Featured

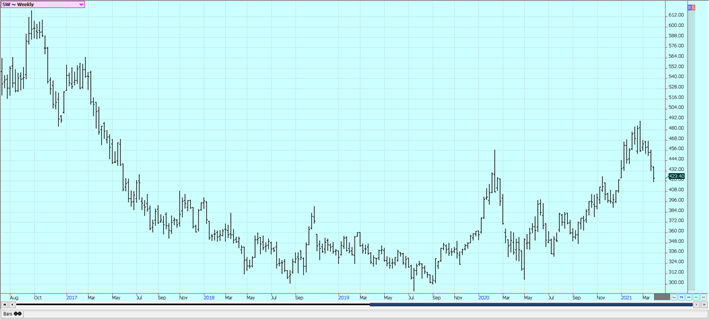

Why are chart trends for cocoa futures still down

Both cocoa markets closed a little higher in consolidation trading on Friday but were still lower for the week. Chart trends are still down on the daily and weekly charts. New York is near recent contract lows. The main crop harvest is active in Nigeria and is spreading to Ivory Coast and Ghana. Demand should improve as the Covid vaccinations get administered.

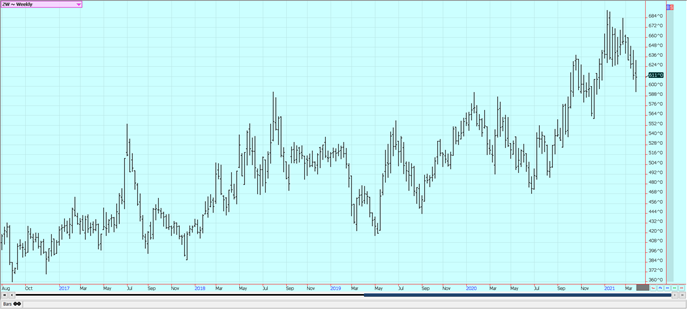

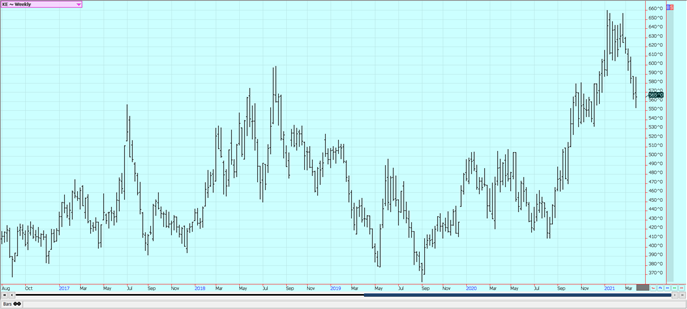

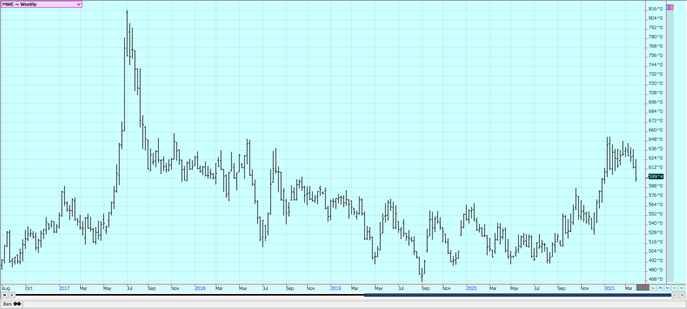

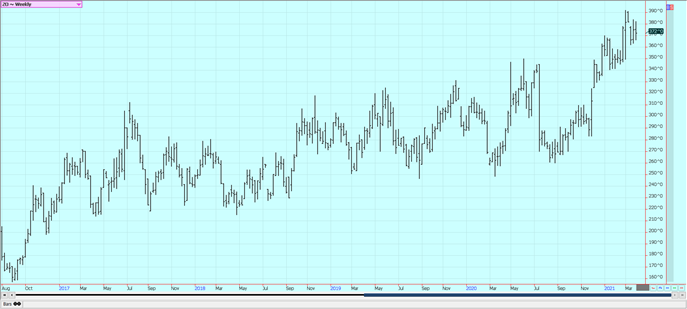

Wheat: Wheat markets were lower on Friday on what appeared to be speculative selling. The markets were a little lower for the week after being much lower earlier in the week and then recovering. Weekly chart trends are still down but daily chart trends are mixed. USDA said that the quarterly stocks and the planted area were higher than trade expectations. Demand has been disappointing so far as traders had expected better exports due to problems in Russia and parts of Europe earlier in the year. Ideas are that rain that has been falling in the Great Plains will help injured Winter Wheat. Temperatures dropped below 0F in many areas a few weeks ago and that is cold enough to kill an unprotected crop. The actual damage will take some time to see under warmer temperatures and it might take until harvest to see the full effects of the recent extreme cold. Wheat conditions are improved overall after a rough start to the crop.

Weekly Chicago Soft Red Winter Wheat Futures

Weekly Chicago Hard Red Winter Wheat Futures

Weekly Minneapolis Hard Red Spring Wheat Futures

Corn: Corn closed mixed, with what appeared to be speculative profit-taking driving nearby prices a little lower but continued speculative buying supporting new crop prices. Corn closed a little higher for the week. Oats were a little lower. Corn traded limit up on Wednesday in response to the USDA reports. USDA showed that inventories were a little less than expected, implying greater than expected feed use. USDA also showed significantly less planting intentions by farmers for Corn than the trade had expected. It was the latter report that really sent the market up to or close to limit up levels. Oats were higher, Traders are still concerned that China might not buy more US Corn because the political talks were not productive and the South American harvest is just down the road. Chinese demand had been strong until recently and it looks like they need the Corn. Prices inside China for Corn remain extremely high. It is drier in central and parts of northern Brazil, and farmers are able to harvest much of the Soybeans area and plant much of the Winter Corn. The Winter Corn crop progress is well behind normal. Argentina has seen a general rain in the last week and Corn in Argentina has stabilized after losing yield to dry conditions and crop stress. Southern Brazil is also in a better place on crop conditions. More rain is in the forecast for these areas in the next week.

Weekly Corn Futures:

Weekly Oats Futures

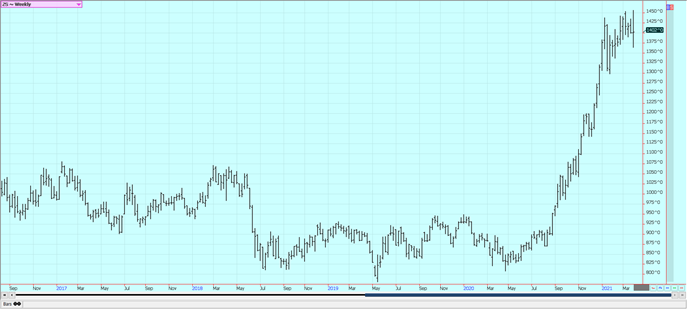

Soybeans and Soybean Meal: Soybeans were sharply lower in old-crop months on Thursday as some speculative profit-taking showed up after trading limit up on Wednesday. New crop months moved higher on Thursday after trading limit up on Wednesday. The rally came in reaction to the USDA reports that showed quarterly stocks about as expected but planting intentions at levels much less than expected by the trade. Futures price trends turned up in Soybeans and Soybean Meal and are mixed in Soybean Oil. Higher prices for Soybeans appear to be likely. Selling has come in recent sessions on ideas that the ongoing Brazil harvest will kill the current demand for US Soybeans. Demand was worse last week but the US has now sold 99% of its target amount of Soybeans for the marketing year and really has very few Soybeans left to sell. The Brazil harvest had been delayed due to late planting dates early due to dry weather and now too much rain that has caused harvest delays and some quality problems in the north as well. Harvest activities have increased but the harvest remains very slow overall. China has been buying for next year here but now is buying mostly in South America. US internal demand has been strong.

Weekly Chicago Soybeans Futures:

Weekly Chicago Soybean Meal Futures

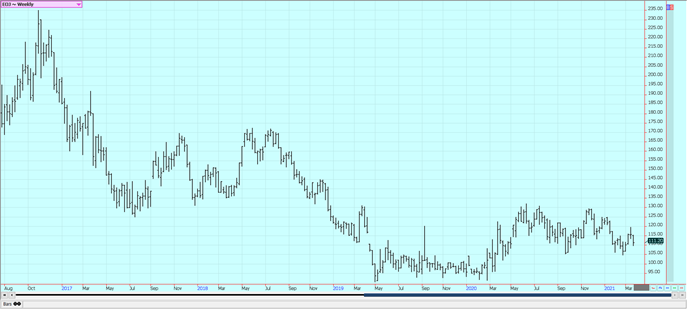

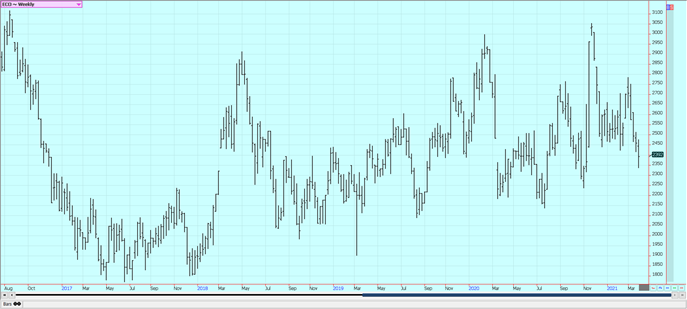

Rice: Rice was lower on Thursday on what appeared to be speculative selling that came in reaction to the USDA reports released Wednesday morning. Planted area estimates were on the low side of expectations while the quarterly stocks report showed big supplies with merchants and big supplies overall. Demand has been solid for exports but less for the mills and this remains the feature of the trade. The export demand has been primarily for paddy Rice and not for milled Rice. The cash market has not felt any increased export demand lately and mill operations are reported to be on the slow side. Texas is about out of Rice, but there is Rice available in the other states, especially Arkansas. Asian and Mercosur markets were steady to firm last week. New crop Rice is getting planted in Texas and planting is up to half done in Louisiana. Mississippi is about to start.

Weekly Chicago Rice Futures

Palm Oil and Vegetable Oils: World vegetable oils prices were mixed last week with Palm Oil higher and the other markets lower. Palm Oil closed higher last week on reports of good demand from private sources. Demand had been expected to drop off but recovered instead. Ideas of tight supplies are still around but supplies should start to seasonally increase. The production of Palm Oil is down in both Malaysia and Indonesia as plantations in both countries are having trouble getting workers into the fields. Wet weather has caused even more delays. The weather is improved and trees seasonally increase production about now. Canola was lower on what appeared to be speculative selling tied to price action in Chicago. There were reports that the US was about to import a couple of cargoes of Soybean Oil from Argentina to break prices in both Soybean Oil and Canola. Worries about South American production are supporting both markets but the weather is better now and both are looking for new triggers to promote more buying.

Weekly Malaysian Palm Oil Futures:

Weekly Chicago Soybean Oil Futures

Weekly Canola Futures:

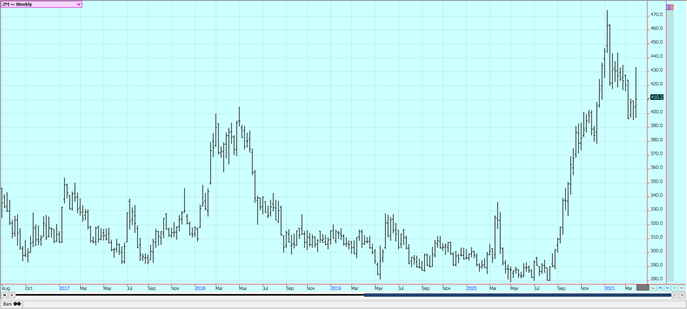

Cotton: Futures were lower on Friday on what appeared to be renewed speculative selling. Futures were lower for the week as the US Dollar rallied and hurt demand ideas. Producers told USDA they intend to plant 11.95 million actresses of Cotton this year although this could change if prices rally or fall from current levels. Most likely the market will want a bigger area planted to Cotton and will rally prices. The trends turned down on the weekly charts due to the price action of last week. The chart trends are sideways on the daily charts. The demand for US Cotton in the export market has been strong even with the Coronavirus causing disruptions at the retail level around the world. The US stock market has been generally firm to help support ideas of a better economy here and potentially increased demand for Cotton products.

Weekly US Cotton Futures

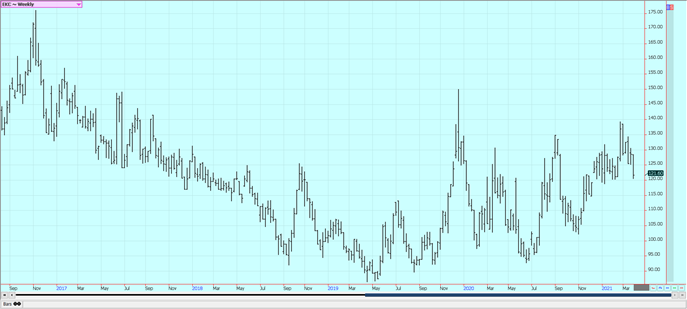

Frozen Concentrated Orange Juice and Citrus: FCOJ closed a little higher and the trends are now sideways on the daily charts and the weekly charts. Support is showing at current price levels as futures do not appear ready to make new lows on the daily charts. The demand for FCOJ is said to be weaker as the Coronavirus has been less in the US. The weather has turned warmer so less flu is around as well. Moderate temperatures are expected for Florida this week. The weather in Florida is good with a few showers or dry weather to promote good tree health and fruit formation. Showers have fallen in Brazil, but it is dry now and crop conditions are called good even with drier than normal soils. Stress to trees could return if the dry weather continues. Mexican crop conditions in central and southern areas are called good with rains, but earlier dry weather might have hurt production. It is dry in northern and western Mexican growing areas.

Weekly FCOJ Futures

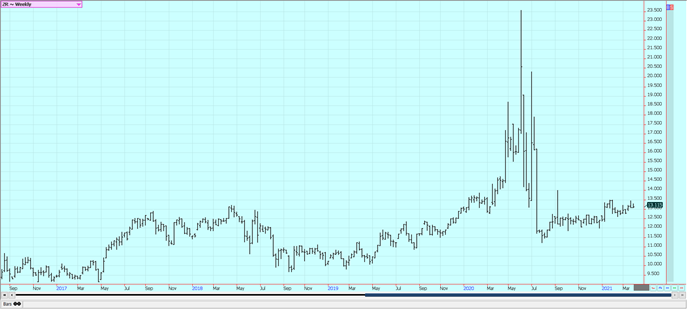

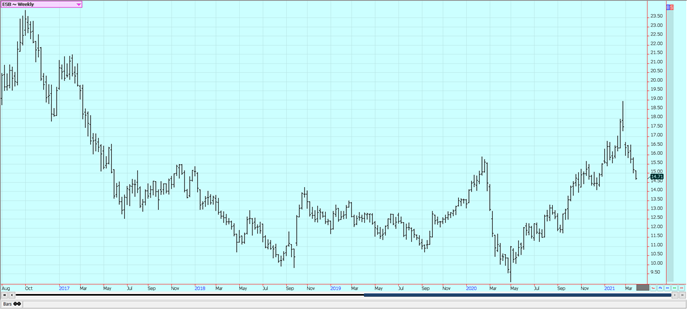

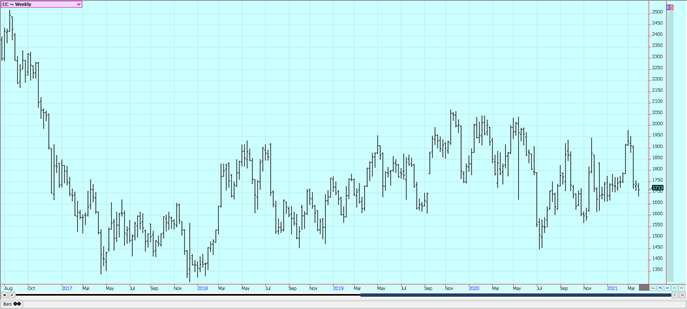

Coffee: Futures were lower for the week and trends are down on the weekly charts. The price action is weak in both markets but New York is now near objectives for the move. London can slide further. Cash market buyers are not buying much Coffee but offers are not strong from many origins. Vietnam producers are selling some Coffee. There are reports of good weather in Vietnam for the harvest. Indonesia has had good weather but has little coffee to sell now. Dry conditions are reported in Brazil again but crop conditions are still good. Trees might get stressed again in the dry weather continues for several more days. Cooxupe said its members anticipated producing about 32% less Coffee this year due to dry and hot conditions last year and the second year of the production cycle for the trees. Central America is also drier for harvesting but production might have been reduced due to very wet conditions during the growing season. Good growing conditions are reported in Colombia and Peru. Africa is also noting good growing conditions.

Weekly New York Arabica Coffee Futures

Weekly London Robusta Coffee Futures

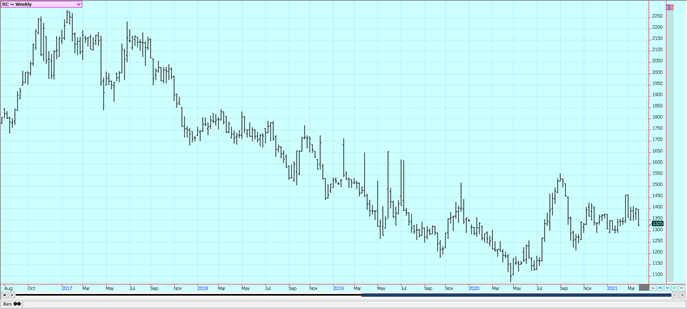

Sugar: New York closed lower on Friday on improved world production prospects. London closed mixed, with nearby prices a little higher. The chart trends are still mostly down on the daily and the weekly charts. Current Sugar demand is called average. Dry conditions were reported in Brazil. It has been raining in south-central Brazil until recently and the production of cane is looking good for the next harvest. Production has been hurt due to dry weather earlier in the year and this week could be dry again. Traders are worried about a delayed Brazil harvest and lack of space at Brazil ports for Sugar shipments due to the high Soybeans shipments and delayed nature of the harvest of the Soybeans. India is exporting Sugar and is reported to have a big cane crop this year. Thailand is expecting improved production after drought-induced yield losses last year.

Weekly New York World Raw Sugar Futures

Weekly London White Sugar Futures

Cocoa: Both markets closed a little higher in consolidation trading on Friday but were still lower for the week. Chart trends are still down on the daily and weekly charts. New York is near recent contract lows. The main crop harvest is active in Nigeria and is spreading to Ivory Coast and Ghana. Demand should improve as the Covid vaccinations get administered and as at least some governments around the world invest in fiscal stimulus on their economies. Fears of a Coronavirus resurgence are hurting demand ideas and the vaccinations have been harder to administer in Europe lately due to citizen resistance. Production appears to be good this year and the supply surplus is growing.

Weekly New York Cocoa Futures

Weekly London Cocoa Futures

—

(Featured image by Tom Coady CC BY 2.0 via Flickr)

DISCLAIMER: This article was written by a third party contributor and does not reflect the opinion of Born2Invest, its management, staff or its associates. Please review our disclaimer for more information.

This article may include forward-looking statements. These forward-looking statements generally are identified by the words “believe,” “project,” “estimate,” “become,” “plan,” “will,” and similar expressions. These forward-looking statements involve known and unknown risks as well as uncertainties, including those discussed in the following cautionary statements and elsewhere in this article and on this site. Although the Company may believe that its expectations are based on reasonable assumptions, the actual results that the Company may achieve may differ materially from any forward-looking statements, which reflect the opinions of the management of the Company only as of the date hereof. Additionally, please make sure to read these important disclosures.

Futures and options trading involves substantial risk of loss and may not be suitable for everyone. The valuation of futures and options may fluctuate and as a result, clients may lose more than their original investment. In no event should the content of this website be construed as an express or implied promise, guarantee, or implication by or from The PRICE Futures Group, Inc. that you will profit or that losses can or will be limited whatsoever. Past performance is not indicative of future results. Information provided on this report is intended solely for informative purpose and is obtained from sources believed to be reliable. No guarantee of any kind is implied or possible where projections of future conditions are attempted. The leverage created by trading on margin can work against you as well as for you, and losses can exceed your entire investment. Before opening an account and trading, you should seek advice from your advisors as appropriate to ensure that you understand the risks and can withstand the losses.

Corn Prices Slip Amid Strong Crop Conditions and Favorable Weather

Corn was lower again last week on Midwest rains despite a neutral WASDE report. The report showed slightly higher beginning...

Advances in Biomarkers and Targeted Therapies Transform Kidney Care in Autoimmune Disease

New biomarkers and targeted therapies are reshaping the management of kidney damage in autoimmune diseases like lupus and vasculitis. Experts...

Bitcoin Rises on Iran Deal as Crypto Markets React to AI and SpaceX News

Bitcoin rose above $65,000, gaining about 5% as a tentative Iran war agreement boosted markets. ETFs still show weekly outflows....

Rising Inflation, Fed Uncertainty, and Market Excess Amid War and SpaceX Mania

Rising inflation, driven by war, debt, and money growth, puts the Fed in a difficult position ahead of its meeting....

SpaceX IPO Sparks Déjà Vu as Market Risks Loom and Gold Bulls Stay Hopeful

The author compares the 2000 AOL Time Warner merger to SpaceX’s planned IPO, warning it may signal a market top....

|

|

|  |

|

|

-

Cannabis2 weeks ago

Cannabis2 weeks agoMedical Cannabis in England Sees Shift Toward Vaporizers and Pills Amid Rapid Market Growth

-

Africa2 weeks ago

Africa2 weeks agoBank of Africa Leads Winners at African Banker Awards

-

Impact Investing6 days ago

Impact Investing6 days agoTransition to a Sustainable Economy as a Strategic Global Shift in a Fragmented World

-

Cannabis2 weeks ago

Cannabis2 weeks agoTilray Expands in Europe as Medical Cannabis Market Grows