Featured

What’s Next, Inflation or Deflation? What Does it Mean for the Markets?

The credit markets should be freezing up and the stock market should be plunging from record-high valuations by that time. Today’s Fed decision expedited the timeline for that chaos to begin. The buy and hold portfolio is a danger to your retirement’s health. the time to get into a dynamically-managed strategy in now.

The Producer Price Index for the month of May was up 6.6% year over year. This was the greatest yearly increase since the Bureau of Labor Statistics began tracking the data. In addition, the Headline Consumer Price Index rose 5% year over year in May, which is the fastest pace since August 2008. Import Prices also surged in May, soaring by 11.3% in the past twelve months—the greatest surge in a decade. However, those blistering rates of inflation didn’t rattle the bond market much at all. In fact, the bond market is completely unfazed by the current inflation data.

Below is a chart of the Benchmark Treasury yield intra-day on June 10th, the day of the hottest CPI print in 13 years. And it wasn’t a sell-the-news even either, because interest rates had been falling into the release of the strongest inflation print in over a decade.

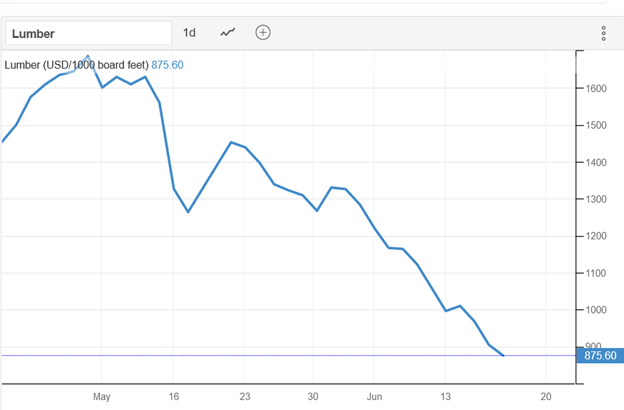

But it’s not just the bond market that is quiescent about inflation. Commodity prices have started to slip too. Lumber prices are tumbling, as new home prices have now climbed above the reach of most consumers. And, Dr. Copper is declaring that peak growth and inflation has arrived too, regardless of the strong data seen today.

Of course, having interest rates this low are completely ridiculous. The Atlanta Fed GDP estimate for Q2 real economic growth is 10.3%–estimate as of June 16, 2021. When you add Consumer Price Inflation into the calculation, you get 15.5% nominal GDP growth. Now, what would you think an investor would require in a fixed income instrument offered by Uncle Sam going out 10 years when nominal growth is above 15%? Well, history dictates that it should be close to that 15% nominal GDP figure. But instead, Benchmark Treasuries offer just 1.5!

That is the most distorted and manipulated rate in the history of the United States, thanks to relentless central bank intervention. However, such a low relative yield could only exist if the current rate of growth and inflation is deemed to have peaked by whatever is left of the free market. Who are these players? For the most part, they are an elite group of individuals with massively deep pockets and access to the best information.

But still, the current inflationary environment is confounding many investors and most in the main stream financial media; who tend to just perform the exercise of linear extrapolation to predict the future.

So why are bond yields falling, along with key commodity prices, when the current data on growth and inflation are so strong? The answer is threefold. These savviest of investors understand that the bulk of government fiscal stimulus has passed. In fact, approximately 88% of the total amount earmarked for direct relief has already been disseminated, according to the IRS. Also, the Fed is on the precipice of winding down its humongous and record-setting $120 billion per month stimulus scheme. But perhaps the most important reason for the certainty we have that growth and inflation rates have peaked, is that this past pandemic-induced recession was anything but typical.

During most economic downturns, the economy goes through a period of sharp deleveraging. But the exact opposite occurred during the COVID-19 recession. Total debt, both public and private, has now soared to just below $80 trillion, which is now 380% of GDP. The previous cycle-high was 370%, which occurred back in Q2 2009—at the nadir of the Great Recession. And debt is still being piled on. Household debt totaled $16.9 trillion for the 1st quarter of this year. It soared at a 6.5% annual rate, which was the fastest pace of debt growth since 2006.

The fact is, the economy was late-cycle prior to the pandemic, and has simply returned to late- cycle once again. Meaning, there has been no deleveraging of the corporate or consumer balance sheets, as is the usual case at the end of a recession and the start of a new business cycle. Debt levels have increased significantly across the board–especially at the Federal government level. The US economy was debt-disabled prior to the pandemic and it will be even more so ex post. An economy with a debt to GDP ratio near 400% just can’t grow quickly and will experience low inflation–that is, of course, unless and until the currency plummets and causes interest rates to soar.

Not only this, but there has been absolutely zero reconciliation of asset prices this time around. In an ordinary recession, asset prices are sold as debt is paid off. In this case, real estate, equities and bond prices are trading at all-time record-highs. Hence, the economy should soon return to its pre-pandemic late business cycle conditions of below trend growth and inflation, with the most dangerous and deflationary asset price correction in history still ahead.

Mr. Powell and his merry band of money printers at the Fed recently wrapped up the June FOMC meeting. After aggressively courting inflation for years, they have finally received satisfaction. But they now want to spurn it–happily, in my opinion. Hence, they pulled forward the dot-plot to indicate 2 rate hikes by the end of 2023. And, during Powell’s press conference he indicated the tapering talks have begun. However, the 10-year Note still was anchored around 1.5% despite the more hawkish fed.

Here’s a glimpse of what lies ahead for the market: by the second quarter of 2022, which is only 3 quarters away now. The year over year rate of change in growth and inflation will not just be slowing down, it should be plunging. At the same time, as mentioned already, virtually all the fiscal stimulus will be over and done. No more expanded child income tax credits, no more stimulus checks, enhanced unemployment will have ended, student loan/mortgage and rental forbearance will have expired. And, the Fed won’t just be talking about tapering, it will be in the middle of eliminating its $120 billion per month bond-buying scheme.

In other words, the credit markets should be freezing up and the stock market should be plunging from record-high valuations by that time. Today’s Fed decision expedited the timeline for that chaos to begin. The buy and hold portfolio is a danger to your retirement’s health. the time to get into a dynamically-managed strategy in now.

__

(Featured image by AbsolutVision via Unsplash)

DISCLAIMER: This article was written by a third party contributor and does not reflect the opinion of Born2Invest, its management, staff or its associates. Please review our disclaimer for more information.

This article may include forward-looking statements. These forward-looking statements generally are identified by the words “believe,” “project,” “estimate,” “become,” “plan,” “will,” and similar expressions. These forward-looking statements involve known and unknown risks as well as uncertainties, including those discussed in the following cautionary statements and elsewhere in this article and on this site. Although the Company may believe that its expectations are based on reasonable assumptions, the actual results that the Company may achieve may differ materially from any forward-looking statements, which reflect the opinions of the management of the Company only as of the date hereof. Additionally, please make sure to read these important disclosures.

Credibur Scales Rapidly: €2 Billion in Structured Debt Facilities in Six Months

Infrastructure fintech Credibur has added over two billion euros in structured debt facilities within six months. Its platform connects lenders,...

EU Taxonomy 2025: Progress in ESG Reporting, Gaps in True Sustainability

EY’s EU Taxonomy Barometer 2025 shows improved ESG reporting among European companies, but a major gap remains between “eligible” and...

Democratizing Farmland Investment: The Rise of Farm Fractions in Agritech

Farm Fractions is a Chilean startup that enables individuals to invest in farmland from US$100 through fractional ownership. Using fintech...

Crypto Markets Edge Up as Caution Persists and April Fools’ Scams Loom

Bitcoin and Ethereum rise slightly amid geopolitical easing and renewed ETF inflows, with BTC near $68,000 and ETH above $2,100....

Lowryder: The Autoflowering Revolution in Cannabis Cultivation

Lowryder is a groundbreaking cannabis strain that introduced autoflowering, allowing plants to flower automatically without light changes. Created by The...

|

|

|  |

|

|

-

Impact Investing2 weeks ago

Impact Investing2 weeks agoITAS Mutua Reports Strong 2025 Growth and Sustainability Progress

-

Fintech2 days ago

Fintech2 days agoCrypto Lending Hits $30 Billion, Becomes Key DeFi Pillar

-

Markets1 week ago

Markets1 week agoCocoa Markets Steady as Weak Demand and Rising Supply Signal Potential Surplus

-

Impact Investing6 days ago

Impact Investing6 days agoH&M Advances Sustainability and Cuts Emissions by 2025