Featured

A historical examination of the Dow Jones’ dividend

The pending failure in the corporate bond market will reflect on the Dow Jones’ dividend payouts. In the past nine years, dividend payouts for the Dow Jones have gone up.

The Dow Jones was down six points this week, effectively unchanged from last week’s close.

© Mark Lundeen

Below is the Dow Jones in daily bars. I circled this week’s data, and what little market action we saw this week. Be ye a bull or a bear; don’t get discouraged as there’s always next week.

© Mark Lundeen

Later in this article I’ve covered the history of the Dow Jones dividend yields and payouts. But as the stock market was very quiet this week, there isn’t much to comment on, so let’s move into gold.

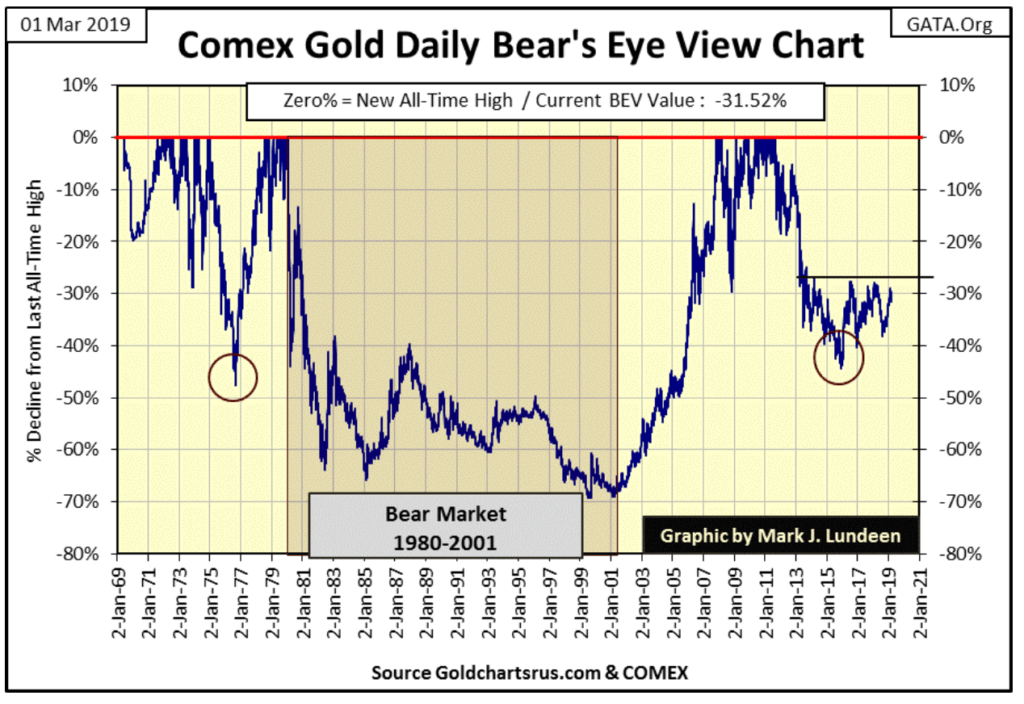

This week found gold below $1,300 for the first time since January 24th. But it’s evident in its BEV chart below that the retracement so far is minimal.

Gold in its current post-August 2011 bear market is a much different bear than it was from 1980 to 2001. At its deepest decline in December 2015 (-44.24%), gold had less downside than its correction low seen in August 1976 (-47.26%). This fact leads me to understand our current decline as more a correction within a bull market than a bear market. An incredibly frustrating correction, but a correction within a bull market nonetheless.

© Mark Lundeen

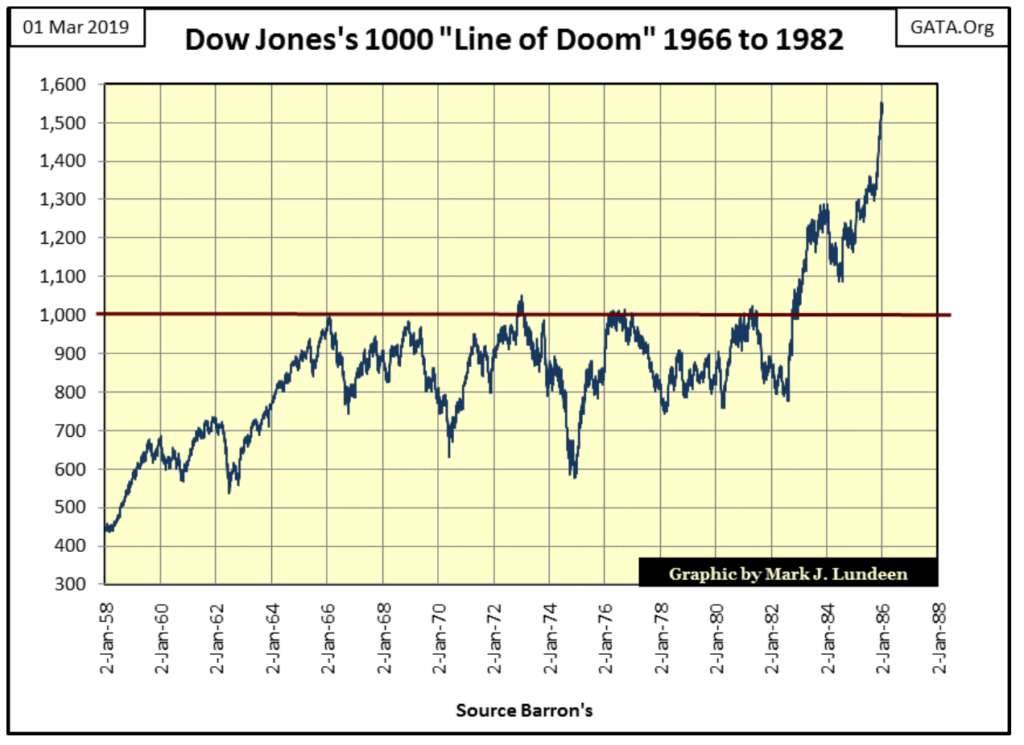

I’m also looking at the -27.5 BEV ($1366) line of resistance seen in the chart, where since 2013 this line has confounded all attempts by the bulls to break above and stay above it. It reminds me of the Dow Jones from 1966 to 1982, where Dow Jones 1000 proved to be the line of doom for the bulls (chart below).

Five times the bulls attempted to get the Dow Jones to break above and stay above 1000 during these sixteen years only to fail miserably on each attempt. When the Dow Jones finally did break above this line of resistance in October 1982, the ingrained bearishness of the market prevented most investors from believing what was happening before their very eyes; a new bull market had begun in the stock market.

For your information, our bull market, with the occasional 40% market corrections since January 2000, is the same bull market seen beginning in 1982 below.

© Mark Lundeen

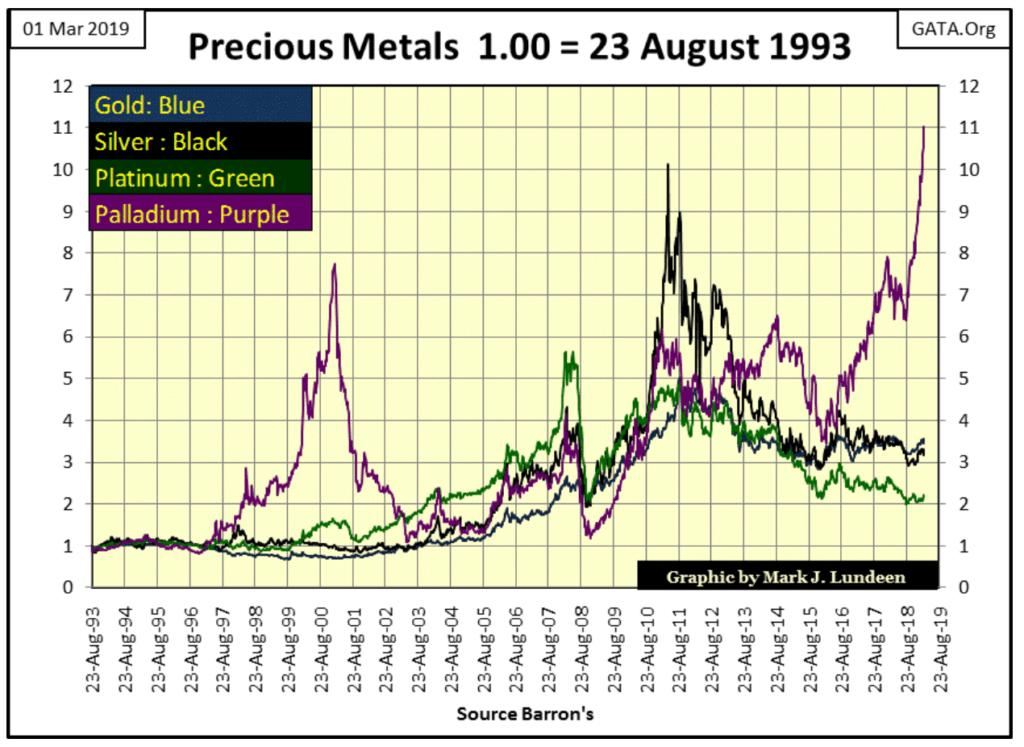

I had some comments last week on Craig Hemke’s revelation in the palladium market. One item I missed was an indexed chart for gold, silver, platinum, and palladium. So, I thought this week’s market commentary would benefit from this chart as it’s very interesting, especially in light of the line of doom chart above.

It’s not just gold that’s currently burdened by a multi-year line of resistance; silver and platinum are too. But look at palladium below (Purple Plot); since last August it has been making new all-time highs for the past six months. It broke loose of the policymakers’ valuation control system, and I don’t think they can get palladium back in their box.

© Mark Lundeen

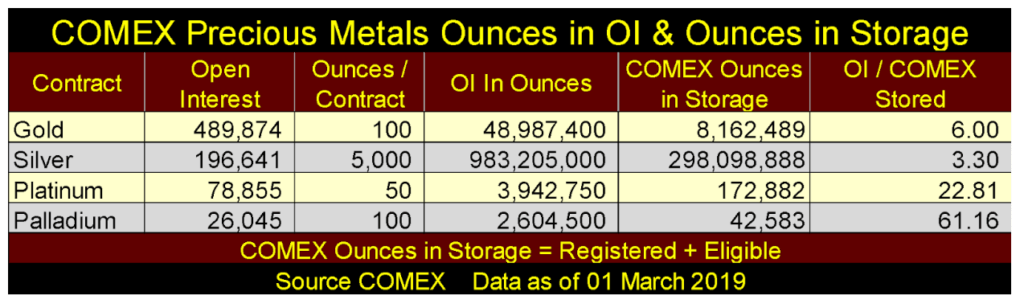

But they’re trying, as seen in the table below. The bears in the palladium market have promised to deliver 61.16 ounces of metal — metal that will never be delivered to the market for every ounce of palladium in COMEX storage.

The day is coming when the shorts (the sellers of paper palladium) in the palladium futures market are going to have to close their losing positions. To do so, they are going to have to buy long contracts in the futures market. What happens then maybe a historic moonshot for the price of palladium.

© Mark Lundeen

Considering the shorts in the palladium market are the same big banks and hedge funds that are now shorting gold and silver, a painful lesson in palladium may weaken their desire to participate rigging the gold and silver markets. Let’s pray that 2019 will prove to be a totally different year for gold and silver investors.

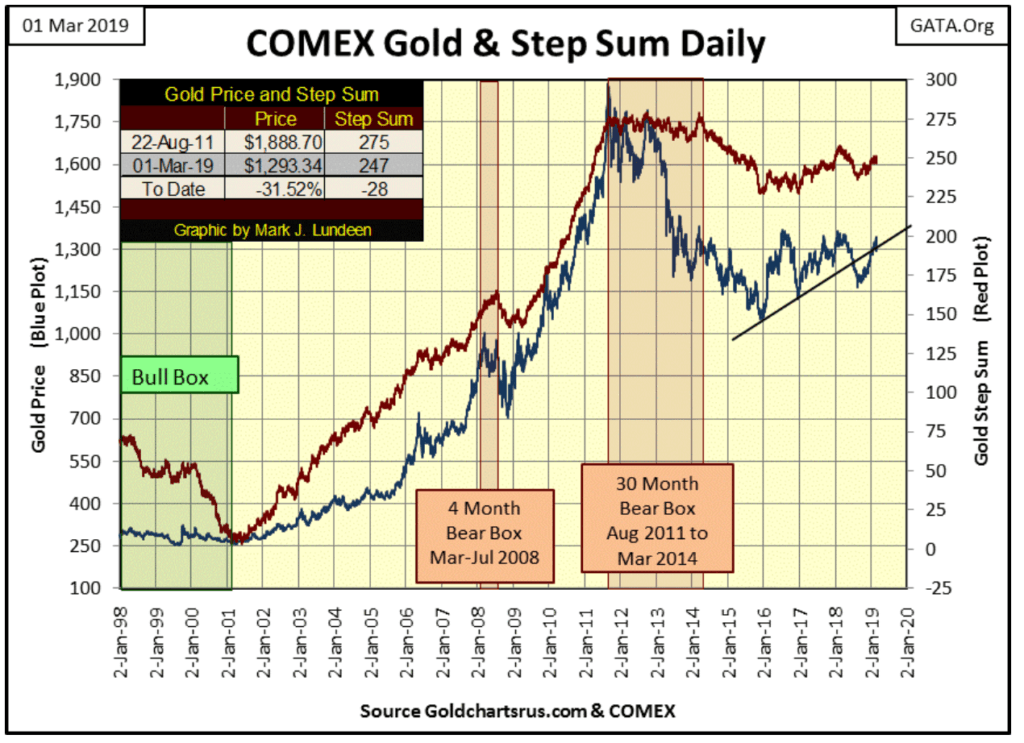

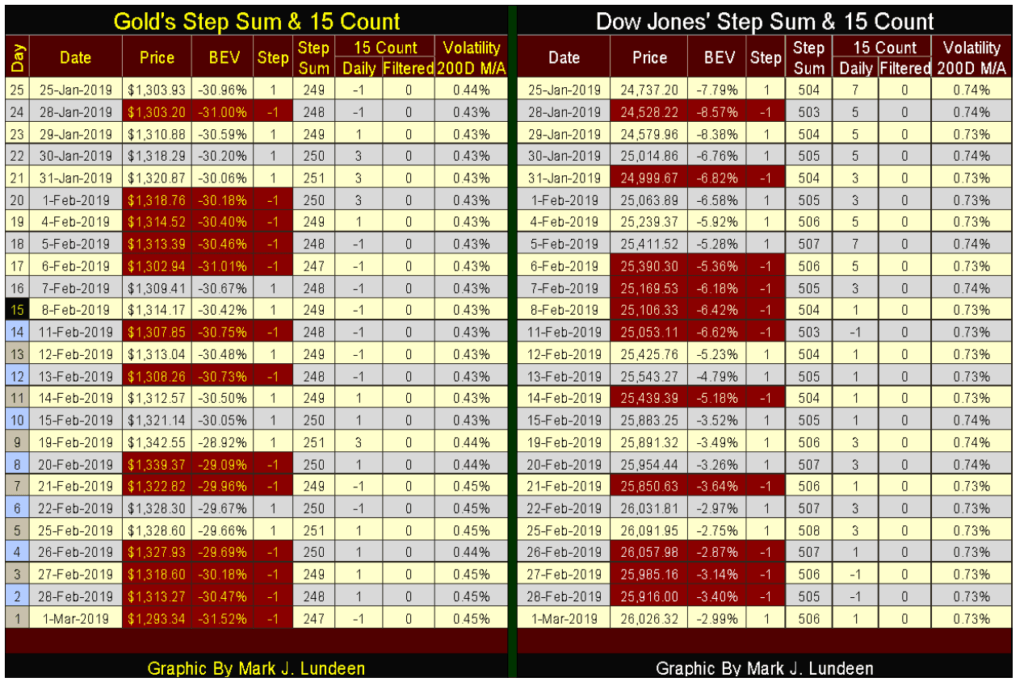

At the close of the week, gold and its step sum below still look positive. Yes, gold was down $35 since last Friday, but advances in any market always include some declines, just as market declines always see some advances. What gold needs to do now is break above its line of resistance at $1366; that done we may see the price of gold also breaking free of the policymakers’ bearish machinations.

© Mark Lundeen

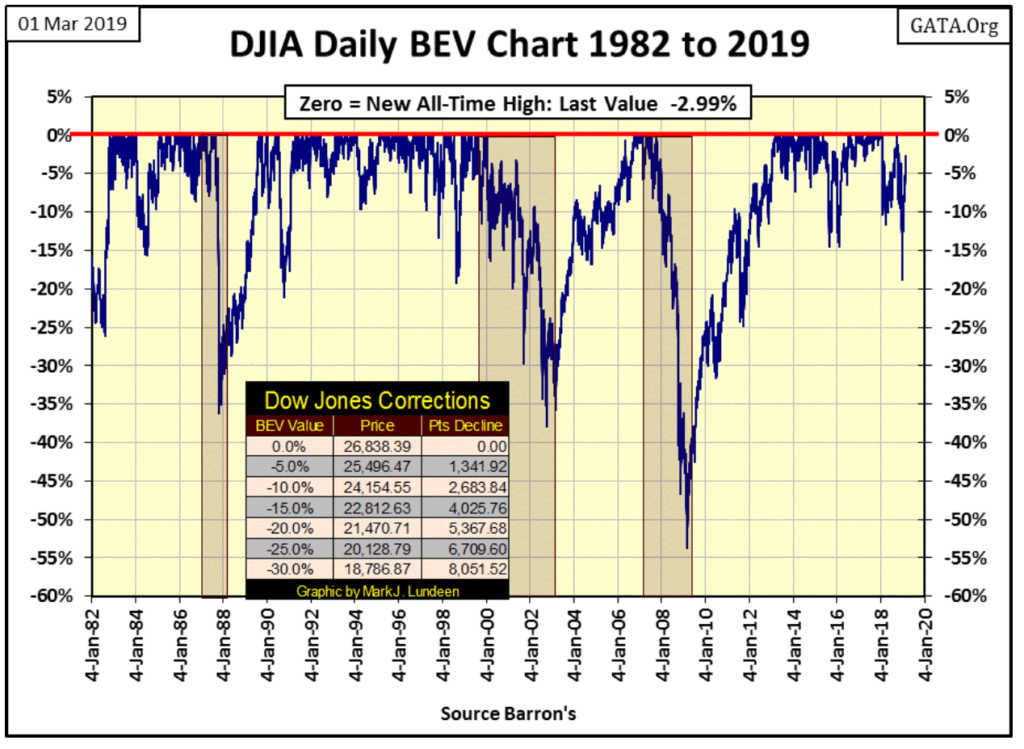

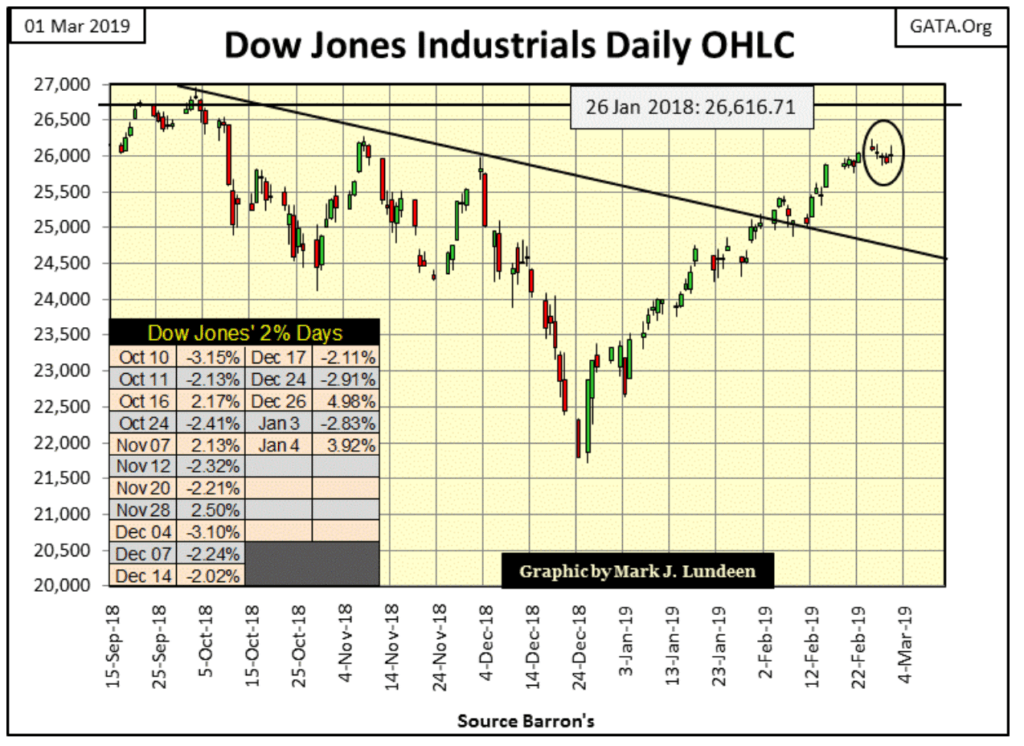

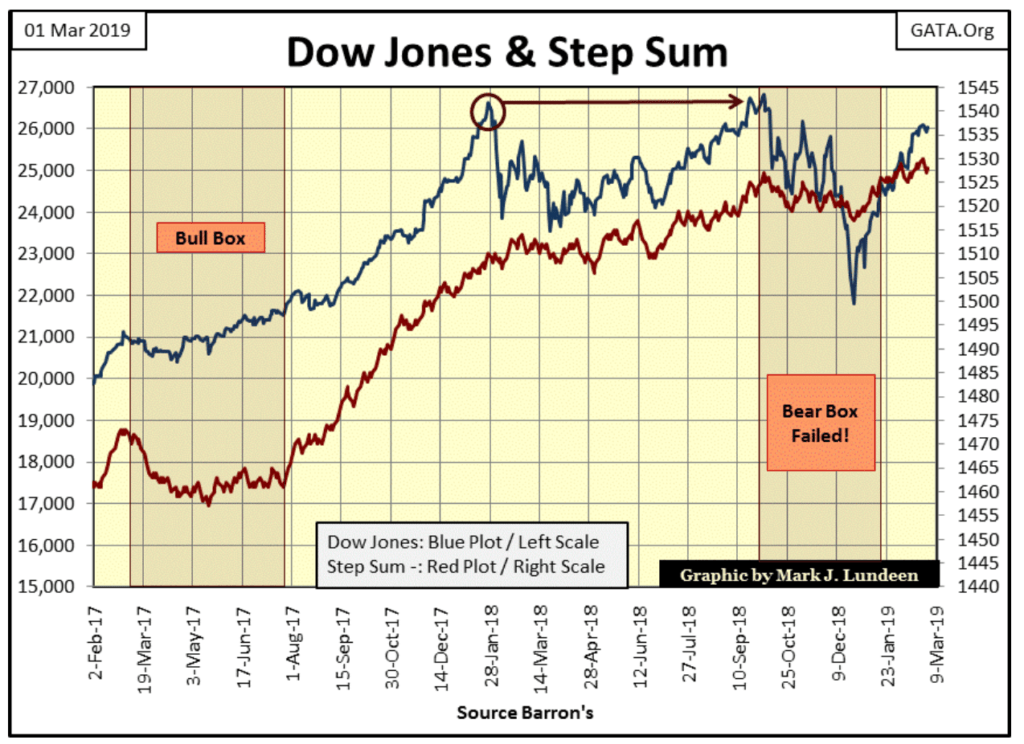

The Dow Jones and its step sum are looking good in the chart below. This week the Dow Jones closed only 2.99% from making a new all-time high. This gap between this week’s close and stock market history could easily be closed in the next few weeks; maybe next week.

What happens after that is the big question. I don’t expect the moonshot the Dow made in 1982-83, or the advance palladium has made since last August will prove to be the answer to this question.

I don’t know what the market capitalization for the NYSE and NASDAQ are, but after many decades of being inflated, they must be huge. To inflate these market valuations another 10% or even another 5% above their current all-time highs will be very difficult.

© Mark Lundeen

With its highs of January and October 2018, the Dow Jones has made a double top. I’m just speculating, but a giant bull market that’s been making history for the past thirty-seven years deserves to end in a dramatic fashion. A dramatic and rare triple top crowning this bull market would serve the purpose. Whether this happens or not is something we’ll all have to wait to see.

Gold and the Dow Jones step sum tables are generally bullish. Gold was down for the week. Looking at all that red for the past fifteen days one should not be surprised. But seeing the week close with a 15 count of -1 is actually a neutral indicator.

© Mark Lundeen

A step sum plot is only a single item A-D Line using the daily advances and declines in the Dow Jones or the price of gold as its input. The fact is during market advances there are about as many daily declines as advances, as with market declines, there are about as many advances as declines.

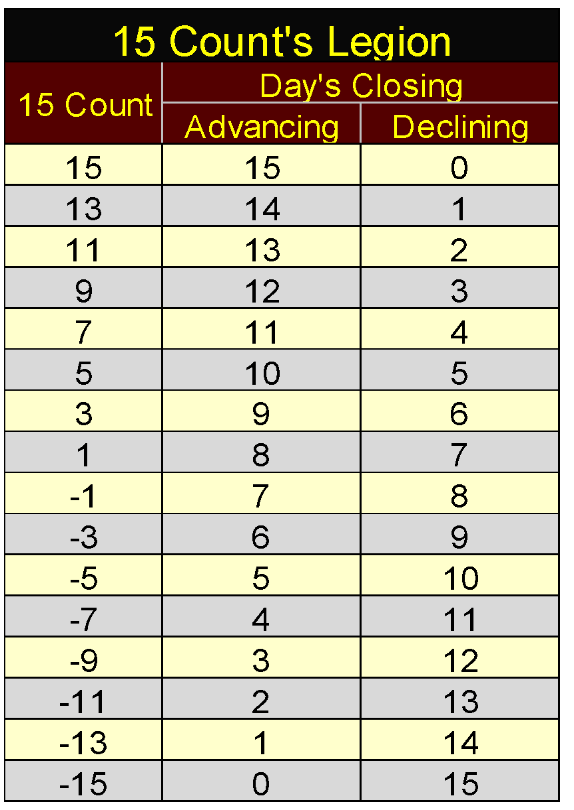

Looking at their 15 counts, gold closed the week at -1 while the Dow Jones at +1. The 15 count’s legion below tells us that gold in the past 15 days saw 8 daily declines and 7 advances, while the Dow Jones saw 8 daily advances and 7 declines. In other words, there isn’t much difference between a -1 and +1 in a 15 count. And that’s also pretty much true with the -3 and +3s in a step sum 15 count.

© Mark Lundeen

The 15 count becomes interesting when its values rise to 5 or more, with the (+/-) 9s to 15s being very rare and important short-term inflection points in the market. For example, a +9 or 11 indicates the market has seen a strong advance and is due for a pullback; a -9 or 11 indicates the market has seen a strong pullback and is due for a rebound.

But 9s or more in a step sum 15 count are very rare. Typically a market advances or declines with the majority of its step sum 15 counts between +3 and -3.

Two famous and long familiar American companies, Kraft and Heinz, were merged in 2015. As per the 2015 press release from Kraft-Heinz, the future couldn’t look brighter for these merged companies.

Four years later, CNN reports a one day collapse of 27% for shares of Kraft-Heinz on February 22nd on news of a 36% cut in its dividend, difficulties with debt service on its $31 billion long-term debt and an SEC investigation.

Some companies decided to use debt (at attractive rates) to fund their share buyback and dividend programs. For Kraft & Heinz, that meant a merger for these two companies in 2015. This fiasco, as well as General Electric’s of a few months ago, will ultimately prove to be the result of too much money, at rates far too low being injected into the financial system by the Federal Reserve.

The item that caught my attention — with both Kraft-Heinz and GE’s debt dilemmas — was how vulnerable their dividend payouts were. Kraft-Heinz reduced payouts by 36%. GE wanted to eliminate their dividend payout completely but decided to cut it back to only $0.01 a share so shares of GE would continue to be eligible for purchase by money managers.

These companies have been in operation for over one hundred years. Companies that stood firm as others failed during the Great Depression. But in the coming years, they may not survive Doctor Bernanke’s three bouts of quantitative easings and zero interest rate policy. They’ll have plenty of company before Mr Bear is finished cleaning up Wall Street and the global financial system.

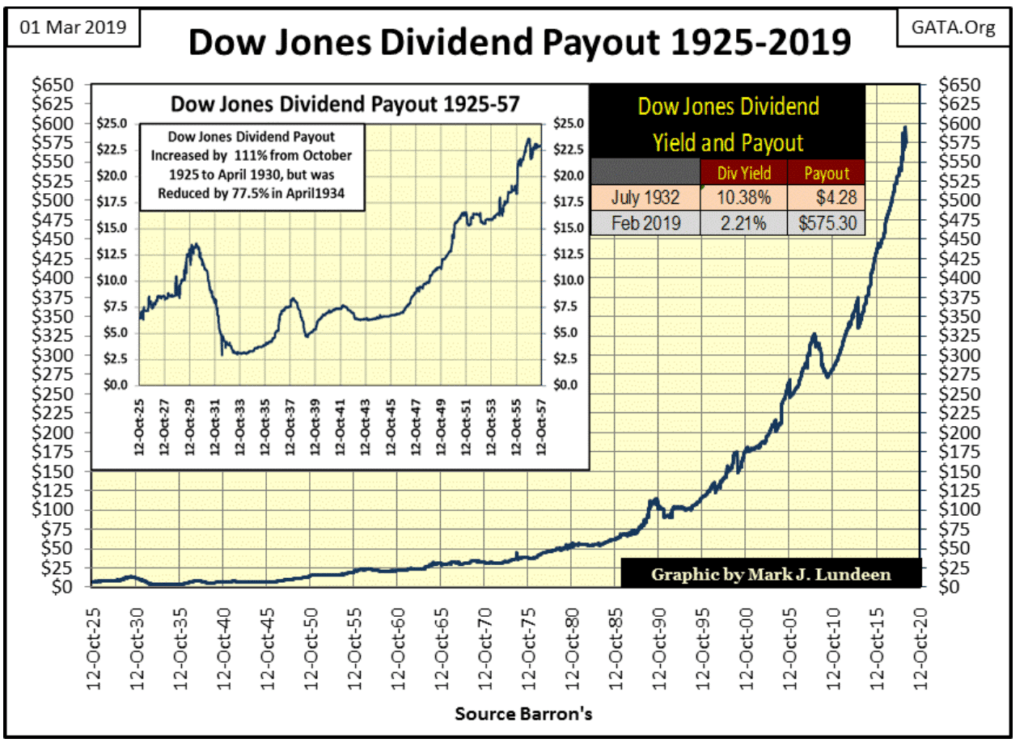

Speaking of dividend payouts, here’s a chart of the Dow Jones payouts since 1925. Before the 1929-32 crash, dividend payouts increased by 111% from October 1925 to April 1930 as the Federal Reserve System flooded Wall Street and the American economy with monetary inflation. However, good times funded by monetary inflation are short-lived. Note how dividend payouts for the Dow Jones were cut by 77.5% during the crash. A similar 77.5% reduction of today’s Dow Jones dividend payout would cut its cash payout from $577.78 to $130.

© Mark Lundeen

Dividends are profit-sharing programs corporations have for their shareholders. In the early 1930s, profits for business were hard to come by. Like the Post-Credit Crisis business boom, I suspect corporate America during the Roaring 1920s weren’t afraid of leveraging their balance sheets with debt. How many of those disappearing dollars in dividend payouts seen above during the early 1930s didn’t actually disappear at all, but were re-routed to service debts taken on during the 1920s inflationary boom?

But dividends are more than just a source of cash flow from corporate America. Like income from a bond, they also have a yield, an annual percentage rate of return for invested funds. But unlike bond income, dividends are not fixed income, as seen above.

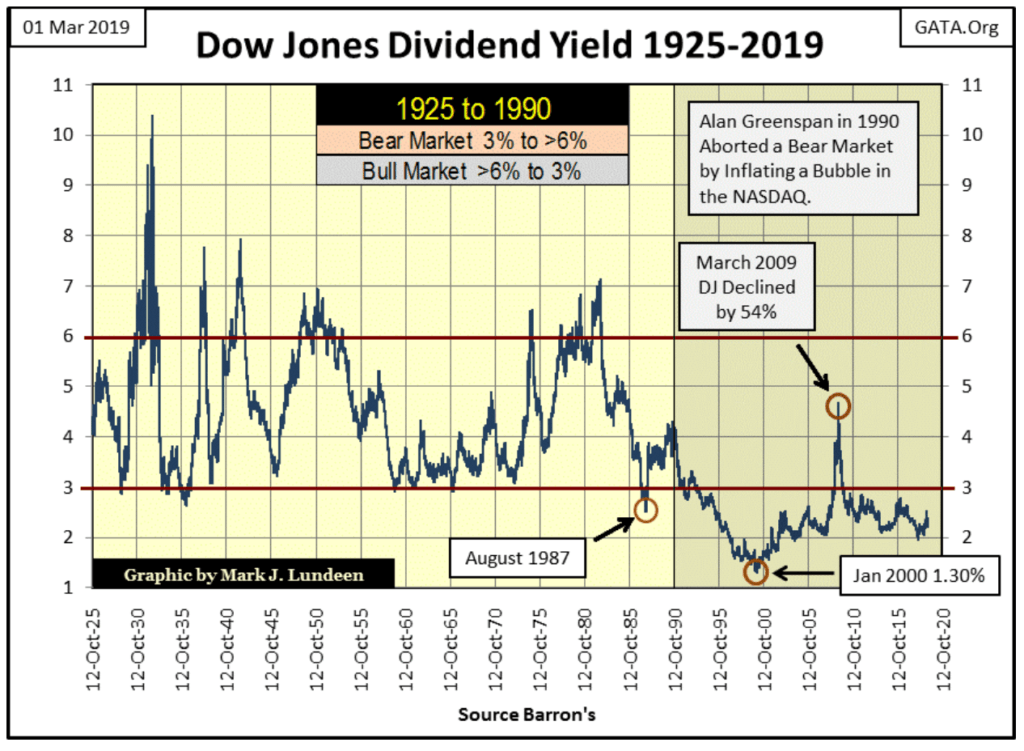

Dow Jones’ dividend yields going back to 1925 is a fascinating study of the stock market. From October 1925 to August 1987, investors could use these yields to time exits from overvalued markets (bull market tops) and re-entry points for undervalued markets (bear market bottoms). For sixty years, this rule-of-thumb; sell when yields declined to 3%, and buy back when the Dow Jones yielded something over 6% was all an investor needed to know to profitably invest in the stock market.

© Mark Lundeen

Sadly, all this changed in August 1987 when Alan Greenspan became Chairman at the Federal Reserve. Greenspan became Fed Chairman with the Dow Jones yielding its lowest since 1925 (2.54%). After the huge gains seen in the Dow Jones since August 1982 (five years, 250% advance), it was time for a bear market ending with a Dow Jones dividend yield at or above 6%. But that didn’t happen.

Instead, Greenspan inflated a historic bubble in the stock market where in January 2000 the Dow Jones yielded an incredible 1.30% (see chart above). In doing this Greenspan and his fellow policymakers have decoupled the stock market from any objective measurement of value, a situation that continues today.

From 2002 to the present, the yield for the Dow Jones has oscillated between 2% & 3%, with the exception for the 4.75% yield of 09 March 2009, at the bottom of the subprime mortgage bear market. This was the second deepest percentage decline in the Dow Jones since 1885, yet the yield for the Dow Jones only increased to 4.74%?

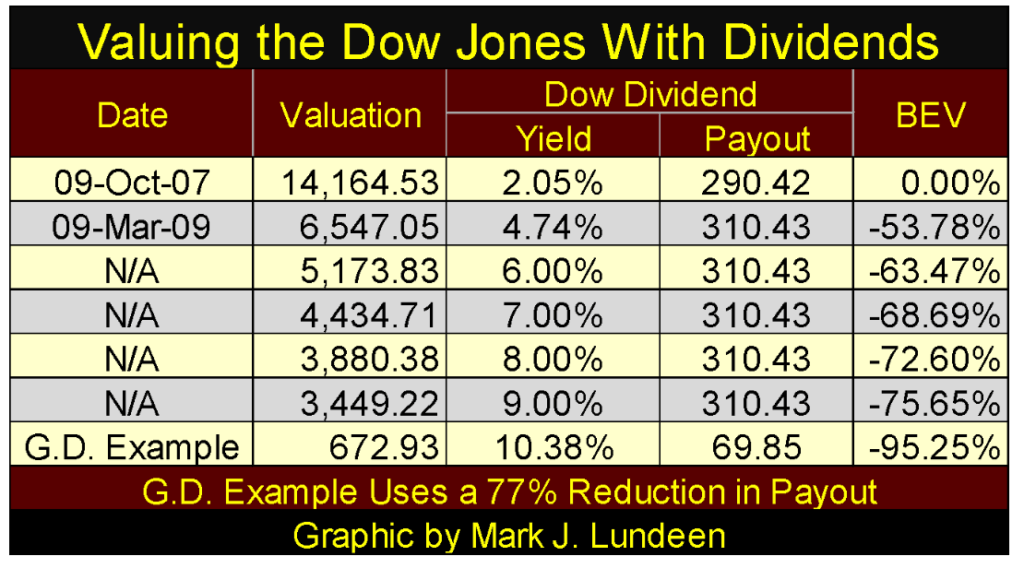

In 2008-09, had Doctor Bernanke not flooded the financial system with monetary inflation during his first QE, the Dow Jones would have fallen more than 54%, as its yield increased to something above 6%. As the Dow Jones payout at the time was $310.43, the traditional 6% yield found at bear market bottoms would have taken the Dow Jones down to 5,173, a 63% bear market decline. But who’s to say the bottom of the 2007-09 market decline would have stopped with a dividend yield of 6%, or Dow dividend payouts unaffected. This was a bear market that threatened to shut down the global banking system, something not seen since the early 1930s.

The table below is a model of the 2007-09 market decline using dividends from the Dow Jones’ 09 October 2007 market top to its bear market low of 09 March 2009. Those rows after the 09 March 2009 data illustrate possible bear market bottoms using dividend yields. These yields are well within the historic range (see chart above), and the Great Depression example which includes a 77% cut in dividend payout and its July 1932 yield of 10.38%.

© Mark Lundeen

Had Doctor Bernanke not reflated the financial markets with his three quantitative easings, the Dow Jones (my proxy for the broad stock market) could have seen all its gains since August 1982 wiped out. This was exactly what did happen during the Great Depression crash; valuations for the Dow Jones were deflated back to 1914 levels, all the way back to when the Federal Reserve began inflating the US money supply.

There are two methods for valuing the stock market. One is based on inflation, where the bulls study current market trends and project them on future valuations in the market. There is nothing wrong doing this; as long as the market is a bull market.

The other is based on dividends in the Dow Jones, the preferred method for the bears from 1925 to 1987, as seen in the above chart for the Dow Jones dividend yields. For sixty-two years the smart money would exit their bullish positions when the Dow Jones declined to 3%, and wouldn’t become bullish again until it once again yielded something above 6%. However, as noted above, that hasn’t worked since Alan Greenspan became Fed Chairman in August 1987.

But I’m assuming this decoupling of market valuations from their dividend fundamentals is only a temporary anomaly; an anomaly that has endured for the past thirty-seven years, but will ultimately prove to be a temporary anomaly nonetheless.

When will the Dow Jones and the broad stock market’s valuations once again be coupled to their dividend fundamentals? I can’t give a date when this will happen. However, in the coming bear market, when the policymakers lose their grip on market valuations, I expect Mr Bear will once again recouple stock-market valuations to their dividend fundamentals. Learning exactly how overvalued the shares trading on the NYSE and NASDAQ has been since Alan Greenspan became Fed Chairman will be a brutal experience.

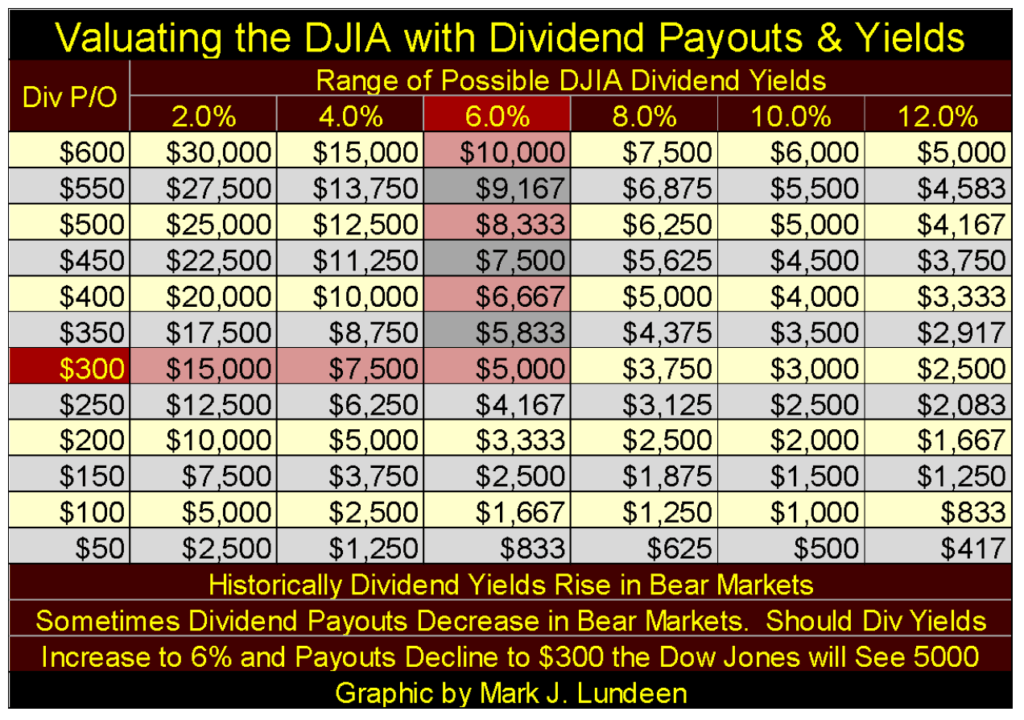

The table below gives Dow Jones valuations at the intersection of the listed dividend payouts and yields. For example, at the close of this week the Dow Jones had a payout of $577.78, a 2.22% yield fixing the Dow Jones at 26,026. If in the coming stock market deflation the Dow Jones sees its payout reduced to $300, and its yield increase to 6%, the Dow Jones would see its valuation deflated to 5,000. That’s a whopping -81% market decline from its last all-time high of October 3rd of last year (26,838), and an 81% bear market for the Dow Jones may be a future best case scenario.

© Mark Lundeen

A best-case scenario? Well, this is what I’m thinking of: accounting is important. I don’t have all the specifics, but after the 9-11 attack came the Patriot Act that made Wall Street a bear-free zone in times of national emergencies. As I recall the Patriots Act also had some provisions in it that also denigrated accounting standards. This was certainly true during the 2007-09 credit crisis.

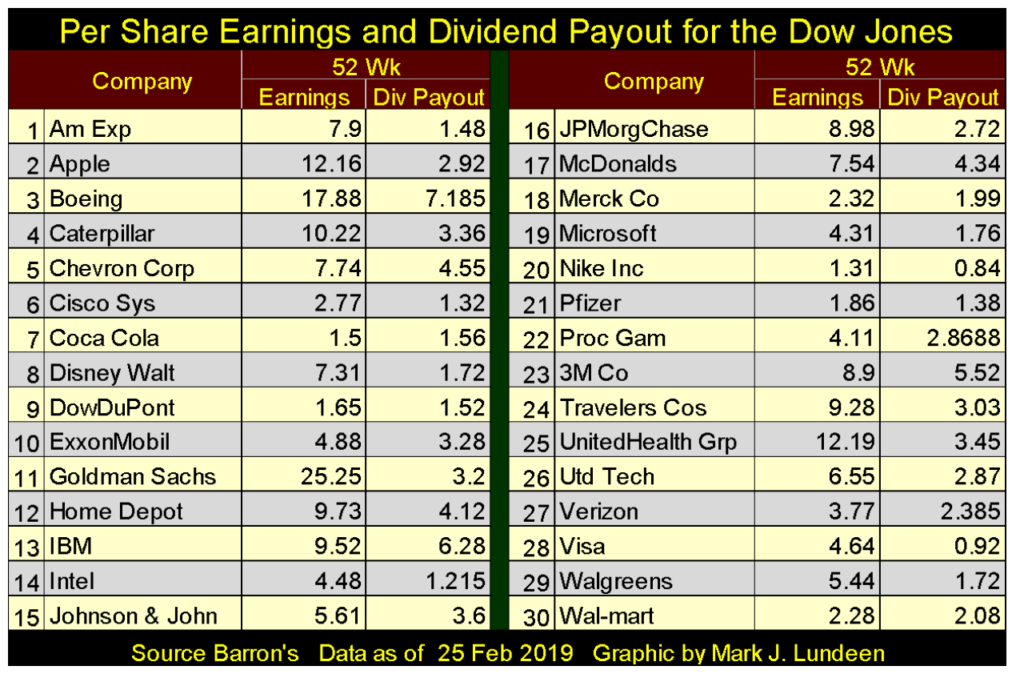

I’m not an accountant, but I doubt many people would question my assertion that accounting standards since the 1950s have been compromised. Believing that to be true and looking at the earnings and dividend payouts for the Dow Jones below, I wonder just how solid these published values are?

© Mark Lundeen

In an X22 Report Spotlight on Harley Schlanger, Mr. Schlanger had some very interesting comments on the $13 trillion global corporate bond market.

-

-

First is corporate debt in the bond market has doubled since 2008.

-

-

54% of these bonds are currently rated BBB or lower – near or rated as junk.

I believe it’s a safe assumption the thirty corporations included in the Dow Jones have all sold bonds. What isn’t a safe assumption is that all the thirty corporations listed above have their bonds rated as AAA investment grade.

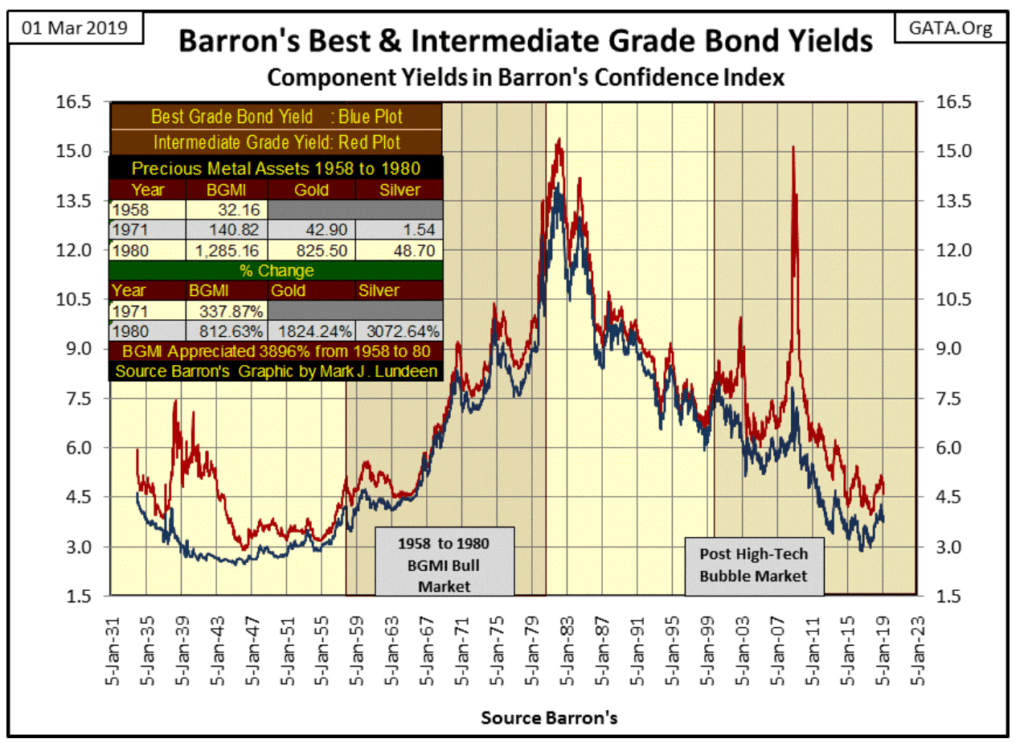

As Mr. Schlanger noted, many companies now struggling to service their bonds interest payments are very vulnerable to increases in bond yields. Here’s a chart plotting Barron’s Best and Intermediate Grade Bond Yields going back to 1934. Corporate bond yields bottom a few years ago, yet are still at levels not seen since the early 1960s.

Here is a question whose answer could mean the difference between your investments being a success or failure in the years to come: are corporate bond yields going to continue rising, or will they resume a decline that began in October 1981?

© Mark Lundeen

For myself, I’m going to assume bond yields have bottom years ago and have no place to go but up in the years to come. The inevitable outcome for this will be massive defaults in the corporate bond market – bankruptcy for those corporations who can’t pay their debts.

I’m also going to assume a good number of companies listed in the Dow Jones and the S&P 500 have burdened their balance sheets during the good times with more debt than can be serviced in the coming bad times.

The impact of this pending failure in the corporate bond market will be seen in the Dow Jones dividend payouts. For the past nine years, dividend payouts for the Dow Jones have only gone up (see chart above). Since February 2010 they have increased by 119%.

The Dow Jones itself can decline without seeing a decline in its dividend cash payouts — happens all the time. However, as was the case in the early 1930s; seeing a 77% decline in payouts for the Dow Jones spoke volumes on the structural imbalances to corporate finance the boom years of the 1920s had fostered.

(Featured image by ymgerman via Shutterstock)

—

DISCLAIMER: This article expresses my own ideas and opinions. Any information I have shared are from sources that I believe to be reliable and accurate. I did not receive any financial compensation for writing this post, nor do I own any shares in any company I’ve mentioned. I encourage any reader to do their own diligent research first before making any investment decisions.

Morocco’s Growth Holds at 4.6% as Agriculture Offsets Economic Pressures

Morocco’s economy grew 4.6% in Q1 2026, driven by a strong agricultural rebound offsetting declines in industry. Services expanded moderately...

Abivax Shares Surge as New Trial Data Eases Safety Concerns Over Ulcerative Colitis Drug

Abivax shares surged nearly 36% after positive updated trial results for its ulcerative colitis drug obefazimod reassured investors following earlier...

El Dorado Raises $9M to Expand Cross-Border Fintech Platform

El Dorado, a Latin American fintech improving cross-border financial services, raised a $9 million Series A led by Paradigm with...

Bitcoin Stalls Near $60K as Strategy Moves, ETFs Outflow, and EU MiCA Rules Take Effect

Bitcoin hovers near $60,000 with ETF outflows, while Strategy boosts reserves, sells BTC, and raises dividends to reassure investors. Ethereum...

Cannabis Dominates Global Drug Use: Trends, Risks, and Shifting Markets

Cannabis remains the world’s most widely used illicit drug, with 256 million users in 2024, surpassing all others combined. Growth...

|

|

|  |

|

|

-

Cannabis7 days ago

Cannabis7 days agoSpain Cannabis Laws: Private Use, Fines, and Grey Areas

-

Crowdfunding2 weeks ago

Crowdfunding2 weeks agoWyrmgold Launches Crowdfunding Campaign for Believe in me! (please)

-

Business2 days ago

Business2 days agoDow Jones Near Highs Signals Strength Until Volatility Returns

-

Crypto1 week ago

Crypto1 week agoXRP Under Pressure Amid Macro Forces, Fed Policy, and Regulatory Shifts