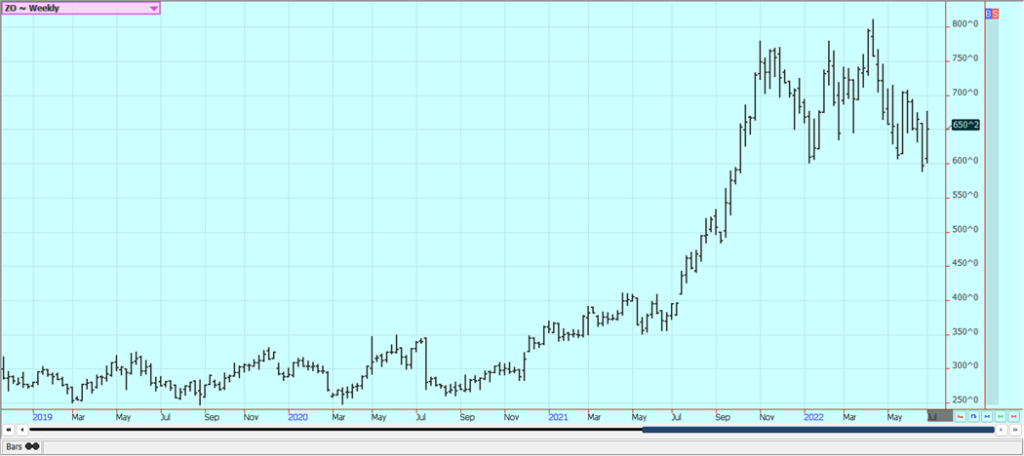

Weekly Oats Futures

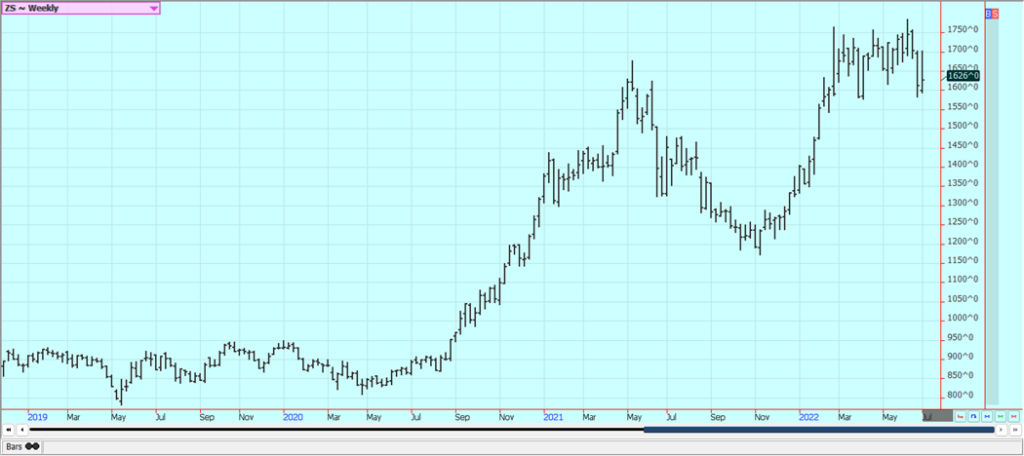

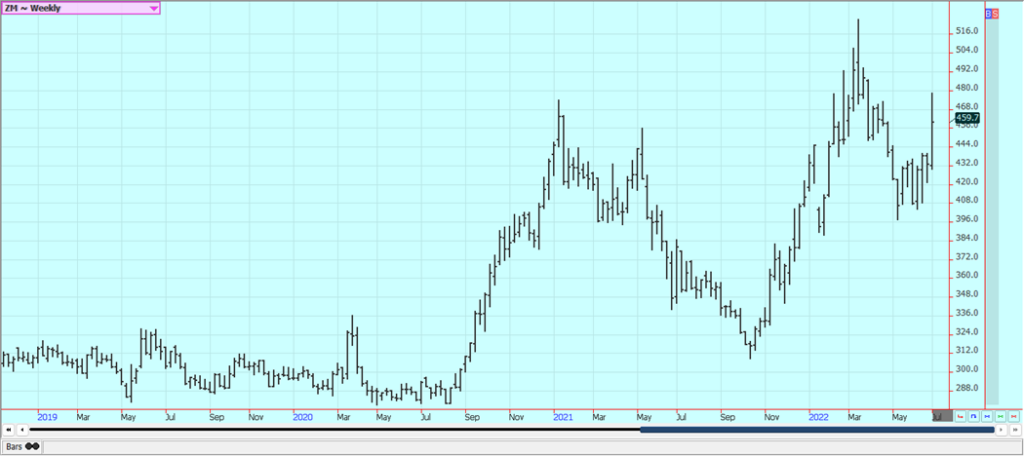

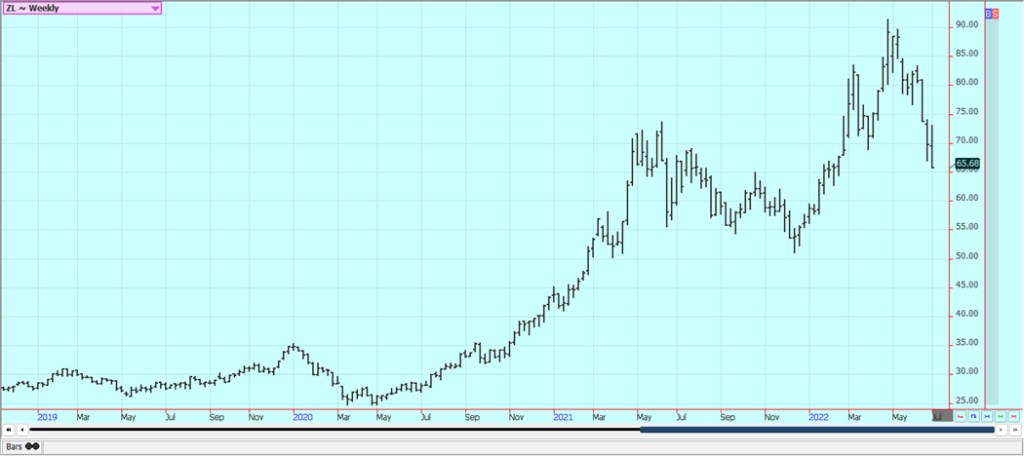

Soybeans and Soybean Meal: Soybeans and the products were sharply lower on Friday as warm and dry weather invades the US and as demand concerns hurt for both markets. A lot of the selling came from fears of a world recession in the short term. USDA found much higher quarterly stocks than anticipated by the trade at 971 million acres but found less planted area than trade expectations at 88.3 million acres. The weekly export sales report showed poor demand for all three markets. US cash market is still running low on Soybeans but there are still renewed Chinese lockdowns. There is less Chinese demand for Soy products due to the lockdowns there and China is starting to renew the lockdowns now as Covid cases have risen in number. China has been a major buyer of US Soybeans this year after a very slow start due to the problems in South America. They are buying for this year and already have booked a large amount of new crop Soybeans to cover future needs. Most of the current buying is for next year.

Weekly Chicago Soybeans Futures:

Weekly Chicago Soybean Meal Futures

Rice: Rice was lower on Friday but higher for the week and sideways trends held together in response to the USDA reports. USDA said that 2.343 million acres of all Rice were planted and that current stocks are now 56.6 million cwt. Both levels are below those of a year ago and should have been considered neutral to positive for prices. The speculators have been the best sellers lately even with perceived bullish fundamental news as many are worried about a worldwide recession. The weekly export sales report showed poor demand. Growing conditions are said to be deteriorating due to hot and dry weather in Texas expanding to include Arkansas.

Weekly Chicago Rice Futures

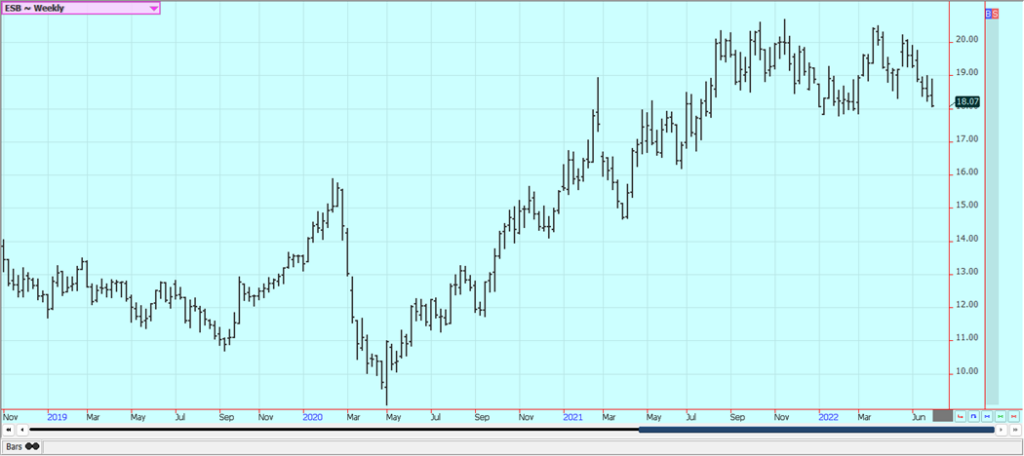

Palm Oil and Vegetable Oils: Palm Oil closed the week lower although the market did trade sideways for much of the week. Export reports from the private sources are showing the weaker demand this month. Some analysts think Palm Oil is topping out anyway due to reduced demand ideas. Hopes for better demand from India keep the market supported, but Chinese demand could be less. Production from Malaysia is expected to increase as well as the Covid lockdowns finally go away and as the weather is good for production. Canola was last week along with other vegetable oils markets. Ideas of poor demand have hit this market as well as the others. The crops are going in the ground and the growing conditions are much improved. It is reported to be very dry and has been cold for planting but better planting weather is coming now as it is now much warmer. There are ideas of reduced Sunflower export potential from Russia and Ukraine. The market is worried about South American production as well. Canada produced a very short crop of Canola last year so supplies are tight.

Weekly Malaysian Palm Oil Futures

Weekly Chicago Soybean Oil Futures

Weekly Canola Futures:

Cotton: Cotton was higher last week in part on the acreage reports that said that 12.5 million acres of Cotton of planted this year. The report suggested that all of the Cotton got planted and now the market is concerned about the weather. There continues to be talk of a big recession here in the US and around the world. Traders worry that the continued Chinese lockdowns will hurt demand for imported Cotton for that country and that a weaker economy in the west will hurt demand from the rest of the world. There are forecasts for hot and dry weather to return this week after some showers in West Texas and the rest of the Great Plains over the last couple of weeks. The crop conditions are better than expected after a very hot and dry period in West Texas and the rest of the western Great Plains. The Indian weather is cooler and wetter and conditions appear good. Chinese demand could become less due to the Covid lockdowns there be trimming imports due to Covid and has closed a number of cities as the Covid spreads through the nation. The cities and ports are shut down again as Covid returns.

Weekly US Cotton Futures

Frozen Concentrated Orange Juice and Citrus: FCOJ was higher yesterday and trends are turning up on the charts. The fall has been dramatic since the market made new contract highs earlier this month. The weather remains generally good for production around the world for the next crop. Brazil has some rain and conditions are rated good. Weather conditions in Florida are rated mostly good for the crops with some showers and warm temperatures. The Florida FCOJ movement and pack report showed that inventories are more than 24% below last year. Nielsen said that 29.22 million gallons of FCOJ were sold through June 16, the lowest volume since October 2019. Volumes are now 23% below those of last year.

Weekly FCOJ Futures

Coffee: New York and London closed lower Friday and mixed for the week, with New York a little higher and London a little lower. It seemed that recession fears hit futures once the North American trading started. Demand for Coffee overall is thought to be less as the world economic situation changes for the worse but the strong cash market means that even less Coffee is on offer. In fact, certified stocks in New York keep dropping and are becoming low. There is less Coffee on offer from origin, with Brazil offering less and Central America and Vietnam offering less as well. Temperatures are near to above normal in Brazil and there are no forecasts for frosts or freezes in the short term.

Weekly New York Arabica Coffee Futures

Weekly London Robusta Coffee Futures

Sugar: New York and London closed lower on Friday on selling that hit all pits. New York closed lower for the week, but London closed higher as White Sugar supplies and production are short right now. New York Raw Sugar and London White Sugar trends are sideways to perhaps up in London on the daily charts. India is reported to have a big crop of Sugarcane coming and as Brazil is harvesting its crop of Sugarcane and turning most of it into Ethanol but some Sugar is making it into export channels. Sugar production from these countries is expected to be surplus or at least in line with demand. Thailand is still offering and exporting. Reports from India indicated that conditions are generally good for Sugar production. The Indian weather service is predicting a normal monsoon season this year.

Weekly New York World Raw Sugar Futures

Weekly London White Sugar Futures

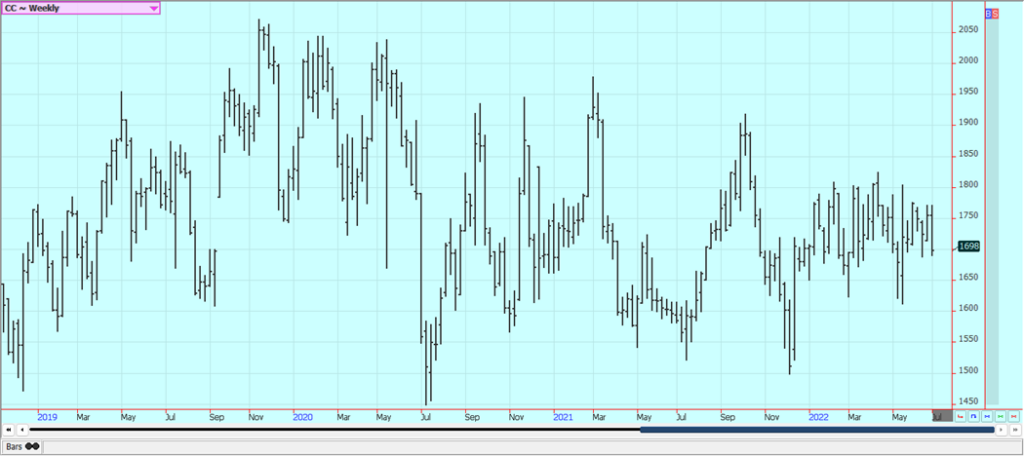

Cocoa: New York and London were lower on Friday and trends are still down on the daily charts on weak demand ideas. Selling came from ideas that a recession for the world is just around the corner. Reports of sun and dry weather along with very good soil moisture keep big production ideas alive in Ivory Coast. Some very good rains were reported last week. Ideas are still that good production is expected from West Africa for the year. The weather is good for harvest activities in West Africa. Current reports from Ivory Coast indicate that the weather is a good mix of sun and rain so a good midcrop production is expected. The weather is good in Southeast Asia.

Weekly New York Cocoa Futures

Weekly London Cocoa Futures

__

(Featured image by lightluna94 via Pixabay)

DISCLAIMER: This article was written by a third party contributor and does not reflect the opinion of Born2Invest, its management, staff or its associates. Please review our disclaimer for more information.

This article may include forward-looking statements. These forward-looking statements generally are identified by the words “believe,” “project,” “estimate,” “become,” “plan,” “will,” and similar expressions. These forward-looking statements involve known and unknown risks as well as uncertainties, including those discussed in the following cautionary statements and elsewhere in this article and on this site. Although the Company may believe that its expectations are based on reasonable assumptions, the actual results that the Company may achieve may differ materially from any forward-looking statements, which reflect the opinions of the management of the Company only as of the date hereof. Additionally, please make sure to read these important disclosures.

Futures and options trading involves substantial risk of loss and may not be suitable for everyone. The valuation of futures and options may fluctuate and as a result, clients may lose more than their original investment. In no event should the content of this website be construed as an express or implied promise, guarantee, or implication by or from The PRICE Futures Group, Inc. that you will profit or that losses can or will be limited whatsoever. Past performance is not indicative of future results. Information provided on this report is intended solely for informative purpose and is obtained from sources believed to be reliable. No guarantee of any kind is implied or possible where projections of future conditions are attempted. The leverage created by trading on margin can work against you as well as for you, and losses can exceed your entire investment. Before opening an account and trading, you should seek advice from your advisors as appropriate to ensure that you understand the risks and can withstand the losses.

Blockchain Adoption Accelerates as SwissChain and Amundi Launch Tokenized Financial Solutions

SwissChain Holding SA has digitized its share certificates using blockchain, improving transparency, efficiency, and ownership tracking while maintaining Swiss legal...

Cocoa Markets Steady as Weak Demand and Rising Supply Signal Potential Surplus

New York and London markets higher range trading, with mixed short term trends. Strong West African harvests and favorable rains...

Global Markets on Edge as Iran Conflict, Inflation Pressures, and Financial Risks Intensify

Iran conflict threatens economy disruptions beyond energy to agriculture and goods. Rising PPI signals persistent inflation, risking stagflation reminiscent of...

The Iran War Tests Bitcoin and Crypto Market Resilience

The Iran war has driven oil prices higher and disrupted crypto markets. Bitcoin rose despite volatility, while mining activity declined....

Italy’s Pharmaceutical Sector Drives Innovation, Sustainability, and European Leadership

Italy’s pharmaceutical sector invests €4 billion annually, including €2.3 billion in R&D and €1.7 billion in industrial technologies, up 21%...

|

|

|  |

|

|

-

Crypto5 days ago

Crypto5 days agoBlackRock’s $94M Crypto Move Signals Rising Institutional Momentum

-

Crypto2 weeks ago

Crypto2 weeks agoXRP vs Solana ETFs: Retail Hype Meets Institutional Interest

-

Fintech1 week ago

Fintech1 week agoSwiss Fintech Sector Enters Maturity as AI and Infrastructure Take the Lead

-

Impact Investing2 weeks ago

Impact Investing2 weeks agoIntegrated Energy Solutions Boost Profitability and Cut Emissions in Italy’s Decarbonization Efforts