Business

Corn grows stronger; Bad weather slams US cotton

Corn rallies are looking optimistic, closing strong on weekly export sales. US cotton futures are weak owing to bad crop conditions.

Wheat

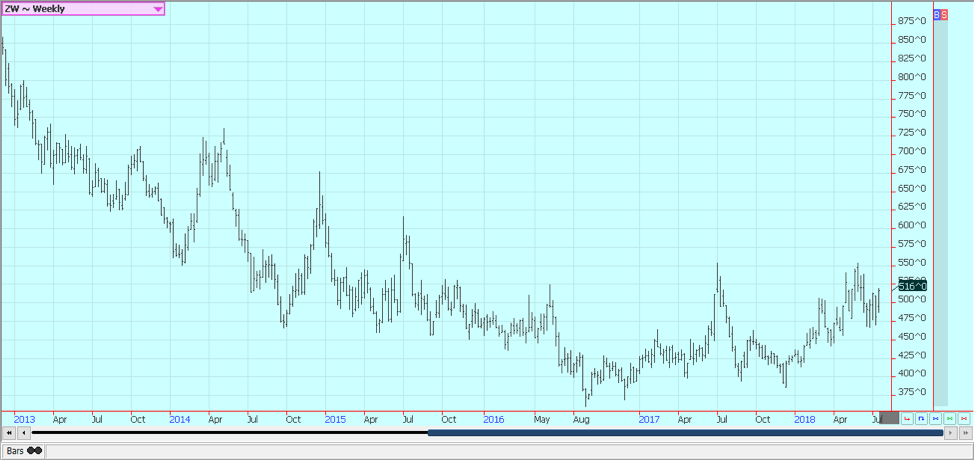

Wheat markets were higher again on Friday on improved export sales and increasing world prices. Wire stories highlighting the potential for losses to wheat in northern Europe got the attention of the market. The harvest is underway in some southern areas and yields, in general, have been disappointing. A downgrade in production for European wheat is likely in coming months and comes on the back of earlier downgrades. The market is trying to complete a bottom at this time.

A bottom might have been completed in Chicago futures on Friday, but Minneapolis and Kansas City were only able to trade to the top end of their ranges on the daily charts. Trends turned up in all three markets on the weekly charts. Weekly Chicago wheat continuation charts imply that a move to 560 or 570 basis the nearest futures is possible. USDA world estimates released last week for the coming year showed a sharp reduction in production due to problems in major growing areas around the world and projects improved demand for US wheat in the world market.

East Europe and Russia remain mostly hot and dry, although spring wheat areas are now getting more favorable growing conditions. Australia is another producing country where some rains are badly needed, mostly in eastern and southeastern areas as western areas have seen enough rain. The US winter wheat harvest will start to wind down soon. Spring wheat crops are developing well, and the condition is holding strong amid periods of rains and warm temperatures.

Weekly Chicago Soft Red Winter Wheat Futures © Jack Scoville

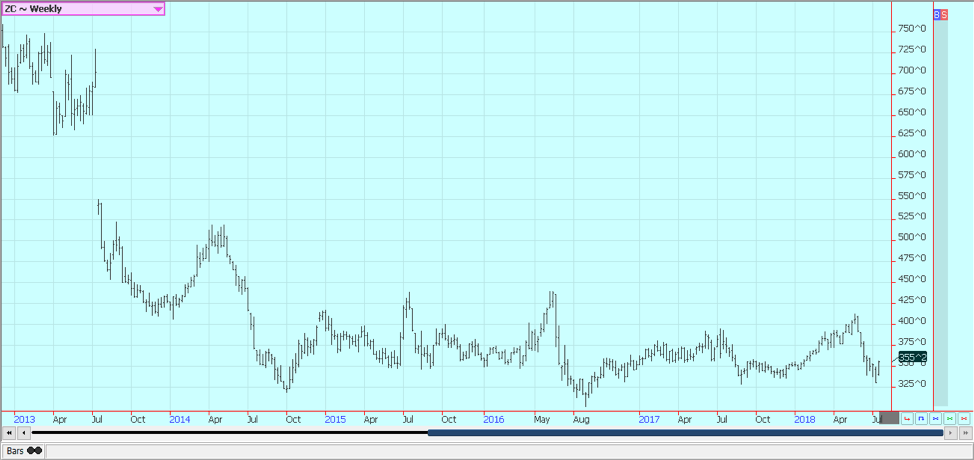

Weekly Chicago Hard Red Winter Wheat Futures © Jack Scoville

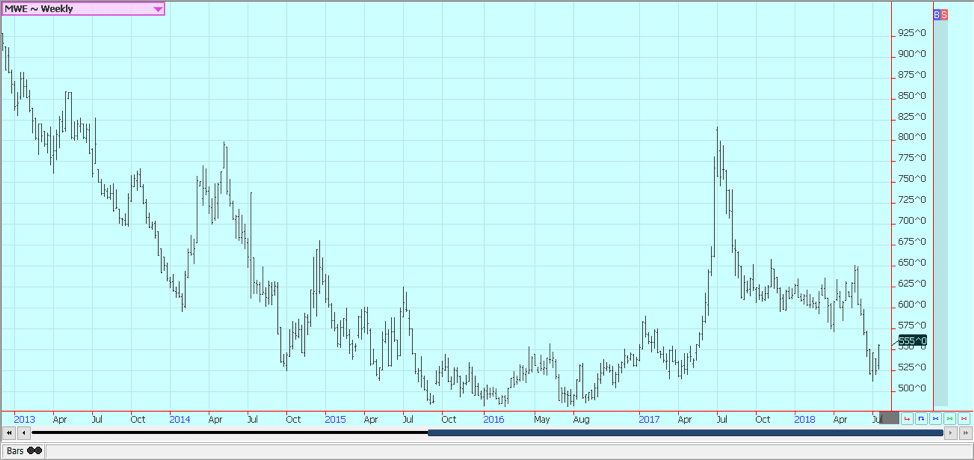

Weekly Minneapolis Hard Red Spring Wheat Futures © Jack Scoville

Corn

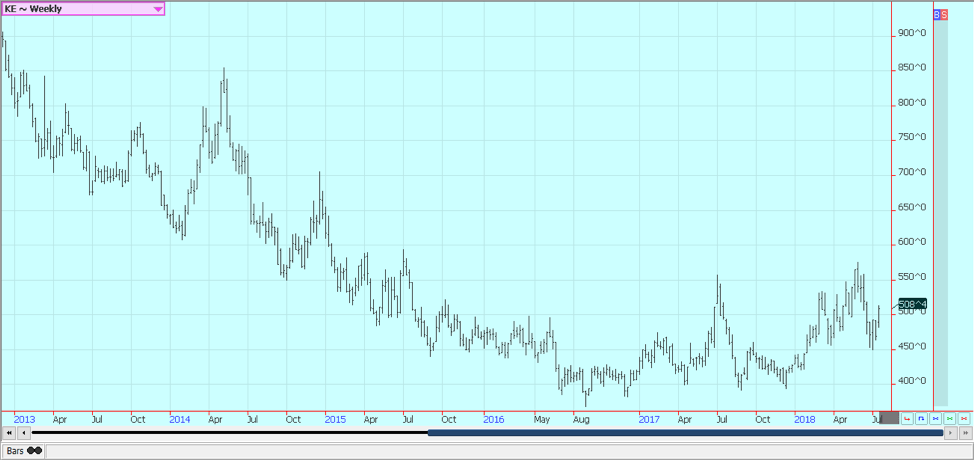

Corn closed higher again on Friday and higher for the week on strong weekly export sales. The sales showed that US prices are very competitive and strong sales are expected to continue. Corn is pollinating, but not always pollinating or filling well in the dry areas of the southwestern and eastern Midwest, and some northern crops are small and yellow from too much rain.

Producers have said that the weather has been variable enough to think that the yields might be trimmed a bit. The trade had been talking about a national yield near 180 bushels per acre, but now some are suggesting that a national yield closer to 175 or 177 bushels per acre is more likely given the weather until now. That implies that conditions should continue to drop in the next couple of weeks unless the weather improves in all areas. Demand remains at a very high level on the domestic and export sides.

Crop conditions are fair to good here, and feed grains in Europe and Russia are being stressed due to the hot and dry weather there. US corn prices are as cheap as any in the world, so the US should do a lot of selling for a while. Producers show no interest in selling at current levels. Chart trends on daily and weekly charts suggest that a low has formed or is forming. Nearby futures could move to about 395 in a recovery trade.

Weekly Corn Futures © Jack Scoville

Weekly Oats Futures © Jack Scoville

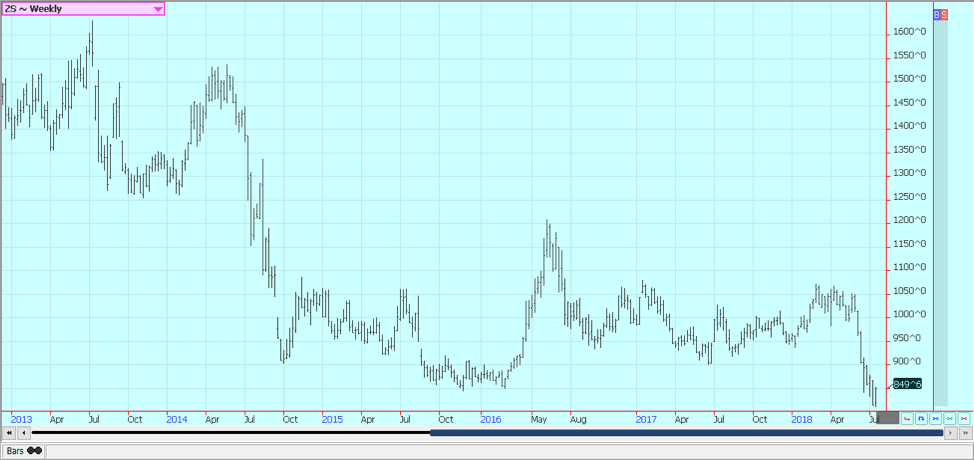

Soybeans and soybean meals

Soybeans and soybean oil were higher, but soybean meal was lower. Ideas that new demand is surfacing in the export market for US soybeans continue to be heard, and Gulf basis levels have held. Brazil basis levels have held very strong as the market continues to price in the Chinese tariffs against US soybeans. The export sales report last week was considered to be strong and showed that other buyers besides China are taking advantage of our lower prices. US soybeans are cheap when compared to Brazil. There are ideas that a low for the current move was made last week, so some speculators are exiting short positions.

The Trump administration is coming under increasing pressure to get a deal negotiated to alleviate the tariffs. The president announced on Friday that he is willing to impose a tariff on all Chinese exports to the US if it does not improve on its negotiating offer. Prices for US soybeans reflect almost a 25% discount to those from South America due to the tariff wars, and there are hopes now that other world buyers will become new clients of the US as these cheaper levels.

Ideas are that Soybeans sales to China will suffer for an extended period, but other countries might buy on ideas that the current relatively cheap prices could encourage new demand. No one thinks that China will buy here in the short term, but they will need to buy here eventually. In the meantime, Brazil prices stay very strong with basis levels up to about 240 over futures. US growing conditions have been variable, with hot and dry conditions in the east and southwest and too much rain in the north.

Weekly Chicago Soybeans Futures © Jack Scoville

Weekly Chicago Soybean Meal Futures © Jack Scoville

Rice

Rice was trapped in a range on the weekly charts and closed a little higher for the week. The market focus has turned to the new crop and still worries about demand potential. Nearby months were firm as supplies available to the cash market are very tight. The export sales report was not large last week, but there is not much rice to sell. Producers tell us that some areas near the Gulf Coast could be ready for cutting by the end of this month and that many parts of Texas and the southern half of Louisiana could be under active harvest by then.

The crop progress is being pushed by the hot weather in many areas. That could mean less yield, but for now, the crops, in general, look good. No one will know of yield loss, if any, until the harvesters roll. The charts show a short-term sideways trend, but a new leg higher is still very possible.

Weekly Chicago Rice Futures © Jack Scoville

Palm oil and vegetable oils

World vegetable oils prices were higher in recovery trading last week. Futures had traded to new lows for the move the previous week on ideas of weak demand, but demand showed signs of recovery last week as private sources in Malaysia reported stable exports and as USDA showed better exports. The markets still show the potential to work lower as production ideas remain generally high and as world vegetable oils demand has turned soft.

Soybean oil was locked in a sideways to lower trend all week and closed lower. Trends are sideways to down in the market. Canola was higher as Chicago prices firmed. Some parts of the western Prairies saw some beneficial rains last week, and most areas are reported in good condition. Some areas remain hot and dry and are getting stressed. Offers from farmers were down last week as they wait for higher prices and as they work in the fields.

Weekly Malaysian Palm Oil Futures © Jack Scoville

Weekly Chicago Soybean Oil Futures © Jack Scoville

Weekly Canola Futures © Jack Scoville

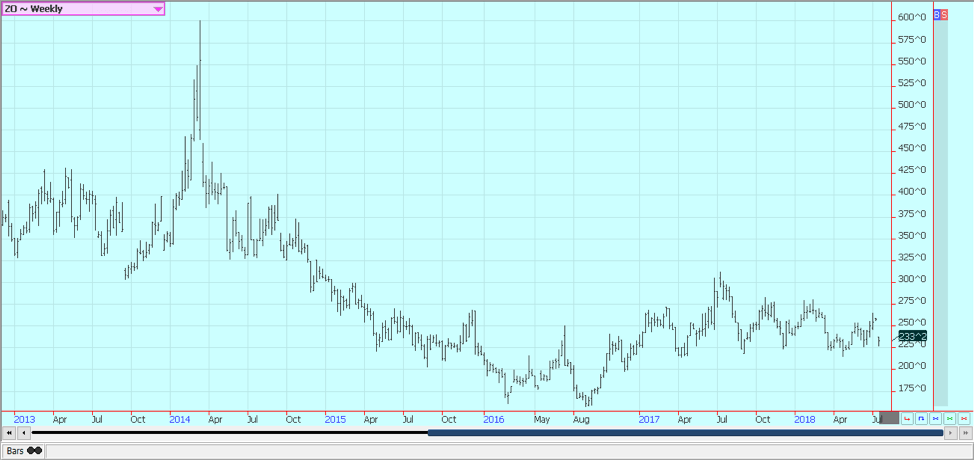

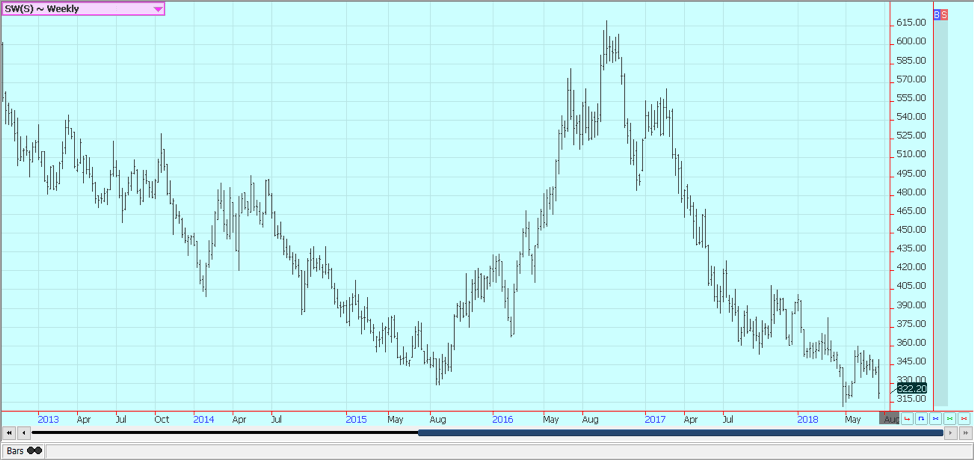

Cotton

Cotton was lower again on Friday and lower for the week. Bad crop conditions in parts of the US have kept the market supported, but the market worries about demand due to the China tariffs. US crop conditions are fading due to the extreme Texas weather and pockets of problems in other states. However, the market acts as if the bad weather news is part of the market. It has not really been able to extend gains from the limit up a day after the latest supply and demand reports earlier in the month.

Demand prospects are not as good as they were a couple of months ago because of the tariff war with China. Chinese tariffs against US cotton have forced buyers in China to look to India. Forward sales have increased and prices there have held firm. Crop conditions are good in the rest of the Southeast as these areas have been a little drier. Texas now is hot and dry again. The weather is improving in India and China as monsoon rains are reported in India and as China has turned drier. The monsoon has started in southern and central India and rains are now moving into northwest India and Pakistan.

Weekly US Cotton Futures © Jack Scoville

Frozen concentrated orange juice and citrus

FCOJ was a little higher again Friday and is trying to break some resistance areas on the weekly charts. It remains a weather market, but there is no storm development in the Atlantic at this time. Florida weather remains good. The only question is if FCOJ will be available in increased quantities from Brazil this year as production ideas there are down due to hot and dry growing conditions.

Florida producers are seeing good sized fruit, and work in groves maintenance is active. Irrigation is being used. Brazil could use more rain as Sao Paulo has been hot and mostly dry. The harvest there is active, but will start to wind down soon. Production is expected to be down significantly from last year.

Weekly Frozen Concentrated Orange Juice Futures © Jack Scoville

Coffee

Futures were higher in both markets again on Friday in light to moderate trading interest. It was a strong close on the daily and weekly charts, so some follow-through buying should be seen this week. A weaker US Dollar caused buying interest in general in commodities. New York continues to be the weaker market on ideas of big and never-ending production in Brazil.

London remains the stronger market as Vietnamese production is not moving. There is not much Robusta on offer in the world markets right now even though supplies in storage in Europe are very high. Brazil weather remains good for harvesting and as production is thought to be very big at around 60 million bags. The harvest is now entering its final stages.

It has been dry in Vietnam, and there is little on offer from that origin as producers want to see how big the next crop will be and try to wait for higher prices. Better rains are reported to be improving crop conditions now. The Vietnamese producer is mostly waiting in vain as prices internally have been moving lower for the last few weeks.

It remains mostly dry in Arabica areas of Brazil, and there is no rain in the forecast for the next week. Temperatures have been moderate. Origin is still offering in Central America and is still finding weak differentials. Growing conditions are good.

Weekly New York Arabica Coffee Futures © Jack Scoville

Weekly London Robusta Coffee Futures © Jack Scoville

Sugar

Futures were higher in New York but lower in London. London has become the weaker market as demand for refined sugar appears to be less. Meanwhile, raw sugar prices have held firmer, so processing and refining margins are getting squeezed. Ideas of big world production are keeping the market tone weak. Traders note dry conditions in Brazil, the EU, and Russia, but also note very good conditions in Thailand and India. Brazil producers are also worried about cane production even with the rapid early harvest. Much of the early cane harvest in Brazil has been used to make ethanol.

The dry weather in much of Europe and in southern Russia near the Black Sea has hurt sugar beets production potential in these areas. Wire reports on Friday highlighted the poor growing conditions in France and said major production losses are expected. India is exporting sugar again and has a large surplus to move. It could produce more than 35 million tons of sugar in 2018-19. Thailand has produced a record crop and is selling. Both countries are having trouble finding buyers according to wire reports.

Weekly New York World Raw Sugar Futures © Jack Scoville

Weekly London White Sugar Futures © Jack Scoville

Cocoa

Futures were sharply lower in both markets. Trends in both markets are down. The North American quarterly grind data showed a decline in processing, but the Asian data was very strong. The outlook for strong production in the coming year has been enough to keep the prices weak. Main crop production ideas for Ivory Coast are near 2.0 million tons.

Ideas that current weather conditions are good for the next crops in West Africa continue. There have been reports of good rains throughout the region and big yields are possible. Showers and more seasonal temperatures have been seen in the last few weeks to improve overall production conditions in West Africa. Conditions also appear good in East Africa and Asia.

Weekly New York Cocoa Futures © Jack Scoville

Weekly London Cocoa Futures © Jack Scoville

—

DISCLAIMER: This article expresses my own ideas and opinions. Any information I have shared are from sources that I believe to be reliable and accurate. I did not receive any financial compensation in writing this post, nor do I own any shares in any company I’ve mentioned. I encourage any reader to do their own diligent research first before making any investment decisions.

Wyrmgold Launches Crowdfunding Campaign for Believe in me! (please)

Wyrmgold has launched a Gamefound campaign for Believe in me! (please), a darkly humorous board game where 2–4 players compete...

Fintech and AI: Adoption Grows, but Profits Favor Agile Innovators

AI is becoming standard in financial services, but adoption doesn’t guarantee returns. While most institutions use AI, many remain stuck...

AseBio 2025 Report Highlights Growth and Future Potential of Spanish Biotechnology

AseBio presented its 2025 report on the Biotech Act, highlighting opportunities for Spanish biotechnology while urging greater ambition, funding, and...

Bitcoin and Ethereum Markets Steady as Strategy and Bitmine Expand Holdings Amid World Cup Crypto Activity

Bitcoin trades sideways around $66,000 while ETFs see $64 million outflows. Strategy bought 1,587 BTC for $100 million and increased...

SBTi Net-Zero Standard 2.0 Enhances Corporate Climate Action

The Science Based Targets initiative (SBTi) has released Corporate Net-Zero Standard Version 2.0, a major update to its global framework...

|

|

|  |

|

|

-

Crowdfunding5 days ago

Crowdfunding5 days agoSustainable Restoration of the Haus Hövener Garden in Brilon

-

Crowdfunding2 weeks ago

Crowdfunding2 weeks agoImpact Food Launches Crowdfunding to Expand Plant-Based Fast Food Concept

-

Cannabis1 day ago

Cannabis1 day agoEurope’s Cannabis Shift: Rising Use, and New Risks

-

Markets1 week ago

Markets1 week agoSugar Markets Rise Slightly Amid War, Oil Price Pressure, and Strong Global Supply

You must be logged in to post a comment Login