Featured

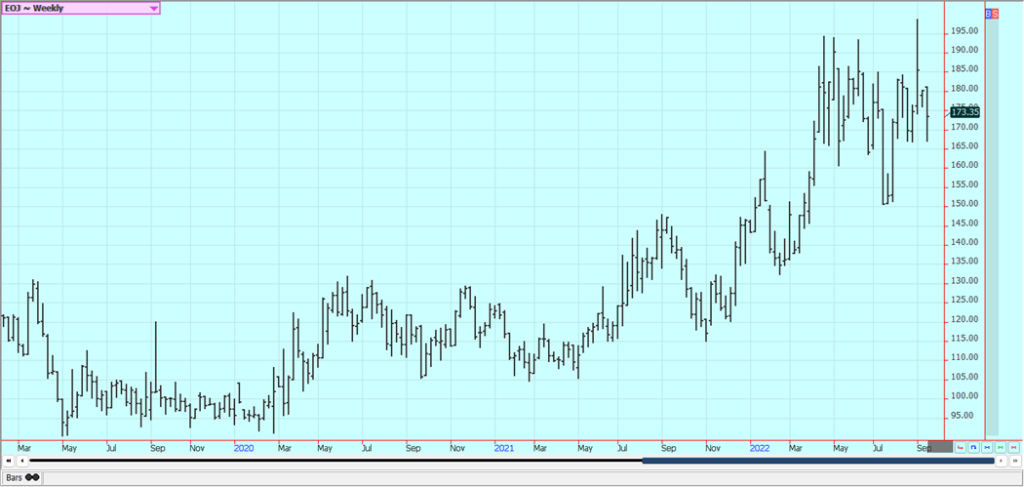

Rice Prices Might Increase if India Restricts Exports

Rice was a little higher last week but could not make new weekly highs. Futures closed just below those levels on Friday. The USDA reports showed smaller production and ending stocks estimates. Demand for Rough Rice was cut hard, but demand for Milled Rice held together in the latest estimates. News that India will restrict exports of some grades of Rice also supported futures

Wheat: Wheat markets edged higher last week and the weekly charts show that all three markets could have completed their harvest lows. The moves are hard and slow on the strength of the US Dollar and no one is sure what will happen to exports from Ukraine and Russia. USDA world supply and demand estimates showed a lot more Ukrainian and Russian Wheat production. Those countries still need to get the Wheat out through Black Sea ports and this could become a problem. For now, though, the world feels that the Wheat is there and people will not go hungry due to increased production estimates released by USDA on Monday. Russia has threatened to cut off exports from Ukraine unless it can have more exports, too. Russia now appears to be losing the war and could do something rash to try to hold things together. The demand for US Wheat still needs to show up and right now there is no demand news to help support futures. Europe is too hot and dry and the US central and southern Great Plains have also been too hot and dry. Dry weather is affecting Indian production as well.

Weekly Chicago Soft Red Winter Wheat Futures

Weekly Chicago Hard Red Winter Wheat Futures

Weekly Minneapolis Hard Red Spring Wheat Futures

Corn: Corn closed a little lower last week as demand ideas were weak and as USDA caught up with weekly export sales reports. The Corn sales were not exciting to anyone. USDA cut production about as expected in its reports released last Monday but cut demand even more for a higher than expected ending stocks estimate. The report was considered neutral by the trade, but the demand side will need to be watched as Corn demand needs to hold to keep lower ending stocks estimates in play. There are reports of less cattle and that means domestic demand could be hurt. Ethanol demand ideas took a hit last week although Crude Oil moved higher. There are also increasing concerns about demand with the Chinese economic problems caused by the lockdowns creating the possibility of less demand as South America has much better crops this year to compete with the US for sales. Ending stocks estimates could be very tight for the coming year if the crop projections hold true. Basis levels in the Midwest are strong amid light farm selling. It is still very hot and dry in parts of China and there is increasing concern about Corn production there this year. It has also been very hot and dry in Europe. Oats also closed higher.

Weekly Corn Futures

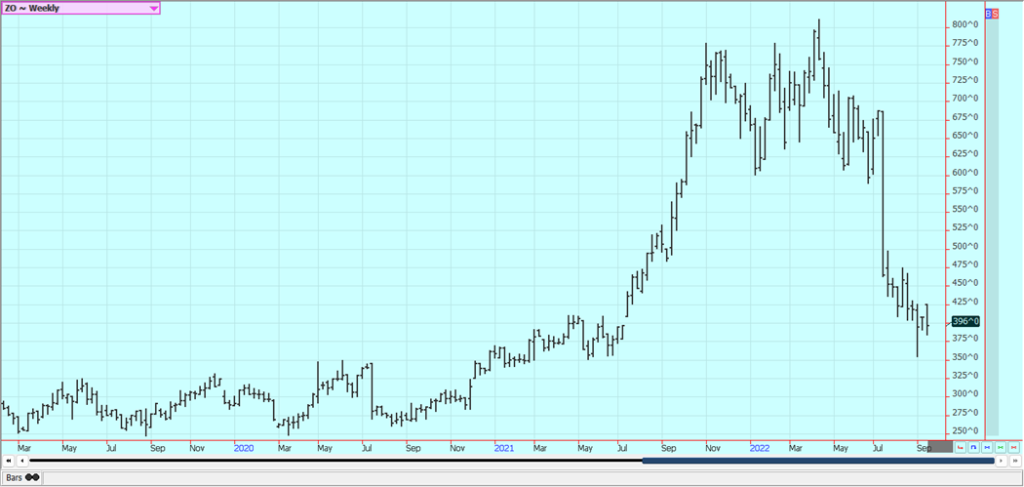

Weekly Oats Futures

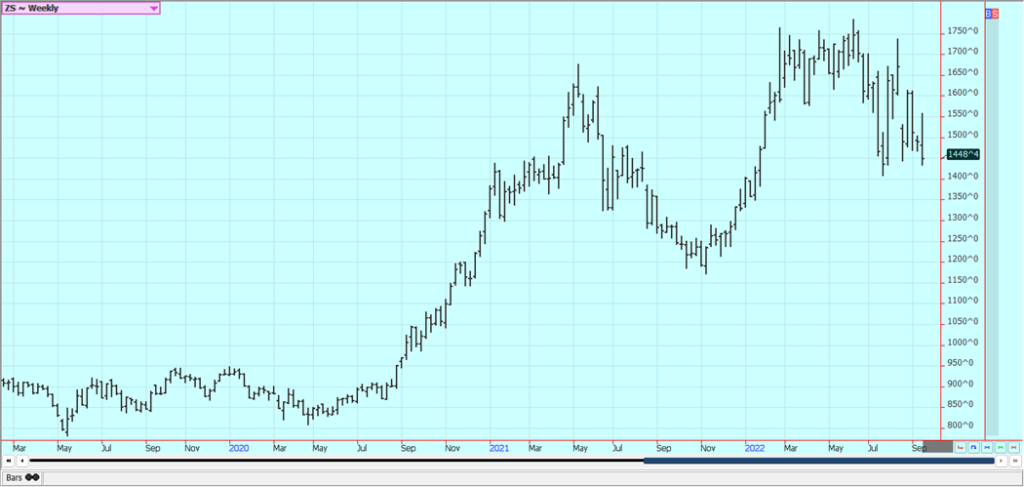

Soybeans and Soybean Meal: Soybeans and the products were higher last week on the back of bullish USDA production and supply and demand estimates and as the weekly export sales reports showed strong new crop sales but as the US Dollar moved higher. USDA on Monday showed less yield and planted and harvested area than trade expectations and estimated production much less than the trade had expected. Demand was cut back some, but the overall effect of the estimates was ending stocks at just 200 million bushels for the coming year instead of 240 as estimated by the trade. Demand remains an issue for the market to contend with. The trade is worried about demand due to a lack of Chinese interest caused by the Covid lockdowns there and in part by the stronger US Dollar. Brazil is still offering and that South America as a whole are expected to produce a very big crop later this year for harvest next Spring. US production ideas remain strong after mostly good weather in August. Basis levels are still strong in the Midwest. There are still renewed Chinese lockdowns and there are fears that China has been importing less as a result.

Weekly Chicago Soybeans Futures:

Weekly Chicago Soybean Meal Futures

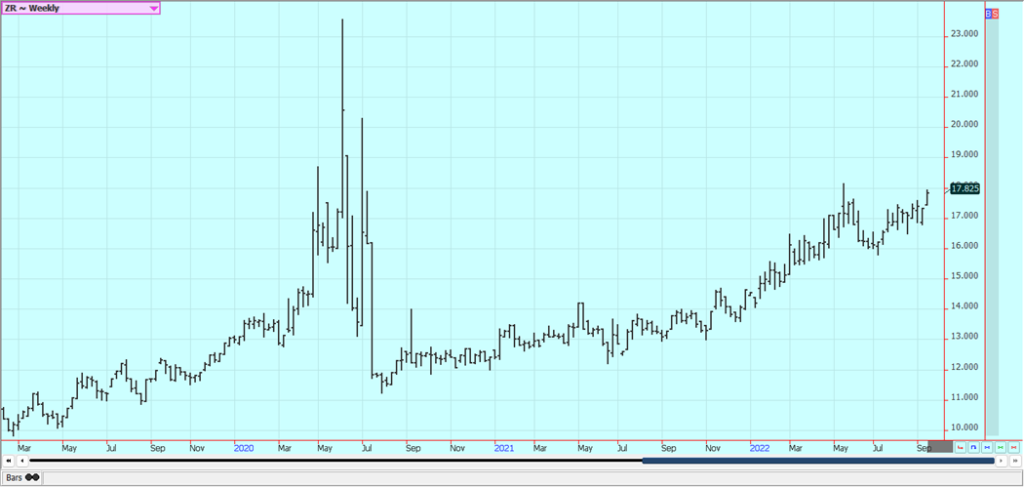

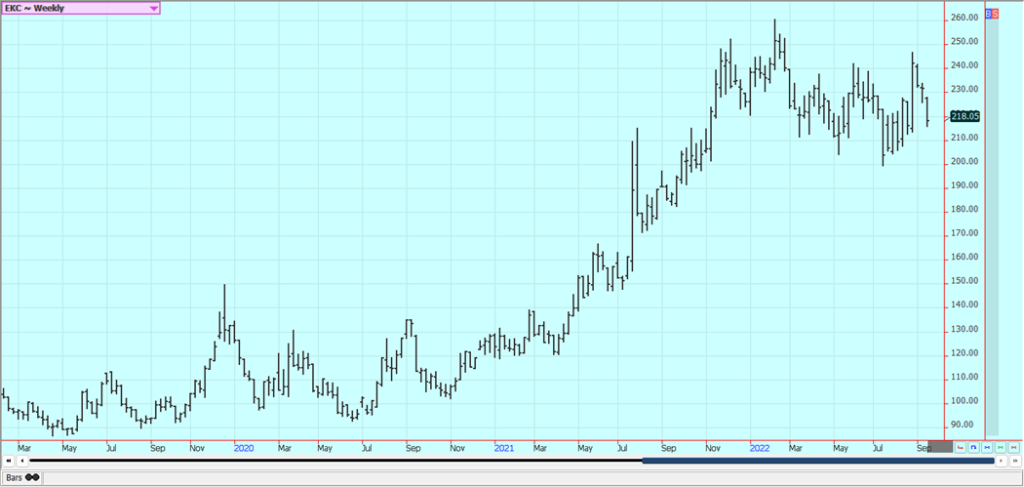

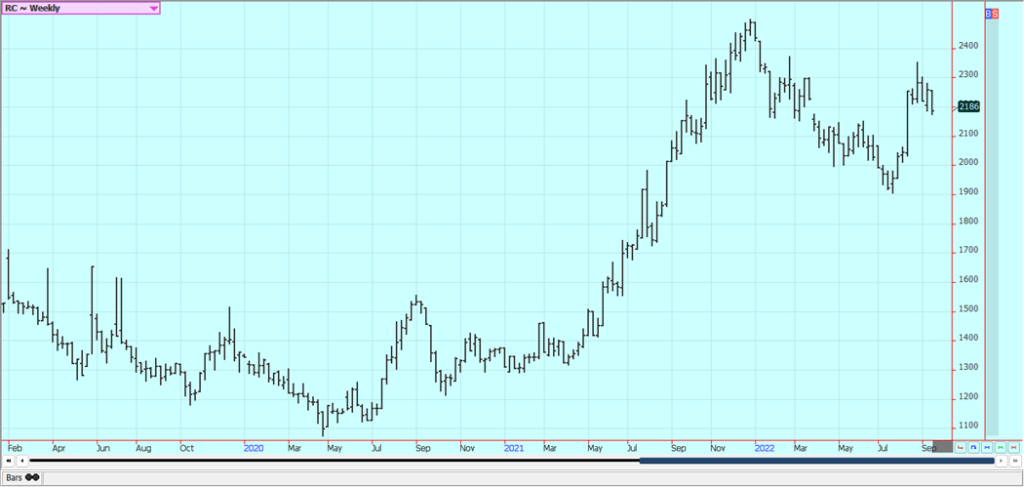

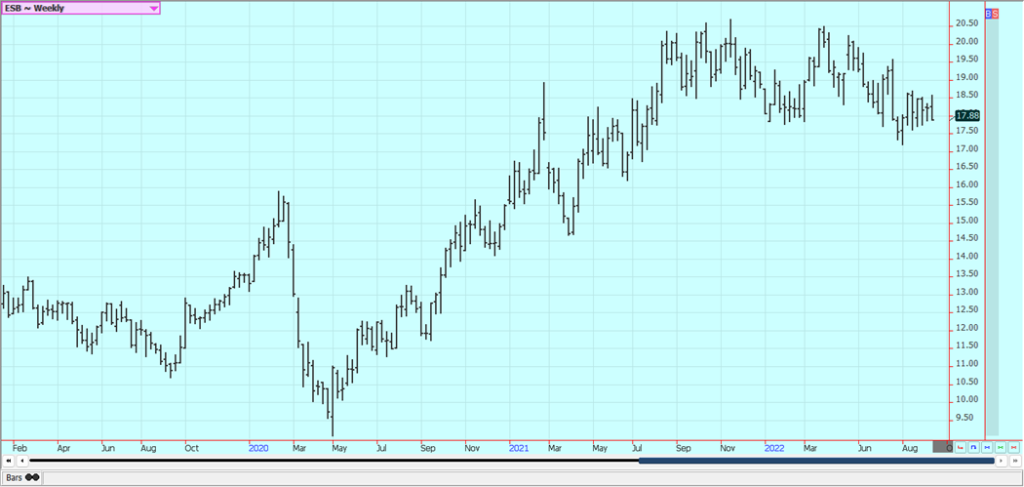

Rice: Rice was a little higher last week but could not make new weekly highs. Futures closed just below those levels on Friday. The USDA reports showed smaller production and ending stocks estimates. Demand for Rough Rice was cut hard, but demand for Milled Rice held together in the latest estimates. News that India will restrict exports of some grades of Rice also supported futures. Brokens cannot be exported and export taxes on White and Brown Rice are now 20%. Parboiled and Basmati exports are permitted with no restrictions or additional costs. Wire reports suggest that Indian Rice exports could be cut by 25% to 50% by the moves. The move follows a drought that hurt Rice production and the government is apparently afraid of a lot of food inflation hitting the people. Any move by India to restrict exports can be bullish as India is far and away the cheapest seller of Rice in the world market. The US harvest is moving along to completion and yield reports have been variable as have been quality reports. Some producers are getting done with harvesting in Texas as well as in southern Louisiana. Yield reports have been generally good in Louisiana and quality reports are generally good. Yield and quality have been up and down in Texas. Crop conditions are mostly good to excellent for now in Arkansas and Mississippi.

Weekly Chicago Rice Futures

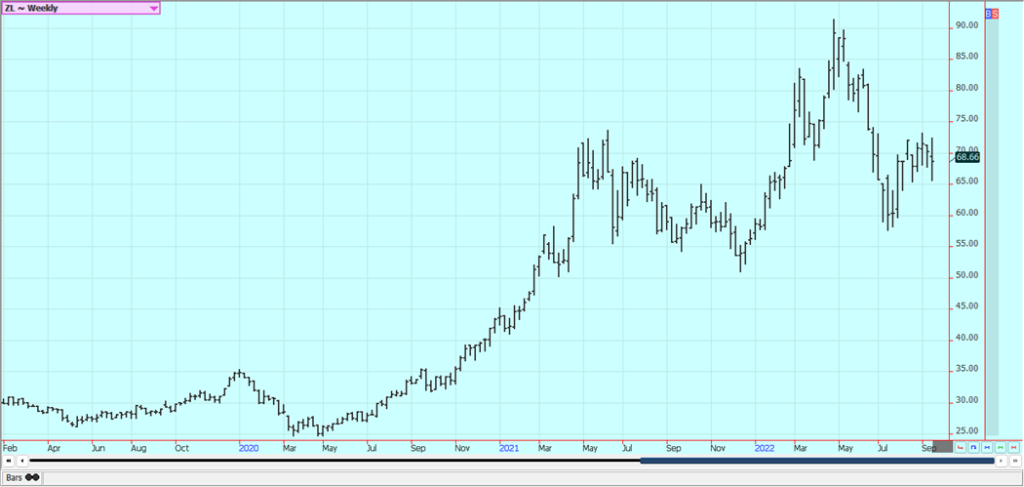

Palm Oil and Vegetable Oils: Palm Oil was a little higher last week as demand was stronger than expected. There are still ideas of bigger production and less demand, but SGS reported a big increase in demand in its reports released earlier in the week. Ideas are that supply and demand will be strong, but demand ideas are now weakening and the market will continue to look to the private data for clues on demand and the direction of the futures market. Canola was higher last week on the price action in Chicago and as the Canola harvest approaches. The Canola growing conditions are much improved and production estimates are higher for the year. The market is still short of Canola in the near term due to the reduced production of last year.

Weekly Malaysian Palm Oil Futures

Weekly Chicago Soybean Oil Futures

Weekly Canola Futures:

Cotton: Cotton closed lower on Friday and for the week. Price trends turned down on Friday when futures broke through some short-term support areas. Traders are worried about a global recession and demand in that recession. USDA showed good but not great sales over the last few weeks when the data was finally updated on Thursday. The late-season weather in the Great Plains was better and the crop showed improvement. An increase in export volumes was noted by USDA because of the increased production, but the supply increase was bigger than the demand increase, and ending stocks estimates increased. The harvest is coming and the market is preparing for it with sideways to lower prices. The trade is still worried about demand moving forward due to recession fears and Chinese lockdowns but is also worried about total US production potential. The Chinese quarantine is one week now instead of one month as before. It is possible that the continued Chinese lockdowns will continue to hurt demand for imported Cotton for that country and that a weaker economy in the west will hurt demand from the rest of the world.

Weekly US Cotton Futures

Frozen Concentrated Orange Juice and Citrus: FCOJ was lower last week but the daily charts show that a rally is possible this week. USDA last Monday issued a lower production estimate for California oranges, but California oranges are mostly used for fresh consumption and not for juice. USDA increased the Florida production estimate to 41.1 million boxes, from 41.0 million last month. The weather remains generally good for production around the world for the next crop. Brazil has some rain and conditions are rated good. It has been dry recently in Sao Paulo but apparently not dry enough to affect the trees or fruit all that much. Weather conditions in Florida are rated mostly good for the crops with some showers and warm temperatures. It has been dry in Brazil but showers are expected to develop over the next couple of weeks. Mexican areas are showing mixed trends, with dry weather in some northern areas but better weather to the south. FCOJ inventories are now 39.8% less than a year ago.

Weekly FCOJ Futures

Coffee: New York and London were lower last week as the US Dollar worked higher and offers in the cash market increased. Better offers in Arabica are reported from Brazil. Robusta shipments were down sharply and overall Coffee exports were less. There is concern that Brazil will produce less Coffee this year due to very dry conditions after early rains led to premature flowering. The forecasts call for some light and isolated to scattered showers in the region for this weekend. Vietnam has also been dry and wire reports from there indicate that production losses are likely. Demand for Coffee overall is thought to be less but the cash market remains strong. There is less Coffee on offer from origin, with Brazil offering less and Central America and Vietnam offering less as well. The weather in Brazil is good for Coffee production and any harvest activities. Temperatures are mostly above normal in Brazil and conditions are mostly dry. The dry weather is raising some concerns about the next crop potential but it is normally dry at this time of year.

Weekly New York Arabica Coffee Futures

Weekly London Robusta Coffee Futures

Sugar: New York and London were lower last week and the London market had a reversal down on the weekly charts. Reports from UNICA indicated increased cane processing and increased Sugar in the production mix at the expense of Ethanol. The New York market is worried that the lack of clarity about ethanol demand in Brazil will force mills down there to continue to produce more Sugar for export. The Brazilian president has lowered the fuel taxes in Brazil and this is squeezing the profit margins of the mills. The mills could produce much more Sugar over time due to the tax changes. The London market had been looking for increased White Sugar supplies from origin and now is more worried about demand after recent price strength. Indian exporters are waiting for the government to announce its export policy for the coming year and are not selling White Sugar. The government is expected to announce a first tranche of 5.0 million tons for the export market in the next few days.

Weekly New York World Raw Sugar Futures

Weekly London White Sugar Futures

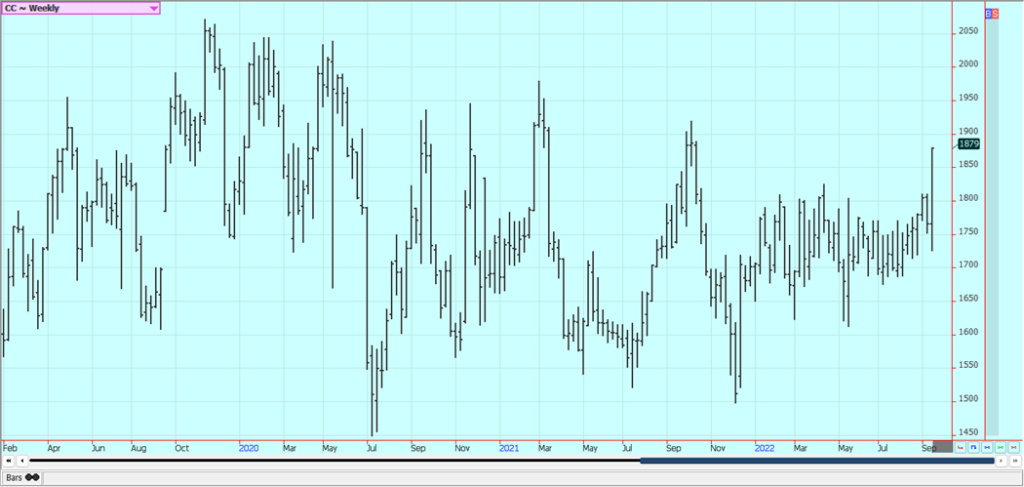

Cocoa: New York was a little lower and London was higher and turned trends up on the daily charts. Ideas of big production and uncertain demand are still around but reports from Africa indicate that demand has improved lately. Trends are mixed in New York. Reports indicate that buyers of Cocoa have enough coverage for now and can afford to wait for lower prices to develop. Supplies of Cocoa are as large as they will be now for the rest of the marketing year. Reports of scattered showers along with very good soil moisture from showers keep big production ideas alive in Ivory Coast. Ideas are still that good production is expected from West Africa for the year. The weather is good for harvest activities in West Africa but the harvest should be winding down now. The weather is good in Southeast Asia. Ivory Coast arrivals are now 59,000 tons, up 9.2% from last year.

Weekly New York Cocoa Futures

Weekly London Cocoa Futures

__

(Featured image by ThuyHaBich via Pixabay)

DISCLAIMER: This article was written by a third party contributor and does not reflect the opinion of Born2Invest, its management, staff or its associates. Please review our disclaimer for more information.

This article may include forward-looking statements. These forward-looking statements generally are identified by the words “believe,” “project,” “estimate,” “become,” “plan,” “will,” and similar expressions. These forward-looking statements involve known and unknown risks as well as uncertainties, including those discussed in the following cautionary statements and elsewhere in this article and on this site. Although the Company may believe that its expectations are based on reasonable assumptions, the actual results that the Company may achieve may differ materially from any forward-looking statements, which reflect the opinions of the management of the Company only as of the date hereof. Additionally, please make sure to read these important disclosures.

Futures and options trading involves substantial risk of loss and may not be suitable for everyone. The valuation of futures and options may fluctuate and as a result, clients may lose more than their original investment. In no event should the content of this website be construed as an express or implied promise, guarantee, or implication by or from The PRICE Futures Group, Inc. that you will profit or that losses can or will be limited whatsoever. Past performance is not indicative of future results. Information provided on this report is intended solely for informative purpose and is obtained from sources believed to be reliable. No guarantee of any kind is implied or possible where projections of future conditions are attempted. The leverage created by trading on margin can work against you as well as for you, and losses can exceed your entire investment. Before opening an account and trading, you should seek advice from your advisors as appropriate to ensure that you understand the risks and can withstand the losses.

The TopRanked.io Weekly Digest: What’s Hot in Affiliate Marketing [++ KuCoin Affiliate Program Review]

X now allows people to block certain topics from their feed. This week, we're going to tell you how to...

Hotel Stay Project Supports Wildlife Conservation in Japan

Iwate Prefecture launched a project linking hotel stays to conservation through Morioka Zoological Park Zoomo. A themed room at Yunomori...

Bitcoin Leads Modest Crypto Rebound Amid Mixed Signals

Bitcoin rose 2 percent to above 77000 as ETFs saw 15 million inflows and April gains of 12.2 percent. Ethereum...

Major Pharma Advances: EU Approvals, Vaccine Progress, and Breakthrough Clinical Results

Johnson & Johnson has EU approval for nipocalimab for generalized myasthenia gravis, showing superior control and sustained benefits. Sanofi reported...

Agential Cannabis 2026 to Drive APAC Market Growth and Global Industry Collaboration

Agential Cannabis 2026 will take place September 23–24 in Bangkok, bringing global experts together to advance the APAC medical cannabis...

|

|

|  |

|

|

-

Cannabis1 week ago

Cannabis1 week agoCannabis Stocks Show Signs of Rebound as Policy Shift Sparks Optimism

-

Crowdfunding4 days ago

Crowdfunding4 days agoItaly Extends SME Guarantee Fund to Crowdfunding with New 2026 Framework

-

Markets2 weeks ago

Markets2 weeks agoMarkets Rally Amid Uncertainty and a Widening K-Shaped Economy

-

Crypto1 day ago

Crypto1 day agoBitcoin Leads Modest Crypto Rebound Amid Mixed Signals