Business

USDA reports a lower trade of market wheat, corn and oats last week

Increased sugar stocks offset a dip in the trade market of wheat, corn and oats. Changes in production and usage predict accountability in the next months.

Wheat

US markets closed lower on Friday and lower for the week in response to the USDA planted area estimates. USDA showed higher than the expected planted area for all three classes of Winter Wheat. Minneapolis is Spring Wheat, but it fell in sympathy with the Chicago markets. Total Winter Wheat area is still small, but at 32.6 million acres it is not as small as the trade guess of 31.4 million acres. The market is noting dry conditions in western Kansas and other parts of the western Great Plains and the La Nina Winter weather forecast.

A drought remains in the region and could become serious. The crop has not established itself well due to the dry weather. World estimates, in general, remain large and even reduced US production cannot change this fact very much. US prices will need to remain competitive with European and Russian prices to get much business, and Russian prices remain the lowest in the world right now. The weekly charts show that both Winter Wheat markets and Minneapolis Spring Wheat markets remain in sideways trends. Futures in Winter Wheat are at low prices and are backtesting important support areas now. Minneapolis prices are also holding just above important support areas on the weekly charts.

Weekly Chicago Soft Red Winter Wheat Futures © Jack Scoville

Weekly Chicago Hard Red Winter Wheat Futures © Jack Scoville

Weekly Minneapolis Hard Red Spring Wheat Futures © Jack Scoville

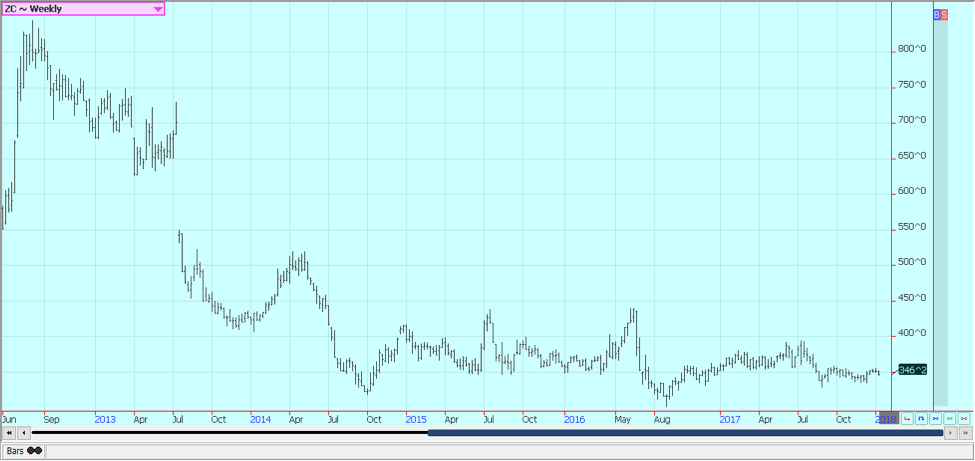

Corn

Corn closed a little lower and oats closed slightly higher last week. Corn futures closed a little lower on Friday in response to the USDA reports. The reports did not show anything new but gave no reason to buy. USDA showed a slight yield increase and slightly higher production last year when compared to most trade estimates. US production last year was estimated at 14.604 billion bushels, up from the USDA estimates of 14.578 billion in November, but less than the 15.140 billion produced last year. US ending stocks were estimated at 2.477 billion bushels and world stocks were estimated at 206.6 million tons, both higher than previous estimates.

Stocks as of December 1 were estimated at 12.514 billion bushels. CONAB in Brazil estimated Corn production for the current year at 92.3 million tons, down from 97.8 million tons last year. The higher US production was somewhat of a surprise as many in the trade had expected slightly less production as had been the USDA tendency in the past few years. This year it found a little more corn instead of a little less.Overall demand for corn remains good, and demand for other feed grains such as sorghum and oats is strong. Demand in the US has been very strong from the ethanol sector and USDA will still likely need to increase corn consumption from this sector again this month in the supply and demand updates that will be released next month. It made no changes to ethanol demand last week. It could easily add another 25 million bushels to the demand side of the data.

Questions continue about corn demand from the feed sector, but the animals are out there to feed. The trade is still looking at the dry weather in southern Brazil and Argentina. Forecasts for this week are hot and dry again, with the biggest problems in Argentina. Ideas of big supplies and weaker demand keep pulling the market down fundamentally, and it has been the funds who have established a huge and near record short position in futures. Farmers have reportedly sold some corn for the end of the year cash and tax considerations. Not much selling is reported in South America. US prices are cheap now and trends in the market are sideways.

Weekly Corn Futures © Jack Scoville

Weekly Oats Futures © Jack Scoville

Soybeans and Soybean Meal

Soybeans and products were higher in reaction to the USDA reports. USDA cut yields and left harvested area unchanged for lower than expected production at 4.392 billion bushels. US ending stocks projections were a little lower than expected at 470 million bushels, and world stocks were lower than expected at 98.6 million tons. The lower stocks levels came even as USDA reduced export demand by 65 million bushels due to the strong competition this year from Brazil and Argentina in the world market and some concerns about the quality of US Soybeans produced last year.

Stocks as of December 1 were a Little higher than expected and were just above 3.15 billion bushels. On Thursday, CONAB estimated Brazil Soybeans production at 110.4 million tons, which should be about in line with trade expectations. Traders had expected bearish reports for Soybeans, with many saying that the US ending stocks levels could be well over 500 million bushels because of the weak demand. USDA has accounted for the weaker demand and still kept ending stocks levels at much more moderate levels than the most bearish trade expectations. Ideas that Soybeans production in southern Brazil and Argentina are still suffering from dry weather are still the main features of the market. However, there are rain forecasts for next week in the driest areas, so some of the recent buyers started to sell. Northeast Brazil has also been dry and is missing out on the current rains.

Weekly Chicago Soybeans Futures © Jack Scoville

Weekly Chicago Soybean Meal Futures © Jack Scoville

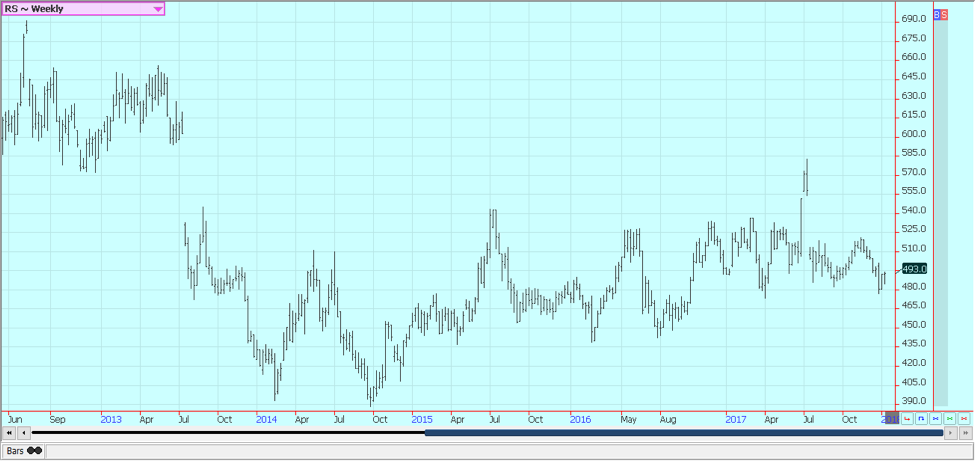

Rice

Rice closed higher in reaction to the USDA reports. USDA cut production estimates and also current supplies in the data on Friday. The monthly supply and demand updates showed that less export demand should be expected, so ending stocks were lower on a month to month basis, but not as much as the reduced production and current supplies would have implied. It was still a Price friendly report. USDA also cut its average farm prices on Friday, but current futures prices are below the cash market and remain below the average prices expected by USDA. The charts show that futures held to the short-term trading range on Friday, but the charts still present a weaker

The cash market remains rather quiet. Futures market fundamentals have not really changed, but traders are leaving the market as the open interest has been dropping. The situation for rice remains somewhat bullish at this time.

Weekly Chicago Rice Futures © Jack Scoville

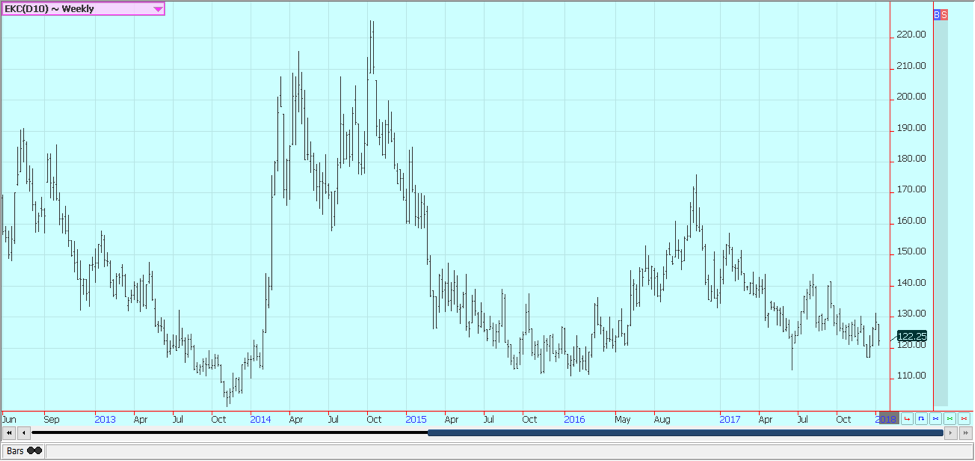

Palm Oil and Vegetable Oils

World vegetable oils prices were generally lower last week. Palm Oil found selling interest in response to the strong supply estimates released by MPOB in Malaysia. It said that December production was 1.83 million tons, which was less than expected. Export demand was so0lid, but below trade expectations at 1.42 million tons, and ending stocks were above trade expectations at 2.73 million tons. Palm Oil had been trading higher on stronger than expected export demand in Malaysia as reported by the private sources. There are hopes that the stronger demand can extend into this month.

Trends in Palm Oil are down on the daily charts. Canola markets have firmed and could turn into a trading affair. It is warmer in the Prairies this week and the harvest is over, so farmers are not as willing to sell. However, deliveries to elevators have been strong due in part to forward selling earlier in the year. US demand for Soybean Oil in biofuels should remain strong as the US moved to put punitive tariffs on imports from Indonesia and Argentina.

Weekly Malaysian Palm Oil Futures © Jack Scoville

Weekly Chicago Soybean Oil Futures © Jack Scoville

Weekly Canola Futures © Jack Scoville

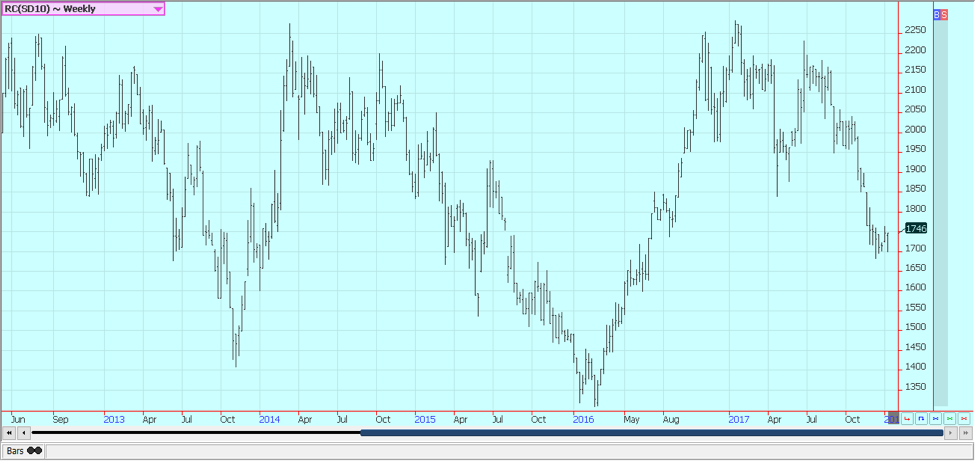

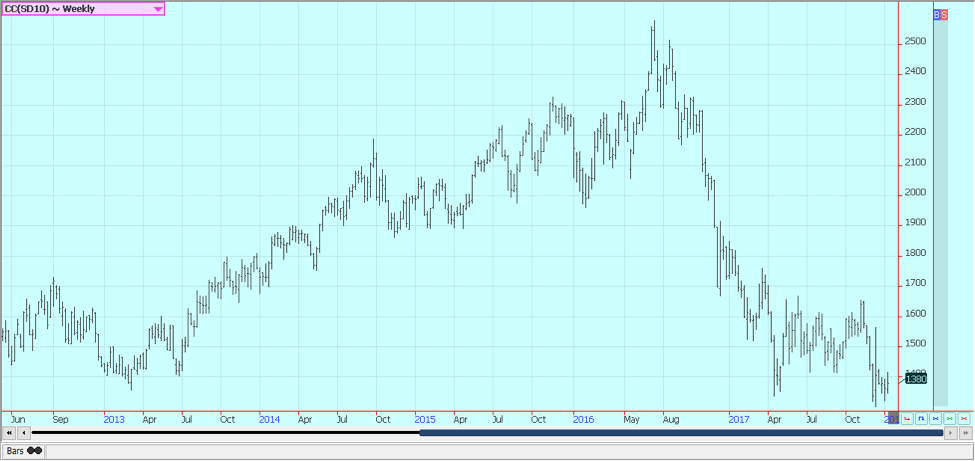

Cotton

Cotton was higher again last week and nearby months made new contract highs before the market collapsed on Friday in response to the USDA reports that showed ample production and supplies for the US. World ending stocks were higher than expected as USDA increased Chinese supplies and cut Indian supplies less than expected. The reports show that there is plenty of Cotton here and around the world, but getting it out of producers hands has been difficult and prices have been much higher than most commercials had expected. Commercials are being forced now to buy Cotton at higher levels to cover the big on-call position of unpriced Cotton that they have contracted for. Trends are still up. The Cotton quality has been dropping as the harvest is over, and the lower quality seems to be the biggest effects from the hurricanes seen during the growing season and then the freeze in the west at the tail end of the growing season. Farmers are reported to be quiet sellers right now.

Weekly US Cotton Futures © Jack Scoville

Frozen Concentrated Orange Juice and Citrus

FCOJ closed lower as it waits for some news to counter the overall good Florida weather and lack of consumer demand. Overall weather conditions are considered good in Florida at this time, with mostly dry and warm conditions. The harvest is progressing well and fruit is being delivered to processors and the fresh fruit packers. Trees in Florida that are still alive now are showing fruits of good sizes, although many have lost a lot of the fruit. Florida producers are actively harvesting and performing maintenance on land and trees. Processors are getting packinghouse eliminations along with taking mostly field-run fruit. FCOJ processors are also getting imports from Brazil, Mexico, and Europe.

Weekly FCOJ Futures © Jack Scoville

Coffee

Futures were lower in New York and in London for the first part of last week. The market was able to recover at the end of the week as New York held a support zone on the charts. New York traders are noting the good weather currently being reported in Brazil and expect another bumper crop. The ICO did nothing to help supply bulls last week when it increased world supply estimates by a couple of million bags. London remains in a trading range. Internal prices in Vietnam remain at high levels compared to London. The situation seems little changed in Latin America.

Brazil exports are reduced at about 2.8 million bags on what is called reduced inventories held by exporters and producers. Many are concerned about the potential for reduced Brazil production due to earlier drought and the cold and dry Winter, although some exporters suggest that the loss potential has been greatly overestimated. There is plenty of rain in some areas now. There are also reports of short crops in parts of Central America and some areas in South America due to the lack of farmer investment from the low prices. However, Honduras has been a very active exporter and appears to be in a position to make up the difference in exports from reduced offers in the rest of Central America and Colombia.

Weekly New York Arabica Coffee Futures © Jack Scoville

Weekly London Robusta Coffee Futures © Jack Scoville

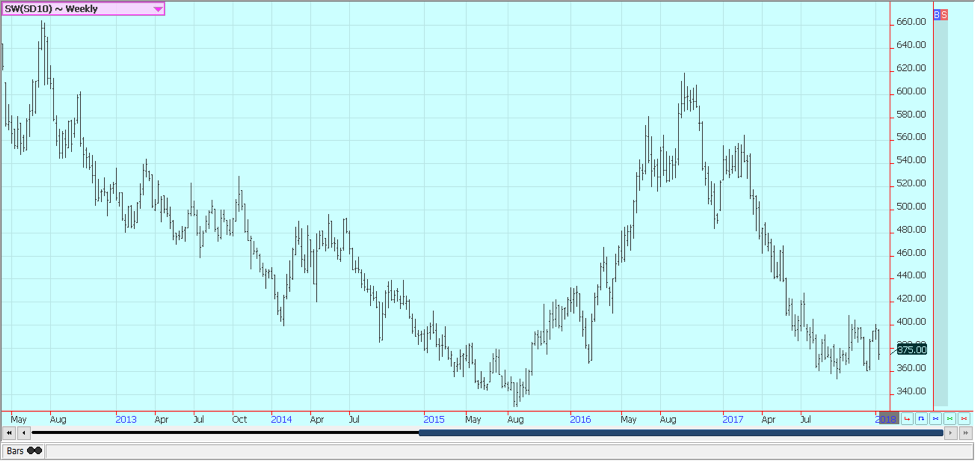

Sugar

Futures were lower last week and trends are sideways to down on the daily and weekly charts. Price action had been strong due to the strong demand for ethanol that has diverted some Brazil mill production away from Sugar. However, prices fell apart as resistance on the charts could not be breached and on forecasts for excessive production from the ISO and from private analytical firms. Mills in Brazil have decided to make more Ethanol as world Crude Oil and products prices have been very strong. Ideas are that these prices can continue strong as OPEC and Russia have agreed to keep production constrained compared to world demand. There are also ideas that index funds will add significantly to long positions in the rebalancing operations at this time. The rebalancing could cause significant new buying for the market. This buying was not seen last week and might not appear.

Weekly New York World Raw Sugar Futures © Jack Scoville

Weekly London White Sugar Futures © Jack Scoville

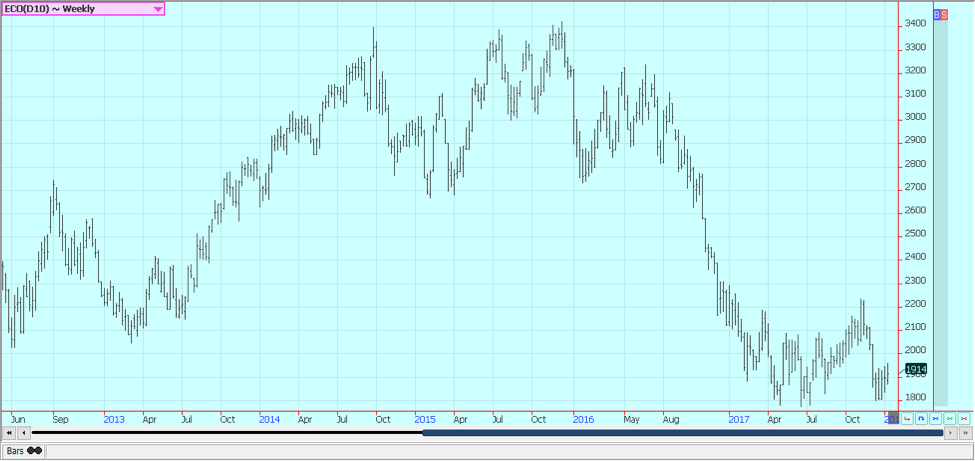

Cocoa

Futures closed lower in New York and lower in London last week. Trends are sideways in both markets for the short term. Weekly charts show that New York might be forming a bottom. Arrivals have been good in West Africa and are reported to be good in Southeast Asia so far this season. However, arrivals in West Africa have been behind year-ago levels when they were expected to be above year-ago levels. Ghana purchases have been about as expected. Prices are weak overall due to the ongoing harvest but have found some good buying interest at current levels as some are now viewing the market as cheap. Current prices in New York remain close to lower levels seen for at least five years. World supply ideas remain high. Harvest reports show good production will be seen this year in West Africa. The growing conditions in other parts of the world are generally good. East Africa is getting better rains now. Good conditions are still seen in Southeast Asia and harvest should be strong now amid mostly dry weather.

Weekly New York Cocoa Futures © Jack Scoville

Weekly London Cocoa Futures © Jack Scoville

_

DISCLAIMER: This article expresses my own ideas and opinions. Any information I have shared are from sources that I believe to be reliable and accurate. I did not receive any financial compensation in writing this post, nor do I own any shares in any company I’ve mentioned. I encourage any reader to do their own diligent research first before making any investment decisions.

Eli Lilly Hits $1 Trillion Valuation Amid Strong Bullish Momentum

Eli Lilly stock hit a record high, surpassing $1 trillion market value after strong product demand. Shares surged over 7%,...

BOAD Approves Major Funding Boost to Drive West African Development

At its 151st session in Lomé, BOAD approved eleven operations worth 344.577 billion FCFA, raising total financing since 1973 to...

Oil Surges on U.S.–Iran Tensions as Global Markets Show Diverging Trends and Rising Risk Fears

Rising U.S.-Iran tensions expose a fragile agreement, likely pushing oil prices higher while pressuring stocks and gold. Markets show mixed...

Dow Jones Near Highs Signals Strength Until Volatility Returns

The Dow Jones stayed below all-time highs all week, signaling continued strength while it remains in “scoring position.” Since November...

PayPal’s Slowdown: From Fintech Leader to Low-Growth Dividend Stock

PayPal has shifted from fintech leader to low-growth, value-style stock, losing over 25% in market value and trading at a...

|

|

|  |

|

|

-

Crowdfunding5 days ago

Crowdfunding5 days agoIthaca: Climate Road Trip RPG on Climate Resistance

-

Fintech2 weeks ago

Fintech2 weeks agoFintech and AI: Adoption Grows, but Profits Favor Agile Innovators

-

Fintech3 days ago

Fintech3 days agoPayPal’s Slowdown: From Fintech Leader to Low-Growth Dividend Stock

-

Impact Investing1 week ago

Impact Investing1 week agoEdison Accelerates Renewable Growth and ESG Impact in 2025

You must be logged in to post a comment Login