Featured

On our way to a recession? Markets plunge after rallying

It was the week of the Fed. We take a look back at its origins on Jekyll Island and a small look at how the Fed works.

The Fed surprised with its dovish statement. Stock markets rallied then plunged. Some interest rates and interest rates have turned negative signaling a potential recession. Nonetheless our closely watched ‘’Recession Spread’’ remains positive so any recession remains months away. We look at household debt and corporate debt to GDP in our “Chart of the Week.’’

Gold continues to meander and the US$ Index appears poised to go higher. Stock markets could have a rough week following Friday’s drop and volatility picked up. We define the breakdown points.

The Creature from Jekyll Island

“The Creature from Jekyll Island”— that is what the Federal Reserve is known as in some circles. The name comes from a book called, of course, The Creature from Jekyll Island by G. Edward Griffin. The book is a favorite of libertarians, conservatives, and conspiracy theorists because it claims that the Fed is the root of all evil, given its ability to finance wars, spark economic booms, and create depressions.

So, what is Jekyll Island? In 1910 a group of old-boy American financiers met on Jekyll Island off the coast of Georgia to discuss monetary policy and out of it spawned the legislation that created the central bank—the Federal Reserve. Despite the name, Jekyll Island is actually a lovely place with white-sand beaches and a beautiful landscape. Triggering the meeting was the concern over a series of financial crises that had befallen the markets.

The most noteworthy were financial panics that occurred in 1901, 1903, and 1907. But before that the U.S. and the world had gone through what was known as the “Long Depression” of 1873–1879. Actually, the “Long Depression” was two deep depressions with the golden age of railroads in the middle. There were banking panics in 1873, 1884, 1890, 1893, and 1896. The second depression ran from 1893 to 1897. Despite the depressions, the period from roughly 1870 to 1900 was known as the “Gilded Age.” Not surprisingly, wealth inequality soared during this period.

The banking panic of 1907 was a financial crisis spread over a 3-week period as the NYSE fell about 50% and there were runs on numerous banks and trusts. The panic would have been worse except for the intervention of J.P. Morgan who put up huge sums of the bank’s money to prevent a bigger collapse. The key, however, is that it led to the creation of the Federal Reserve System with the Federal Reserve Act passed in 1913.

The Fed is an independent entity. It has both private and public sector characteristics. It is divided into 12 regional banks that act like private banks to represent the diverse regions of the U.S. The President and Congress approve all members of the Federal Reserve Board of Governors. The President appoints the Federal Reserve Chair, currently Jerome Powell, but the Chair reports to Congress, not to the President. That is why the President would have a very difficult time firing the Chair of the Fed. The Board is an independent agency and, as such, its decisions do not have to be approved by either the President or Congress.

Other central banks around the world, including Canada, are also independent and they too do not require approval from elected officials. The Bank of Canada is a privately-owned crown corporation with all of its shares owned by the Minister of Finance. While the Deputy Minister of Finance sits on the board, he does not have a vote. The Bank of Canada does provide reports to Parliament. The Governor of the Bank is appointed by the Prime Minister (PM); however, the position does not report to the PM.

The Fed does not receive funding from Congress. Instead, its funds come from its investments acquired as a result of open market operations. The Federal Reserve banks are required to maintain reserve requirements. They can borrow from each other at the fed funds rate. They can also borrow at the discount window at the discount rate. To be a member of the Federal Reserve System commercial banks must own stock. The stock cannot be traded but they are mandated by law to pay the owners of the stock 6% even as all profits must be returned to the U.S. Treasury. The commercial banks that are members of the Federal Reserve system are some of the biggest names in global banking.

The Fed is responsible for monetary policy through three tools: open market operations, the discount rate, and reserve requirements. It is responsible for helping to maintain a healthy economy and full employment, and to keep inflation in check. Through open market operations, the Fed buys and sells securities. Hence the huge role the Fed played in the 2008 financial crisis even as its balance sheet ballooned from $800 billion to $4.5 trillion. Quantitative easing (QE) was open market operations on steroids.

The Fed (FOMC) has 12 members. Seven are appointed governors including the Chairman, the president of the New York Fed, with the remaining four coming from the other eleven Federal Reserve banks on a rotating basis. The FOMC meets eight times a year, the most recent being March 19–20, 2019. Currently, there are two vacancies. This past week, President Trump nominated economist Stephen Moore to the Fed Board of Governors to fill one of the vacancies. Moore is an outspoken critic of Jerome Powell and a close colleague of Larry Kudlow, President Trump’s economic advisor. Moore has been an outspoken critic of the Fed’s interest rate policy. Assuming he is approved by the Senate, Mr. Moore would still only be one vote amongst 12.

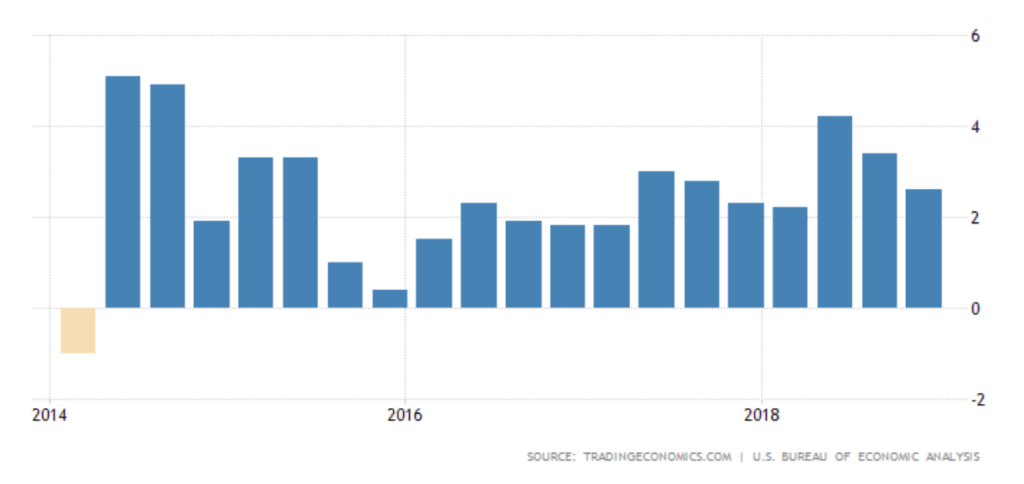

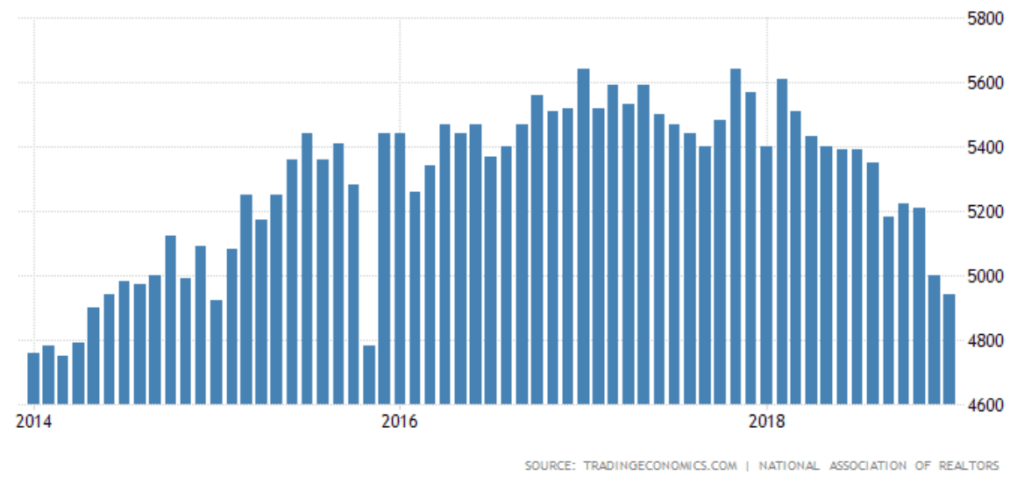

This past week was dominated by the Fed. The Fed surprised many with its dovish report. The Fed surprised when it stated it had no plans to raise interest rates further in 2019. The Fed is concerned about the potential effects of Brexit, a slowing global economy, particularly in the EU, Japan, and China, possible collapse of ongoing trade talks with China, and even some signs of slowing in the U.S. A recent quarterly GDP numbers bear out signs of a slowing economy. Existing home sales have been sliding for months although new home sales have been mixed. Housing starts have also generally been sliding despite a big bump in January. We note GDP and existing home sales below.

U.S. GDP growth rate quarterly

© David Chapman

U.S. existing home sales

© David Chapman

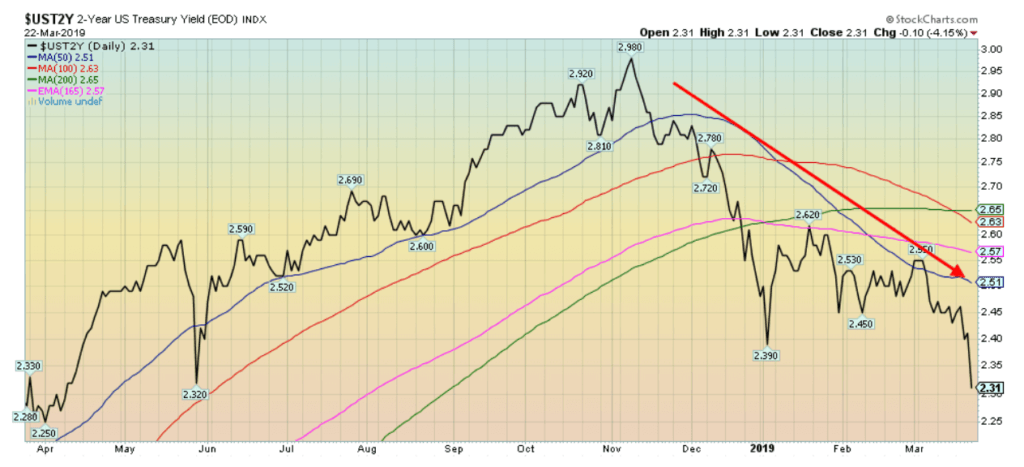

The Fed also announced they would end the drawdown of their bonds in September. What that means is that quantitative tightening (QT) will be no more. The markets reacted. After some hesitation, stocks took off. Gold took off at first but when the U.S. dollar bounced back gold sold off. Yields fell and—no surprise—the 2–10 spread narrowed further. (See under Recession Watch Spread Page 15.) The 2-year U.S. Treasury note has been in a downtrend now since peaking last November. The 2-year has, in some respects, been leading the market towards the dovish stance of the Fed.

© David Chapman

Other central banks chimed in their concern about the slowing global economy as well. The United Kingdom is careening towards a no-deal Brexit—or maybe they will get lucky and get an extension. Nonetheless, Theresa May’s tenure as PM seems to be slip-sliding away. No matter what happens, Brexit is a disaster. That the Fed is ending its rate hikes came as a surprise because it was only in December 2018 that they suggested two more rate hikes in 2019. Now, none.

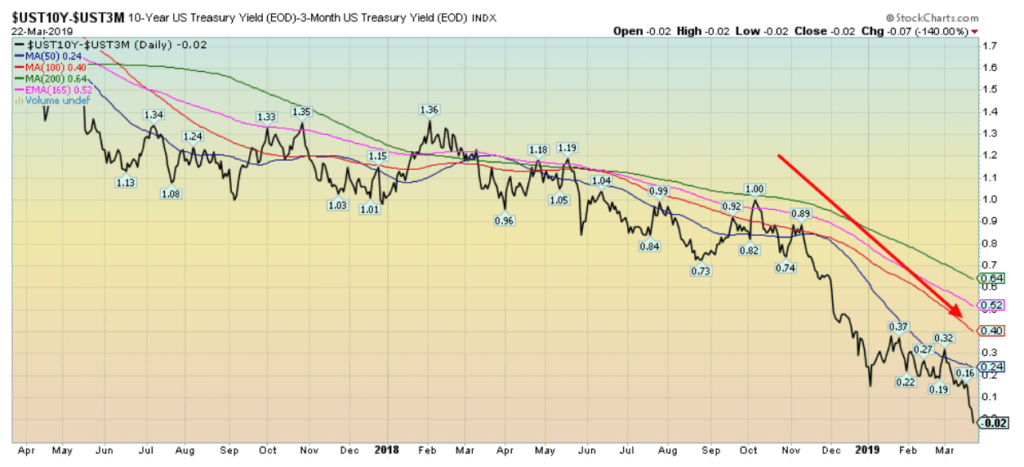

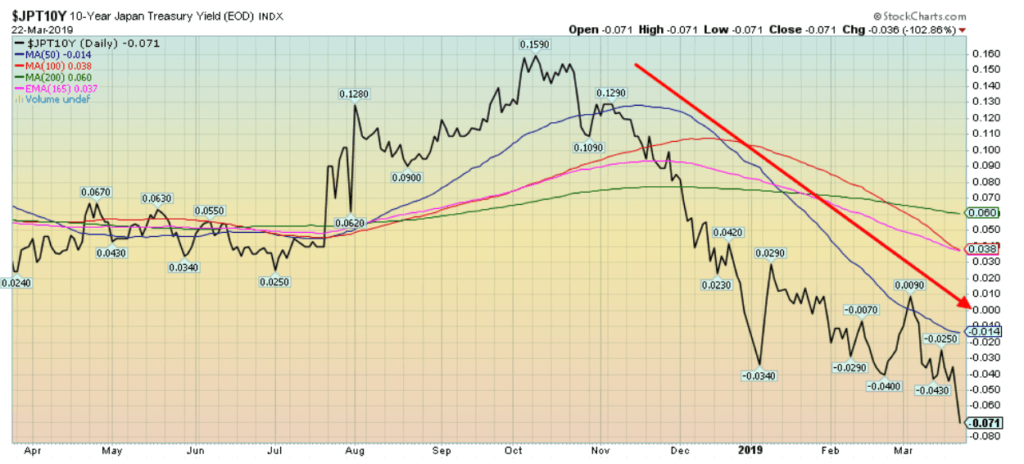

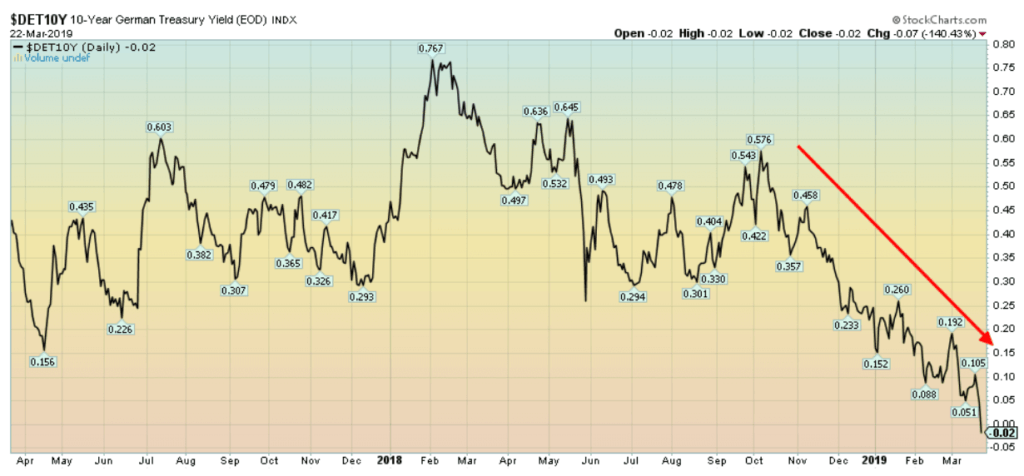

Our suspicion is that the Fed knows the global economy is headed for a hard landing but they can’t say that. Friday’s sharp down day in the stock market was a response to signs of a slowing global economy and that the 10-year Japanese Government Bonds (JGBs) and the 10-year German bund all went negative. As well, we note the 3-month Treasury bills – 10-year U.S. Treasury note spread turned negative. While these are negative signs, remember we are still early and, in the past, there were at least 6 months of negative spreads before the economy turned down into a recession. The well-followed 2-year—10-year spread remains positive, but did turn down again this week.

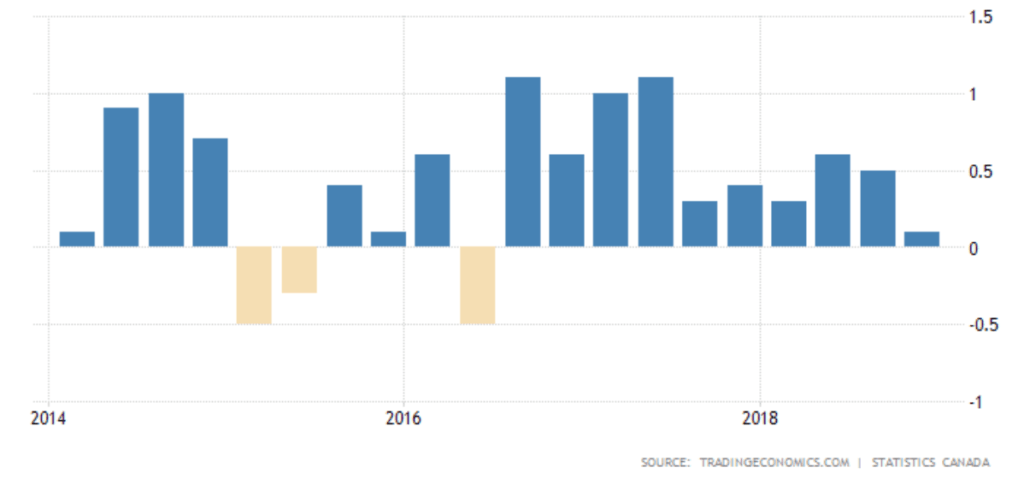

For the record, Canada is also slipping as the GDP monthly chart shows below. So, a potential slowdown is not just limited to the EU, Japan, and China. It is spreading in North America as well. But these things take time. And a reminder that in a slowing economy that’s when the accidents occur in the form of a fund going bust, a large dealer in trouble, or a bank in trouble that could spread. A major “black swan” event is most likely months away, but things can change fast.

A reminder that coming out of the 2008 financial crisis the world embarked on a period of ultra-cheap money, and a massive provision of liquidity through QE. The result was a roaring stock market that may not be finished yet and a world engorged on debt as global debt leaped from roughly $140 trillion in 2008 to $250 trillion today. In a financial collapse, it is always about debt collapse. And, no, “this time is not different.”

In any case, we’ll always have the Creature from Jekyll Island. But will he and the other central banks be able to save the day once again?

Canada GDP growth monthly

© David Chapman

Markets and trends

![]()

*New highs/lows refer to new 52-week highs/lows. © David Chapman

© David Chapman

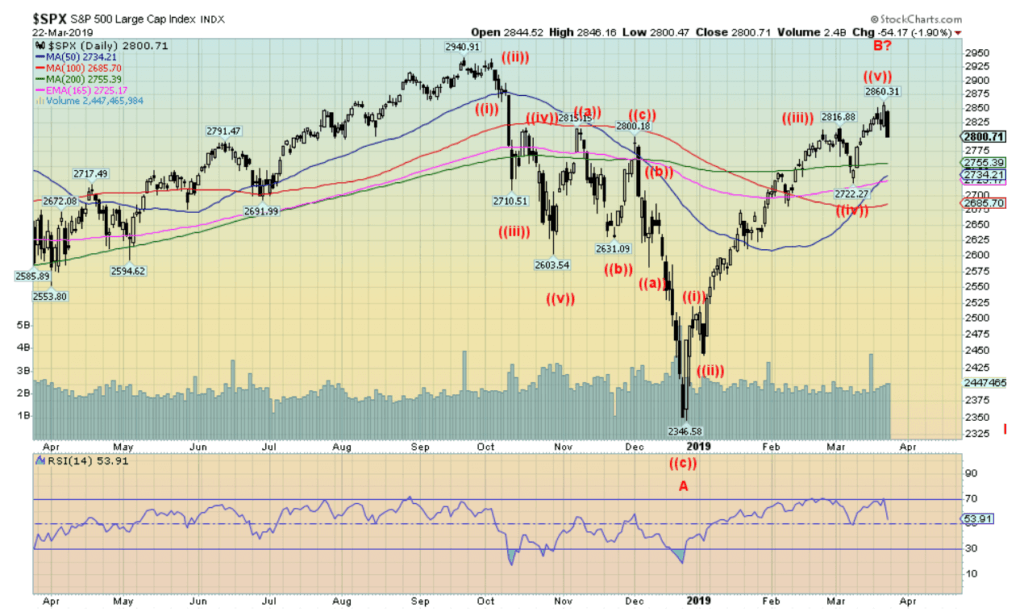

On Thursday, stock markets appeared poised to take off as both the S&P 500 and the NASDAQ leaped to new highs for the current move. Stock indices were responding positively to the Fed’s dovish stance of no further rate hikes and the end of QT in September 2019. On Friday, that was all reversed as a spat of economic numbers from Germany, in particular, were weak, Brexit appeared headed for the rocks, and German and Japanese 10-year bonds went negative. The result was the Dow Jones Industrials (DJI) fell 460 points (1.8%) with a sharp uptick in volatility.

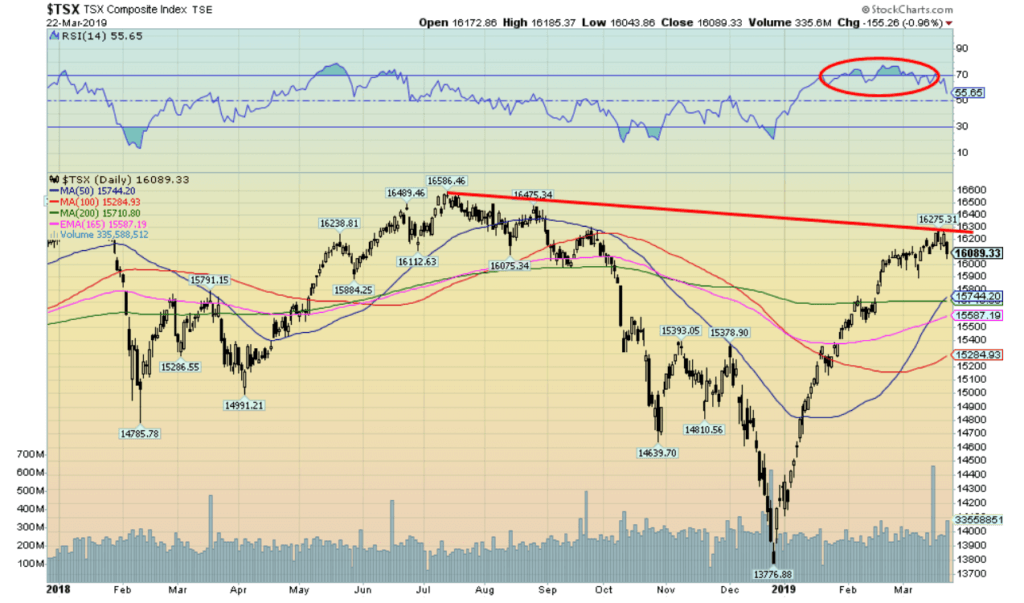

So, what happened with the run to new all-time highs? It hit a bump. Time will tell whether this is a fatal bump or merely a forming correction to the sharp run-up seen since the lows in December 2018. On the week the S&P 500 fell 0.8%, the DJI was off 1.3%, the Dow Jones Transportations (DJT) was hit hard falling 2.5%, while the NASDAQ dropped 0.6%. Given that both the S&P 500 and the NASDAQ hit new highs for the current move, Friday’s action constitutes a reversal day, although the highs were made on Thursday. Elsewhere, the small-cap Russell 2000 dropped 3.1%, the TSX Composite fell 0.3%, but the junior TSX Venture Exchange (CDNX) put in a positive week, gaining 1.6%.

Overseas, the Brexit-challenged FTSE 100 fell 0.6%, the Paris CAC 40 was off 0.5%, while the German DAX dropped 1.2%. Not so in Asia as China`s Shanghai Index (SSEC) gained 2.6%, maintaining its recent positive run, and the Tokyo Nikkei Dow (TKN) was up 1.5%. The MSCI World Index was off by a small 0.5%.

So, what to make of the reversal of fortune seen on Friday? Expect the volatility to continue into next week. And it is probable that the indices will fall further. There is considerable support for the S&P 500 between 2,700 and 2,750. A break below 2,700, while giving off potential sell signals on the daily charts is not necessarily a fatal move. Of bigger concern would be a break under 2,600, and below 2,450 new lows could loom.

The break for the S&P 500 over 2,825 was supposed to signal a potential move to new all-time highs. However, the breakout was not confirmed by the DJI nor the DJT. The NASDAQ broke as well to new highs for this move. This divergence has, for the moment at least, shifted the focus to the downside. Does this mean the market is finished and we are doomed to crash to new lows? No, it does not. The fact that some spreads went negative and the JGBs and the German bunds turned negative does not signal that a crash is about to occur. But it does signal that the first signs of a potential recession are now upon us. In the past, it has taken more than one reading of negative yields and spreads to suggest an impending recession. Most likely we are anywhere from three to six months away from that and at this point, we are not even guaranteed we’ll see a recession.

If we are correct, then this pullback would be a B wave within the context of an ABC-type move to the upside. The A wave may have peaked this past week. We note that the up wave from the December 2018 low unfolded in five waves. The B wave could take anywhere from a few weeks to a couple of months to form. Support zones are noted above but beware a breakdown under 2,450. Unsurprisingly, the sentiment at the high this past week was about 95%, meaning there were few bears about. Our guess is once this B wave is formed the indices could return to the highs and possibly see new all-time highs (the C wave). This is where we would get a number of non-confirmations between the indices and between indicators.

In the interim, fasten your seat belt. The next week or two looks a little bumpy. Support zones are noted above.

© David Chapman

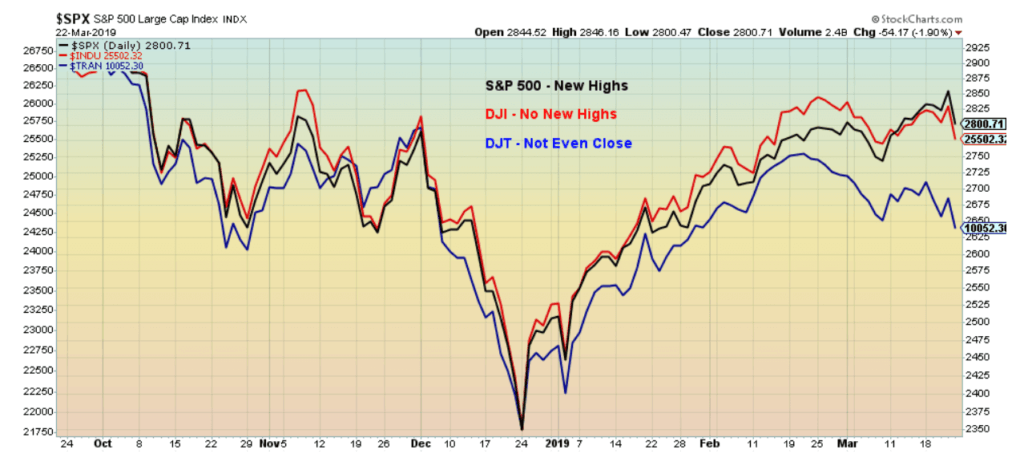

Here is the S&P 500, the DJI, and the DJT. Note how the S&P 500 made new highs but was not confirmed by the DJI. The DJT wasn’t even close. Watch the relationship between the DJI and the DJT going forward for major divergences.

© David Chapman

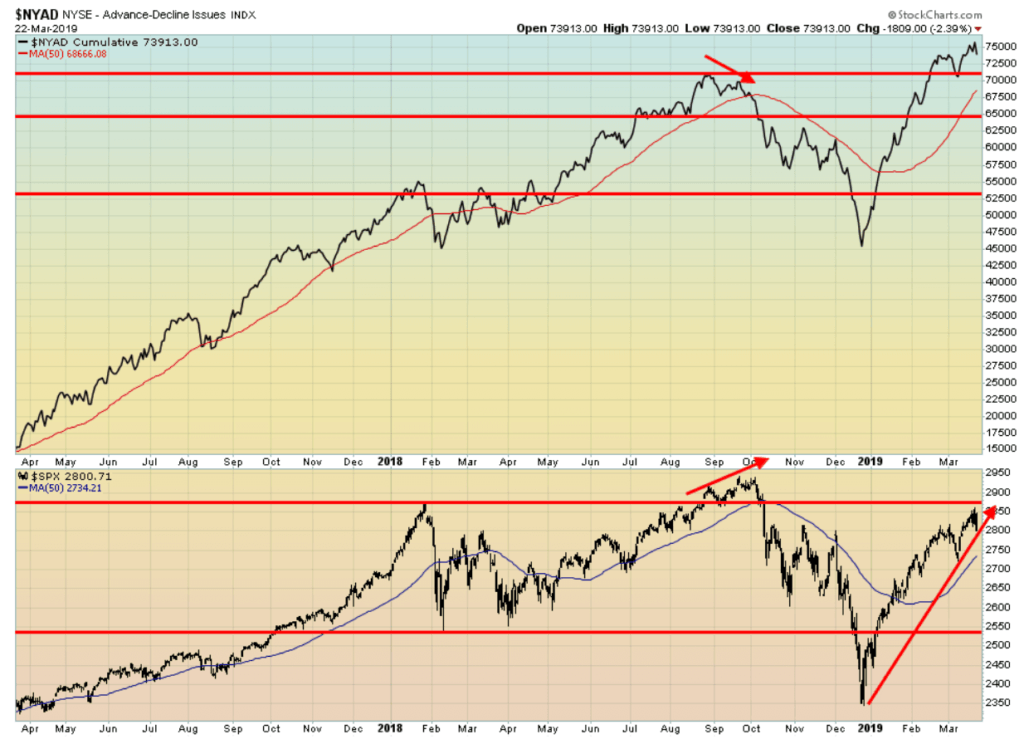

The NYSE Advance-Decline continues to fascinate. It ran to new all-time highs; however, it was not confirmed by the S&P 500 that remains short of its all-time highs. The Advance-Decline line turned down this past week with the market. What we would like to see is if the markets are headed for a corrective move, as the move on Friday would seem to indicate, then, when we go back up again, ideally, we would see the S&P 500 make new highs with the Advance-Decline line failing to make new highs. All this remains to be seen. A reminder, however, that the NASDAQ Advance-Decline line did not see new all-time highs; thus, it diverged with the NYSE Advance-Decline line.

© David Chapman

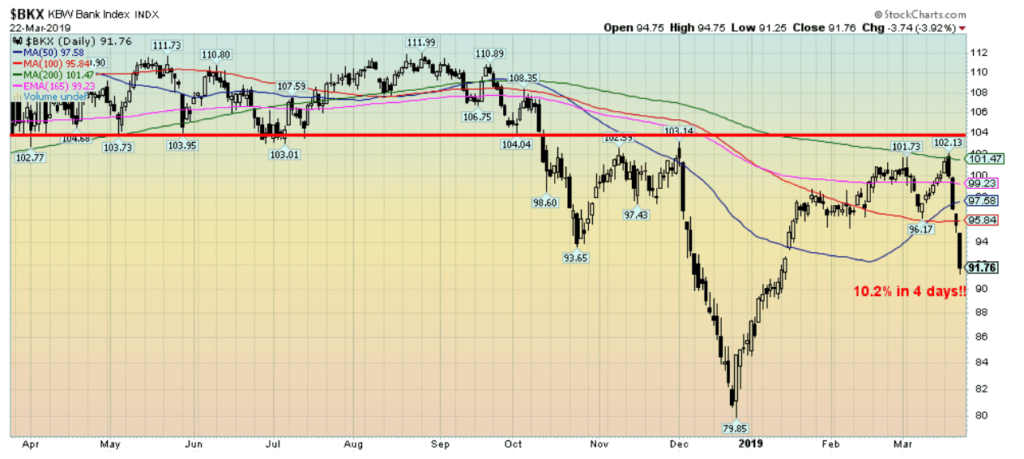

Wow! A 10.2% drop in just four days for the KBW Bank Index (BKX). It is probably no surprise that banking stocks fared the worst with the Fed’s dovish tone. If a recession is coming, it also suggests that bankruptcies and delinquencies will rise which in turn puts pressure on the Bank’s loan portfolio. As well, thoughts of lower rates also mean lower spreads for the banks. The KBW Bank Index topped way back in February 2007. The recent high in 2018 fell short of the 2007-high. We are in a world where debt has accrued exponentially since 2008 and the banks have a lot of it on their books.

We also note the KBW Bank Index was down 28.7% at its low in December 2018. That was well above the general markets’ 19% decline. The bank stocks were in a bear market. Even now they are still down 18%. Beware the banks. For Canadian banks, we note that the TSX Financials (TFS) fared better than the KBW. Unlike the KBW, the TFS saw its all-time high in January 2018 at a level well above its high of 2007. At its worst, in December 2018 it was down 17.5%. This past week the TFS fell 1.5%, nowhere near the hit the KBW took. Canadian banks are much better capitalized and while they may suffer in a downturn, the odds of one of them going under is nil. They also regularly increase their dividends.

© David Chapman

The materials dominated TSX Composite lost a small 0.3% this past week. As it has done in the past, it will follow the U.S. markets to the downside. The TSX has solid support just below 15,800 and down to 15,300. Below 15,200 would spell trouble and likely a severe test of the December low. We note the Income Trust sub-index and the Real Estate sub-index moved to new highs this past week and didn’t follow the market down. Other indices that look positive are golds, materials, and mining.

© David Chapman

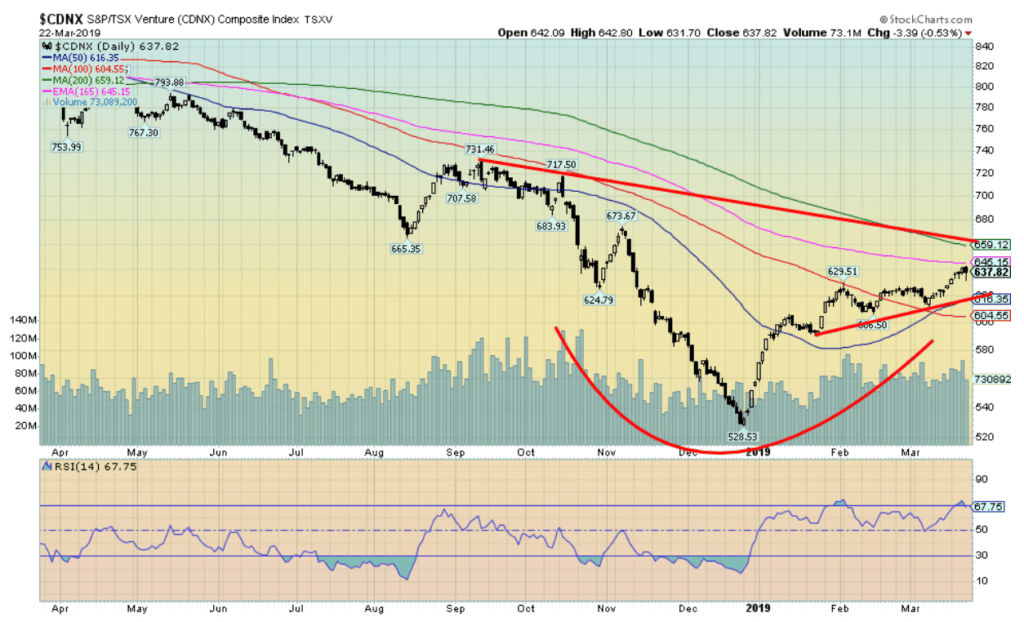

It has been some time since we showed the TSX Venture Exchange (CDNX). The CDNX is made up of roughly 50% junior mining stocks, but you would also find health care, energy, cannabis, consumer, and other stocks on the exchange. The CDNX is up 14.5% so far in 2019. Grant you, that is after a disastrous year in 2018 when the CDNX fell almost 44% from its January 2018 top. Many junior mining stocks were down even more, with some falling 90%. So, the current rally is welcomed. This may be the beginning of a stealth rally. We note the pickup in volume since this rally got underway. It has a long way to go. There is considerable resistance up to 650, but over 700 the index should perk up. Remember the CDNX can give off both great gains and great losses. After a horrible 2018, the CDNX looks poised to put in even more gains.

© David Chapman

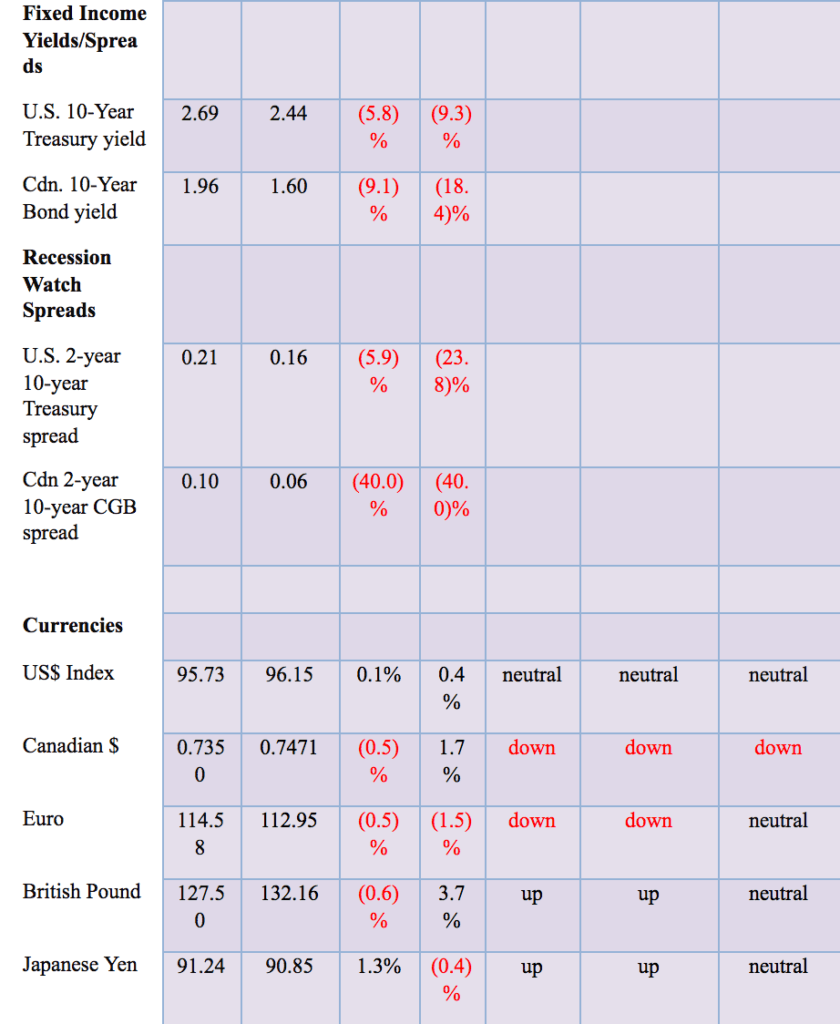

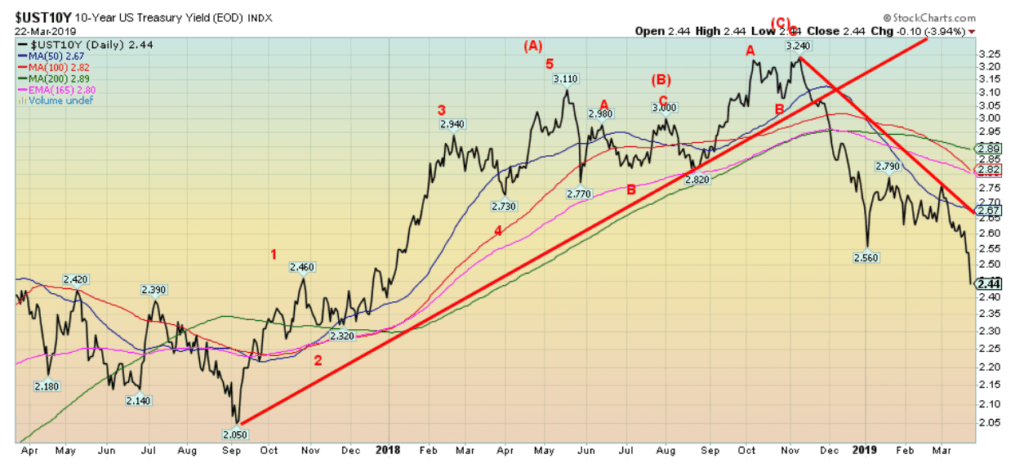

Bond yields continue to fall in the wake of the dovish tone adopted by the Fed. In some respects, given that the decline in yields got underway last October, the bond market has been leading the Fed. The question now is, is the bond market spent and will the fall in the yields will come to a halt? The daily RSI indicator has dropped below 30, a level that often signals that a low could form. It was last below when the 10-year U.S. Treasury note fell to 2.56% in December. If you have been long 10-years above 3%, then it might be time for some profit-taking. It is possible for the 10-year to fall further, but at 2.44% it is hitting a band of resistance from previous declines. Below 2.30% the 10-year could take a run at the 2017 low of 2.05%. The all-time low was seen in July 2016 at 1.37%.

Recession watch spread

© David Chapman

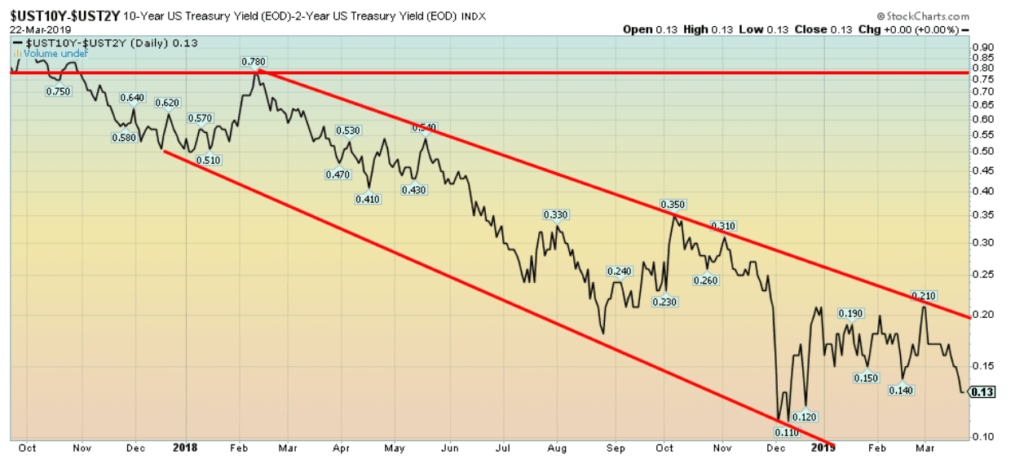

With the fall in yields this past week, our recession watch spread (10-year Treasury note minus the 2-year U.S. Treasury note) fell to 13 bp from 16 bp the previous week. Unlike some others, this spread is still not negative. It remains above its December low of 11 bp. A recession call would come when we see the 2–10 spread turn negative and remain so for at least 3 to 6 months. This spread is nowhere near signaling a recession just yet. We believe the markets will calm down and realize that their fears are overblown — at least for the moment.

© David Chapman

The 3-month U.S. Treasury bill and the 10-year U.S. Treasury note spread turned negative this past week. That had pundits jumping up and down screaming “recession” and the stock market tanked 400 points. For the record, the 3-month 10-year spread turned negative a good year or more before the start of the 2007–2009 recession. It first went negative in February 2006. The spread actually bottomed in February 2007, well before the stock market peaked in October 2007. So, the pundits’ screaming is, we believe, premature.

© David Chapman

Pundits also screamed about the JGBs turning negative this past week. They peaked at about 16 bp back in October 2018. But the JGBs have been in and out of negative now since the beginning of the year, although this is the lowest so far at negative 7 bp. The JGBs lowest was in July 2016 at negative 29 bp.

© David Chapman

The pundits were screaming even louder about the 10-year German bund turning negative. It is down sharply from a peak back in January 2018 of about 77 bp. This week’s low was at negative 2 bp. Like its Japanese counterpart, the 10-year bund was negative in 2016, hitting a low of about negative 19 bp. At the time some pundits were screaming it was the “end of the world.” Not quite. The 10-year bund recovered and hit a peak of about 77 bp in January 2018.

There have been definitive signs of a slowdown in Germany as some German economic numbers this past week were not encouraging. One of the big concerns was the manufacturing PMI falling to 44.7% in March 2019, a level well below the expectation of a reading of 48%. Export orders have been falling. PMI levels below 50 are considered recessionary. The PMI fell below 50% in January 2019 and has remained below that level ever since. Germany is also trying to engineer a merger between the deeply troubled Deutsche Bank (DB) and Commerzbank, Germany’s second-largest bank.

That would create a banking behemoth, considering Deutsche Bank is already a substantially sized bank. But the merger itself has been troubling. DB is saddled with a large number of Italian debts. Not a good place to be, considering the troubles with the Italian banking system. DB also has Russian loans and, apparently, even loans to the Trump organization. DB also has an extremely large derivatives portfolio which could prove troublesome. Could DB collapse? It has been mentioned numerous times, but its size alone brings considerable attention from both the Bundesbank and the ECB.

© David Chapman

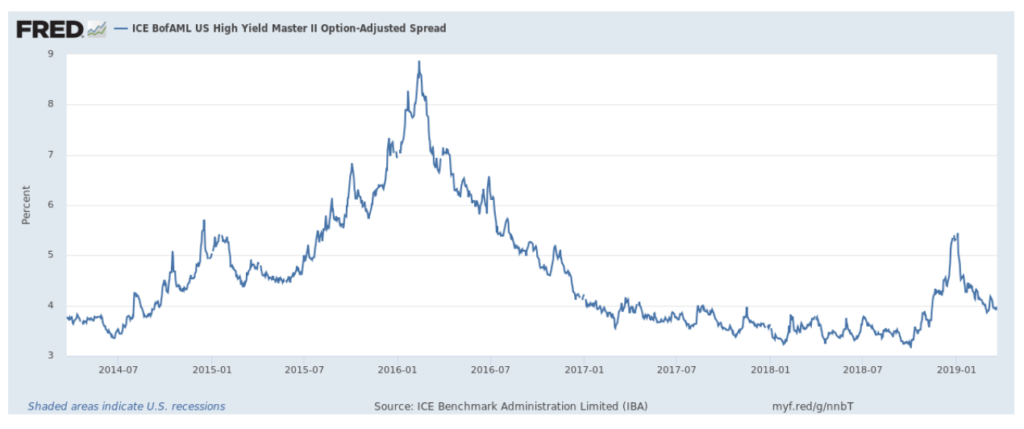

In all of the screaming over bonds and spreads turning negative, we wonder why the high-yield junk bond spread hasn’t moved higher. Maybe the current concern is overblown. Note how the spread on the high-yield junk bonds started moving higher in 2015, well before its peak in 2016. If the rise in spreads follows the path of 2015–2016, then the spread has probably bottomed and should start rising over the next few months. We’ll keep an eye on this one.

© David Chapman

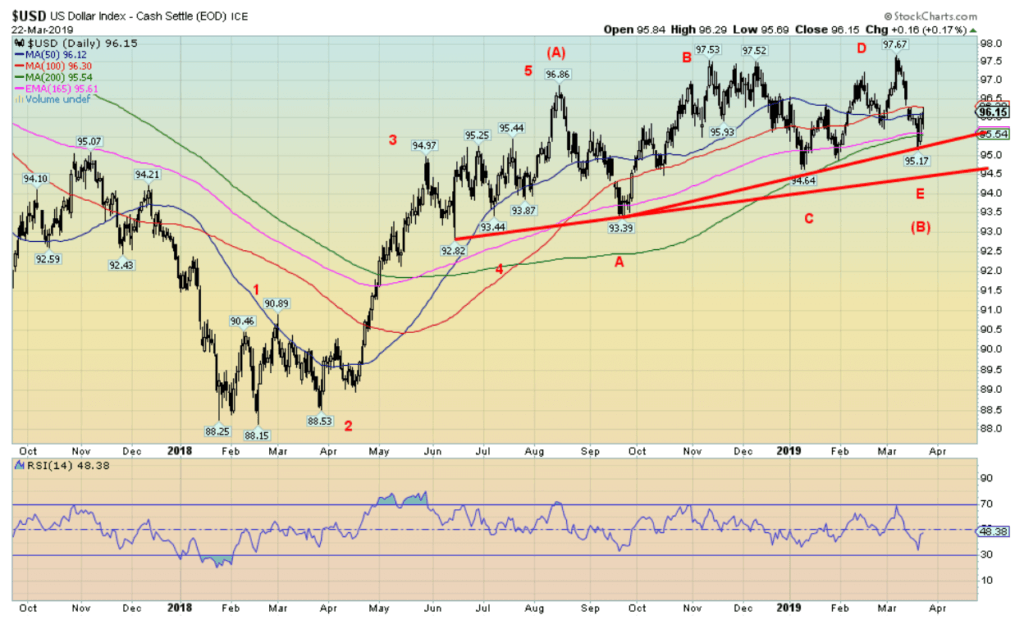

Wither the U.S. dollar? We freely admit that the past few weeks have been confusing as to the direction of the US$ Index. It looks down, but it also looks up. But that is the frustration of these type of patterns. They are complex and give off all sorts of signals, none of which seem to make sense. That line at around 95.50 seems to hold. It was tested as the index dipped down to a low of 95.17 but then rebounded and is now above 96 once again.

We note in following Elliot Wave International that they too have been fighting trying to make sense of the pattern. The best call now is that the US$ Index has made a rather complex ABCDE-type pattern, thus forming a B intermediate wave up from the low of February 2018. The A intermediate wave topped out in August 2018 labeled (A). If this is correct, then a C wave up should soon get underway. That would take the US$ Index to new highs, possibly up to around 100. Breakdown points remain at 95.50 and especially at 94.50.

The US$ Index closed higher this past week, up 0.1%. The U.S. dollar could rise against the euro, pound, and yen, largely because while the U.S. economy might be weakening its performance is still stronger than the EU, Japan, and the U.K. This past week the euro fell 0.5%, the pound sterling was down 0.6% but the Japanese Yen gained 1.3%. The Canadian dollar was weak because of signs of a weakening Canadian economy as it fell 0.5%. A breakout for the US$ Index above 96.50 would suggest another move above 97.

© David Chapman

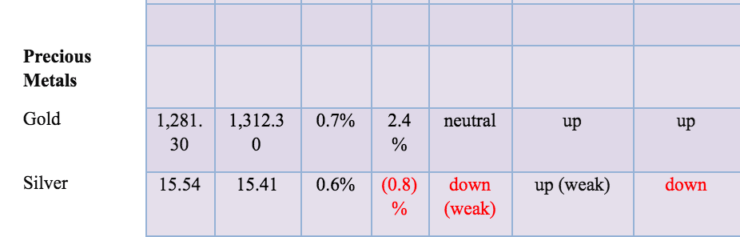

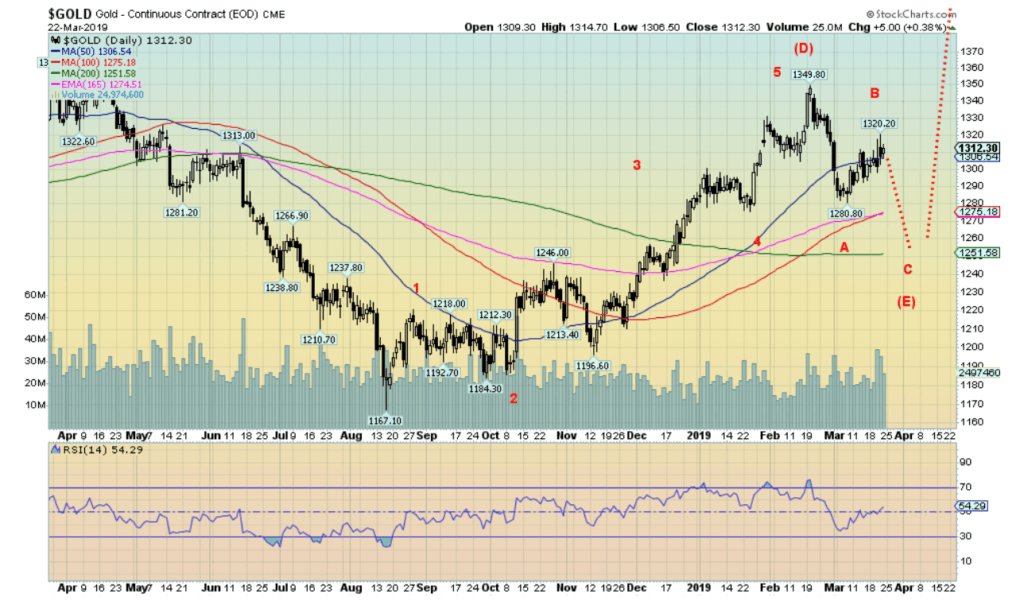

If the US$ Index were to rise as we noted that would be negative for gold. After rallying from $1,167 to a high of almost $1,350 a correction was to be expected. The A wave down took gold to a low of near $1,281. The current rebound is, we suspect, the B wave. The high so far is $1,320. Our target zone was $1,320 to $1,330 so it is possible we have topped for the moment. The C wave down could take us to $1,250. That would be in line with a rise of the US$ Index to 100. Once that wave is complete, we believe it would be the E wave of a rather complex ABCDE type correction that has been ongoing since the top in July 2016 at $1,377. Once that low is in, expected possibly by May 2019, gold should begin a powerful rally that would take it above $1,400.

Gold responded positively this past week to the dovish Fed, but Friday’s drop in the stock market saw gold only rise a small $4.40. The $1,320 to $1,330 zone is resistance, but above $1,330 a push to $1,350 would take place. Gold breaks under $1,300.

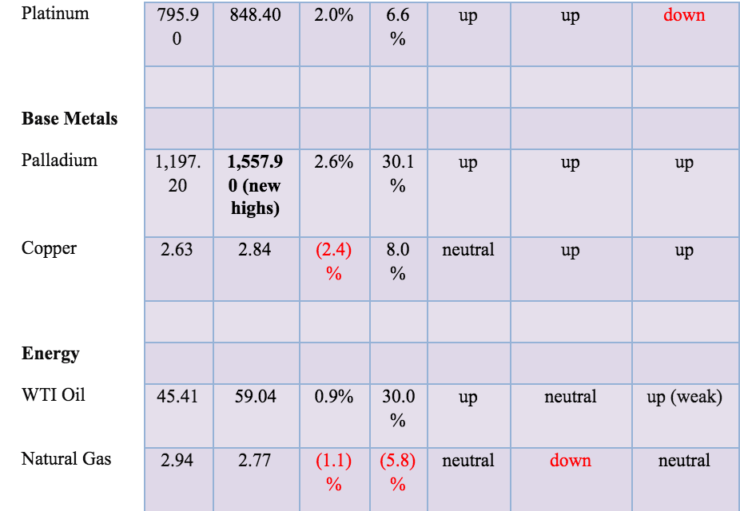

We note that platinum continues its amazing run. Once again it made new highs at $1,576.90. Gold should eventually follow platinum to the upside.

© David Chapman

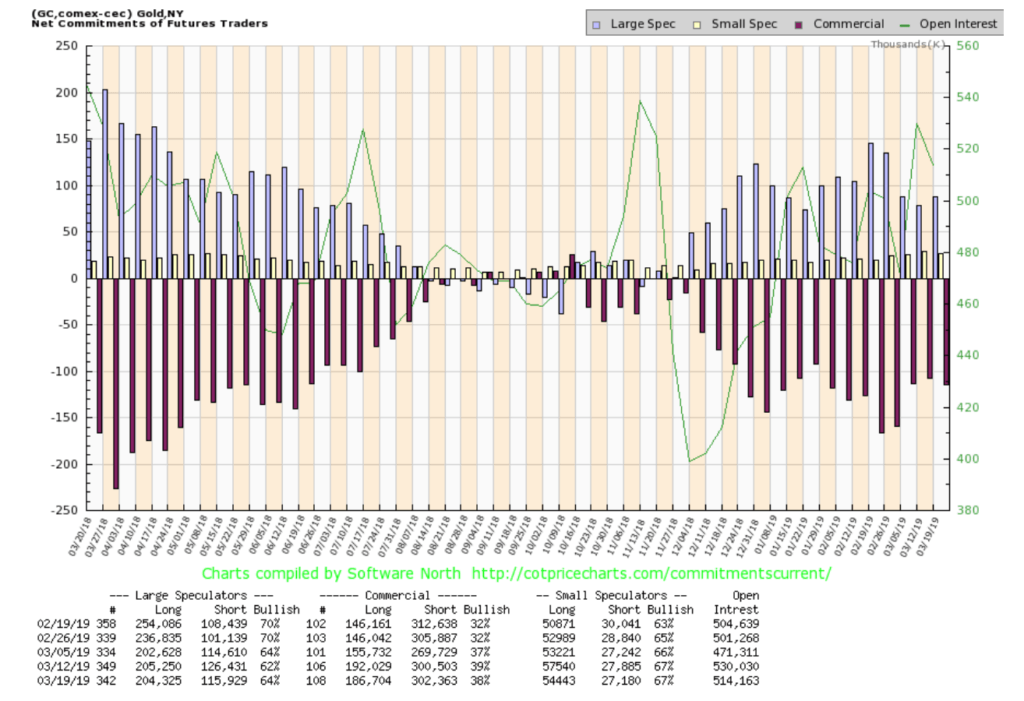

The commercial COT for gold slipped to 38% this past week from 39% the previous week. Short open interest rose about 2,000 contracts but long open interest fell around 5,000 contracts. The COT is mildly bullish. The large speculators COT (hedge funds, managed futures, etc.) rose to 64% from 62%.

© David Chapman

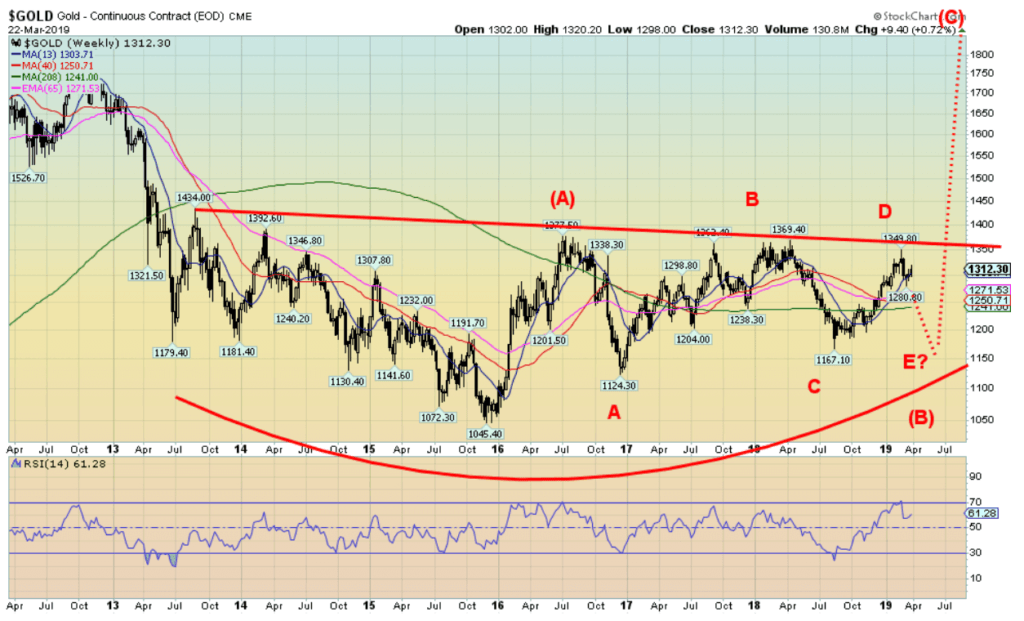

The bottom pattern forming on gold is one of the best we have ever seen. It is a very complex pattern and trying to figure it out is not particularly easy. The major breakout point remains at around $1,350. But the reality is gold would need to overhaul $1,370 to suggest a move to $1,400 and beyond. The pattern suggests potential targets up to $1,775. But first things first. We need to complete that corrective move, then start our rebound and take out $1,350 and $1,370 before we can even think about $1,400. This all breaks down if gold took out $1,167 on the downside. But we highly doubt that would occur.

© David Chapman

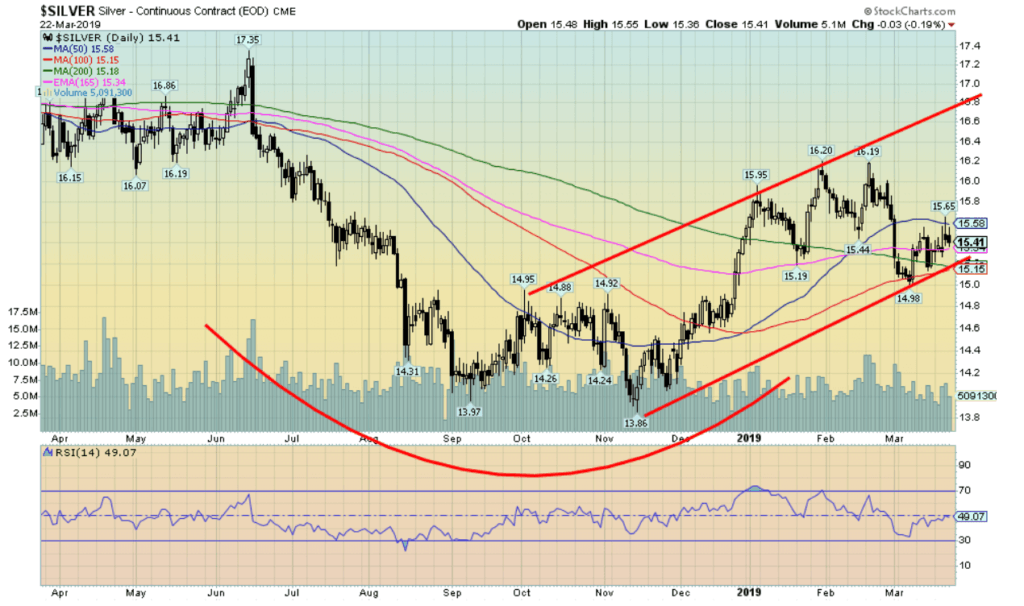

Silver remains in a nice uptrend. However, our expectation is that silver should follow gold to the downside. It would be interesting, however, if silver held the channel line and fell no further than around $15.15. If $15.15 were to fall, then a decline to the $14.30 to $14.50 zone could be underway. As with gold we expect this could be final low for silver. Silver’s breakout spot is around $16. A breakout above that zone and especially over $16.50 could suggest a move to $23.50.

© David Chapman

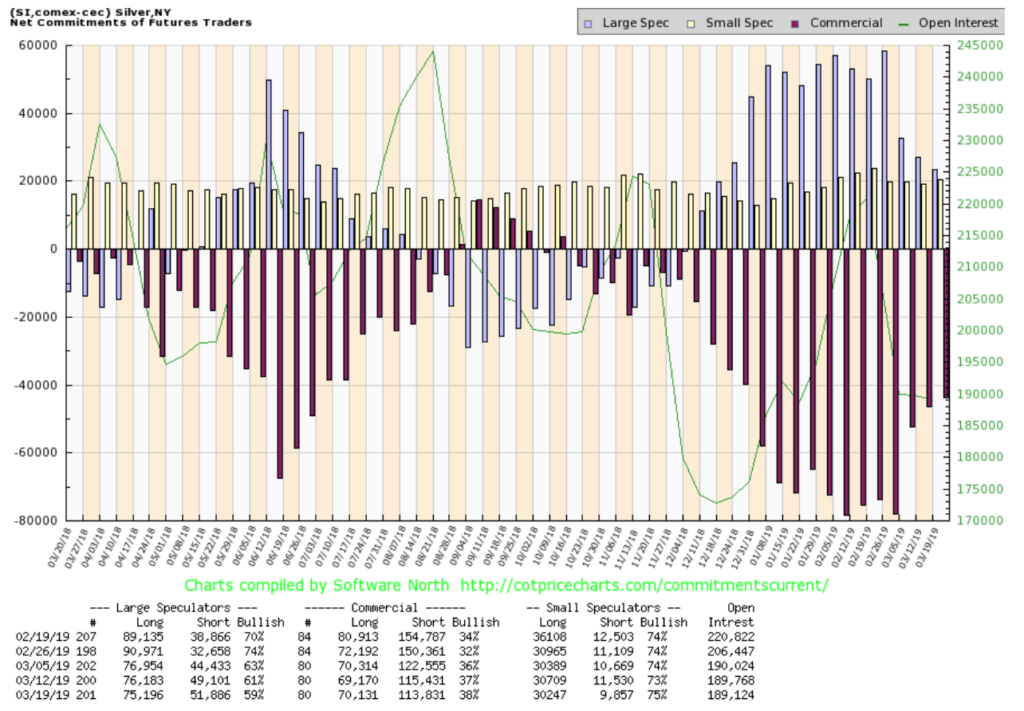

The silver commercial COT improved this past week to 38% from 37%. That has to be considered minimum movement. Long open interest rose about 1,000 contracts while short open interest fell about 1,600 contracts. As with gold, we view this as mildly bullish. The large speculators COT fell to 59% from 61%.

© David Chapman

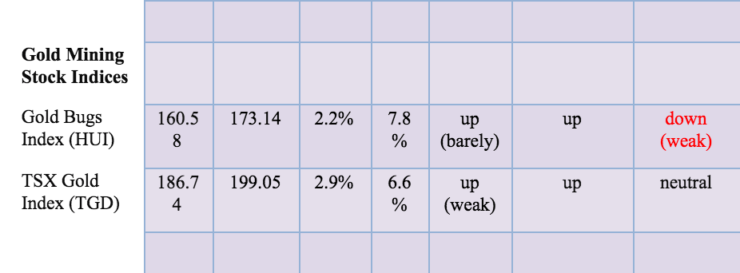

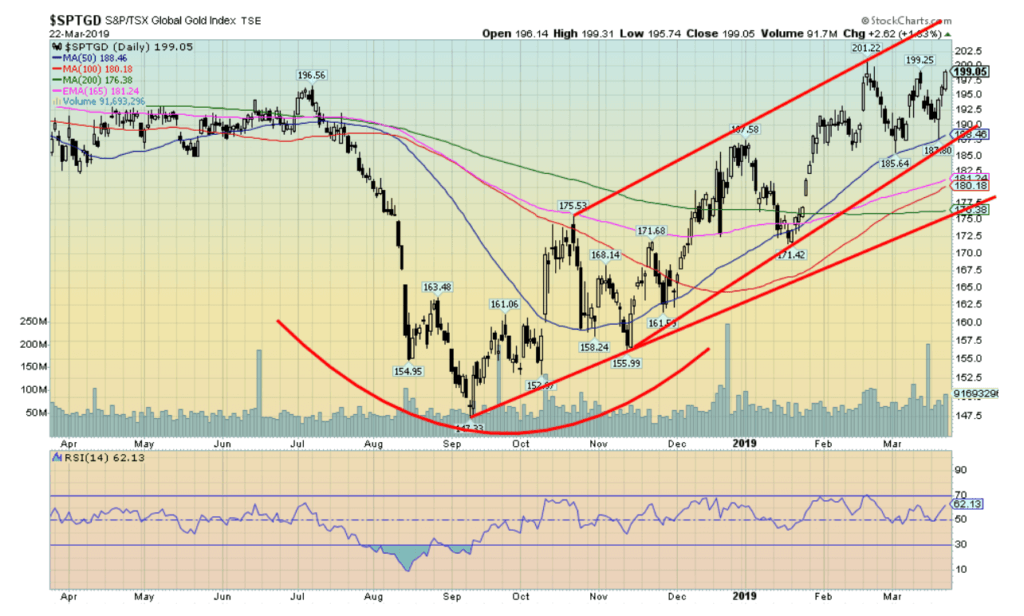

Gold stocks did well this past week. They were up on Friday even as the broader stock market fell sharply. The TSX Gold Index (TGD) rose 2.9% on the week and the Gold Bugs Index (HUI) was up 2.2%. The TGD made a zig-zag pattern from the low of 147 in September to the high of 201 in February. Since then, the TGD has been in a choppy pattern of down, up, down, up.

Whether the TGD makes a new high here or not is moot. The pattern suggests the TGD should eventually fall back once again. Below 188.50, a decline to trendline support at 170 is possible. Volume has typically fallen off on this up move. If gold and silver were to fall as we suspect, the gold stocks should follow to the downside. But, as with gold and silver, we believe it will be a final low and then a powerful rally could get underway.

© David Chapman

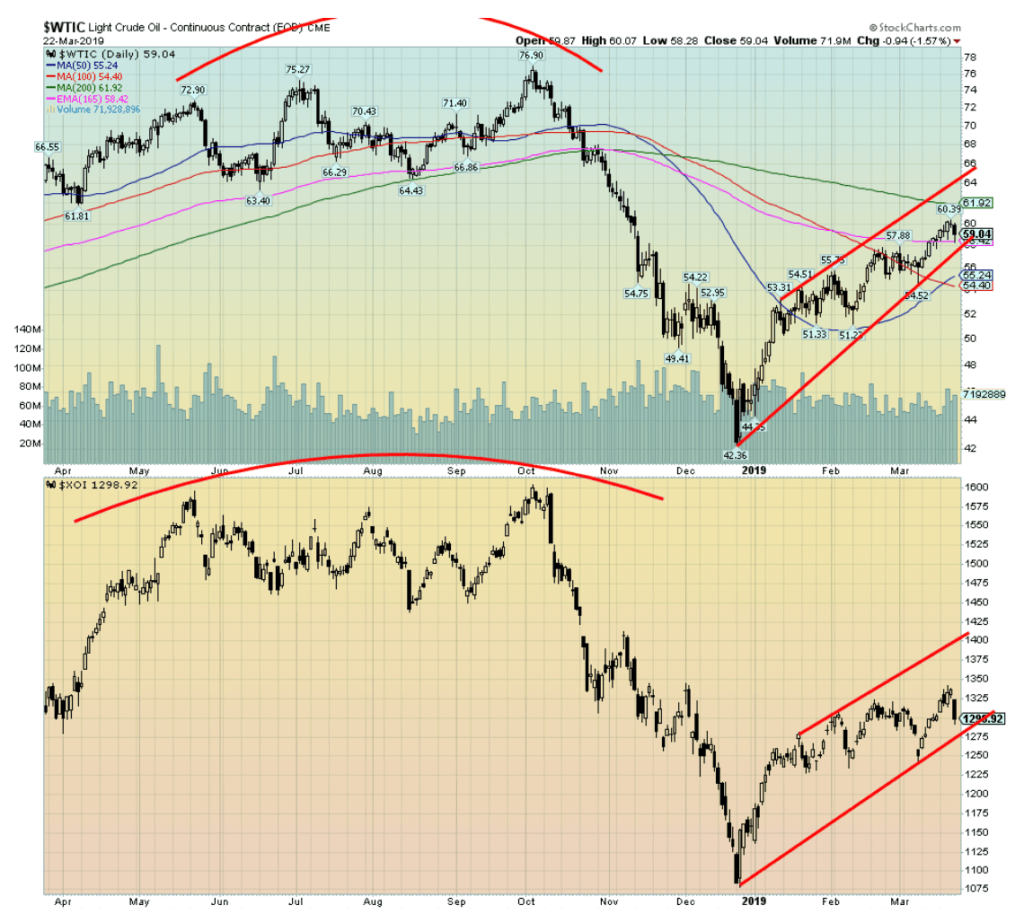

WTI oil rose to a high of $60.39 this past week, but on Friday it followed the stock market lower. We’d love to see WTI oil rise to the top of the channel near $64, but Friday’s drop was brought on by thoughts of a slowing economy. However, we are soon approaching the major driving season. As well, despite threats, OPEC and Russia have not increased production to put pressure on U.S. shale producers. Of course, it all depends on what is being called the NOPEC legislation whereby it would allow the U.S. government to sue the OPEC cartel.

It has been said that if that were to happen, OPEC would flood the market with oil pushing down the price of oil. That would put pressure on the highly leveraged shale producers. If WTI oil failed to hit the top of a channel WTI oil could be forming an ascending wedge pattern which is bearish. It starts to break down under $58 and under $54 a bigger sell-off could be underway. The energy stocks reacted negatively on Friday along with the broader market. The XOI breaks down under 1,275. The pattern that has formed appears as a wedge, so any bullish expectations are limited.

Chart of the week

© David Chapman

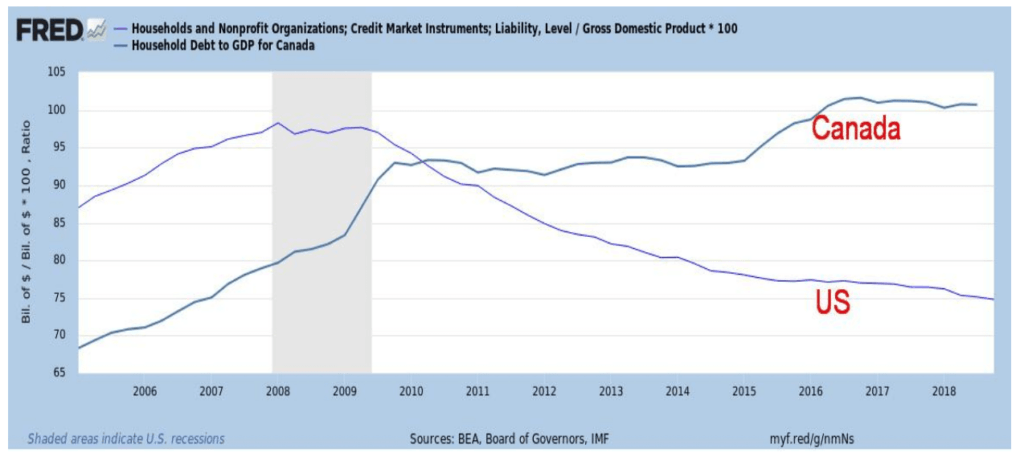

We have constantly heard from central bank officials and finance officials expressing concern about the level of household debt here in Canada. The latest figures from Q3 show Canada’s household debt to GDP is 100.7%. (Note: you usually hear about it in relation to income, but measuring it to GDP is also quite valid). That’s above the levels seen in the U.S. before the 2008 financial crisis. We also read that 46% of Canadians are a mere $200 from insolvency if a household member lost a job. The U.S. household debt to GDP hit a peak of 98.3% in Q1 2008. From there it has been downhill and it currently sits at 74.8% in Q4 2018—still high, but not quite as drastic. Still, it is high and also highly imbalanced. As in Canada, many are merely a job loss away from serious financial trouble.

© David Chapman

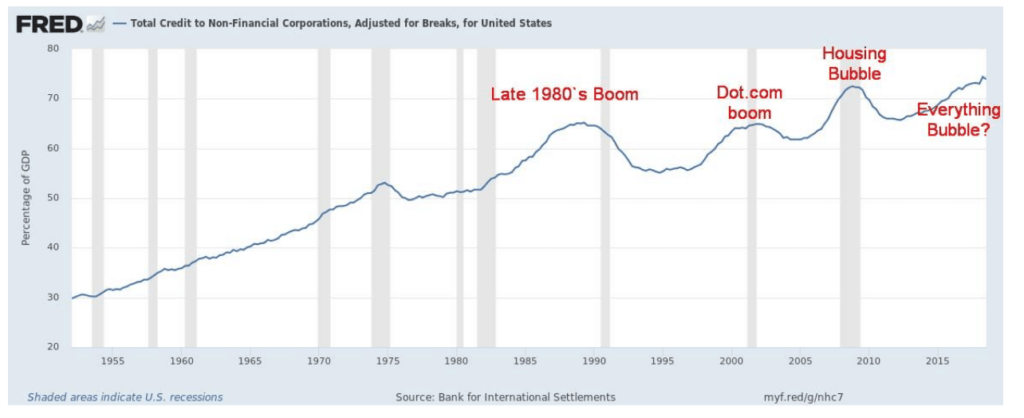

Corporations have also gorged on debt. Here is the ratio of corporate debt to GDP. Note how it has peaked each time before a downturn. And not only has it peaked but it did so at increasingly higher levels. The late 1980s boom saw it peak at 65%. The dot.com bubble’s peak was also seen at about 65%. It went higher for the housing bubble in 2008 with the peak seen in Q4 2008 at 72.5%. This time it has exceeded all the previous peaks, currently at 73.9% in Q3 2018. We suspect it is probably higher now. Nonetheless, it is not a positive sign.

(Featured image by katjen via Shutterstock)

—

DISCLAIMER: David Chapman is not a registered advisory service and is not an exempt market dealer (EMD). We do not and cannot give individualized market advice. The information in this article is intended only for informational and educational purposes. It should not be considered a solicitation of an offer or sale of any security. The reader assumes all risk when trading in securities and David Chapman advises consulting a licensed professional financial advisor before proceeding with any trade or idea presented in this article. We share our ideas and opinions for informational and educational purposes only and expect the reader to perform due diligence before considering a position in any security. That includes consulting with your own licensed professional financial advisor.

The TopRanked.io Guide to 2026’s Biggest and Best Affiliate Opportunities

Want to earn affiliate commissions on literal billions of dollars worth of revenue? Then this week, we've got something special...

Eni Advances Energy Transition with Major Investment and Emissions Cuts

Eni showcased its “Just Transition” report in Rome, highlighting stakeholder collaboration and progress toward decarbonization goals. The company invested over...

The German Fintech Market Shows Resilience and Strong Investment Growth in 2026

Germany’s fintech sector remained resilient in 2026 despite economic crisis and rising insolvencies. Investments reached €14.2 billion, showing strong investor...

Cannabis Legalization in Germany: A Mixed Interim Assessment

Germany’s cannabis legalization has reduced criminal cases and eased pressure on the justice system, while the black market is slowly...

Sustainable Restoration of the Haus Hövener Garden in Brilon

The Brilon Construction Workers Association is restoring the Haus Hövener garden into a cultural community space, funded through a €10,000...

|

|

|  |

|

|

-

Crowdfunding2 weeks ago

Crowdfunding2 weeks agoSpain’s Crowdfunding Sector Surges as Real Estate and SME Financing Expand

-

Cannabis5 days ago

Cannabis5 days agoArgentina Legalizes Cannabis Seed Sales Under New Regulatory Framework

-

Fintech2 weeks ago

Fintech2 weeks agoZulu Powers Instant Corporate Payments Launch in Colombia

-

Business7 days ago

Business7 days agoDow Jones Rally Faces Uncertainty Amid NASDAQ Reversal