Featured

How the U.S. Dollar Influences the Price of Cotton Futures

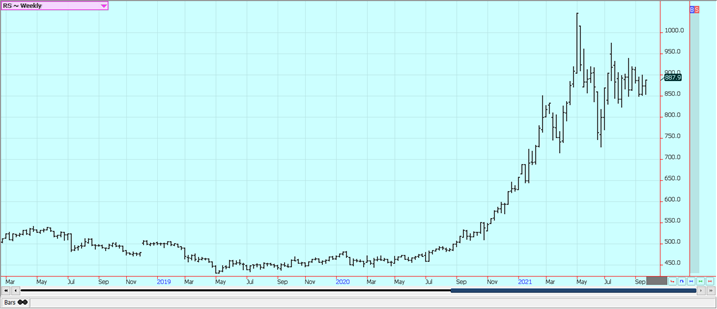

Cotton futures were higher on Friday in response to a stronger U.S. dollar and a strong weekly export sales report. The weekly charts imply that significantly higher prices are coming soon. Demand for US Cotton remains very strong and that is good news for sellers as the strong demand implies strong prices should continue. The demand is expected to be strong from Asian countries.

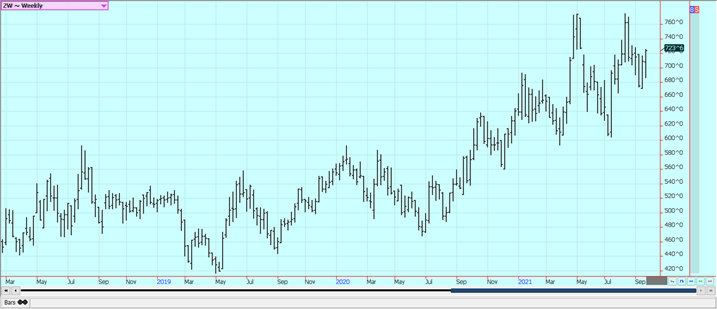

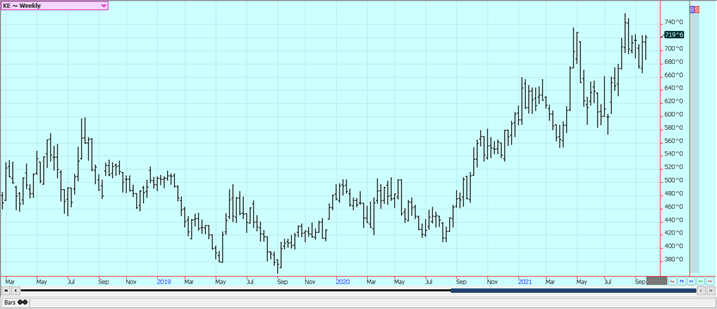

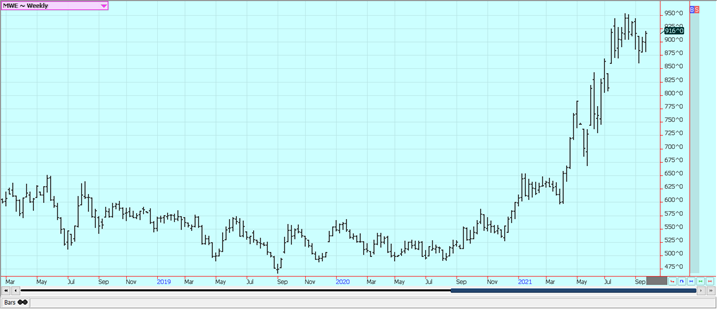

Wheat: Wheat was higher in all three markets last week as trends started to turn up on the daily and weekly charts. The weekly export sales report showed average sales but there is more talk that Russia would severely restrict Wheat exports due to production lost to drought. Production is less this year and internal prices have been strong. Dry weather in southern Russia as well as the northern US Great Plains and Canadian Prairies remains a supportive feature in the market although the weather has become old news. The Russian weather has been good for production in northern and western areas but is still trending dry in southern areas and into Kazakhstan. Siberian Spring Wheat conditions have been very good. Europe is expecting top yields in some areas but less yield in others and parts of eastern Europe and northern Russia are expecting strong yields. European quality is a problem due to too much rain in some areas and not enough in others.

Weekly Chicago Soft Red Winter Wheat Futures

Weekly Chicago Hard Red Winter Wheat Futures

Weekly Minneapolis Hard Red Spring Wheat Futures

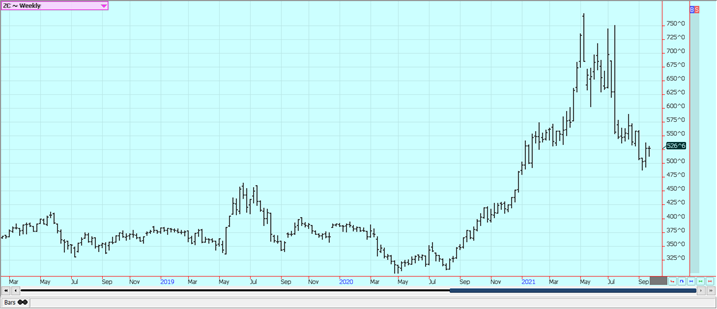

Corn: Corn was near unchanged for the week and is breaking out to the upside on the daily charts even with ideas of expanding harvest progress and weaker demand. Trends remain down on the weekly charts. Traders are now waiting on the harvest and yield reports but the gut slot of the harvest is still a week away. Ideas are that the yield reports will be high and will confirm the USDA production estimates or even find better yields. However, there have been reports of diseases in Illinois fields so record production might not happen in that state. Initial yield reports have been mixed, with some lower yields reported due to disease. There are still the drought-reduced crops in the northwestern Corn Belt and northern Great Plains to be counted as well. Most of the elevators along the Mississippi are starting to export again which is good news for nearby demand. New Orleans area elevators are now reported to be about 50% open. Electricity has been restored and the elevators are transloading grain if they are not fully open yet. The weather remains a feature of the trade but is less important now as the Corn is filling kernels and starting to mature. The EPA could ask the Biden Administration to reduce its blending requirement for Ethanol and could cut Corn demand in a significant way. Ideas are that Brazil Corn production could be less than 85 million tons so reduced production estimates are expected in coming reports. Oats are sharply higher on reduced Canadian production estimates. A large part of the US Oats consumption is fed by Canadian Oats.

Weekly Corn Futures

Weekly Oats Futures

Soybeans and Soybean Meal: Soybeans and Soybean Oil closed higher Friday despite the approaching harvest, but Soybean Meal was lower. The weekly charts show downtrends for all three markets. The debt ceiling fight in Congress and Chinese demand is supportive. People are worried about the taper away from debt by the Fed and how that will go as well. Harvest will soon be underway for Soybeans. The destruction of Gulf port facilities along the Mississippi River near New Orleans was still a factor in the trade but the elevators are coming on line and exports are increasing slowly. The hurricane moved onshore in Louisiana a week ago and did extensive damage to the state, including the grain export elevators. The state also lost electrical posser in all affected areas but power to the export elevators is being restored. China was the major buyer of US Soybeans in the weekly report even with cancellations showing. The demand news was positive for prices even though sales were down from the previous week and are less than the previous year.

Weekly Chicago Soybeans Futures:

Weekly Chicago Soybean Meal Futures

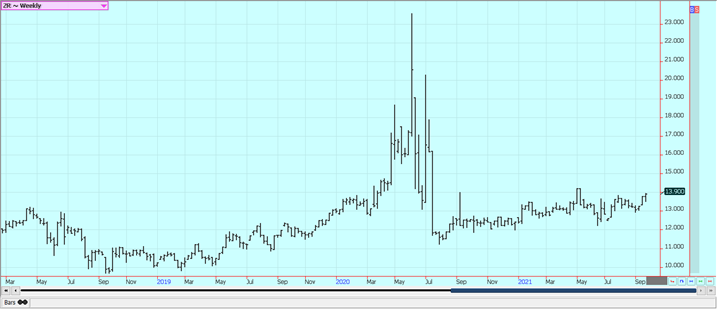

Rice: Rice closed higher last week on what appeared to be commercial buying. November futures finally broke strong resistance at 1380 and closed above that level for the last few days and this is considered a positive technical sign for prices. The first crop has been largely harvested in Texas and in Louisiana, but the second crop s still in the field and is still at risk of loss in both states. Harvesting will start to wind down in both states now. Mississippi and Arkansas producers are at harvest now. Yield reports and quality reports have been acceptable to many in Texas and are called good in Louisiana. The reports have been good in both Arkansas and Mississippi.

Weekly Chicago Rice Futures

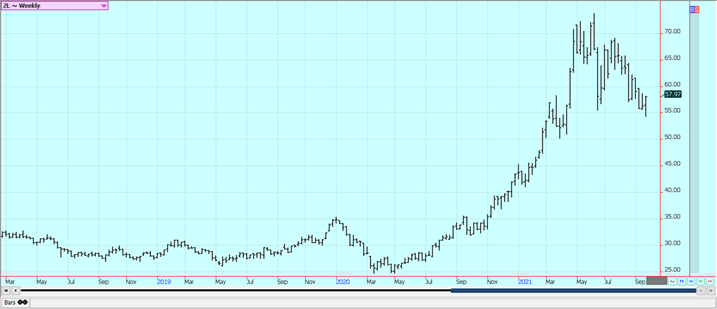

Palm Oil and Vegetable Oils: Palm Oil closed higher last week on ideas of reduced production. It was lower Friday as liquidation selling was seen before the weekend and the new round of export data. The weekly chart trends are sideways. Export volumes were up very significantly for Malaysia for the month so far. Ideas of strong export demand, especially from India, kept futures higher today. Exports were not strong last month and the trade saw big ending stocks when MPOB released its monthly data last week. Ideas are that Palm Oil got too expensive when compared to the other vegetable oils markets. There are ideas of tight supplies due to labor problems. There are just not enough workers in the fields due to Coronavirus restrictions. Production has also been down to more than offset the export losses so prices have trended higher. Canola closed higher on Chicago price action as the harvest is underway amid good conditions in the Prairies. The weekly chart trends are sideways. Production ideas are down due to the extreme weather seen in these areas. It remains generally dry and warm in the Prairies. The Prairies crops are in big trouble now due to previous hot and dry weather.

Weekly Malaysian Palm Oil Futures

Weekly Chicago Soybean Oil Futures

Weekly Canola Futures:

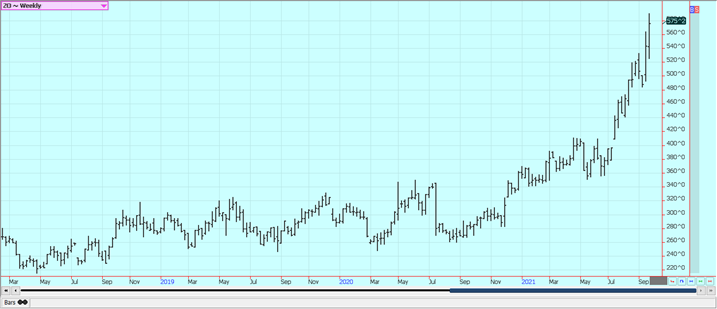

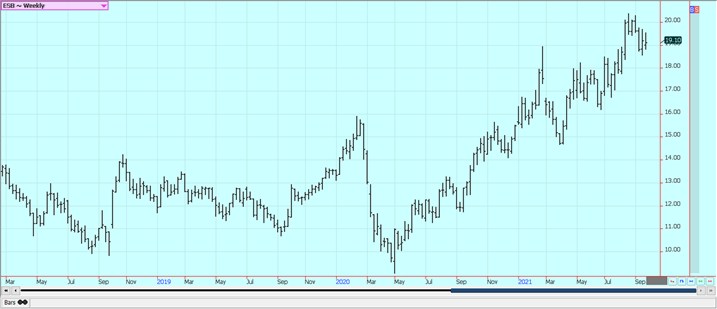

Cotton: Futures were higher on Friday in response to a stronger US Dollar and a strong weekly export sales report. The weekly charts imply that significantly higher prices are coming soon. Demand for US Cotton remains very strong and that is good news for sellers as the strong demand implies strong prices should continue. The demand is expected to be strong from Asian countries as world economies recover from Covid lockdowns. Analysts say the demand is still very strong and likely to hold at high levels for the future. However, the expansion of the Delta variant has given pause to the better demand ideas due to fears of economies here and around the world starting to partially lockdown again. Those fears were magnified yesterday by the debt crisis here and the Evergrande crisis in China. Production ideas are being impacted in just about all areas due to the weather extremes. It has been very hot in parts of Texas and the Delta and Southeast have had drenching rains at various times in the last couple of months. Bolls are opening now so any new system to git the Southeast would have a much better chance to damage the fiber. Good US production totals are expected.

Weekly US Cotton Futures

Frozen Concentrated Orange Juice and Citrus: FCOJ closed lower on Friday and a little lower for the week after trading both sides unchanged as weather concerns, especially for Brazil but also for Florida and Mexico, remained important. A freeze hit Sao Paulo state several weeks ago and reports of significant losses are being heard. Weather conditions in Florida are rated mostly good for the crops with scattered showers and near-normal temperatures. Mexican crop conditions in central and southern areas are called good with rains, but earlier dry weather might have hurt production. Northeastern Mexico areas are too dry, but the rest of northern and western Mexico are rated in good condition. Florida is in the middle of the hurricane season but the storms have missed the state so far and crop conditions are good.

Weekly FCOJ Futures

Coffee: New York closed much higher and London closed higher last week. It remains a bull market on a lack of supplies available from origin. New York has found support from the lack of Coffee available in Brazil after extreme weather events. London is having trouble sourcing Coffee from Vietnam due to a shortage of containers to carry the Coffee out of the country and as the country suffers from a resurgence of the Covid epidemic. Prices in New York have been firm as the current Brazil harvest starts to wind down. Dry weather and warm temperatures are seen now in Brazil for the last of the harvest. Scattered showers are now in the forecast for Southeast Asia. Good conditions are reported in northern South America and good conditions reported in Central America. Conditions are reported to be generally good in parts of Africa.

Weekly New York Arabica Coffee Futures

Weekly London Robusta Coffee Futures

Sugar: New York and London were both a little lower last week and the charts imply that the current rally attempt might be running out of steam. There is still talk of a squeeze developing as the market moves to September expiration. The reduced production potential from Brazil is still impacting the market. India is not offering as world prices are well below domestic prices. The ISO has noted that this will be the second year of deficit production for the world, in large part because of the Brazil freeze that cut production. Consumption of Sugar remains on the light side. Fears that Covid is coming back and could reduce economic activity and demand are still around. Thailand is expecting improved production.

Weekly New York World Raw Sugar Futures

Weekly London White Sugar Futures

Cocoa:

General Comments: New York and London closed lower Friday and chart trends are turning down on the weekly charts in New York. The weekly charts in London are still showing up trends. There are increasing concerns that Ghana will have less production this year. Ghana is the world’s second-largest producer behind Ivory Coast. It signed a deal to borrow money for crop financing and export financing for the year. Ivory Coast has stopped selling for the next crop on fears of less supplies. World economies are starting to reopen after Covid and the open economies are giving demand the boost. The weather has had below-normal rains in West Africa and crop conditions are rated good for now but there is concern about the lack of rain. Drier weather will be beneficial for the harvest which will be underway soon. Some are forecasting less production in the coming year. Ivory Coast sources told wire services that the country has sold between 1.64 million and 1.66 million tons of Cocoa so far this season. This is considered a very big amount and there are concerns about Cocoa availability at origin moving forward. Cocoa production in Ivory Coast is expected to drop by up to 11% in the 2021/2022 season that starts on Oct. 1 from last year.

Weekly New York Cocoa Futures

Weekly London Cocoa Futures

__

(Featured image by Erbs55 via Pixabay)

DISCLAIMER: This article was written by a third party contributor and does not reflect the opinion of Born2Invest, its management, staff or its associates. Please review our disclaimer for more information.

This article may include forward-looking statements. These forward-looking statements generally are identified by the words “believe,” “project,” “estimate,” “become,” “plan,” “will,” and similar expressions. These forward-looking statements involve known and unknown risks as well as uncertainties, including those discussed in the following cautionary statements and elsewhere in this article and on this site. Although the Company may believe that its expectations are based on reasonable assumptions, the actual results that the Company may achieve may differ materially from any forward-looking statements, which reflect the opinions of the management of the Company only as of the date hereof. Additionally, please make sure to read these important disclosures.

Futures and options trading involves substantial risk of loss and may not be suitable for everyone. The valuation of futures and options may fluctuate and as a result, clients may lose more than their original investment. In no event should the content of this website be construed as an express or implied promise, guarantee, or implication by or from The PRICE Futures Group, Inc. that you will profit or that losses can or will be limited whatsoever. Past performance is not indicative of future results. Information provided on this report is intended solely for informative purpose and is obtained from sources believed to be reliable. No guarantee of any kind is implied or possible where projections of future conditions are attempted. The leverage created by trading on margin can work against you as well as for you, and losses can exceed your entire investment. Before opening an account and trading, you should seek advice from your advisors as appropriate to ensure that you understand the risks and can withstand the losses.

Crypto Markets Edge Up as Caution Persists and April Fools’ Scams Loom

Bitcoin and Ethereum rise slightly amid geopolitical easing and renewed ETF inflows, with BTC near $68,000 and ETH above $2,100....

Lowryder: The Autoflowering Revolution in Cannabis Cultivation

Lowryder is a groundbreaking cannabis strain that introduced autoflowering, allowing plants to flower automatically without light changes. Created by The...

Casablanca Climbs the Global Financial Ranks

Casablanca has risen to 49th in the Global Financial Centres Index, strengthening its position as Africa’s top financial hub. It...

Crypto Lending Hits $30 Billion, Becomes Key DeFi Pillar

The decentralized crypto lending market has surpassed $30 billion, signaling a structural shift in capital use. Protocols like Aave and...

Advances in LDL Cholesterol Management for Familial Hypercholesterolemia: From Statins to Innovative PCSK9 and CETP Inhibitors

PCSK9 inhibitors have transformed LDL cholesterol management in familial hypercholesterolemia, with new antibodies and CETP inhibitors like obicetrapib expanding options....

|

|

|  |

|

|

-

Fintech2 weeks ago

Fintech2 weeks agoPayPay Targets Global Expansion After Landmark IPO

-

Impact Investing1 day ago

Impact Investing1 day agoItalian Unlisted Banks Lag on ESG Sustainability

-

Crypto1 week ago

Crypto1 week agoThe Iran War Tests Bitcoin and Crypto Market Resilience

-

Crypto6 days ago

Crypto6 days agoCrypto Markets Volatile as Bitcoin Hovers, Solana Eyes AI Integration