Featured

Why Soybeans and Soybean Oil Closed Lower

Soybeans and Soybean Oil closed lower primarily as Soybeans moved back down to test support at the breakout levels just below the lows of the day yesterday. Soybean Oil weakened due to weakness in Crude Oil futures and subsequent demand concerns due to the potential for closings to return due to a resurgence of the Coronavirus. Soybean Meal was higher as demand has greatly improved in the US and Canada.

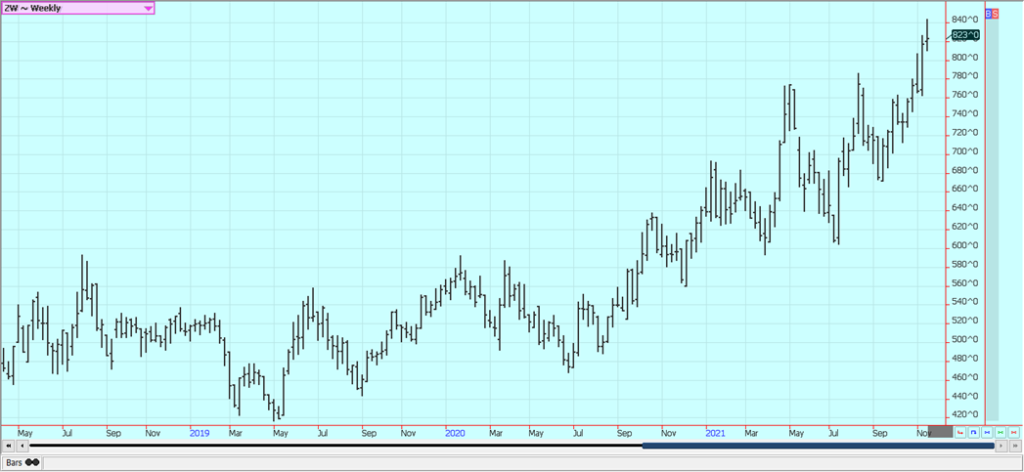

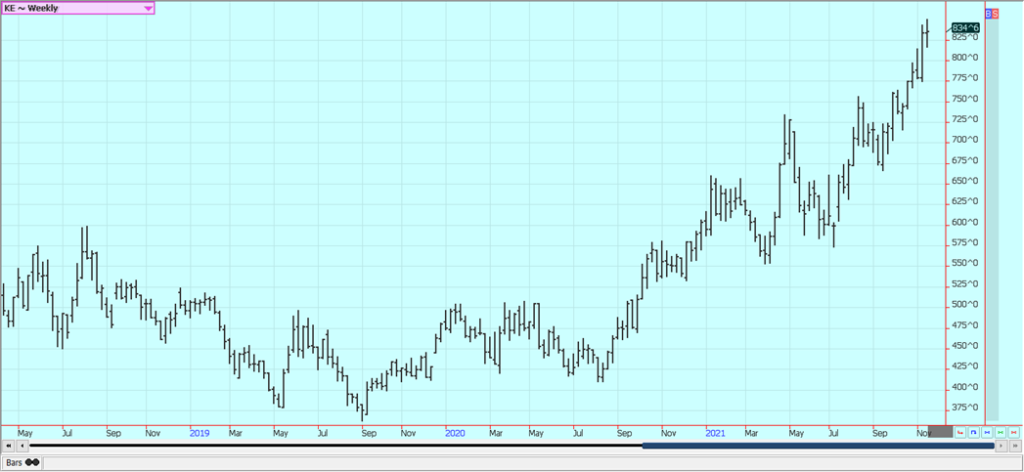

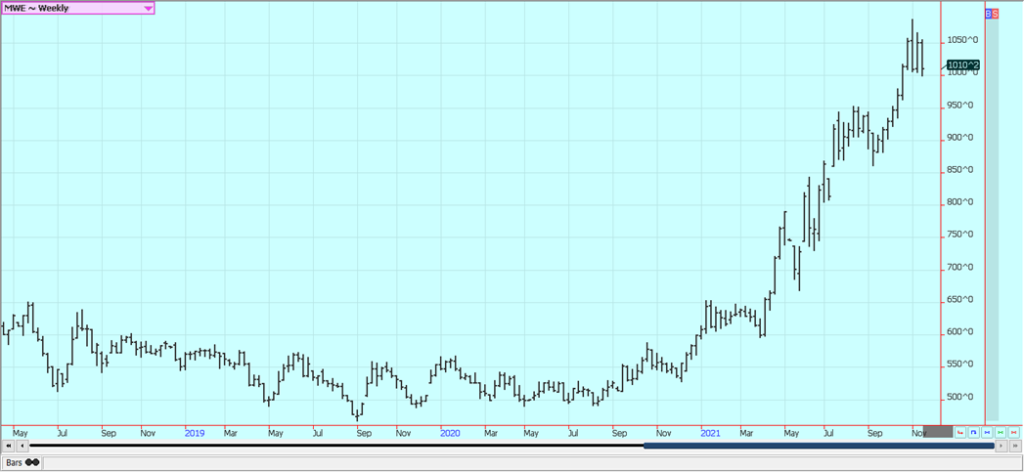

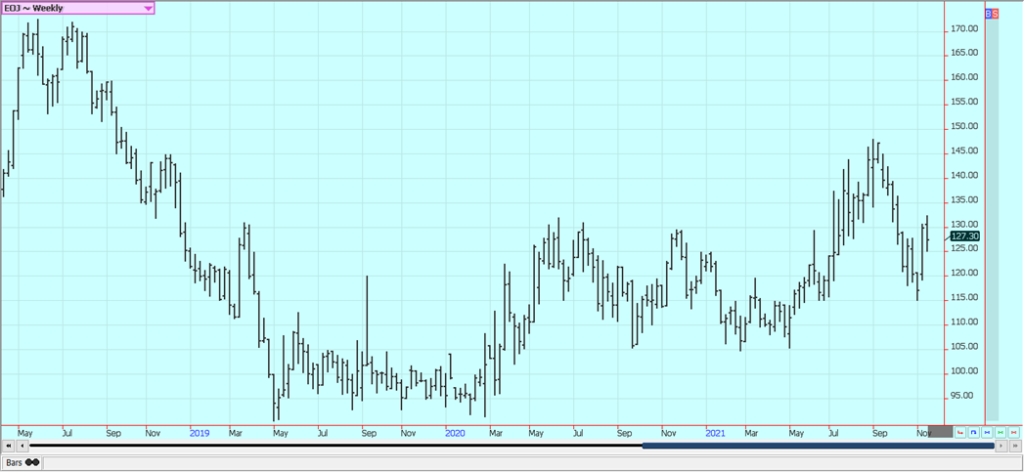

Wheat: Wheat closed lower Friday and for the week in all three markets and prices are back in the recent trading range for the Winter Wheat markets. Minneapolis continues to show topping potential and closed on a weak note on Friday. Speculators appeared to be the best sellers and were reported to be liquidating longs. Ideas are that the US will have good demand for Wheat as the rest of the northern hemisphere is short production this year. Offer volumes are down from both Russia and Europe. Dry weather in southern Russia as well as the northern US Great Plains and Canadian Prairies remains a supportive feature in the market although the weather has become old news. The lack of production has reduced the offers and Russia plans to announce sales quotas for next year very soon. Russia has already increased export taxes to control the flow of export Wheat out of the country. The Russian weather has been good for production in northern and western areas and has recently improved in southern areas and into Kazakhstan in time for the next crop. Siberian Spring Wheat conditions have been very good. Europe is expecting top yields in some areas but less yield in others and parts of eastern Europe and northern Russia are expecting strong yields. European quality is a problem due to too much rain in some areas and not enough in others.

Weekly Chicago Soft Red Winter Wheat Futures

Weekly Chicago Hard Red Winter Wheat Futures

Weekly Minneapolis Hard Red Spring Wheat Futures

Corn: Corn closed lower in range trading last week but the daily charts suggest a correction down is coming in the short term. The weekly charts still suggest higher prices are coming longer term and the fundamentals do as well. Corn has relatively tight supplies as farmers are harvesting and not selling. Demand will be an increasing feature in the trade moving forward as the harvest moves to completion sometime this month. Demand has been good so far this season. Yield reports have been mixed but generally strong. Most of the elevators along the Mississippi are exporting again which is good news for nearby demand. There are a lot of ideas that production and planted and harvested area will be significantly less next year due to the lack of fertilizers available and the cost of production. Oats were higher but held the recent trading range.

Weekly Corn Futures

Weekly Oats Futures

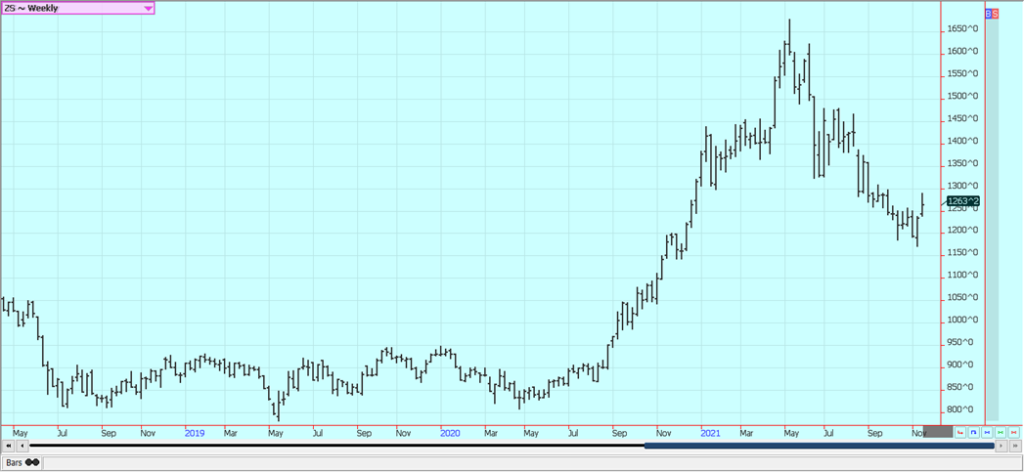

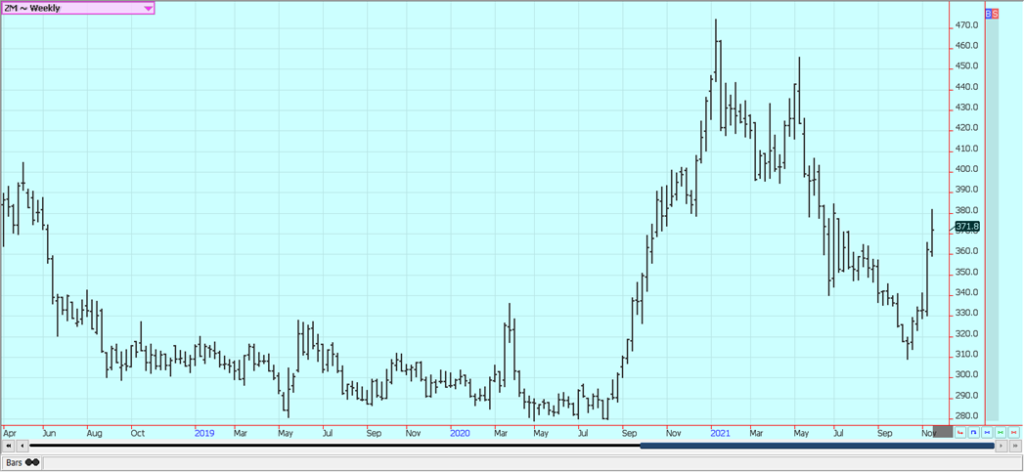

Soybeans and Soybean Meal: Soybeans and Soybean Oil closed lower primarily as Soybeans moved back down to test support at the breakout levels just below the lows of the day yesterday. Soybean Oil weakened due to weakness in Crude Oil futures and subsequent demand concerns due to the potential for closings to return due to a resurgence of the Coronavirus. Soybean Meal was higher as demand has greatly improved in the US and Canada with no big amounts of Rapeseed or Canola Meal available. The breakout has held so far. Harvest is starting to wrap up for Soybeans and a harvest low might have been hit this week. Reports indicate that farmers are limited sellers at best. Gulf port elevators are coming on line and export sales and exports are increasing. Planting and initial crop development is going very well in Brazil. Brazil could have soybeans ready for export by the end of February and the crop potential is up to 150 million tons. It has been dry in Argentina but rain has been falling this week and conditions for planting and initial growth are improving.

Weekly Chicago Soybeans Futures:

Weekly Chicago Soybean Meal Futures

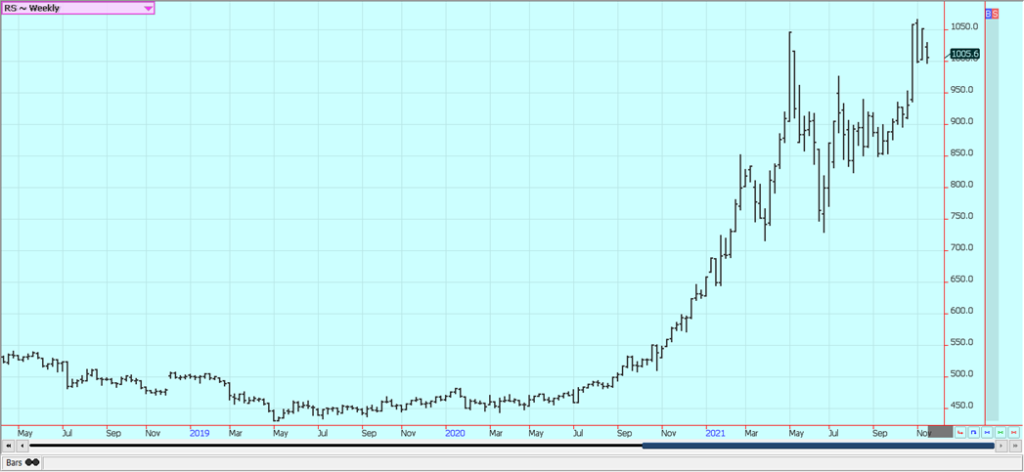

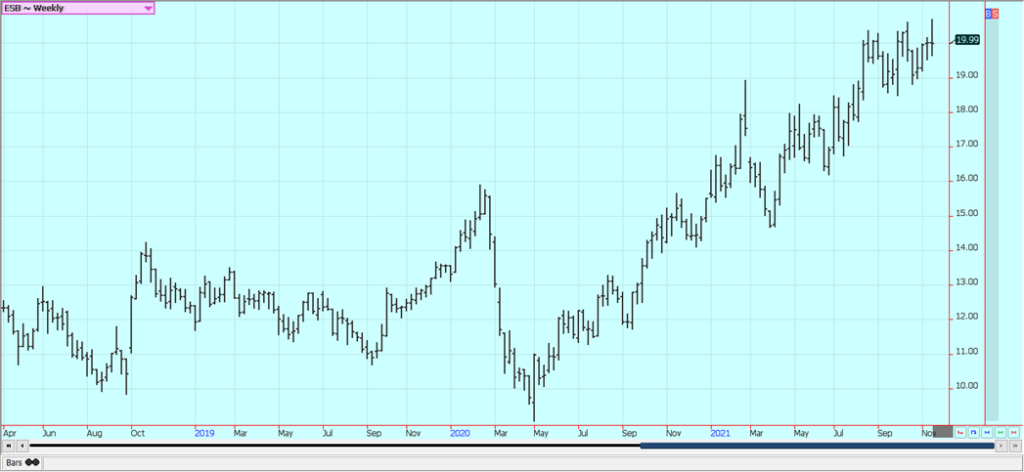

Rice: Rice was near unchanged on Friday but higher for the week. The weekly charts show that the rally continues and has made new highs with futures trading above 1400/cwt for the first time in more than a year. The cash market is also reported to be stronger, especially in Texas. Weekly chart trends are now up. Daily charts show up trends and that futures have broken through important resistance areas. The crop has been largely harvested in all states. Export demand has been good but not great so far and is mostly for paddy. Mill demand has been about average so far.

Weekly Chicago Rice Futures

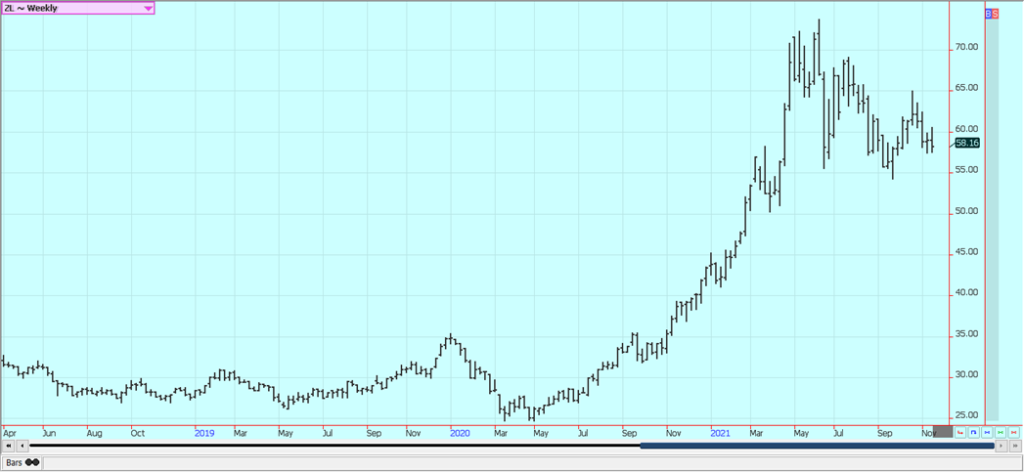

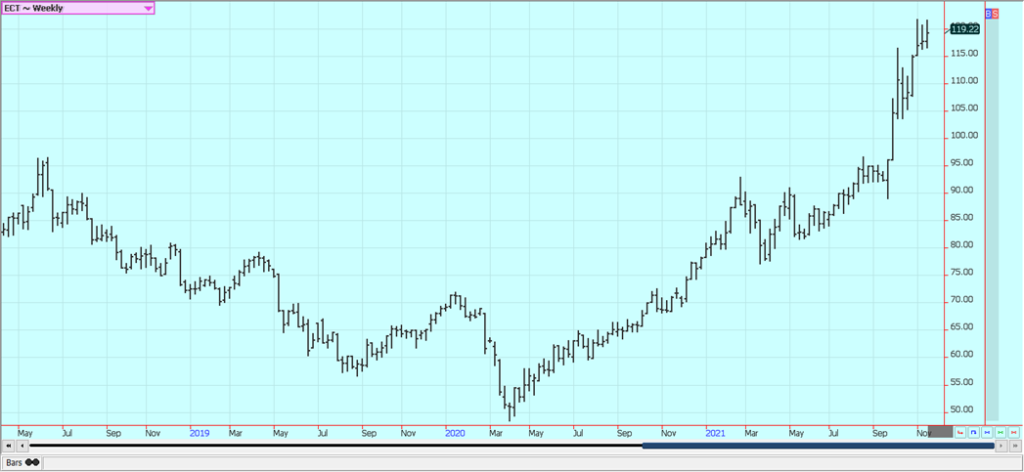

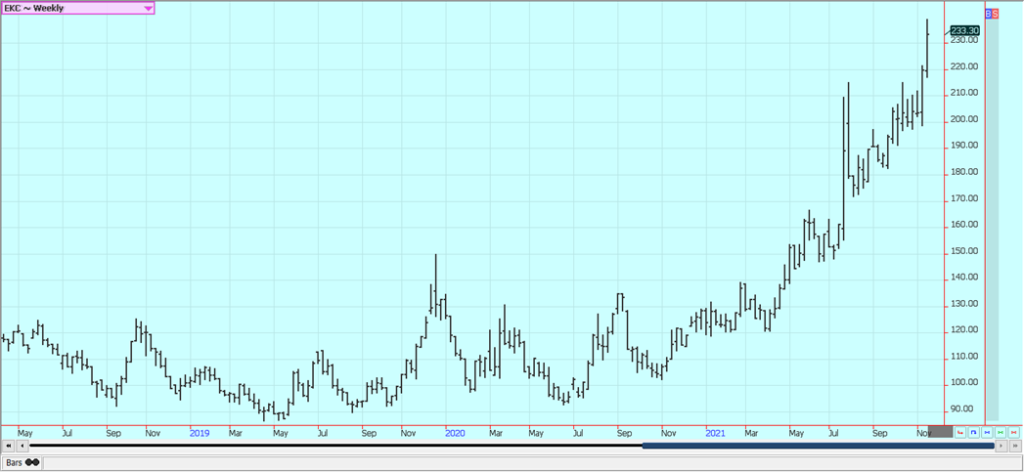

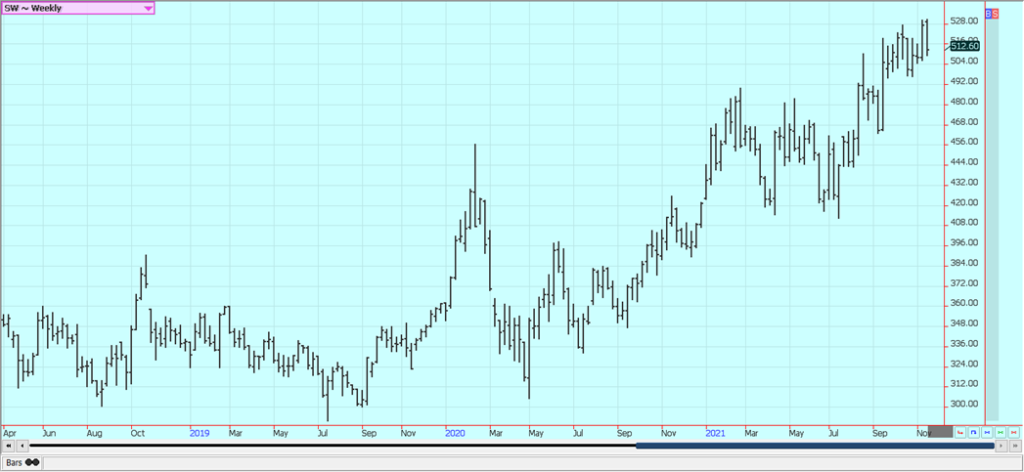

Palm Oil and Vegetable Oils: Palm Oil was a little higher last week on ideas of weak production ahead and good demand, especially from China for fuel uses. Futures are still caught in a trading range on the weekly charts but are now at the upper end of the range. Support still comes from ideas that supply and demand are in balance or supplies are short. The weekly chart trends are up. There are ideas of tight supplies due to labor problems. There are just not enough workers in the fields due to Coronavirus restrictions. Production has also been down to more than offset the export losses so prices have trended higher. Canola was lower along with price action in Chicago Soybean Oil. Farmers are bullish and reluctant to sell because of the sharp reduction in Canola production in Canada this year. The weekly chart trends are up.

Weekly Malaysian Palm Oil Futures

Weekly Chicago Soybean Oil Futures

Weekly Canola Futures:

Cotton: Futures were higher Friday as some speculative buying entered the market. Cotton futures closed higher for the week. Demand has fallen off with the rally in the US Dollar but US prices are reported to be still well below those in China so strong demand is expected to continue, at least from that destination. Trends are sideways on the charts but are starting to turn up again and the fundamentals have not really changed. Demand for US Cotton remains very strong and that is good news for sellers as the strong demand implies strong prices should continue. Analysts say the Asian demand is still very strong and likely hold at high levels for the future. US consumer demand has been very strong as well despite higher prices and inflation. Good US production is expected. The harvest is behind the 5 year average due to rains in the Delta and Southeast that have kept farmers from the fields. Chinese demand is also strong as clothes makers use foreign Cotton to get away from domestic supplies that might have been produced by forced labor and might not be allowed in the US or other western countries

Weekly US Cotton Futures

Frozen Concentrated Orange Juice and Citrus: FCOJ was a little lower last week on speculative profit taking and trends are sideways again in the market. There is not much going on in this market but the charts show that futures might have made a short-term low last week. The hurricane season is over and the chances for a damaging storm to hit the state of Florida are gone so speculators have gotten out of longs and got short. The weather remains generally good for production around the world. Brazil has some rain with more in the forecast and flowering is likely. Brazil production was down last year due to dry conditions at flowering time and then a freeze just before harvest. Weather conditions in Florida are rated mostly good for the crops with a couple of showers and near-normal temperatures. Mexican crop conditions in central and southern areas are called good with rains. Northern and western Mexico is rated in good condition.

Weekly FCOJ Futures

Coffee: New York closed higher and London closed lower last week with the logistical problems in Brazil very important to the trade. The trucks have gone on strike in Brazil, compounding logistical problems for exports from that country but the last few days of higher prices have put the lack of trucking into the price. The lack of Coffee available to deliver against Robusta contracts remains a factor. Containers are not available in Vietnam to ship the Coffee. Covid has also returned to Vietnam and could be a factor in interrupting shipments. Brazil also has limited amounts of Coffee available after bad weather at flowering time and then a freeze before the harvest got underway. More dry weather is in the forecast for much of Brazil and flowering is reported now in many growing areas. There are worries that the flowers might drop before cherries are formed. Production conditions for the next crop in Brazil are called good. Scattered showers are now in the forecast for Southeast Asia and for Vietnam. The weather has been erratic and some harvest delays are being reported due to too much rain falling before. Bad conditions are reported in northern South America with above-average rains and good conditions reported in Central America with near-average rains. Conditions are reported to be generally good in parts of Africa.

Weekly New York Arabica Coffee Futures

Weekly London Robusta Coffee Futures

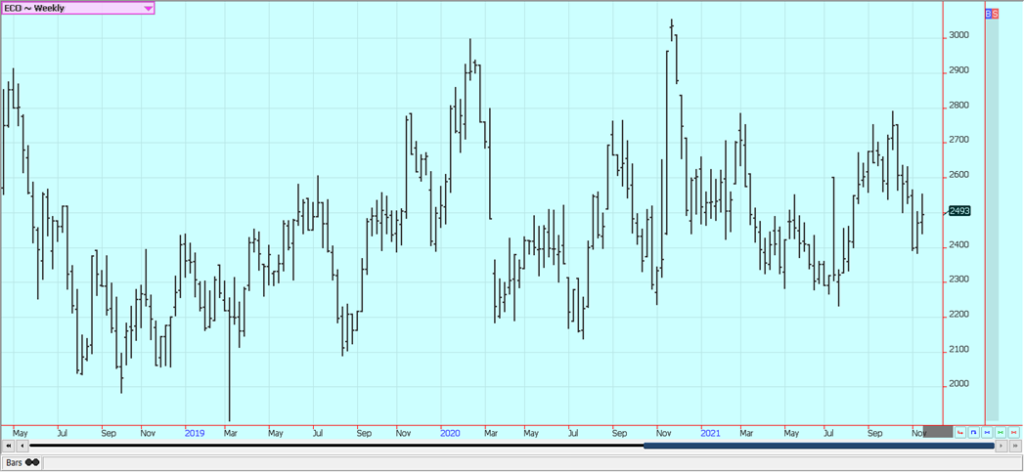

Sugar: New York closed near unchanged for the week on Friday and London closed lower. The daily charts show that futures are back in the recent trading range and the weekly charts also show a range trade. The charts show that futures continue to hold support and keep the longer-term up trends alive. Reports indicate that consumer demand has returned to the market. Ideas are that the supplies are out there but it will take a stronger price to get them into the market. Ideas are that Indian producers and exporters are willing sellers above 20.50 cents. Processors in Brazil are refining the cane for Ethanol more than Sugar right now and this trend is expected to continue due to the relative price spreads. The reduced production potential from Brazil for the current harvest is still impacting the market. India is not offering as world prices are well below domestic prices and has had some weather problems of its own. It has just raised the price of Sugarcane juice for ethanol production so mills can divert more from the Sugar market into Ethanol production. Thailand is expecting improved production. It is raining in southern Brazil which will be good for the next crops there.

Weekly New York World Raw Sugar Futures

Weekly London White Sugar Futures

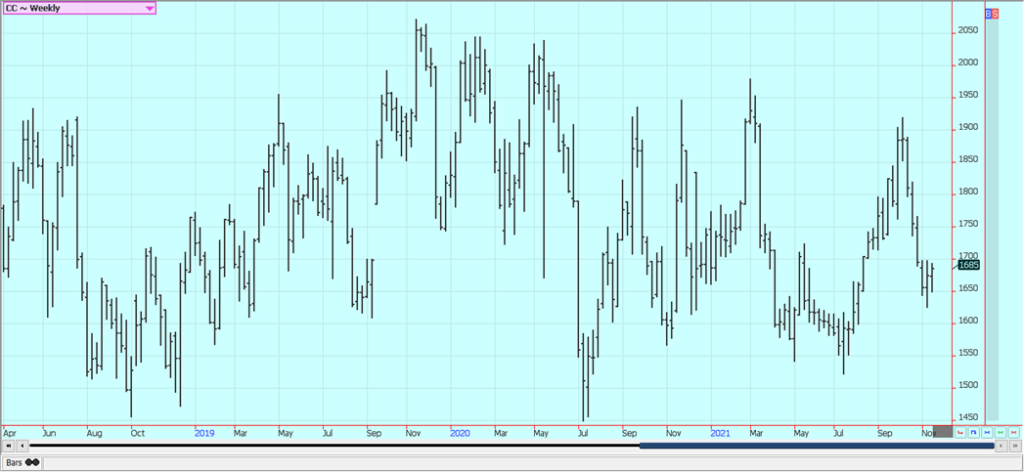

Cocoa: New York closed about unchanged and London closed higher last week and trends are still up in both markets. Ideas are that demand will only improve slightly and production in West Africa appears to be good this year. Both Ivory Coast and Ghana are reporting improved weather as it is now mostly sunny with some scattered showers around. World economies are starting to reopen after Covid and the open economies are giving demand the boost but the boost has not been as strong as hoped for earlier. Ivory Coast arrivals are now estimated at 489,000 tons, down 10.9% from last year.

Weekly New York Cocoa Futures

Weekly London Cocoa Futures

—

(Featured image by Polina Tankilevitch via Pexels)

DISCLAIMER: This article was written by a third party contributor and does not reflect the opinion of Born2Invest, its management, staff or its associates. Please review our disclaimer for more information.

This article may include forward-looking statements. These forward-looking statements generally are identified by the words “believe,” “project,” “estimate,” “become,” “plan,” “will,” and similar expressions. These forward-looking statements involve known and unknown risks as well as uncertainties, including those discussed in the following cautionary statements and elsewhere in this article and on this site. Although the Company may believe that its expectations are based on reasonable assumptions, the actual results that the Company may achieve may differ materially from any forward-looking statements, which reflect the opinions of the management of the Company only as of the date hereof. Additionally, please make sure to read these important disclosures.

Futures and options trading involves substantial risk of loss and may not be suitable for everyone. The valuation of futures and options may fluctuate and as a result, clients may lose more than their original investment. In no event should the content of this website be construed as an express or implied promise, guarantee, or implication by or from The PRICE Futures Group, Inc. that you will profit or that losses can or will be limited whatsoever. Past performance is not indicative of future results. Information provided on this report is intended solely for informative purpose and is obtained from sources believed to be reliable. No guarantee of any kind is implied or possible where projections of future conditions are attempted. The leverage created by trading on margin can work against you as well as for you, and losses can exceed your entire investment. Before opening an account and trading, you should seek advice from your advisors as appropriate to ensure that you understand the risks and can withstand the losses.

Edison Accelerates Renewable Growth and ESG Impact in 2025

Edison reports strong 2025 sustainability progress, boosting renewable investments by 90% to reach 2.3 GW toward a 4 GW 2030...

New Gene Therapies Transform Rare Disease Care, but Gaps Remain

Gene therapies are transforming rare disease treatment, enabling normal lives for some patients. However, only about 6% of 7,000 rare...

Temotiva Launches Crowdfunding Campaign to Advance Preventive Mental Health

Temotiva Innovación Lab has launched a crowdfunding campaign through Santander X Explorer, marking a new phase for the University of...

Fed Policy Shift Raises Concerns Over Debt and Inflation Risks

The Federal Reserve is criticized for resuming balance sheet expansion through Treasury purchases despite expectations of tighter policy under new...

AI Adoption in Italian Retail Stalls Despite Strong Experimentation

A survey on AI in Italian large-scale retail trade shows companies are increasingly adopting artificial intelligence, but only 1.4% have...

|

|

|  |

|

|

-

Cannabis6 days ago

Cannabis6 days agoEurope’s Cannabis Shift: Rising Use, and New Risks

-

Markets2 weeks ago

Markets2 weeks agoSugar Markets Rise Slightly Amid War, Oil Price Pressure, and Strong Global Supply

-

Impact Investing3 days ago

Impact Investing3 days agoAI Adoption in Italian Retail Stalls Despite Strong Experimentation

-

Cannabis1 week ago

Cannabis1 week agoCannabis Legalization in Germany: A Mixed Interim Assessment