Featured

Why Soybeans Futures Closed Lower Last Week

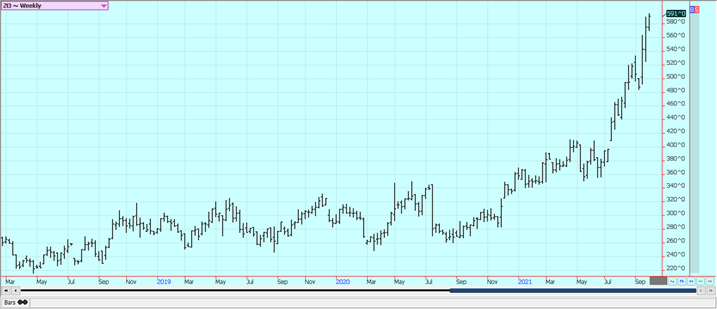

Soybeans and Soybean Meal closed lower last week in response to the USDA reports that showed much higher than expected stocks levels of 256 million bushels. Soybean Oil closed higher as demand ideas for biofuels, especially biodiesel, remained strong. USDA raised production from last year to account for the increased stocks as demand was known.

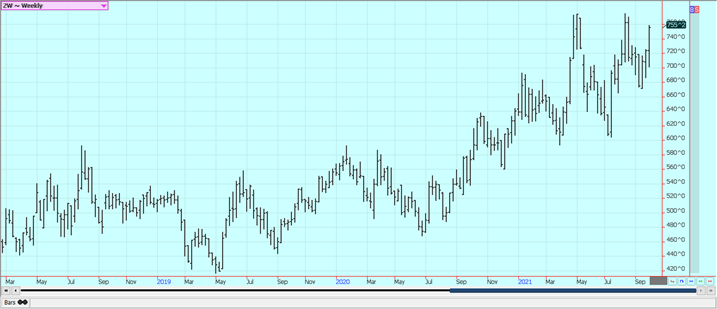

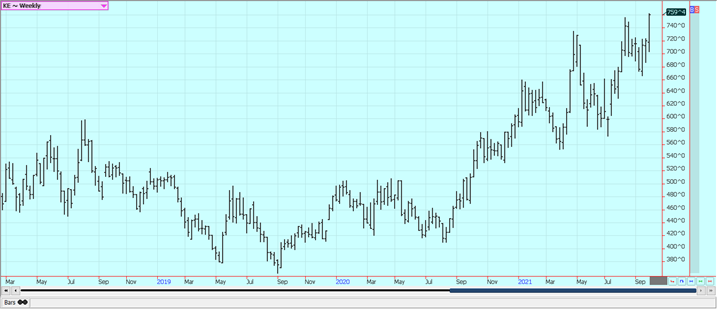

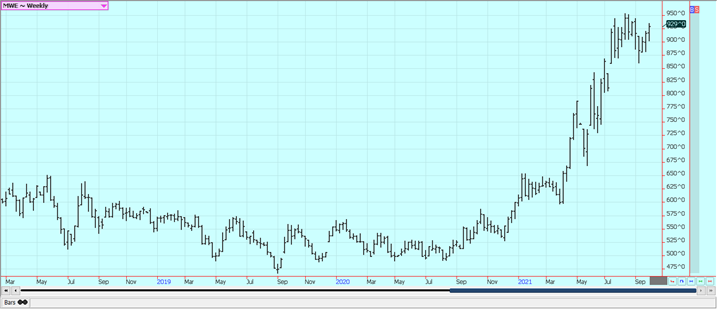

Wheat: Winter Wheat was higher last week as USDA greatly cut production of HRW. Production was just 749 million bushels instead of the previous USDA estimate of 777 million. That forced USDA to cut Winter Wheat and All Wheat production as well. Minneapolis Spring Wheat was higher as USDA cut production in line with trade estimates at 331 million bushels. Trends are up with new highs for the move scored in SRW and Spring and new multi-year highs seen in HRW. Russia could severely restrict Wheat exports due to production lost to drought and those ideas have kept demand hopes for US Wheat alive. Production is less this year in Russia and internal prices have been strong. Dry weather in southern Russia as well as the northern US Great Plains and Canadian Prairies remains a supportive feature in the market although the weather has become old news. The Russian weather has been good for production in northern and western areas but is still trending dry in southern areas and into Kazakhstan. Siberian Spring Wheat conditions have been very good. Europe is expecting top yields in some areas but less yield in others and parts of eastern Europe and northern Russia are expecting strong yields. European quality is a problem due to too much rain in some areas and not enough in others.

Weekly Chicago Soft Red Winter Wheat Futures

Weekly Chicago Hard Red Winter Wheat Futures

Weekly Minneapolis Hard Red Spring Wheat Futures

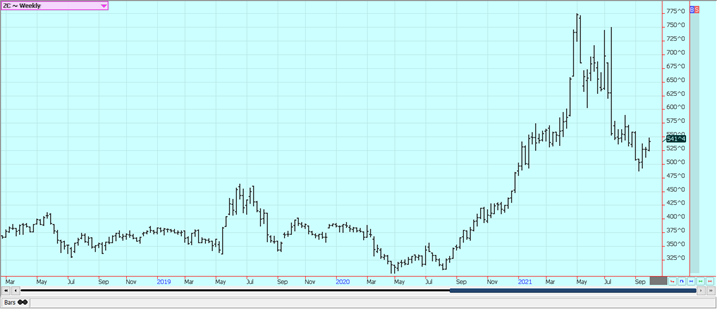

Corn: Corn was a little higher on Friday and higher for the week. The quarterly stocks were higher than anticipated, but production last year was less than anticipated. Demand has not been good and demand will be a feature in the trade moving forward. Trends are mixed to up on the weekly charts and are mixed on the daily charts. Traders are now waiting on the harvest and yield reports but the gut slot of the harvest is still a few days away. Ideas are that the yield reports will be high and will confirm the USDA production estimates or even find better yields. However, there have been reports of diseases in Illinois fields so record production might not happen in that state. Initial yield reports have been mixed, with some lower yields reported due to disease. There are still the drought-reduced crops in the northwestern Corn Belt and northern Great Plains to be counted as well. Most of the elevators along the Mississippi are exporting again which is good news for nearby demand. Oats were also higher as USDA showed small supplies amid a drought in the northern Great Plains and Canada. There will not be much in the way of high-quality Oats for consumers to buy in the coming year.

Weekly Corn Futures

Weekly Oats Futures

Soybeans and Soybean Meal: Soybeans and Soybean Meal closed lower last week in response to the USDA reports that showed much higher than expected stocks levels of 256 million bushels. Soybean Oil closed higher as demand ideas for biofuels, especially biodiesel, remained strong. USDA raised production from last year to account for the increased stocks as demand was known. The increase for production and stocks was about 80 million bushels. Crush and export data are very available to the problems were all on the supply side. The weekly charts still show downtrends for all three markets, and the daily chart trends are down in Soybeans and Soybean Meal. Chinese demand has been supportive until now as the country was active in the US Soybeans market over the weekend. Harvest is underway for Soybeans. Gulf port elevators are coming on line and exports are increasing. The weekly export sales report showed good sales and China was the big buyer.

Weekly Chicago Soybeans Futures:

Weekly Chicago Soybean Meal Futures

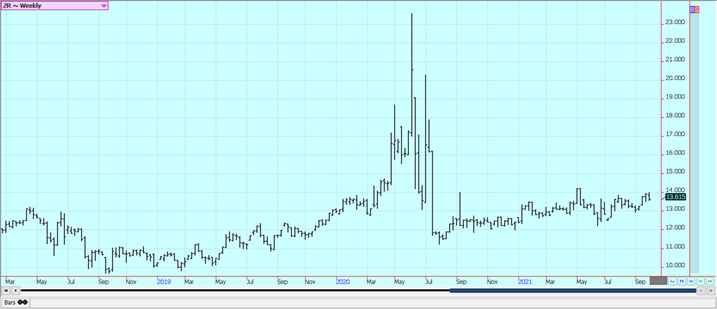

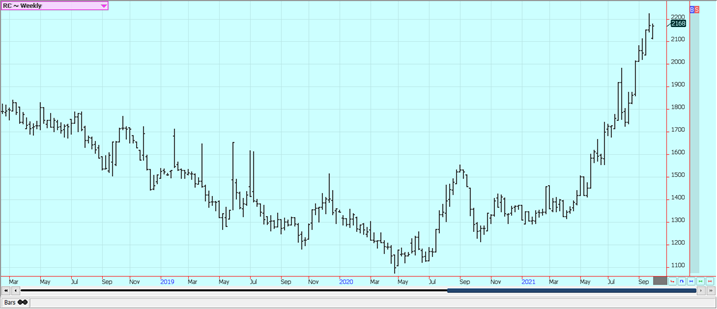

Rice: Rice closed lower last week on what appeared to be speculative selling based on deteriorating chart patterns. The first crop has been largely harvested in Texas and in Louisiana, but the second crop s still in the field and is still at risk of loss in both states. Harvesting will start to wind down in both states now. Mississippi and Arkansas producers are at harvest now. Yield reports and quality reports have been acceptable to many in Texas and are called good in Louisiana. The reports have been good in both Arkansas and Mississippi. Demand was improved last week over the previous week and was considered positive for prices.

Weekly Chicago Rice Futures

Palm Oil and Vegetable Oils: Palm Oil was lower Friday on long liquidation on the back of weaker Chicago SBO prices, but higher for the week as September export demand was very strong. India was the major importer as the country reduced import taxes. The weekly chart trends are turning up again. Ideas are that Palm Oil got too expensive when compared to the other vegetable oils markets. There are ideas of tight supplies due to labor problems. There are just not enough workers in the fields due to Coronavirus restrictions. Production has also been down to more than offset the export losses so prices have trended higher. Canola closed a little lower on Chicago price action as the harvest is underway amid good conditions in the Prairies. The losses were very moderate when compared to the price action in Soybeans. Farmers are bullish and reluctant to sell and would rather work in the fields. The weekly chart trends are sideways. Production ideas are down due to the extreme weather seen in these areas. It remains generally dry and warm in the Prairies. The Prairies crops are in big trouble now due to previous hot and dry weather.

Weekly Malaysian Palm Oil Futures

Weekly Chicago Soybean Oil Futures

Weekly Canola Futures:

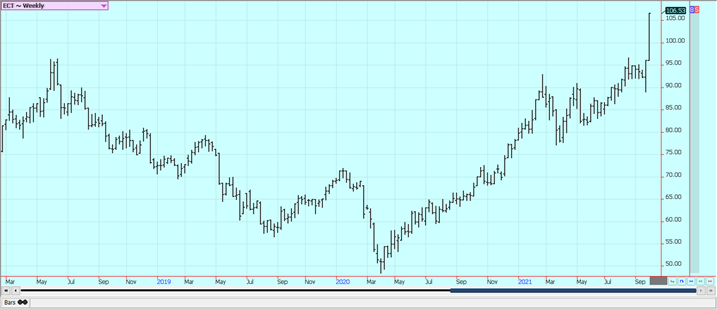

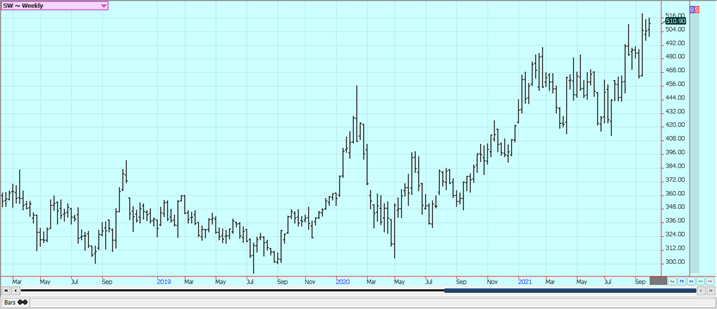

Cotton: Futures were lower on Friday but much higher for the week on ideas of strong demand and questions about supply. The weekly export sales report showed very st4rong sales with China the big buyer. The weekly charts imply that significantly higher prices are coming. Demand for US Cotton remains very strong and that is good news for sellers as the strong demand implies strong prices should continue. The demand is expected to be strong from Asian countries as world economies recover from Covid lockdowns. Analysts say the demand is still very strong and likely to hold at high levels for the future. However, the expansion of the Delta variant has given pause to the better demand ideas due to fears of economies here and around the world starting to partially lockdown again. Good US production is expected.

Weekly US Cotton Futures

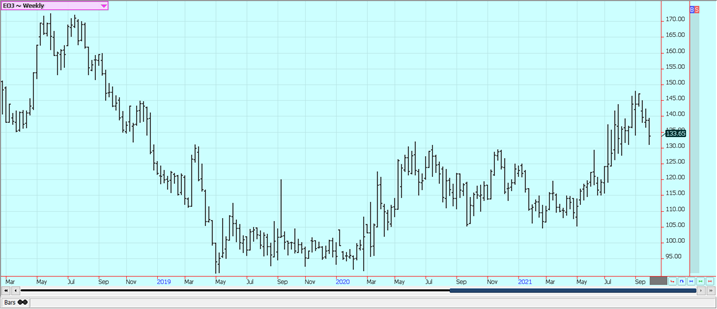

Frozen Concentrated Orange Juice and Citrus: FCOJ closed lower last week and chart trends are turning down as the weather remains generally good for production around the world. Weather concerns, especially for Brazil but also for Florida and Mexico, remained important. A freeze hit Sao Paulo state several weeks ago and reports of significant losses are being heard. It is now warm and dry, but some rain is in the forecast and flowering will be possible in the next couple of weeks. Weather conditions in Florida are rated mostly good for the crops with scattered showers and near-normal temperatures. Mexican crop conditions in central and southern areas are called good with rains, but earlier dry weather might have hurt production. Northeastern Mexico areas were too dry but have gotten good rains in recent weeks, and the rest of northern and western Mexico are rated in good condition. Florida is in the middle of the hurricane season but the storms have missed the state so far and crop conditions are good.

Weekly FCOJ Futures

Coffee: New York closed higher last week and London closed a little lower as tight supplies at origin is still the important fundamental. It remains a bull market on a lack of supplies available from origin and New York had explosive price action on Friday as stops were hit on the way up. New York has found support from the lack of Coffee available in Brazil after extreme weather events. It has been dry in Brazil and there has been a big freeze there. The temperatures are warm now and there are forecasts for rain over the next week to bring some flowering to the trees. No one is really sure just how much rain will fall in Coffee areas but many say there will be only spotty showers. London is having trouble sourcing Coffee from Vietnam due to a shortage of containers to carry the Coffee out of the country and as the country suffers from a resurgence of the Covid epidemic. Vietnam’s coffee exports in the first nine months of this year are expected to show a 4.2% drop from a year earlier to 1.2 million tons. Prices in New York have been firm as the current Brazil harvest starts to wind down. Scattered showers are now in the forecast for Southeast Asia. Good conditions are reported in northern South America and good conditions are reported in Central America. Conditions are reported to be generally good in parts of Africa.

Weekly New York Arabica Coffee Futures

Weekly London Robusta Coffee Futures

Sugar: New York and London were both lower on Friday but higher for the week and trends are trying to turn up again on the daily and weekly charts. Traders expect light deliveries of Sugar against October NY contracts. Ideas are that the supplies available to the cash market are rather slim. The reduced production potential from Brazil is still impacting the market. India is not offering as world prices are well below domestic prices. The ISO has noted that this will be the second year of deficit production for the world, in large part because of the Brazil freeze that cut production. Consumption of Sugar remains on the light side. Fears that Covid is coming back and could reduce economic activity and demand are still around. Thailand is expecting improved production. India has strong production but internal prices are higher than world prices even with big supplies on hand so exporters are quiet. It is raining in southern Brazil which will be good for crops there.

Weekly New York World Raw Sugar Futures

Weekly London White Sugar Futures

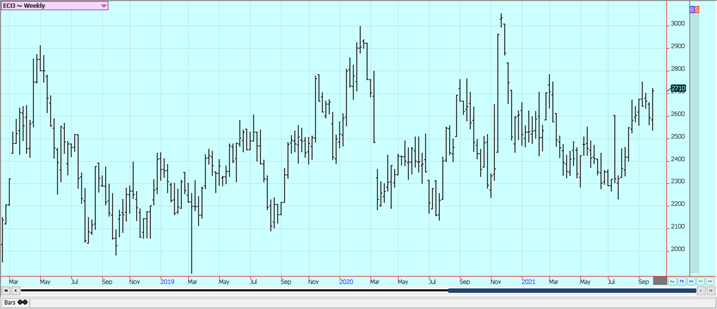

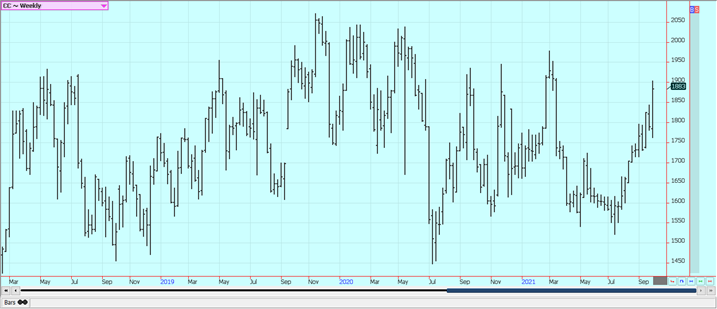

Cocoa: New York and London closed higher again Friday and were higher for the week on ideas of short West African production for the coming year. There are increasing concerns that Ghana will have less production this year. Ghana is the world’s second-largest producer behind Ivory Coast. World economies are starting to reopen after Covid and the open economies are giving demand the boost. The weather has had below-normal rains in West Africa and crop conditions are rated good for now but there is concern about the lack of rain. Drier weather will be beneficial for the harvest which will be underway soon. Some are forecasting less production in the coming year. Cocoa production in Ivory Coast is expected to drop by up to 11% in the 2021/2022 season that starts on Oct. 1 from the previous year.

Weekly New York Cocoa Futures

Weekly London Cocoa Futures

__

(Featured image by CJ via Pixabay)

DISCLAIMER: This article was written by a third party contributor and does not reflect the opinion of Born2Invest, its management, staff or its associates. Please review our disclaimer for more information.

This article may include forward-looking statements. These forward-looking statements generally are identified by the words “believe,” “project,” “estimate,” “become,” “plan,” “will,” and similar expressions. These forward-looking statements involve known and unknown risks as well as uncertainties, including those discussed in the following cautionary statements and elsewhere in this article and on this site. Although the Company may believe that its expectations are based on reasonable assumptions, the actual results that the Company may achieve may differ materially from any forward-looking statements, which reflect the opinions of the management of the Company only as of the date hereof. Additionally, please make sure to read these important disclosures.

Futures and options trading involves substantial risk of loss and may not be suitable for everyone. The valuation of futures and options may fluctuate and as a result, clients may lose more than their original investment. In no event should the content of this website be construed as an express or implied promise, guarantee, or implication by or from The PRICE Futures Group, Inc. that you will profit or that losses can or will be limited whatsoever. Past performance is not indicative of future results. Information provided on this report is intended solely for informative purpose and is obtained from sources believed to be reliable. No guarantee of any kind is implied or possible where projections of future conditions are attempted. The leverage created by trading on margin can work against you as well as for you, and losses can exceed your entire investment. Before opening an account and trading, you should seek advice from your advisors as appropriate to ensure that you understand the risks and can withstand the losses.

XRP Under Pressure Amid Macro Forces, Fed Policy, and Regulatory Shifts

XRP remains under pressure despite easing geopolitical tensions, as macroeconomic factors and Fed policy dominate market sentiment. Liquidations and high...

Edison Accelerates Renewable Growth and ESG Impact in 2025

Edison reports strong 2025 sustainability progress, boosting renewable investments by 90% to reach 2.3 GW toward a 4 GW 2030...

New Gene Therapies Transform Rare Disease Care, but Gaps Remain

Gene therapies are transforming rare disease treatment, enabling normal lives for some patients. However, only about 6% of 7,000 rare...

Temotiva Launches Crowdfunding Campaign to Advance Preventive Mental Health

Temotiva Innovación Lab has launched a crowdfunding campaign through Santander X Explorer, marking a new phase for the University of...

Fed Policy Shift Raises Concerns Over Debt and Inflation Risks

The Federal Reserve is criticized for resuming balance sheet expansion through Treasury purchases despite expectations of tighter policy under new...

|

|

|  |

|

|

-

Markets2 weeks ago

Markets2 weeks agoJobs Strength Triggers Market Reversal as Inflation and Rates Take Focus

-

Africa5 days ago

Africa5 days agoEgypt’s Net Foreign Assets Rise as External Position Continues Gradual Strengthening

-

Crypto2 weeks ago

Crypto2 weeks agoInstitutional Bitcoin Buying and LiquidChain Presale Signal Market Optimism

-

Crypto1 week ago

Crypto1 week agoBitcoin Rises on Iran Deal as Crypto Markets React to AI and SpaceX News