Featured

US Cotton Futures Were Higher as USDA Report Showed Increased Demand

Cotton futures were higher on-demand ideas as USDA showed another strong week of export sales and as the US Dollar Index turned weaker. Demand for US Cotton remains very strong and that is good news for sellers as the strong demand implies strong prices should continue. Analysts say the Asian demand is still very strong and likely to hold at high levels for the future.

Wheat: Wheat closed mixed on Friday and trends are still up in all three markets. The markets were all higher for the week. Minneapolis Spring Wheat was the leader and is in a post-harvest rally that has been very impressive. Ideas that the US will have good demand for Wheat as the rest of the northern hemisphere is short production this year. Offer volumes are down from both Russia and Europe. Dry weather in southern Russia as well as the northern US Great Plains and Canadian Prairies remains a supportive feature in the market although the weather has become old news. The Russian weather has been good for production in northern and western areas and is finally starting to improve in southern areas and into Kazakhstan in time for the next crop. Siberian Spring Wheat conditions have been very good. Europe is expecting top yields in some areas but less yield in others and parts of eastern Europe and northern Russia are expecting strong yields. European quality is a problem due to too much rain in some areas and not enough in others. Speculators keep talking about inflation and are buying commodities for an inflation trade.

Weekly Chicago Soft Red Winter Wheat Futures

Weekly Chicago Hard Red Winter Wheat Futures

Weekly Minneapolis Hard Red Spring Wheat Futures

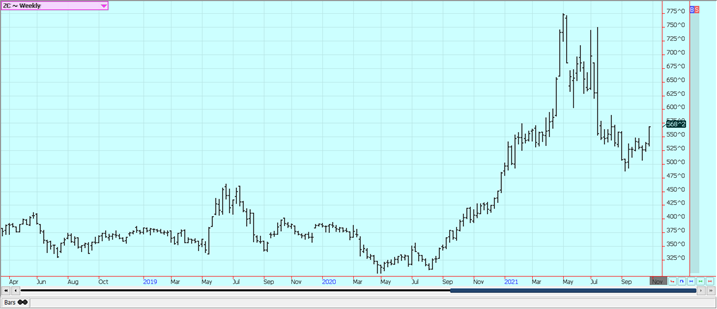

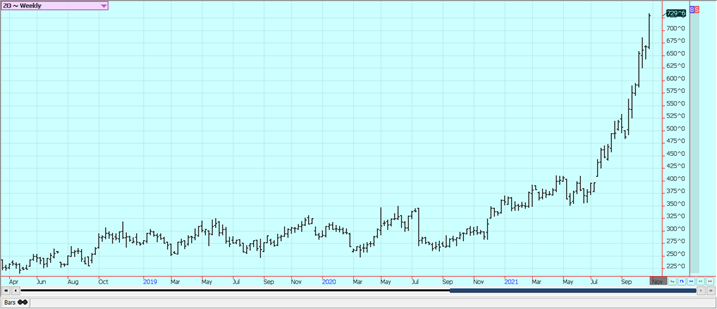

Corn: Corn and Oats closed higher on Friday and for the week. Oats were higher on a lack of supply available to the market from the northern US Great Plains and the Canadian Prairies while Corn is still finding some support from strong ethanol demand. Export demand was not strong last week but has been improved in recent reports. Trends are up on the daily and weekly charts for both markets. Traders keep talking about new demand for the market from exporters and noted that the demand for ethanol production was very strong. Demand will be an increasing feature in the trade moving forward as the harvest moves to completion sometime next month. Initial yield reports have been mixed but good, with some lower yields reported due to disease but some higher than expected yields reported in western areas. Farmers are reported to be limited sellers at best. Most of the elevators along the Mississippi are exporting again which is good news for nearby demand. There are a lot of ideas that production and planted and the harvested area will be significantly less next year due to the lack of fertilizers available and the cost of production. The Oats market knows that supplies will continue to be tight due to a drought in the northern Great Plains and Canada. There will not be much in the way of high-quality Oats for consumers to buy in the coming year.

Weekly Corn Futures

Weekly Oats Futures

Soybeans and Soybean Meal: Soybeans closed higher last week but the products were mixed, with Soybean Oil lower and Soybean Meal higher. The weekly charts imply that Soybeans are constructing a harvest low right now. Ideas of strong demand from China were supportive but there were only two sales announcements last week and the weekly export sales report was less than trade expectations. Mexico also bought US Soybeans. The weekly charts still show downtrends for all three markets, and the daily chart trends are mixed. Harvest has moved past the halfway point for Soybeans and a harvest low might be seen during the second half of the harvest. However, the low will probably not be as low as the previous low seen a few weeks ago. Reports indicate that farmers are limited sellers at best. Gulf port elevators are coming on line and export sales and exports are increasing. Planting and initial crop development is going very well in Brazil. It has been dry in Argentina and panting could be slower there when the time comes.

Weekly Chicago Soybeans Futures:

Weekly Chicago Soybean Meal Futures

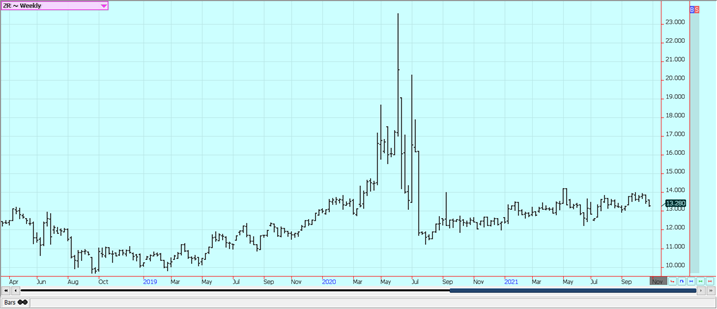

Rice: Rice was a little lower in consolidation trading on Friday and a little lower for the week. Short-term down trends are on the charts but the chart show limited potential for more selling to be effective and ideas are that a bottom could come with the current test of support. Weekly chart trends are sideways to down. Ideas are that demand is not yet strong enough to take up the supply available to the market. The crop has been largely harvested in all states. Yield reports and quality reports have been acceptable to many in Texas and are called good in Louisiana. The reports have been good in both Arkansas and Mississippi although there have been some milling problems as milling yields have been generally low.

Weekly Chicago Rice Futures

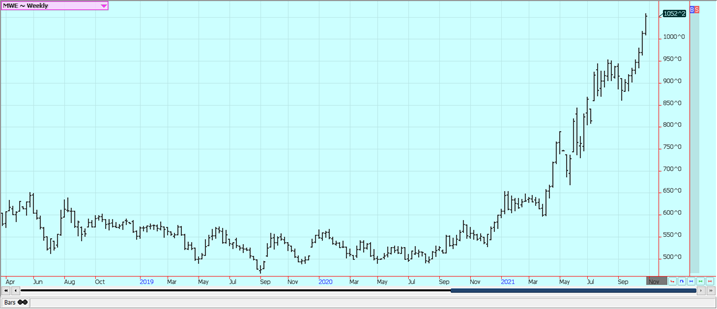

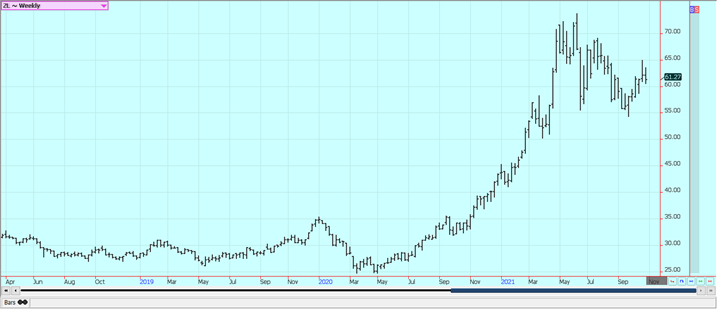

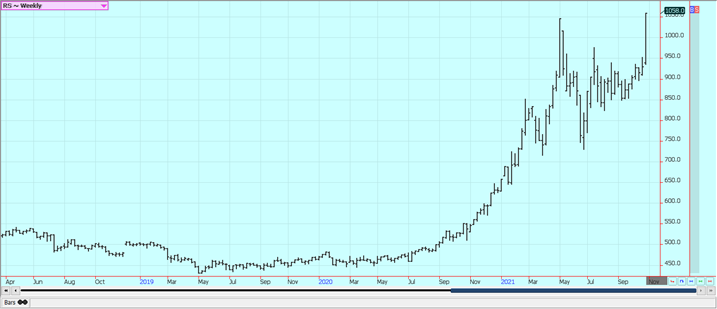

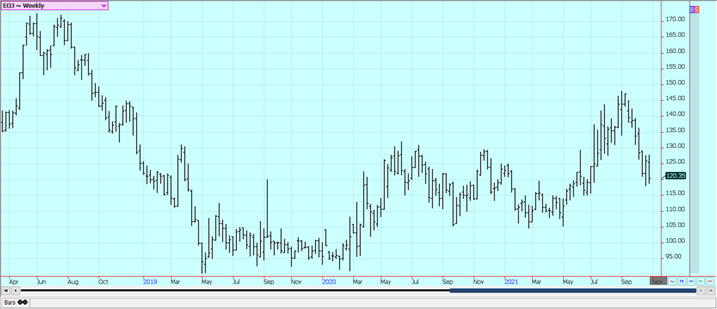

Palm Oil and Vegetable Oils: World vegetable oils prices were higher again last week except for Soybean Oil which was a little lower. Palm Oil was higher for the week even with slow exports as reported by the private services. Support still comes from ideas that supply and demand are in balance or supplies are short. India was the major importer as the country reduced import taxes. It has also reduced import taxes now for Soybean Oil and Canola Oil and this has caused some demand worries for Palm. The weekly chart trends are up. There are ideas of tight supplies due to labor problems. There are just not enough workers in the fields due to Coronavirus restrictions. Production has also been down to more than offset the export losses so prices have trended higher. Canola closed higher for the week as the harvest is starting to wind down. Farmers are bullish and reluctant to sell and would rather work in the fields. The weekly chart trends are up. The Prairies crops are in big trouble now due to previous hot and dry weather.

Weekly Malaysian Palm Oil Futures

Weekly Chicago Soybean Oil Futures

Weekly Canola Futures:

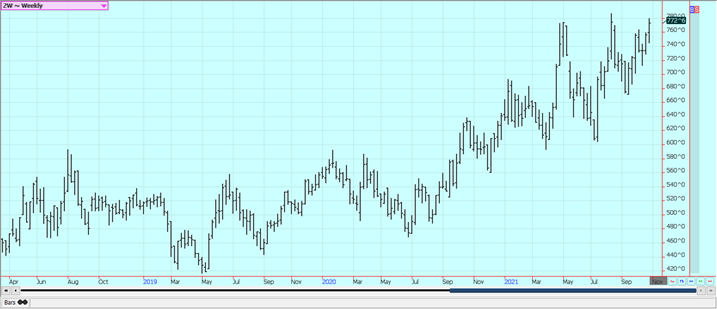

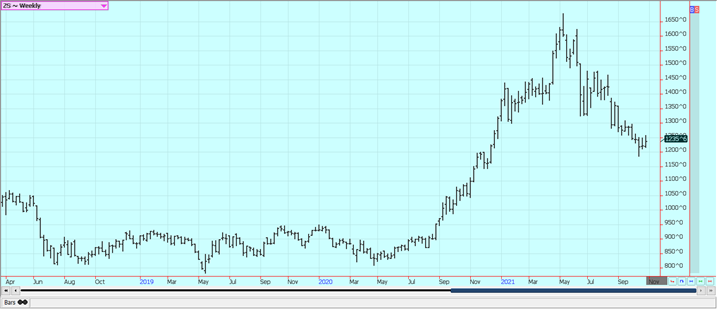

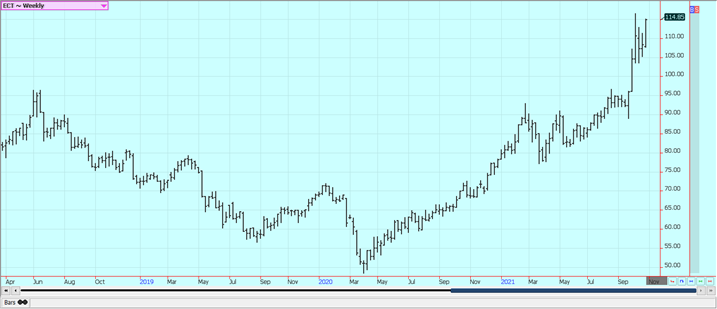

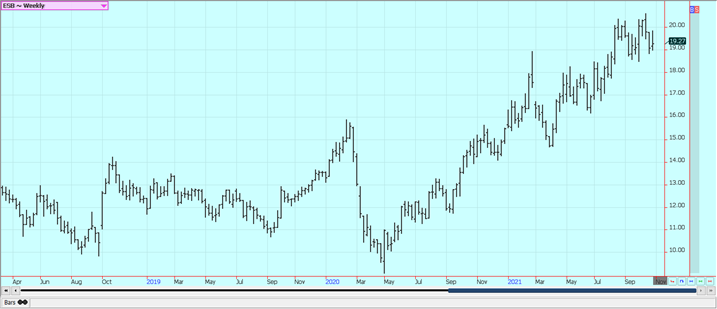

Cotton: Futures were higher on-demand ideas as USDA showed another strong week of export sales and as the US Dollar Index turned weaker. Demand for US Cotton remains very strong and that is good news for sellers as the strong demand implies strong prices should continue. Analysts say the Asian demand is still very strong and likely to hold at high levels for the future. Good US production is expected. Chinese demand is also strong as clothes makers use foreign Cotton to get away from domestic supplies that might have been produced by forced labor and might not be allowed in the US or other western countries

Weekly US Cotton Futures

Frozen Concentrated Orange Juice and Citrus: FCOJ was lower last week and chart trends are starting to turn down. Reports indicate that the selling came from speculators. The hurricane season is just about over and the chances for a damaging storm to hit the state of Florida are almost nothing. The weather remains generally good for production around the world. Brazil has some rain is in the forecast and flowering will be possible in the next couple of weeks. Weather conditions in Florida are rated mostly good for the crops with a couple of showers and near-normal temperatures. Mexican crop conditions in central and southern areas are called good with rains. Northern and western Mexico is rated in good condition.

Weekly FCOJ Futures

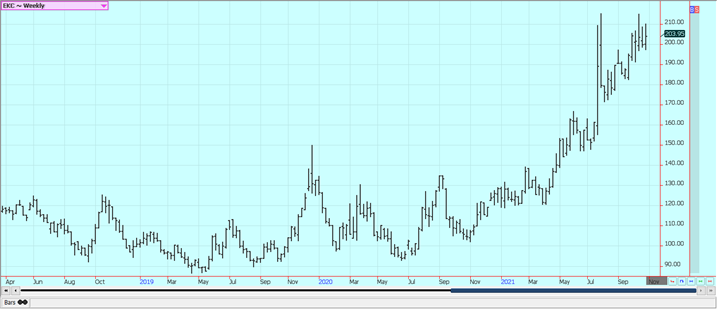

Coffee: New York and London closed higher on Friday and for the week as the lack of Coffee available to deliver against Robusta contracts remains a factor. London was the leader to the upside last week. Some major storms hit Vietnamese Coffee areas and containers are not available in Vietnam to ship the Coffee. Roasters are turning to exchange stocks and are buying futures contracts to get in line for deliveries. The lack of Coffee and freight to move the Coffee that is available is still supporting futures and for now especially the futures market in London. New York and London are both having trouble sourcing Coffee from any country due to a shortage of containers to carry the Coffee out of the origin country. Scattered showers are still in the forecast for Brazil and flowering is being reported now in many growing areas. Scattered showers are now in the forecast for Southeast Asia and for Vietnam now as the tropical storms have passed. Good conditions are reported in northern South America with above-average rains and good conditions reported in Central America with near-average rains. Conditions are reported to be generally good in parts of Africa. Chart trends are mixed on the daily charts but weekly London charts show up trends.

Weekly New York Arabica Coffee Futures

Weekly London Robusta Coffee Futures

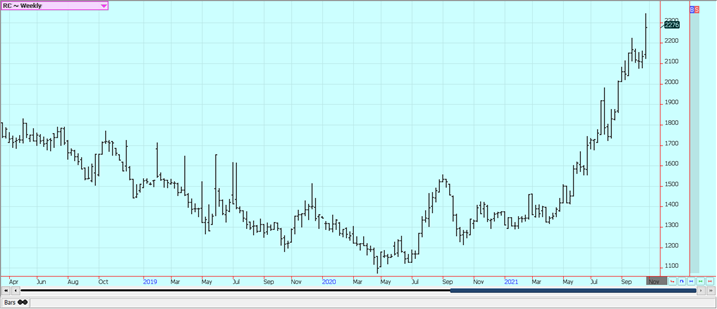

Sugar: New York and London were higher last week as the market tries to hold at current trading levels. Weekly charts show mixed trends but the daily charts show potential downtrends developing. Ideas are that the supplies are out there but it will take a stronger price to get them into the market. UNICA showed less overall Sugarcane processing and much less Sugar production for the two-week period. Processors are refining the cane for Ethanol more than Sugar right now and Unica expects this trend to continue. New York was the weaker market on improved weather conditions for the net Sugarcane crop in Brazil. The reduced production potential from Brazil for the current harvest is still impacting the market. India is not offering as world prices are well below domestic prices and has had some weather problems of its own. Production is now estimated at 30.5 million tons by a producers group there, down 1.6^ from earlier industry estimates. Consumption of Sugar is said to be improving from previous low levels but still remains rather low. Thailand is expecting improved production. It is raining in southern Brazil which will be good for the next crops there.

Weekly New York World Raw Sugar Futures

Weekly London White Sugar Futures

Cocoa: New York and London closed lower as chart trends started to turn down. Trends are sideways on the daily charts for New York. Ideas are that demand will only improve slightly and production in West Africa appears to be good this year. Both Ivory Coast and Ghana are reporting improved weather as it is now mostly sunny with some scattered showers around. Arrivals at Ivory Coast ports are now down 15.3% at 277,000 tons. World economies are starting to reopen after Covid and the open economies are giving demand the boost.

Weekly New York Cocoa Futures

Weekly London Cocoa Futures

—

(Featured image by isaaakc via Pixabay)

DISCLAIMER: This article was written by a third party contributor and does not reflect the opinion of Born2Invest, its management, staff or its associates. Please review our disclaimer for more information.

This article may include forward-looking statements. These forward-looking statements generally are identified by the words “believe,” “project,” “estimate,” “become,” “plan,” “will,” and similar expressions. These forward-looking statements involve known and unknown risks as well as uncertainties, including those discussed in the following cautionary statements and elsewhere in this article and on this site. Although the Company may believe that its expectations are based on reasonable assumptions, the actual results that the Company may achieve may differ materially from any forward-looking statements, which reflect the opinions of the management of the Company only as of the date hereof. Additionally, please make sure to read these important disclosures.

Futures and options trading involves substantial risk of loss and may not be suitable for everyone. The valuation of futures and options may fluctuate and as a result, clients may lose more than their original investment. In no event should the content of this website be construed as an express or implied promise, guarantee, or implication by or from The PRICE Futures Group, Inc. that you will profit or that losses can or will be limited whatsoever. Past performance is not indicative of future results. Information provided on this report is intended solely for informative purpose and is obtained from sources believed to be reliable. No guarantee of any kind is implied or possible where projections of future conditions are attempted. The leverage created by trading on margin can work against you as well as for you, and losses can exceed your entire investment. Before opening an account and trading, you should seek advice from your advisors as appropriate to ensure that you understand the risks and can withstand the losses.

The TopRanked.io Weekly Digest: What’s Hot in Affiliate Marketing [NiftyPM Affiliate Program Review]

As any marketer (affiliate or not) can tell you, the old "it's AI-powered" line has been a real champ when...

Fes-Meknes Drives Investment Growth with Diversified Sectors and Industrial Expansion

In 2025, Morocco’s Fes-Meknes region approved 444 projects worth 17.85 billion dirhams, creating over 18,500 jobs. Investment focused on energy,...

Peru’s Crowdfunding Sector Shrinks Amid License Revocation

Peru’s securities regulator revoked Inversiones Neurona SAC’s crowdfunding license at the company’s request, following compliance checks. Previously suspended for failing...

EU Biotechnology Law Aims to Boost Innovation and Cut Trial Delays

EU Commissioner Olivér Várhelyi proposed a Biotechnology Law to boost competitiveness, cut clinical trial times, and reduce fragmentation. Measures include...

BlackRock’s $94M Crypto Move Signals Rising Institutional Momentum

BlackRock transferred nearly $94 million in Bitcoin and Ethereum to Coinbase, signaling possible trades and rising institutional interest. Ethereum surged...

|

|

|  |

|

|

-

Biotech1 week ago

Biotech1 week agoEvotec Stock: Turnaround Opportunity or High-Risk Biotech Bet?

-

Markets5 days ago

Markets5 days agoOil Surge Sparks Market Turmoil and Shadow Banking Fears

-

Business2 weeks ago

Business2 weeks agoEchoes of 1929: Inflated Valuations and Warning Signs in Today’s Dow

-

Fintech3 days ago

Fintech3 days agoPayPay Targets Global Expansion After Landmark IPO