Featured

Demand Remains Strong for US Cotton Even With the Weaker Export Sales Reports

Cotton futures were little changed last week as futures held to the trading range formed at the beginning of February again. USDA cut export demand and increased ending stocks for the US on Wednesday. It’s been a demand market and futures have been correcting lower over the last few sessions in search of new demand. Ideas are that demand remains strong for US Cotton even with the weaker export sales reports over the last couple of weeks.

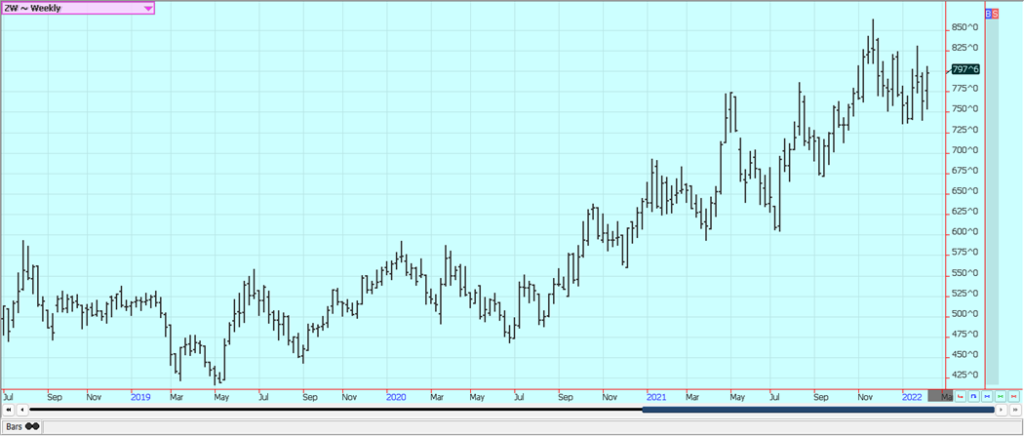

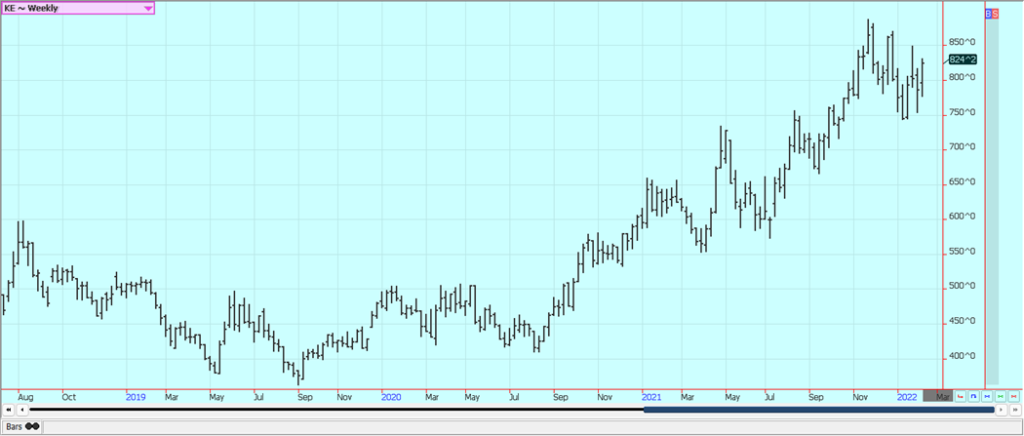

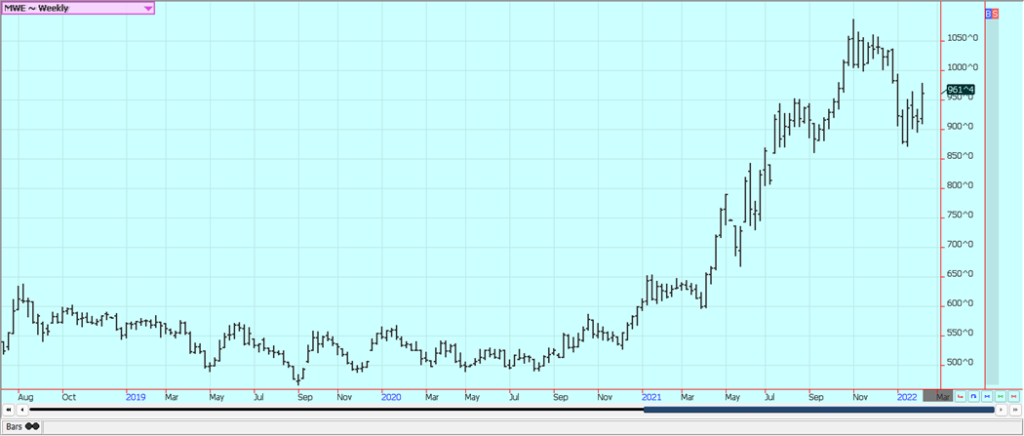

Wheat: Wheat markets traded higher on Friday and formed an outside day up on the daily charts. Futures were higher for the week as tensions started to heat up in Ukraine again. The US said last week that Russia could invade at any time and that Putin has given the army orders to invade and take the Ukraine state back into the orbit of Russia. Ukrainians have no interest in living under Russian occupation so the war could be deadly and very costly to both sides. Russia and Ukraine are both major Wheat exporters so the Wheat market could be damaged. USDA cut demand on the domestic and the export side again in its reports released on Wednesday. It increased the US ending stocks but cut world ending stocks due to reduced Middle East and North African production. It remains dry in the western Great Plains but some precipitation is expected. Ideas had been that the US will have good demand for Wheat as the rest of the northern hemisphere is short production this year but so far demand has been average or less against previous years. Dry weather in southern Russia, as well as the US Great Plains and Canadian Prairies, caused a lot less production. The lack of production has reduced the offers and Russia has announced sales quotas. Australian crop quality should be diminished. North Africa is very dry.

Weekly Chicago Soft Red Winter Wheat Futures

Weekly Chicago Hard Red Winter Wheat Futures

Weekly Minneapolis Hard Red Spring Wheat Futures

Corn: Corn closed higher last week along with Soybeans as both markets reacted to the South American production estimates released by Conab in Brazil and the Rosario exchange in Argentina. There is still support as the weather and the new WASDE reports showed reduced production for South America and no change in the US supply and demand estimates. South American production estimates were lower than USDA by a wide margin. Oats were higher and have broken out to the upside. The South American agricultural areas got an inch or less of precipitation and are now turning hot and dry again. Crop losses are becoming more and more of a reality for the Corn market right now. The Soybeans harvest farther north is being somewhat delayed due to wet weather and this might affect planting of the Safrinha crop in Brazil. Planted area there as well as in the US is in question due to the high costs and the lack of availability of inputs for growing a successful crop.

Weekly Corn Futures

Weekly Oats Futures

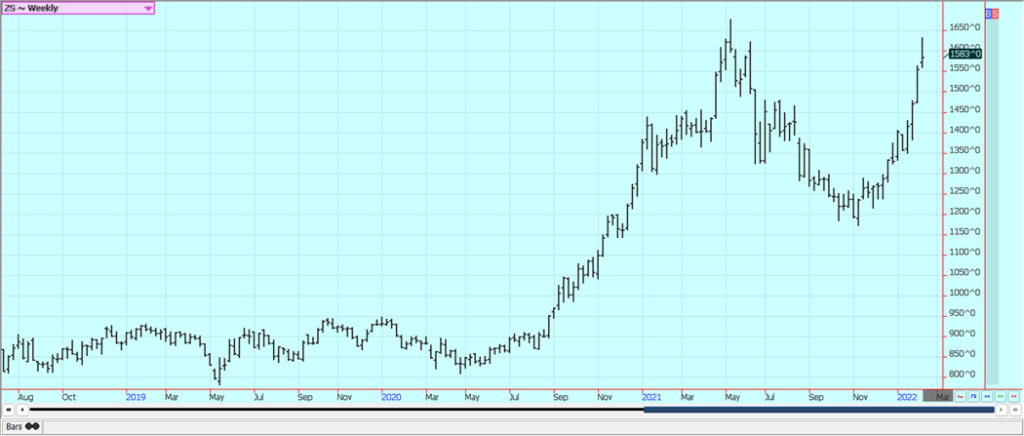

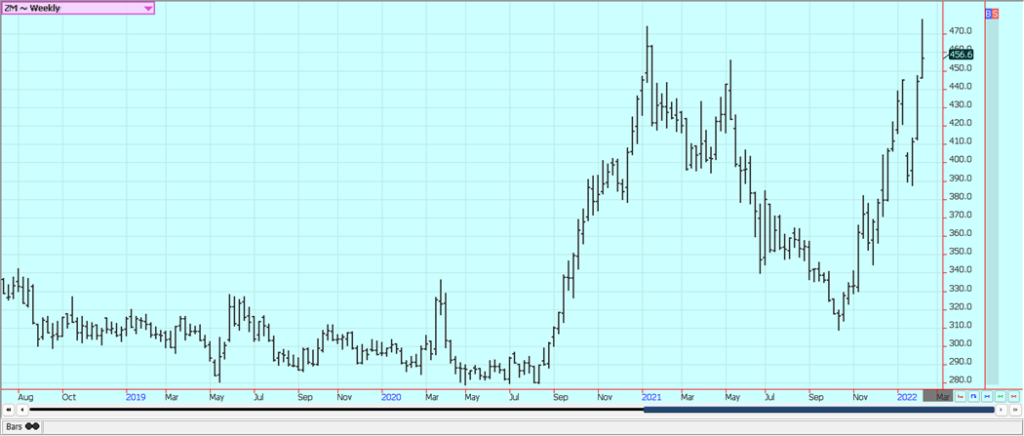

Soybeans and Soybean Meal: Soybeans and the products were higher last week as Conab in Brazil and the Rosario exchange in Argentina released sharply lower Soybeans production estimates. Speculators were early buyers and then became sellers and producers were sellers above 1600 March. It is possible that the market topped out on Thursday at least for the short term. The market had been supported on what appeared to be speculative buying in response the release of the WASDE reports that showed increased domestic demand and unchanged production and export demand. The South American production estimates were cut but not as much as expected by the trade. World-ending stocks levels were lower as well. The South American weather remained difficult. Mostly hot and dry conditions are expected for the next week. It will stay very wet in central and northern parts of Brazil. Crop losses are becoming more and more of a reality for the Soybeans market right now.

Weekly Chicago Soybeans Futures:

Weekly Chicago Soybean Meal Futures

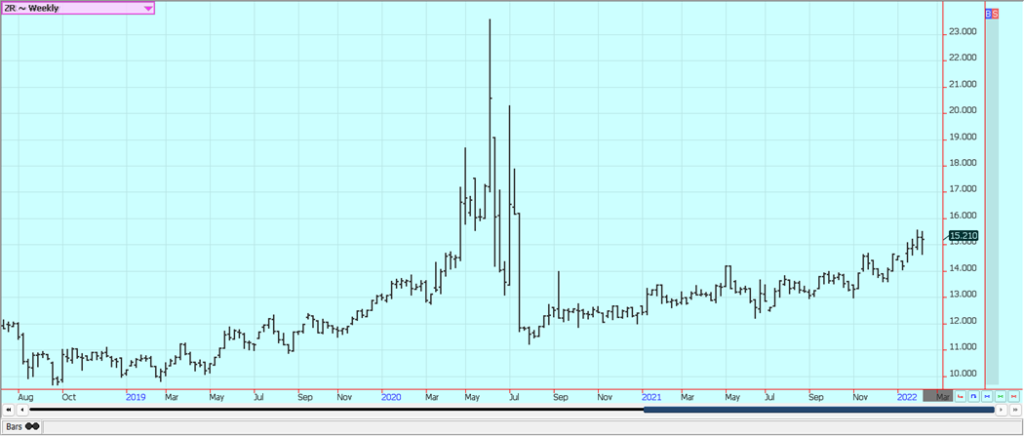

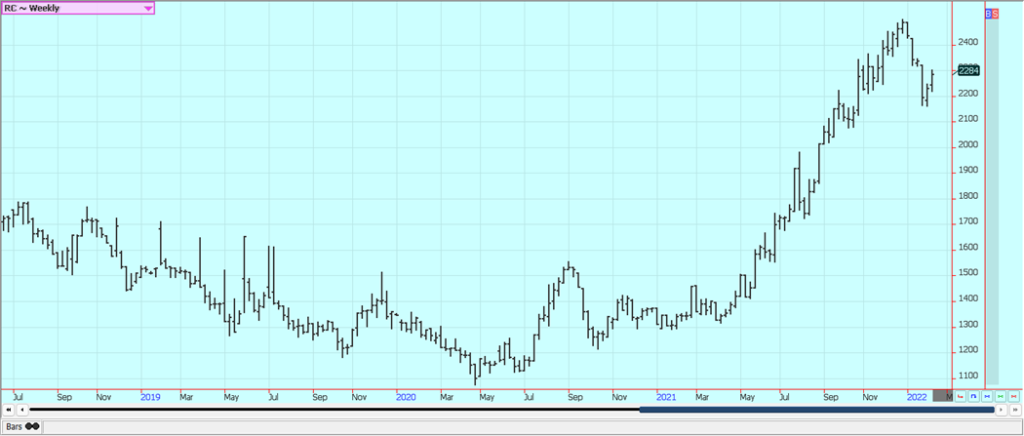

Rice: Rice closed a little lower last week on what appeared to be some speculative selling in response to bearish chart patterns. Those chart patterns started to reverse to higher on Friday as futures made an outside day up on the daily charts. USDA left Long grain estimates unchanged in its monthly WASDE estimates released on Wednesday. It has been a demand-led market recently and the weekly export sales report yesterday was very strong. The cash market is showing that domestic mill business is around everywhere. Many producers are not interested in selling but some are selling the current crop and generating some needed revenue. Producer sales are reported to have been way ahead of average early in the marketing year so stocks on hand in first hands are reported to be lower than normal. Mills are showing more interest in the market as previously bought supplies start to run low. The cash market is reported to be relatively strong in moderately active trading as prices have held firm. Ideas are that there is very little Rice left in producer control.

Weekly Chicago Rice Futures

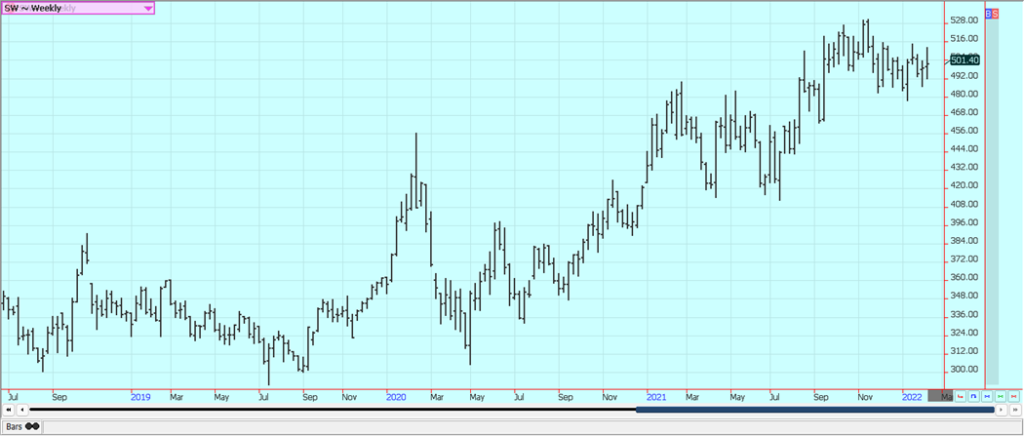

Palm Oil and Vegetable Oils: Palm Oil was higher last week after reports of reduced production and stocks for Malaysia. Demand in Malaysia could improve soon as Indonesia is expected to keep most Palm Oil at home. Indonesia is once again making moves to cut the availability of Palm Oil for export as it seeks to keep more at home for biofuels purposes. There are still poor production conditions in Malaysia and Indonesia. Traders are mostly worried about demand from India who has been buying Soybean Oil in the US instead of Palm Oil from Malaysia and Indonesia and is also worried about China and its demand for Palm Oil for biofuels. Canola was higher last week along with Chicago. Chart trends are mixed.

Weekly Malaysian Palm Oil Futures

Weekly Chicago Soybean Oil Futures

Weekly Canola Futures:

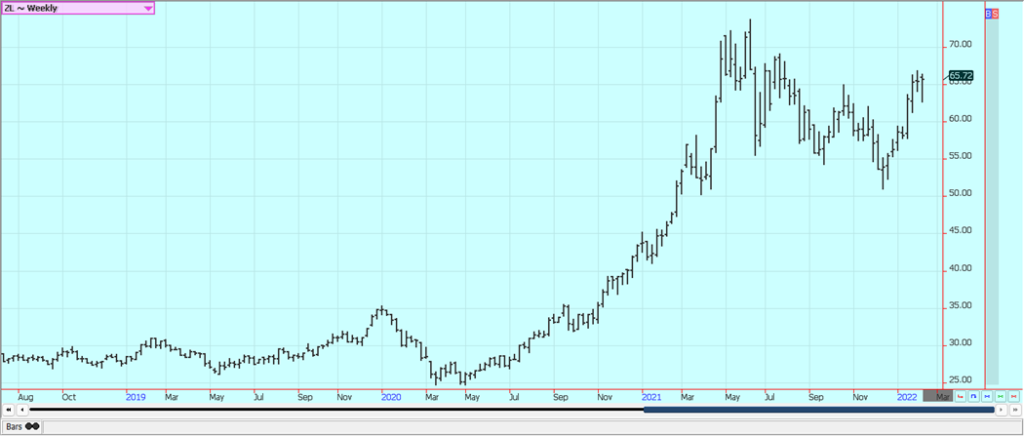

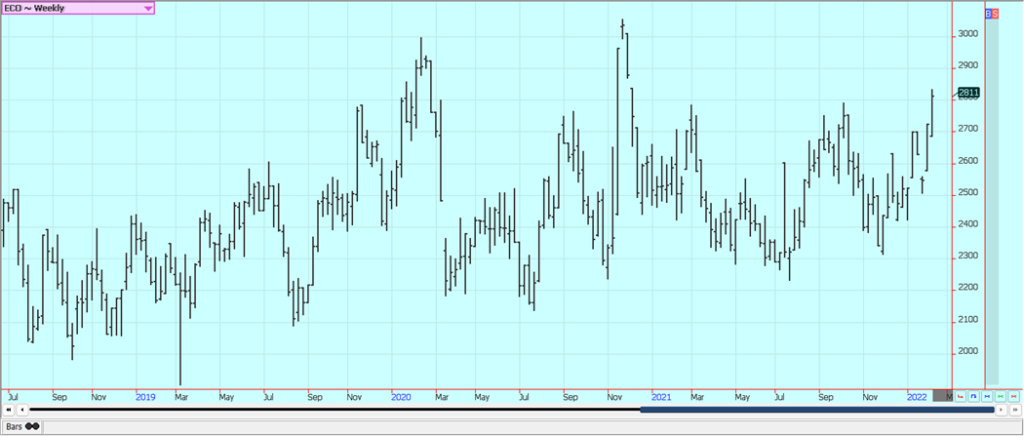

Cotton: Cotton futures were little changed last week as futures held to the trading range formed at the beginning of February again. USDA cut export demand and increased ending stocks for the US on Wednesday. It’s been a demand market and futures have been correcting lower over the last few sessions in search of new demand. Ideas are that demand remains strong for US Cotton even with the weaker export sales reports over the last couple of weeks. Analysts say the Asian demand is still very strong and likely hold at high levels for the future. US consumer demand has been very strong as well despite higher prices and inflation. Good US production is expected for next year as planted area is expected to increase due to high Cotton prices and the expense of planting Corn. Chart trends are still mostly up in this market.

Weekly US Cotton Futures

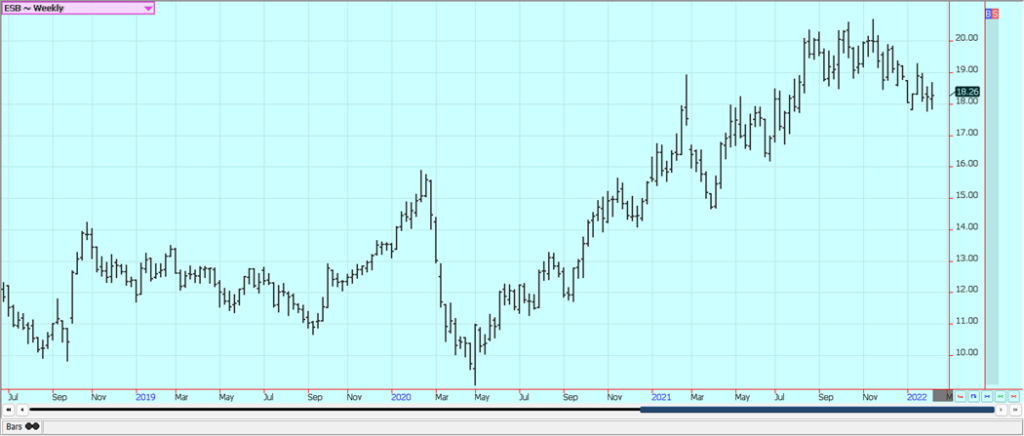

Frozen Concentrated Orange Juice and Citrus: FCOJ was little changed last week as USDA cut its Florida production estimate again on Wednesday. Ideas are that the lost production was already in the market. Florida Mutual said that FCOJ inventories are down 30% from a year ago, and this just highlights the tight supply even more. There are more moderate weather forecasts for the coming week or more. Freezing temperatures reported last weekend did little to hurt the crops. Temperatures in Florida are still below normal, but much warmer than last weekend. The trends are down on the daily charts. Brazil has some rain and conditions are rated very good. Brazil production was down last year due to dry conditions at flowering time and then a freeze just before harvest. Mexico is rated in good condition.

Weekly FCOJ Futures

Coffee: New York and London closed higher last week with the lack of offers from Brazil keeping prices well supported. Ideas continue that the next crop in Brazil is experiencing good growing conditions. Vietnamese producers have been selling and Brazil producers have sold some coffee for the next crop. Safras e Mercado said that producers in Brazil have sold well over 305 of the next crop already and the pacer is well ahead of a year ago. The dry weather and then the freeze in Brazil have created a lot of problems for the trees to form cherries this year. Big rains more recently in some Brazil growing areas have hurt cherry formation as well. The logistical situation in both Vietnam and Brazil has eased in recent weeks but is still considered difficult and expensive to manage. Brazil producers have sold most of the current year crop and are forward pricing for next year. Vietnam producers are also selling and some of the Robusta is going to the exchange in London as differentials have weakened. Vietnam is getting scattered showers on the coast but dry conditions inland. The rest of Southeast Asia should get scattered showers in the islands and mostly dry conditions on the mainland. Production conditions for the next crop in Colombia are not good due to too much rain. Vietnam exported 163,324 tons of coffee in January, down 3.6% from December last year.

Weekly New York Arabica Coffee Futures

Weekly London Robusta Coffee Futures

Sugar: New York and London were little changed in range trading last week and found support on ideas of reduced production from Brazil and hopes for increased demand. There have been reports of improved growing conditions for the crops in central-south areas of Brazil. Showers will continue into much of this week and crops should benefit from the return of moisture to the region. Hot and dry weather is expected for southern areas after the rains pass this week. Ideas are that the supplies are available from India and Thailand as harvests there are off to a good start and reports indicate that India has been selling. Demand is still thought to be good, but supplies could increase as less ethanol is produced. Philippines has tendered to buy 200,000 tons of White Sugar.

Weekly New York World Raw Sugar Futures

Weekly London White Sugar Futures

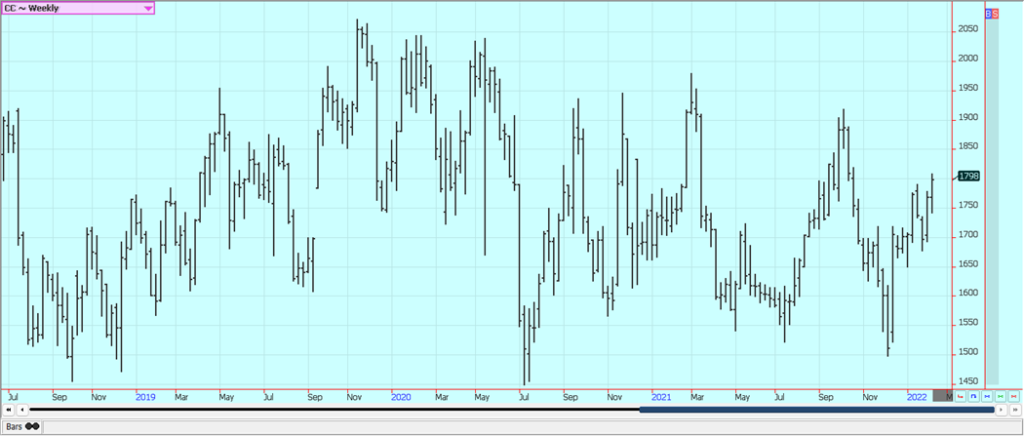

Cocoa: Both markets closed higher last week on ideas of bad weather in Ivory Coast. The weather is generally good for Southeast Asia but some producers in West Africa are worried about the dry weather that has been noted for the last couple of weeks. Ideas are that demand will continue to improve. Both Ivory Coast and Ghana are reporting deteriorating weather as it is now mostly sunny and dry. Some farmers want more rain for the best Spring harvest results. Ghana arrivals are now 383,000 tons so far this marketing year, from 681,000 tons last year.

Weekly New York Cocoa Futures

Weekly London Cocoa Futures

__

(Featured Image by Karl Wiggers via Unsplash)

DISCLAIMER: This article was written by a third party contributor and does not reflect the opinion of Born2Invest, its management, staff or its associates. Please review our disclaimer for more information.

This article may include forward-looking statements. These forward-looking statements generally are identified by the words “believe,” “project,” “estimate,” “become,” “plan,” “will,” and similar expressions. These forward-looking statements involve known and unknown risks as well as uncertainties, including those discussed in the following cautionary statements and elsewhere in this article and on this site. Although the Company may believe that its expectations are based on reasonable assumptions, the actual results that the Company may achieve may differ materially from any forward-looking statements, which reflect the opinions of the management of the Company only as of the date hereof. Additionally, please make sure to read these important disclosures.

Futures and options trading involves substantial risk of loss and may not be suitable for everyone. The valuation of futures and options may fluctuate and as a result, clients may lose more than their original investment. In no event should the content of this website be construed as an express or implied promise, guarantee, or implication by or from The PRICE Futures Group, Inc. that you will profit or that losses can or will be limited whatsoever. Past performance is not indicative of future results. Information provided on this report is intended solely for informative purpose and is obtained from sources believed to be reliable. No guarantee of any kind is implied or possible where projections of future conditions are attempted. The leverage created by trading on margin can work against you as well as for you, and losses can exceed your entire investment. Before opening an account and trading, you should seek advice from your advisors as appropriate to ensure that you understand the risks and can withstand the losses.

Youth Cannabis Use in Colorado Is Falling — But the Full Story Is More Complex

The 2026 Colorado survey shows teen cannabis use fell to 10 percent in 2025, down from 21 percent in 2015....

Morocco’s Growth Holds at 4.6% as Agriculture Offsets Economic Pressures

Morocco’s economy grew 4.6% in Q1 2026, driven by a strong agricultural rebound offsetting declines in industry. Services expanded moderately...

Abivax Shares Surge as New Trial Data Eases Safety Concerns Over Ulcerative Colitis Drug

Abivax shares surged nearly 36% after positive updated trial results for its ulcerative colitis drug obefazimod reassured investors following earlier...

El Dorado Raises $9M to Expand Cross-Border Fintech Platform

El Dorado, a Latin American fintech improving cross-border financial services, raised a $9 million Series A led by Paradigm with...

Bitcoin Stalls Near $60K as Strategy Moves, ETFs Outflow, and EU MiCA Rules Take Effect

Bitcoin hovers near $60,000 with ETF outflows, while Strategy boosts reserves, sells BTC, and raises dividends to reassure investors. Ethereum...

|

|

|  |

|

|

-

Biotech2 weeks ago

Biotech2 weeks agoBavarian Biotech Sector Expands with Record Funding and Startup Growth in 2025

-

Africa2 days ago

Africa2 days agoBOAD Approves Major Funding Boost to Drive West African Development

-

Business1 week ago

Business1 week agoMarkets Diverge as Oil Falls, Rates Hold, and Inflation Persists

-

Impact Investing6 days ago

Impact Investing6 days agoCoastal Cities Lead as Heat Strains Italy’s Urban Livability