Business

Agricultural markets fare better as US seeks to end global trade disputes

The US-China trade talks continued. Enough progress was made that the US, including the president, made noises about postponing and increase in tariffs.

Everyone is waiting for the resolution of the US-China trade dispute. China is apparently willing to buy a lot of US agricultural goods, with some wire services stating that it could buy between $45 and $50 billion each year. The intellectual property rights and forced technology transfers as well as Chinese structural reforms remain key sticking points and will need much more time to be negotiated.

The US is also moving to resolve trade disputes with the EU, Japan, and others and the administration still needs to find a way to get the new North American trade agreement ratified by Congress.

Wheat

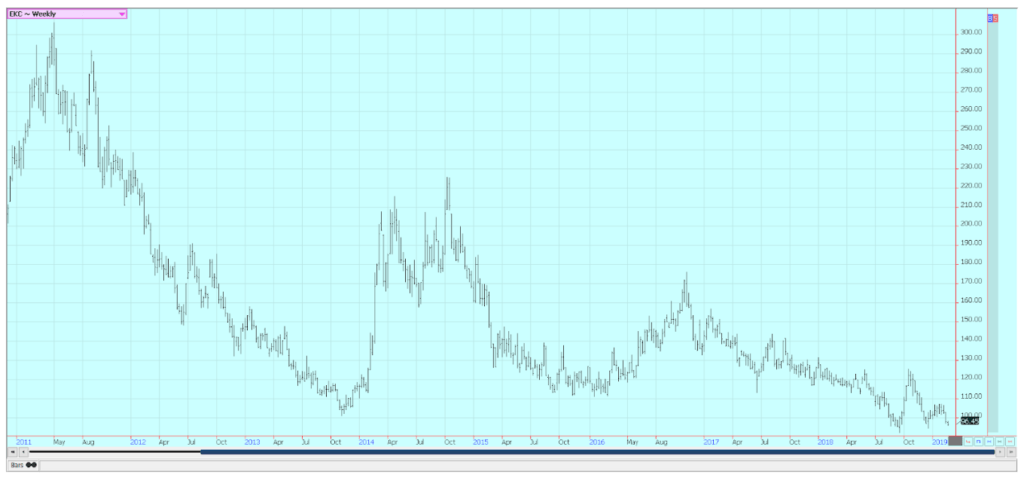

Winter wheat markets were mostly a little higher on Friday, but lower for the week. World wheat prices were softer as well. USDA released its export sales report that covered the month of January, and wheat export sales were very strong and well above any trade projections. Sales of hard red winter made up about half of the demand, and sales of spring and white wheat were very strong as well. Soft red winter sales were the weakest component of the report.

USDA also released its Outlook Conference estimates for the coming marketing year. Production was estimated at 1.902 billion bushels with slight changes made to planted and harvested area and yield. Domestic demand was increased slightly, but export projections were slightly lower. Ending stocks were estimated at 944 million bushels, below a billion bushels for the first time in a couple of years but still very high.

Minneapolis spring wheat markets held firm amid very cold weather in the northern US Great Plains and the Canadian Prairies as well as on the better than expected export demand. The fall season in both winter wheat regions featured a lot of rain that hurt harvest and planting all season long. Wet weather has continued for much of the Winter, and it is likely that the crop will have good soil moisture to work with as it comes out of dormancy in the next month.

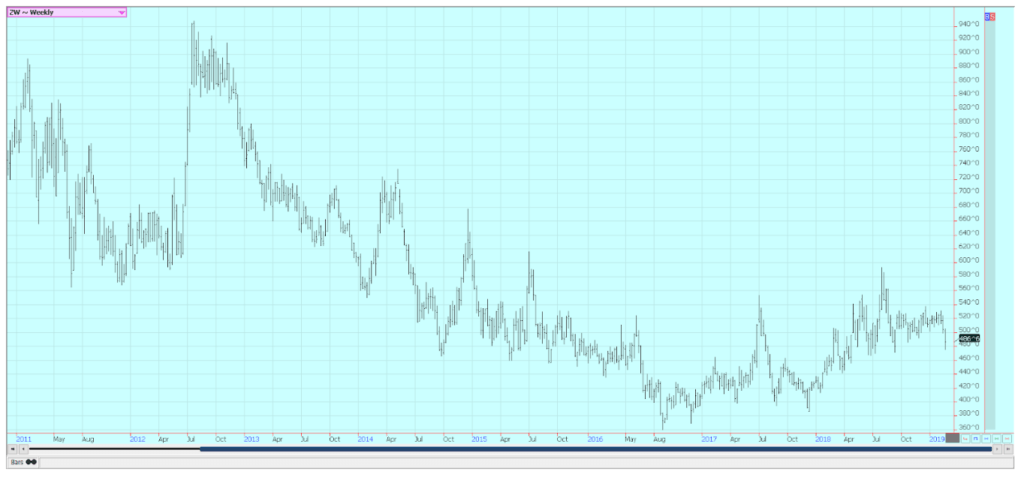

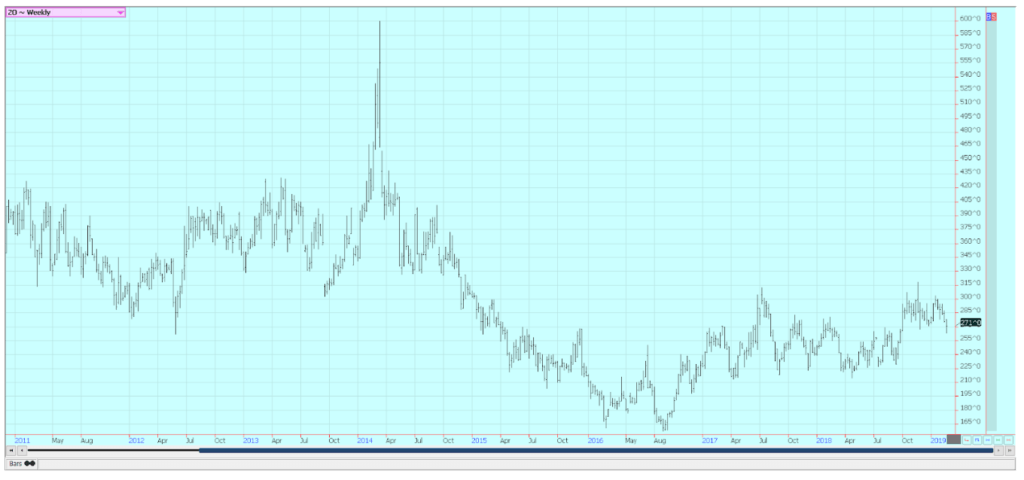

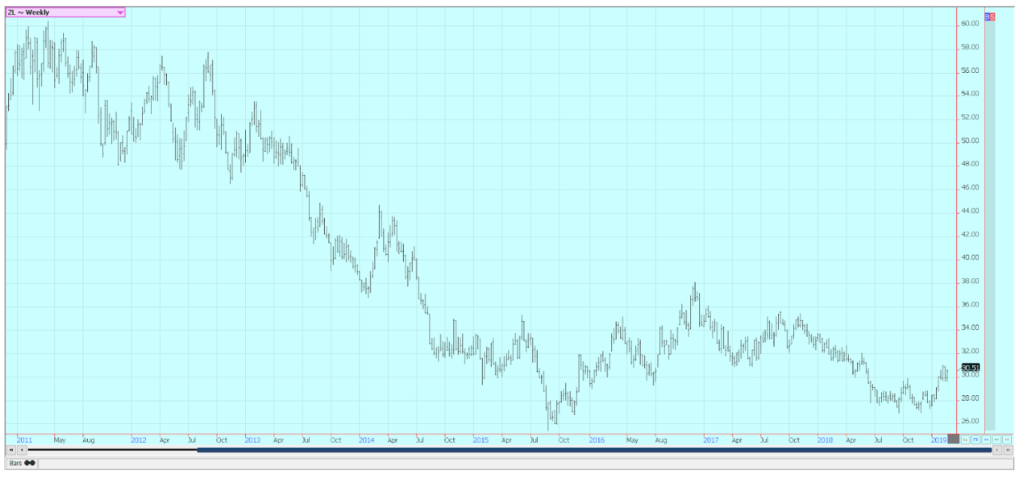

Weekly Chicago Soft Red Winter Wheat Futures ©Jack Scoville

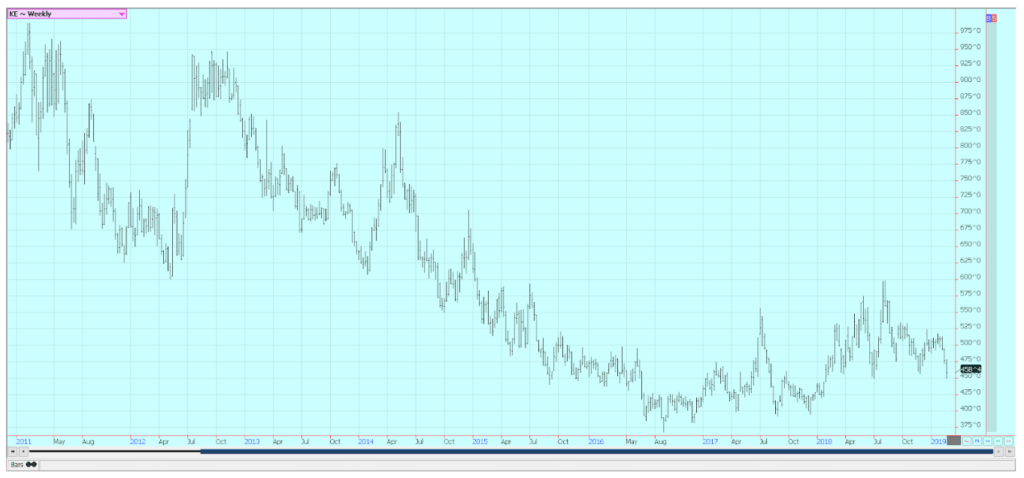

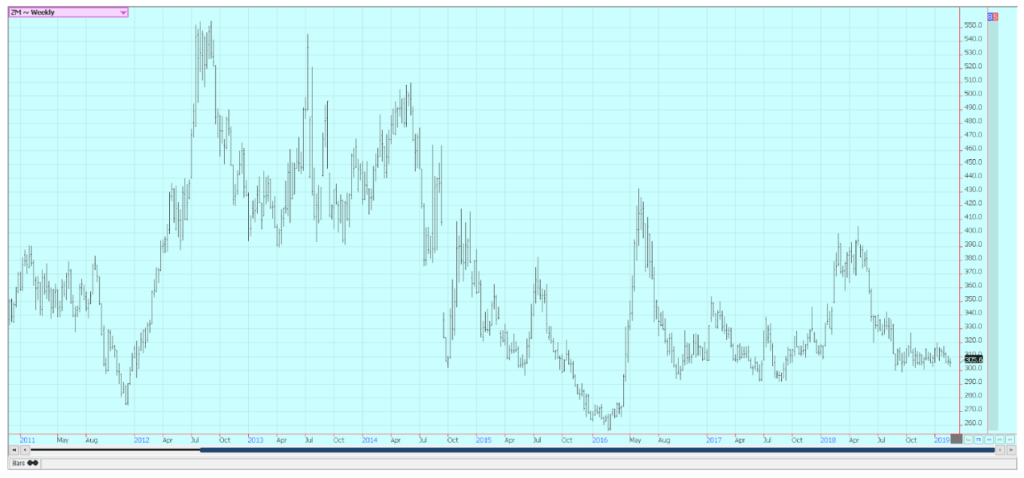

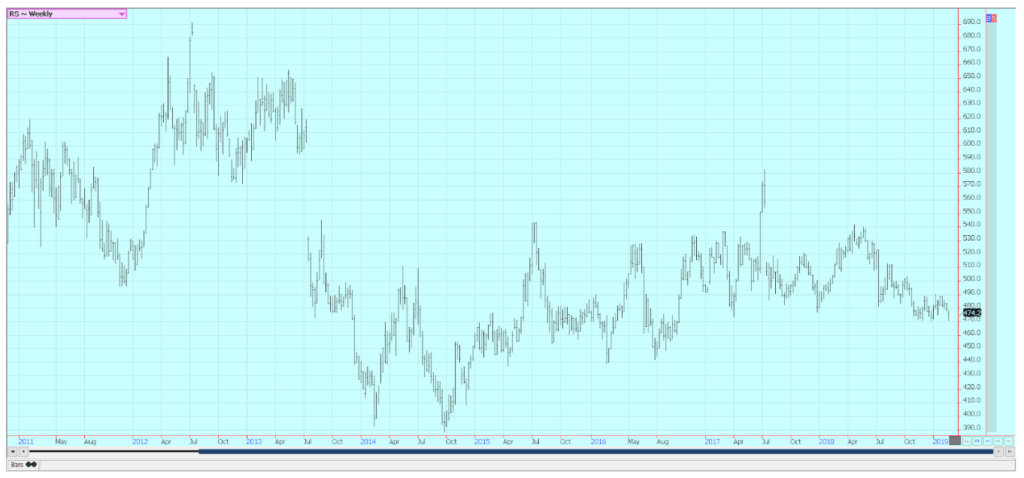

Weekly Chicago Hard Red Winter Wheat Futures ©Jack Scoville

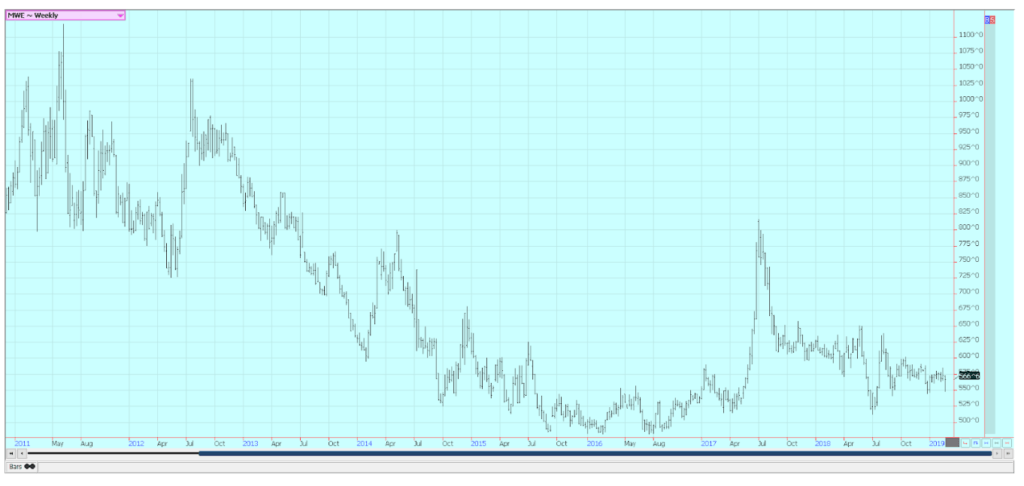

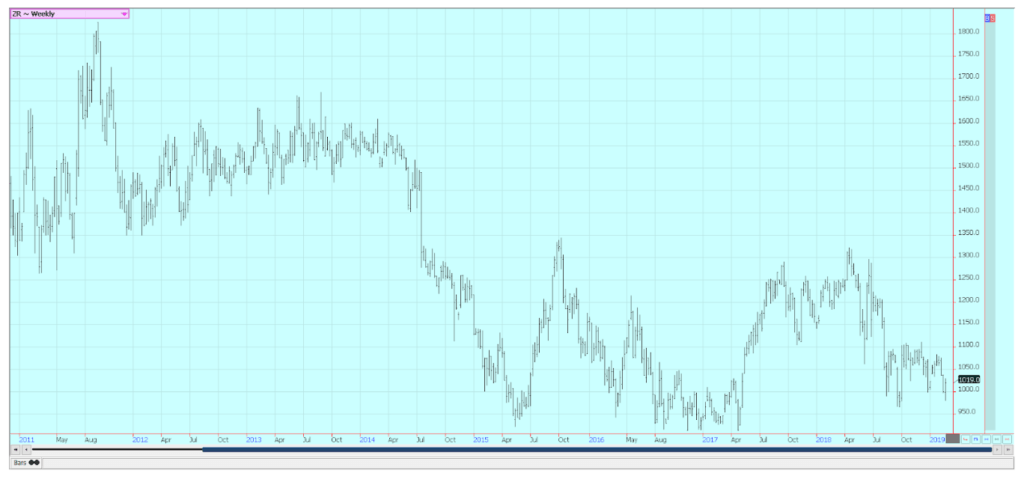

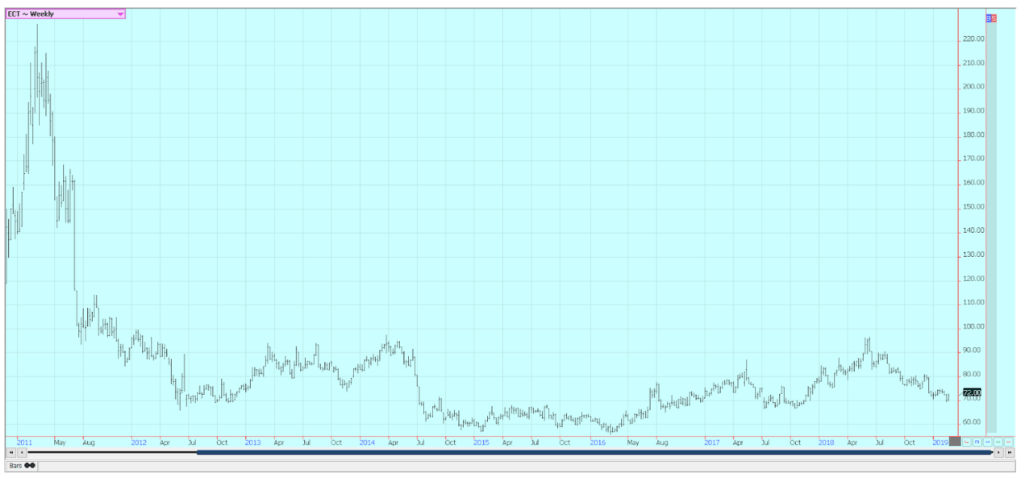

Weekly Minneapolis Hard Red Spring Wheat Futures ©Jack Scoville

Corn

Corn closed about unchanged for the week for the second week in a row on Friday. Oats were near unchanged on Friday, but a little lower for the week. USDA caught up with the weekly export sales reports on Friday as it released a month of data. Export sales were over 6.0 million tons and were at the high end of trade expectations. USDA released its statistically derived planted area and supply and demand estimates late last week. The outlook should help support relatively strong corn prices. Planted area was estimated at 92 million acres, from 89.1 million acres last year.

Yield estimates were trimmed slightly to 176 bushels per acre, and production was estimated at 14.890 billion bushels. Domestic use should be strong than the current marketing year at 12.540 billion bushels and exports could be slightly stronger at 2.475 billion bushels. Ending stocks are estimated lower at 1.650 billion bushels, and are tight enough that any production problems such as bad weather could realty change the supply and price outlook. South American weather is generally good as more showers are reported in central and northern Brazil. The winter corn crop is being planted as soybeans get harvested, so the rains are very beneficial after an extended dry season.

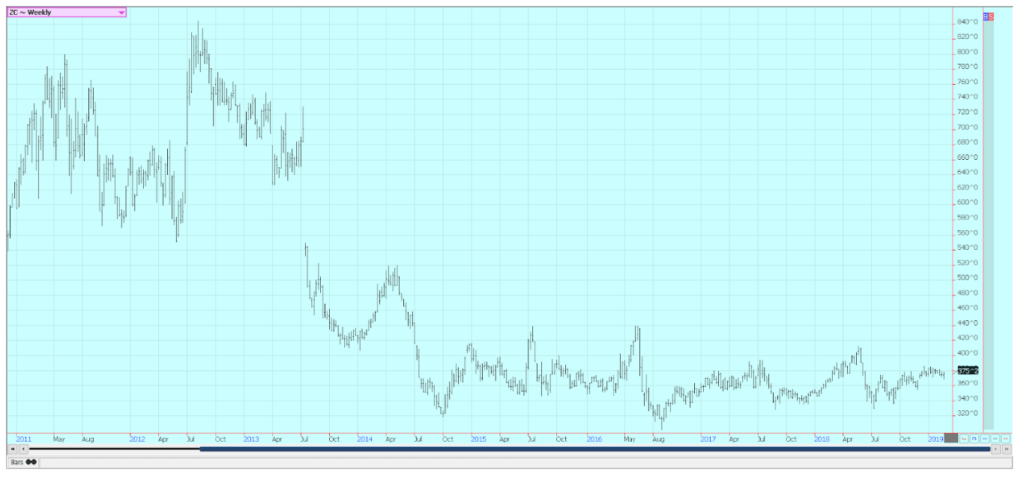

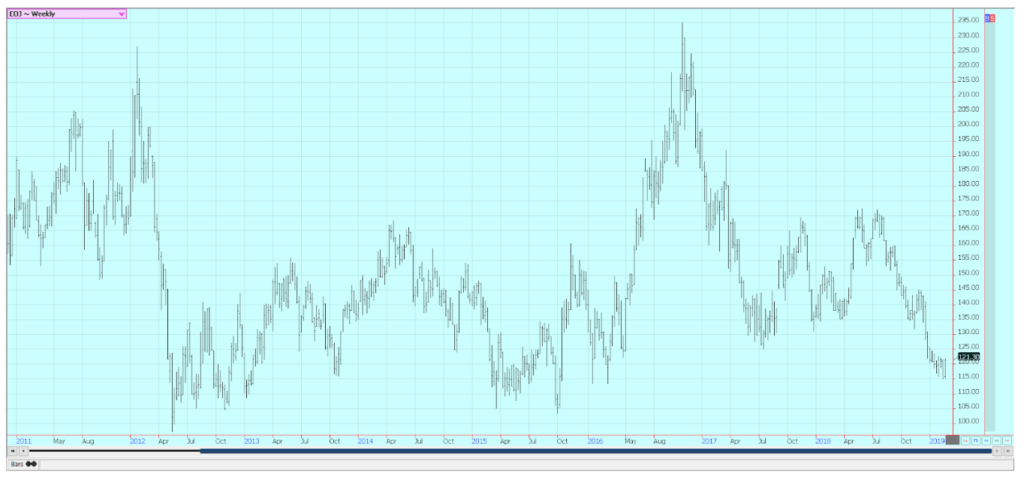

Weekly Corn Futures ©Jack Scoville

Weekly Oats Futures ©Jack Scoville

Soybeans and soybean meal

Soybeans were a little higher and Soybean Meal were slightly lower last week. Soybean oil was higher and the strength of the complex. USDA released its weekly export sales report that covered all weeks in January, and sales for soybeans and soybean meal were strong. Soybeans sales were at the lower end of trade expectations, but featured big sales to China as expected. Soybean meal sales were very strong and higher than expected. USDA also released its estimates for the coming production year at its Outlook Conference. Soybeans planted area was reduced as expected, and yield was trimmed to 49.5 bushels per acre for production of 4.175 billion bushels. USDA increased domestic use and export estimates from the current year and estimated ending stocks at 845 million bushels.

The ending stocks are still high, but certainly no higher than expected and are down from an estimated 910 million bushels this year. Wire services said that China had offered to buy another 10 million tons of US soybeans as a good will gesture.

Weekly Chicago Soybeans Futures ©Jack Scoville

Weekly Chicago Soybean Meal Futures ©Jack Scoville

Rice

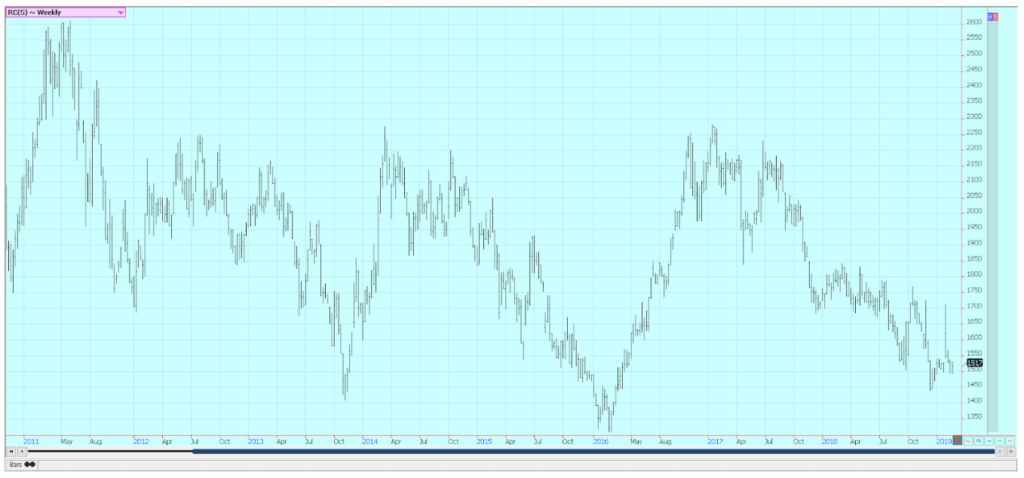

Rice was a little lower on Friday, but higher for the week. Futures made new flows for the move early in the week before reversing. USDA released a months worth of weekly export sales reports and the data showed good demand for US Rice. Much of the demand was for long grain. Colombia was the best buyer for the month, and Latin America was the featured buyer overall. USDA announced its Outlook Conference planted area and supply and demand estimates for the coming year. Planted area was estimated at 2.66 million acres, in part due to the low prices and in part due to the tough harvest last Fall. It is still raining in most rice production areas, and initial fieldwork is not really getting done. Planted area was lower than the trade had expected, and might god lower yet unless the weather gets better or the prices show significant improvement.

USDA showed improved yield potential in its estimates, but production of all rice was estimated lower at 203 million hundredweight. Domestic demand estimates are unchanged from a year ago, but export demand was increased for an overall increase in demand. Ending stocks are estimated lower than the current year at 41.9 million hundredweight, but will be large enough to suggest that there will not be any shortages of rice for the coming year. Private sources suggest that domestic mills are slowly but surely getting covered on needs for the current crop year.

Weekly Chicago Rice Futures ©Jack Scoville

Palm oil and vegetable oils

World vegetable oils prices were mixed, with soybean oil higher and the other markets lower. Soybean oil found support from stronger demand. USDA at its Outlook Conference showed the potential for strong domestic demand for soybean oil. Most of the new demand would come for biofuels. Export demand was cut, and ending stocks projections showed little change on a year to year basis. The chart patterns for soybean oil are positive on the daily charts and sideways on the weekly charts.

Palm oil closed lower and the weekly charts show a failure to penetrate resistance areas. Export demand for February had started off on a very strong note and was well above January, but the latest data from the private surveyors showed that demand has slipped behind the January pace. There is talk that production has held together better than expected. Palm oil production usually turns down at this time of year, but so far this does not seem to be happening this year. Canola was weaker on ideas of weaker demand and big supplies. Farmers are trying to sell and clean out some bins before the Spring season gets underway, but are finding only routine demand or less.

Weekly Malaysian Palm Oil Futures ©Jack Scoville

Weekly Chicago Soybean Oil Futures ©Jack Scoville

Weekly Canola Futures ©Jack Scoville

Cotton

Cotton was higher last week, but sharply lower on Friday. Trends are still mostly down on the daily and the weekly charts. The weekly export sales reports have started to show improved demand for US cotton, and USDA showed overall January demand was almost one million bales. The demand did not feature much in the way of buying from China, but did feature big sales to Turkey and South and Southeast Asia. The Outlook Conference estimates were bearish for prices. Production was estimated significantly higher, and even increased export demand was not enough to offset the big production. Ending stocks were estimated neart 6.3 million bales.

World ending stocks levels not including China were also estimated a little higher at 76.5 million bales. Chinese ending stocks were estimated lower at 287 million bales as it works down its internal supplies. There had been talk of less production from exporter countries like India. Indian and Pakistani sources will continue to insist that production is less than projected by USDA. Cotton futures will have to look for news to cause rallies at this time.

Weekly US Cotton Futures ©Jack Scoville

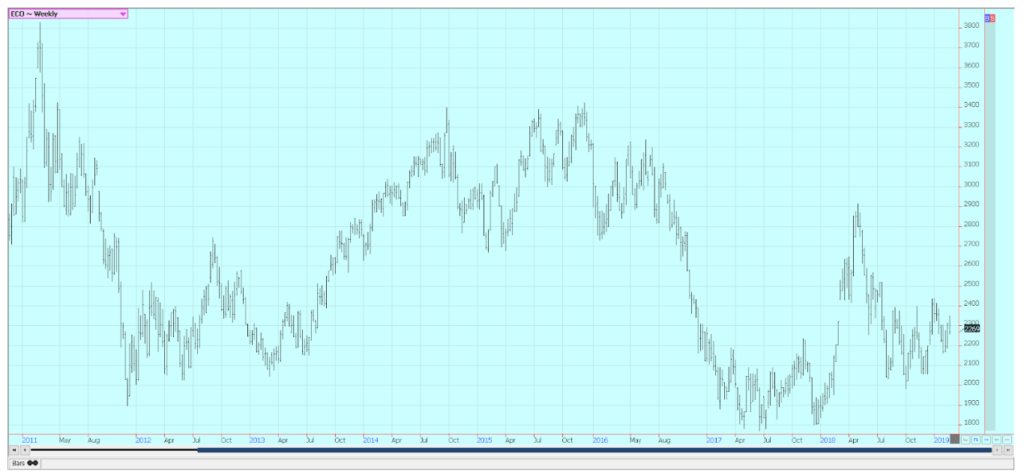

Frozen concentrated orange juice and citrus

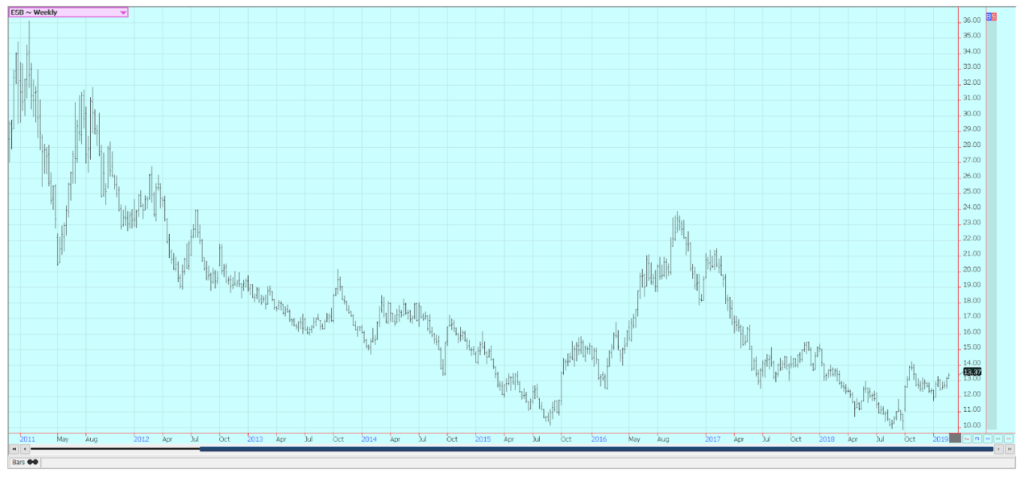

FCOJ was higher and closed near the recent highs on the daily and weekly charts. Trends are sideways on the weekly charts, but moves higher could easily turn trends up and create a seasonal low. The market has absorbed speculative long liquidation and producer selling through the winter as no freeze has developed, and futures can now move seasonally higher. Longer range forecasts show that there is little chance for a freeze to develop this month, and then it will be getting to be too late for a freeze to be seen in the state of Florida. The oranges harvest is active in Florida as the weather is warm and mostly dry.

The fruit is abundant. Florida producers are seeing small sized to good sized fruit, and work in groves maintenance is active. Irrigation is being used in all areas. Packing houses are open to process fruit for the fresh market, and all processors are open in the state to take packing house eliminations and fresh fruit. Mostly good conditions are reported in Brazil, and some beneficial rains should be seen this week.

Weekly FCOJ Futures ©Jack Scoville

Coffee

Futures were lower for the week in New York and in London. New York trends are down. Weekly chart trends are sideways in London. January export data from Brazil was very strong and much above expectations, and ideas of big supplies have kept speculators on the sell side of the market. Brazil should be getting past the gut slot of its harvest, and the strong export pace from the country should start to turn down. Brazil had a big production year for the current crop, but the next crop should be less as it is the off year for production.

Ideas are that the current production of 62 or 63 or more million bags can become about 52 million bags next year. El Nino is fading, but remains in the forecast, and coffee areas in Brazil could be affected by drought that could hurt production even more. Showers are in the forecast for this week. Vietnam is active in its harvest. Selling will increase this week as the Lunar New Year holiday is now over. Production in Vietnam is estimated less than 30 million bags due to uneven weather during the growing season.

Weekly New York Arabica Coffee Futures ©Jack Scoville

Weekly London Robusta Coffee Futures ©Jack Scoville

Sugar

Both markets were higher for the week. Chart patterns on the weekly charts in both markets imply that higher prices are coming. The fundamentals still suggest big supplies, but the turn in the trends on the weekly charts might be a signal that a change in the fundamentals is coming. Reports that Brazilian mills might pause and give sugarcane production a chance to improve helped support the market.

Brazil weather is improving in all areas as there is less rain in southern areas and more to the north. Petroleum futures strength seems to be helping change the tone in sugar. Brazil has been using the majority of its Sugarcane harvest to produce ethanol this year instead of sugar. Very good conditions are reported in Thailand.

Weekly New York World Raw Sugar Futures ©Jack Scoville

Weekly London White Sugar Futures ©Jack Scoville

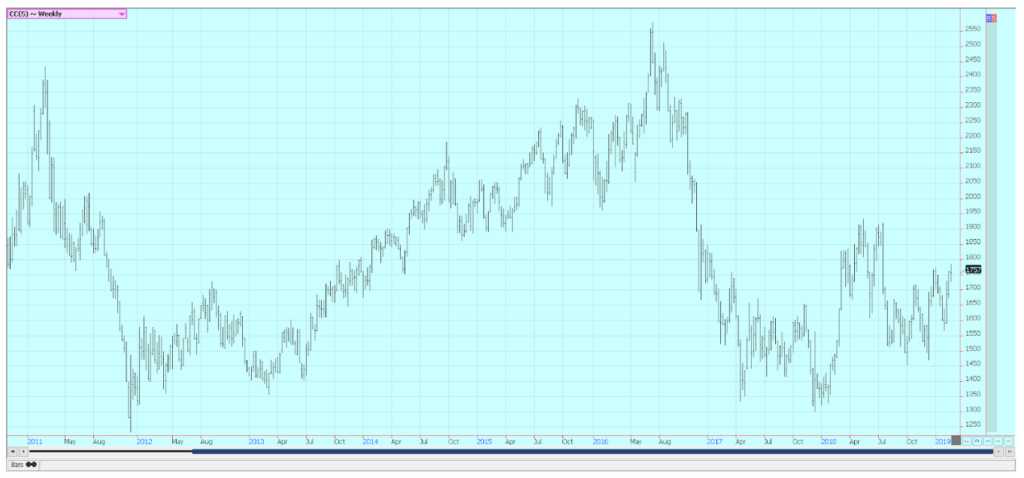

Cocoa

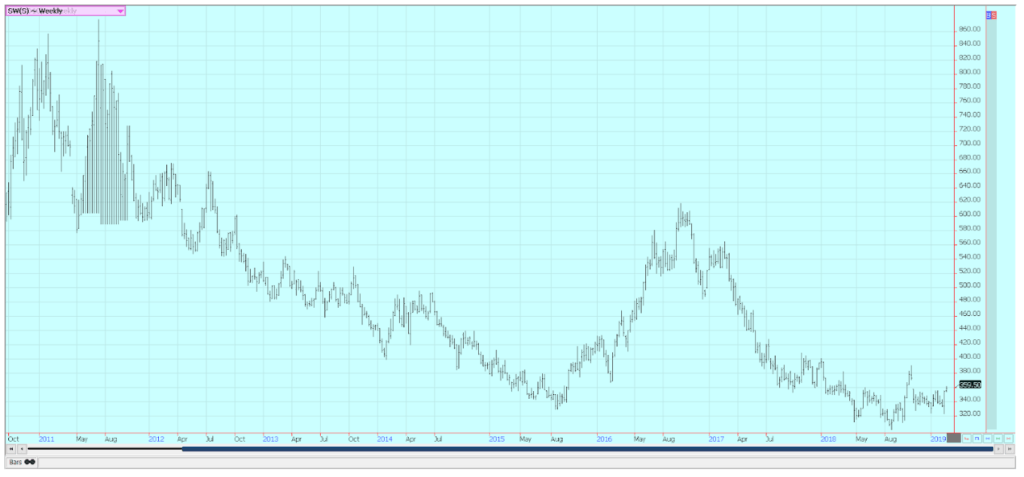

Futures closed higher for the week in New York and slightly lower in London as the new main crop harvest comes to an end in West Africa. The mid crop harvest is still a month or more away. Trends are up, but the market is having trouble holding the trend and a period of consolidation trading could be coming. The main crop harvest is active in West Africa, and Ivory Coast arrivals are strong. However, arrivals have started to fade. The weekly pace just a month or two ago was about 15% ahead of a year ago and now is under 10% of a year ago.

Some early week showers and cooler temperatures were beneficial, it is warmer now and mostly dry. Nigeria is reporting losses to its crops due to recent dry weather. Cameroon is also reporting less production and prices there are reported strong. Conditions appear good in East Africa and Asia. Demand is said to be improving as offers from the new harvest stay strong overall.

Weekly New York Cocoa Futures ©Jack Scoville

Weekly London Cocoa Futures ©Jack Scoville

(Featured image by DepositPhotos)

—

DISCLAIMER: This article expresses my own ideas and opinions. Any information I have shared are from sources that I believe to be reliable and accurate. I did not receive any financial compensation for writing this post, nor do I own any shares in any company I’ve mentioned. I encourage any reader to do their own diligent research first before making any investment decisions.

XRP Under Pressure Amid Macro Forces, Fed Policy, and Regulatory Shifts

XRP remains under pressure despite easing geopolitical tensions, as macroeconomic factors and Fed policy dominate market sentiment. Liquidations and high...

Edison Accelerates Renewable Growth and ESG Impact in 2025

Edison reports strong 2025 sustainability progress, boosting renewable investments by 90% to reach 2.3 GW toward a 4 GW 2030...

New Gene Therapies Transform Rare Disease Care, but Gaps Remain

Gene therapies are transforming rare disease treatment, enabling normal lives for some patients. However, only about 6% of 7,000 rare...

Temotiva Launches Crowdfunding Campaign to Advance Preventive Mental Health

Temotiva Innovación Lab has launched a crowdfunding campaign through Santander X Explorer, marking a new phase for the University of...

Fed Policy Shift Raises Concerns Over Debt and Inflation Risks

The Federal Reserve is criticized for resuming balance sheet expansion through Treasury purchases despite expectations of tighter policy under new...

|

|

|  |

|

|

-

Fintech2 weeks ago

Fintech2 weeks agoGerman Fintech Investment Slumps as AI Becomes Key Focus

-

Crypto4 days ago

Crypto4 days agoCrypto Market Stays Stable as Bitcoin and Ethereum See Mild Declines

-

Crowdfunding2 weeks ago

Crowdfunding2 weeks agoSustainable Restoration of the Haus Hövener Garden in Brilon

-

Cannabis6 days ago

Cannabis6 days agoEurope’s Cannabis Shift: Rising Use, and New Risks