Featured

Coffee Producers in Vietnam and Indonesia Are Said to Have Almost Nothing Left to Sell

Coffee futures in New York and London closed much higher Friday in speculative trading as short-term trends are up in both markets. There are reports of good weather for Arabica production in Brazil with high coffee production expectations. The Arabica harvest has started and offers of Arabica from Brazil are expected to increase over time.

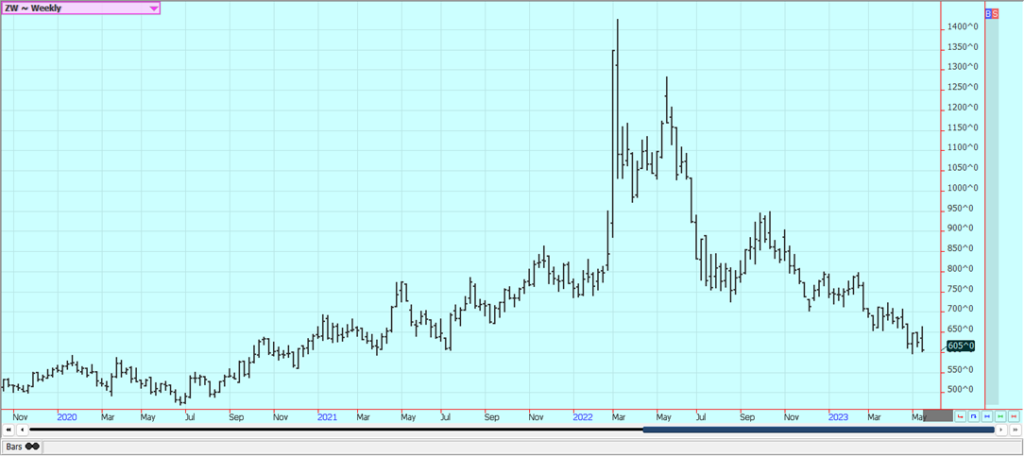

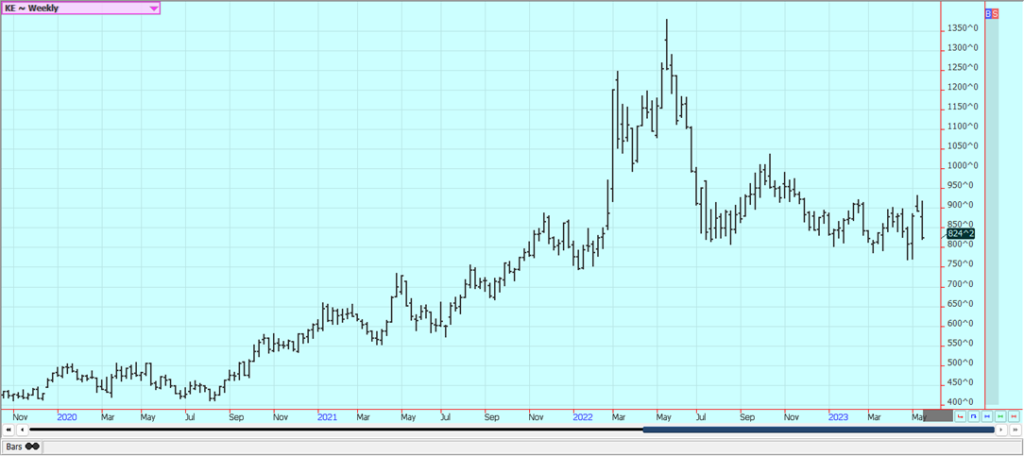

Wheat: Wheat markets were lower last week, with big selling seen in KC and Minneapolis markets. The US Dollar was sharply higher Thursday and the weekly export sales report showed negative net sales. The Dollar gave back some of its gains on Friday. Support came in part in reaction to the USDA production estimates released the previous week. Turkey said Thursday that the grain deal is extended for 60 days and this news was later confirmed by Russia and Ukraine. Planting of Spring Wheat has been delayed due to wet soils from melting snow and now from reports of dry weather in western production areas of both the US and Canada. Dry conditions are a developing problem in Russia, especially in the Spring Wheat areas there. Weak Chinese economic data released last week hurt the price action and caused speculative selling. Ideas that big Russian offers and cheaper Russian prices would be a feature for a while in the world market was the driving force for the weaker prices. Ideas are that both Australia and Russia are harvesting record to near-record Wheat crops this year.

Weekly Chicago Soft Red Winter Wheat Futures

Weekly Chicago Hard Red Winter Wheat Futures

Weekly Minneapolis Hard Red Spring Wheat Futures

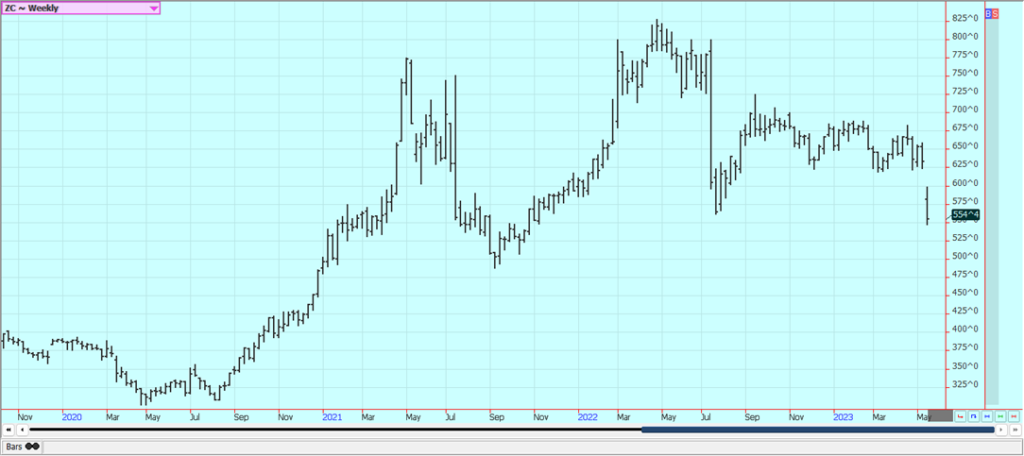

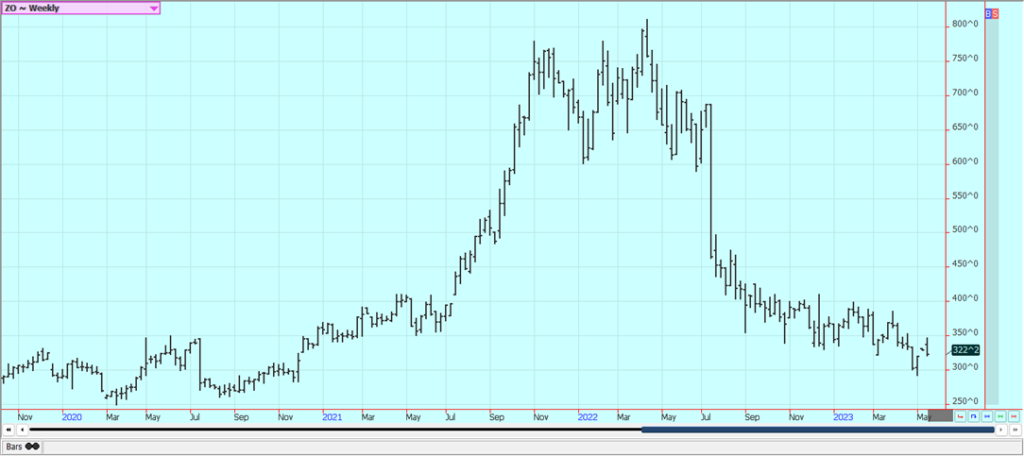

Corn: Corn and Oats closed lower last week, with Corn closing sharply lower on ideas of little current demand and very good planting conditions for the Midwest. Reports of strong planting progress and less Chinese demand hurt the Corn price action as did negative weekly export sales and a strong rally in the US Dollar on Thursday. The Dollar gave back some of the gains on Friday. Chinese economic data was released earlier this week and was worse than expected, so there is now new doubt as to how much the Chinese will buy and import this year. Corn is still finding some support from little US producers selling interest. Most producers are in the fields and are not even worried about the market. Warmer and drier weather for good planting is expected for much of next week, but showers are possible again this weekend. US prices are currently very competitive with those from South America as Brazil concentrates on Soybeans exports and not Corn, so the current export sales pace has been disappointing. NOAA is forecasting that La Nina will develop this Summer and replace El Nino. US growing conditions are usually good when this happens but there are concerns about ocean water temperatures that are increasing rapidly in the Pacific and have alarmed some forecasters.

Weekly Corn Futures

Weekly Oats Futures

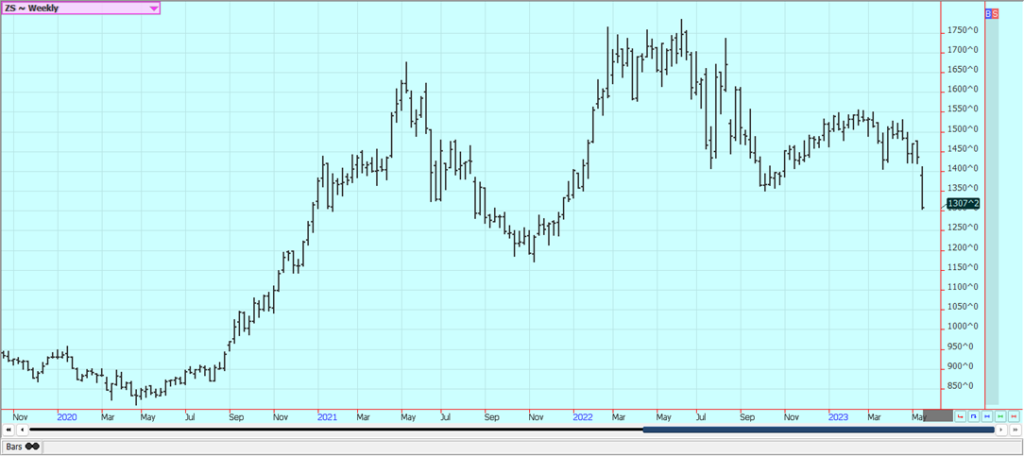

Soybeans and Soybean Meal: Soybeans and the products were lower last week, with the most weakness seen in Soybeans. Funds appeared to be the best sellers. Speculators are still bearish and chart trends are still down on selling tied to the release of Chinese economic data on Wednesday, the cancellation of Chinese Corn purchases here, and good planting weather. Speculators also sold due to the strong rally seen in the US Dollar on Thursday although the Dollar moved lower on Friday. The Chinese economy is in much worse shape than anyone thought, and the data implied that China will probably take less. Brazil’s basis levels are still low and the US is being shut out of the market for most importers. Brazil is still selling a lot of Soybeans to China to feed its Soybeans demand, but Chinese customs is now making delivery of the beans very difficult by delaying entry into the country by about two weeks and the economic news might help keep Chinese imports less than expected. Brazil has a very good crop, but the additional Soybeans grown in Brazil will be partially wiped out by the losses in Argentina. The Argentine crop is now estimated at just 21 million tons. Argentina has been forced to import from Brazil to keep its crushing facilities operating. Forecasts from NOAA for very good growing conditions in the Midwest were also a factor, but there are concerns about ocean water temperatures that are increasing rapidly in the Pacific and have alarmed some forecasters.

Weekly Chicago Soybeans Futures

Weekly Chicago Soybean Meal Futures

Rice: Rice closed lower last week in response to negative weekly export sales and a rally in the US Dollar Index seen on Thursday. Some of the gains in the Dollar were given back on Friday. Cancellations came from Iraq and Japan and buying came mostly from Haiti and Canada. Offers still seem hard to find right now, but demand has been a problem all year. Export demand has been uneven. Mills are milling for the domestic market in Arkansas and are bidding for some Rice, but at least some mills say they now have enough bought to last until the harvest of the next crop. USDA showed that the next crop is developing fast and that conditions are very good in Rice country.

Weekly Chicago Rice Futures

Palm Oil and Vegetable Oils: Palm Oil was lower last week on Chicago price action and on ideas of increasing supplies against slack demand. Ideas are that world stocks are building for vegetable oils. India recently cut its base import price and Chinese economic data released last week showed less activity than expected. In Malaysia, April production was 7% less than March at 1.196 million tons. Exports were also down and ending stocks were estimated at 1.597 million tons, down over 10% from last month. Trends are turning down on the daily charts. The weekly continuation charts show that the nearest futures are now close to support levels that have held the futures market since September. Canola was lower last week on demand concerns and despite dry conditions for planting in the Prairies. Trends are turning down on the daily and weekly charts. Reports indicate that domestic demand has been strong due to favorable crush margins, but export demand is questioned, especially since the release of the weaker-than-expected Chinese economic data last week. It is very dry in the Canadian Prairies, especially in western sections. Producers want to plant but are hoping for some moisture. Only isolated showers are in the forecast.

Weekly Malaysian Palm Oil Futures

Weekly Chicago Soybean Oil Futures

Weekly Canola Futures:

Cotton: Cotton was higher last week and closed at new weekly highs for the move. Speculators appeared to be the best sellers on news from Tuesday of weaker-than-expected Chinese economic data and a weaker USDA export sales report on Thursday. The US Dollar was sharply higher Thursday to keep demand ideas down but gave back part of the rally on Friday. Forecasts for showers are still showing in forecasts for West Texas and are expected to be beneficial. Ideas are that the world economic problems were fading into the background as the US stock market has held strong and as the Chinese economy gets better after all of the Covid lockdowns.

Weekly US Cotton Futures

Frozen Concentrated Orange Juice and Citrus: FCOJ closed higher last week and futures are holding to a trading range again. Trends are trying to turn u[p after the price action on Friday. Futures remain supported by very short Oranges production estimates for Florida. Demand is thought to be backing away from FCOJ with prices as high as they are currently, but the market has not taken any note and continues to work higher. Historically low estimates of production due in part to the hurricanes and in part to the greening disease that have hurt production, but conditions are significantly better now with scattered showers and moderate temperatures. The weather remains generally good for production around the world for the next crop including production areas in Florida that have been impacted in a big way by the two storms seen previously in the state. Brazil has some rain and conditions are rated good.

Weekly FCOJ Futures

Coffee: New York and London closed much higher Friday in speculative trading as short-term trends are up in both markets. There are reports of good weather for Arabica production in Brazil with high production expectations. The Arabica harvest has started and offers of Arabica from Brazil are expected to increase over time. There are still tight Robusta supplies for the market amid strong demand for Robusta, but the Brazil harvest is in the market now. The Brazil harvest of Robusta is in full swing and promising to help relieve tight supplies in that market. The Robusta market is especially tight and has been pushing on the Arabica price, but Arabica supplies are growing tight in the market as well. Producers in Vietnam and Indonesia are said to have almost nothing left to sell and producers in Colombia and Brazil are also reported to be short on Coffee to sell. The market really needs big offers from Brazil to sustain any downside movement. Conab in Brazil estimated production this year at 54.7 million bags, from 54.9 million in January and 50.9 million last year. Arabica production was estimated at 37.9 million bags, from 37.4 million in January and 32.7 million last year. Robusta production is estimated at 16.8 million bags, from 17.5 million in January and 18.2 million last year.

Weekly New York Arabica Coffee Futures

Weekly London Robusta Coffee Futures

Sugar: Both New York and London closed lower for the week, and trends remain sideways for the short term. The market is still hurt by good growing conditions in Brazil but supported by tight current supplies. The production is not there to meet the demand in many countries, with only Brazil among the major producers looking to have a good crop. It should start becoming available soon. Indian production is less this year as mills are closing early there and Pakistan also has reduced production. Thailand mills are also closing earlier than expected so the crop there might be less. Asian countries could face another year of short production as El Nino returns after years of La Nina. European production is expected to be reduced again this year. Chinese production could be the lowest in six years due to bad growing conditions.

Weekly New York World Raw Sugar Futures

Weekly London White Sugar Futures

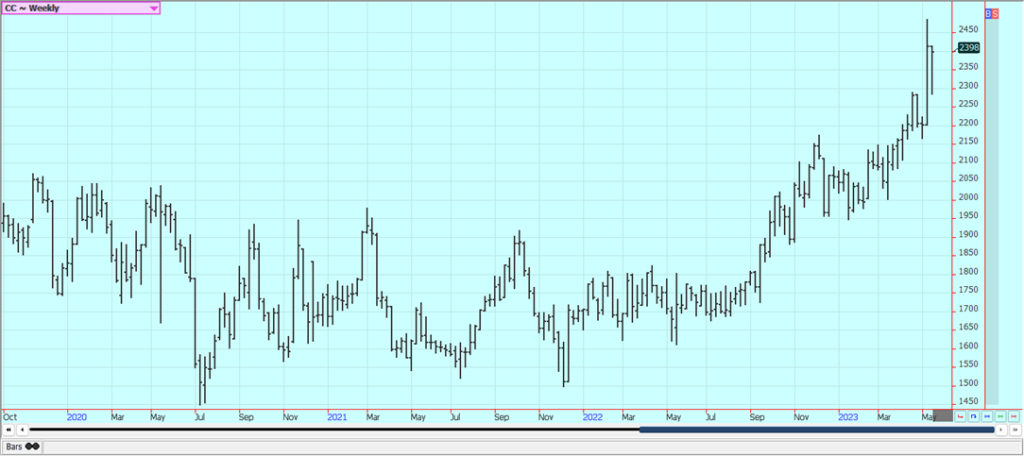

Cocoa: New York and London closed higher and at new highs for the move on the daily charts. Ideas of tight supplies that remain based on more reports of reduced arrivals in Ivory Coast continue. The lack of arrivals from West Africa to ports is still important and is supporting futures, but certified stocks have increased a lot this week in New York and deliveries have picked up as well. Talk is that hot and dry conditions reported earlier in Ivory Coast could curtail main crop production, and main crop production ideas are not strong. Midcrop production ideas are strong due to rain mixed with some sun recently reported in Cocoa areas of the country.

Weekly New York Cocoa Futures

Weekly London Cocoa Futures

__

(Featured image by NoName_13 via Pixabay)

DISCLAIMER: This article was written by a third-party contributor and does not reflect the opinion of Born2Invest, its management, staff, or its associates. Please review our disclaimer for more information.

This article may include forward-looking statements. These forward-looking statements generally are identified by the words “believe,” “project,” “estimate,” “become,” “plan,” “will,” and similar expressions. These forward-looking statements involve known and unknown risks as well as uncertainties, including those discussed in the following cautionary statements and elsewhere in this article and on this site. Although the Company may believe that its expectations are based on reasonable assumptions, the actual results that the Company may achieve may differ materially from any forward-looking statements, which reflect the opinions of the management of the Company only as of the date hereof. Additionally, please make sure to read these important disclosures.

Futures and options trading involves substantial risk of loss and may not be suitable for everyone. The valuation of futures and options may fluctuate and as a result, clients may lose more than their original investment. In no event should the content of this website be construed as an express or implied promise, guarantee, or implication by or from The PRICE Futures Group, Inc. that you will profit or that losses can or will be limited whatsoever. Past performance is not indicative of future results. Information provided on this report is intended solely for informative purpose and is obtained from sources believed to be reliable. No guarantee of any kind is implied or possible where projections of future conditions are attempted. The leverage created by trading on margin can work against you as well as for you, and losses can exceed your entire investment. Before opening an account and trading, you should seek advice from your advisors as appropriate to ensure that you understand the risks and can withstand the losses.

Switzerland’s Medical Cannabis Reform Advances Access, But Barriers Remain

Switzerland’s 2022 medical cannabis reform improved patient access by removing federal approval requirements, but challenges remain. MEDCAN highlights barriers including...

Swisscanto Launches Catastrophe Bond Fund for Portfolio Diversification

Swisscanto launches a Luxembourg UCITS catastrophe bond fund, giving qualified investors access to insurance-linked securities tied to extreme natural events....

AI Agents Transform Payments as Visa, Mastercard, and Qonto Tackle Trust, Liability, and Regulation

Visa and Mastercard are advancing AI-driven autonomous payments, shifting focus to trust, liability, and regulation when agents act without real-time...

Bitcoin ETFs Lead as German Stock Exchange Debuts Mining ETF

Bitcoin and Ethereum remain largely flat, with BTC near 66,600 and ETH around 1,920, while ETFs see steady inflows. A...

Ali G Makes Surprise Wimbledon Appearance with Cannabis-Themed Satire

Sacha Baron Cohen revived his iconic Ali G character at Wimbledon’s men’s final, blending satire with British high society. Dressed...

|

|

|  |

|

|

-

Fintech1 week ago

Fintech1 week agoRobinhood Chain Surges with Rapid Adoption and Billion-Dollar Trading Volume

-

Impact Investing7 days ago

Impact Investing7 days agoPictet Raises $253 Million for Environmental Investment Fund

-

Fintech2 weeks ago

Fintech2 weeks agoPayhawk Reaches $100M ARR Milestone with AI-Driven Growth

-

Africa2 days ago

Africa2 days agoPAASIFEJ: Results-Based Financing Driving Inclusive and Sustainable Rural Growth in Morocco