Business

Do rising Canadian and Australian real estate prices point to a bubble?

Canadian home prices are now 84% higher than in the U.S. Despite Canadian’s slightly lower incomes. And the Aussies’ are even higher. Home prices in Australia are now 107% higher than those in the U.S.

I’ve been seeing a lot in the news lately about Canadian and Australian real estate prices.

Most of what we’re hearing is that there’s little to worry about with our neighbor’s real estate prices shooting to the moon.

There is something to worry about. Something BIG.

Between early 2006 and late 2012, real estate in the U.S. took a whipping worse than what the Great Depression dished out. It lost 34% compared to the 26% it shed back in the early 1930s.

But property prices in Canada and Australia hardly paused, and then they continued their march higher.

Canadian home prices are now 84% higher than in the U.S.

Despite Canadian’s slightly lower incomes.

And the Aussies’ are even higher. Home prices in Australia are now 107% higher than those in the U.S.

It’s terrifying. Stephen King should turn it into one of his horror stories. It’d be a best-seller.

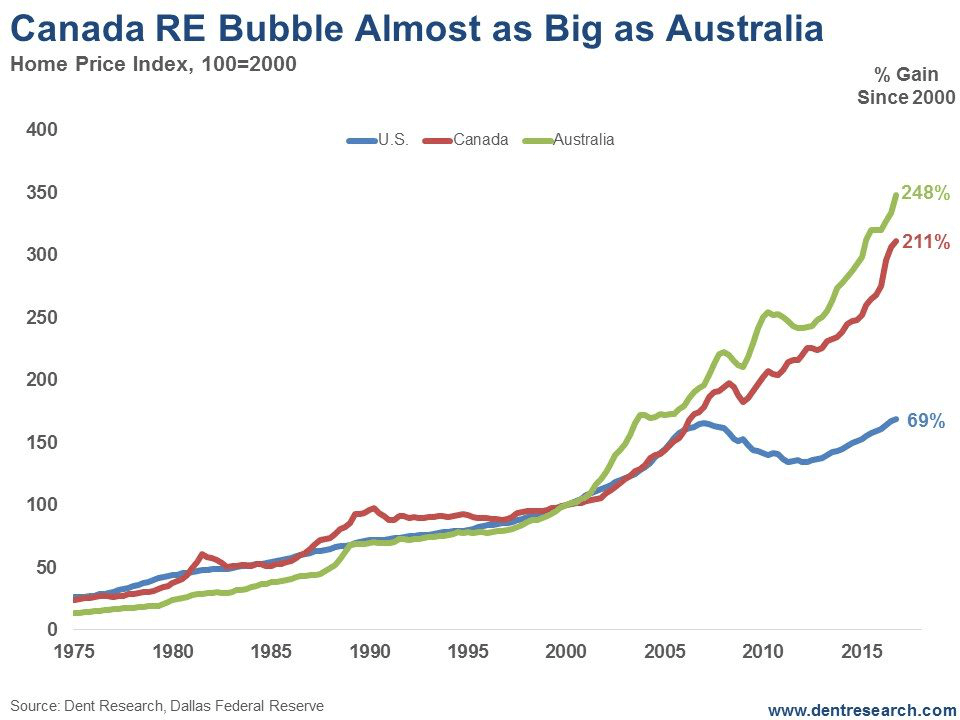

Look at this chart:

(Source)

You can see how the trends in prices correlated closely for three decades, since 1975. But from early 2006 forward, the U.S. diverged, trending downward while all other English-speaking countries – including New Zealand, Great Britain, Singapore, and Hong Kong – seemed to dust themselves off and continue on.

Turns out, that was a blessing in disguise for U.S. property owners. It means that in the next larger and more global real estate crash, we’ll suffer less than our counterparts.

Both Canada and Australia’s real estate prices went exponential again after 2012. And to me, that suggests we’re in the final “orgasm” phase of these bubbles.

During my last speaking tour of Australia in late May, mainstream economists were finally admitting their country had a bubble. Now I’m seeing more and more articles about a bubble in Canada, with surging consumer debt.

It’s fuel on the bonfires.

Tread carefully here, readers. There’s trouble ahead…

What my bubble model warns

Since 1975, the gains in Australian real estate values have been 25.5 times, while in Canada they’ve been 11.9 times, and 5.5 times in the U.S.

But the most important point, for me, is early 2000. That’s what I’ve identified as the real estate bubble origin. Gains since then have been 248%, 211%, and 69%, respectively.

My real estate bubble model calls for a fall 85% of the way back to that bubble origin, on average. That would imply a downside risk of 61% in Australia, 50% in Canada, and 35% in the U.S.

However, because of Australia’s stronger demographic trends, I don’t think its real estate market will suffer such an extreme loss. I suspect it’ll lose closer to 50%, but that’s still a kick to the gonads.

The worst-case scenario would see Australian real estate shed as much as 71%, while Canadian property lost 68%, and U.S. prices declined 41%.

All bubbles ultimately succumb to their own extremes. U.S. real estate burst earlier because of our subprime crisis, a problem not experienced in Canada and Australia. But, as home prices head into the stratosphere, fewer people can afford them, and eventually, it all comes crashing down.

The median price-to-income ratios are highest in Australia, at 7.0. In Canada, they’re 4.7. In the U.S., they’re 3.9 (which is modest, but still high). This means Australians must fork over seven times their income to buy a house.

As an aside, median price-to-income ratios are 18.0 in Hong Kong, 13.0 in China, 10.0 in New Zealand, and 4.2 in the U.K. (although London is higher).

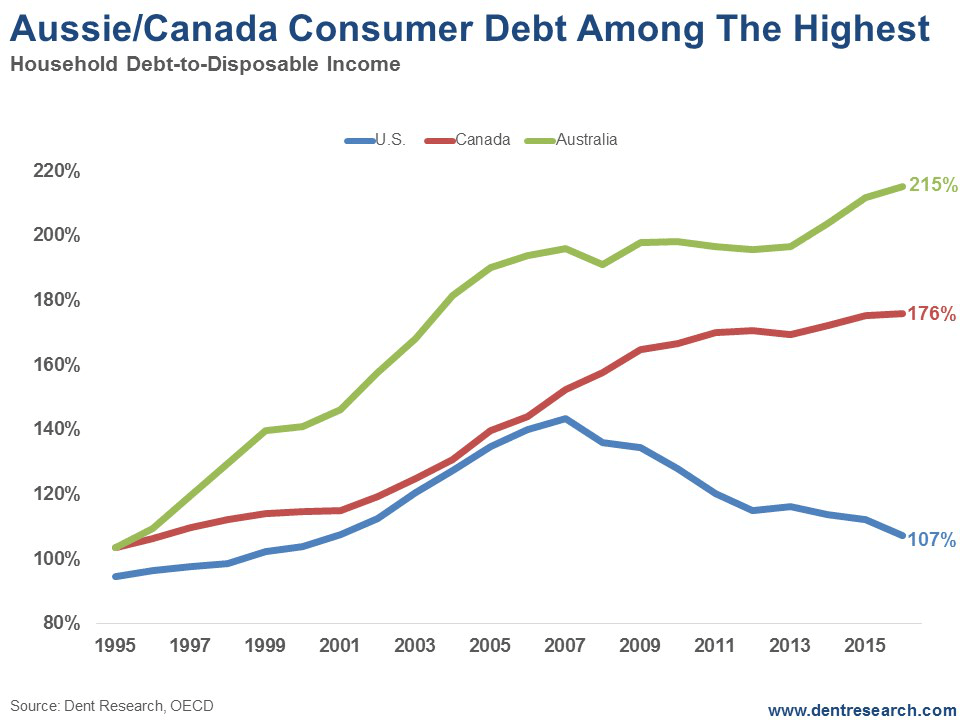

So, the rubber hits the road when it comes to consumer debt burdens, which are heavily weighted with mortgages.

That’s what will put a limit on this bubble, and it’ll happen sooner rather than later. Just look at debt ratios in these three countries.

(Source)

Since 1995, just before the stock and real estate bubbles, consumer debt to disposable income ratios (after tax) have risen a crushing 215% in Australia (3.15 times), 176% in Canada, and, after our first crash, 107% in the U.S.

It’s time for a debt deleveraging.

And that goes for businesses and their commercial real estate even more because it almost always gets hit harder than residential property.

It may well be that the Canada bubble bursting triggers ours this time around. But Australia is the wild card due to the intensive foreign Chinese buying there.

Don’t believe these bubbles won’t burst. Instead, be prepared.

For the last few weeks, we’ve highlighted the prevalence of fake financial news. I include in this the stories we’re hearing about Canadian and Australian real estate.

When property prices roll over, the asset becomes illiquid amazingly fast.

—

DISCLAIMER: This article expresses my own ideas and opinions. Any information I have shared are from sources that I believe to be reliable and accurate. I did not receive any financial compensation in writing this post, nor do I own any shares in any company I’ve mentioned. I encourage any reader to do their own diligent research first before making any investment decisions.

Temotiva Launches Crowdfunding Campaign to Advance Preventive Mental Health

Temotiva Innovación Lab has launched a crowdfunding campaign through Santander X Explorer, marking a new phase for the University of...

Fed Policy Shift Raises Concerns Over Debt and Inflation Risks

The Federal Reserve is criticized for resuming balance sheet expansion through Treasury purchases despite expectations of tighter policy under new...

AI Adoption in Italian Retail Stalls Despite Strong Experimentation

A survey on AI in Italian large-scale retail trade shows companies are increasingly adopting artificial intelligence, but only 1.4% have...

Crypto Market Stays Stable as Bitcoin and Ethereum See Mild Declines

The crypto market remained stable despite slight declines in major coins like Bitcoin and Ethereum. Bitcoin held near $64,362, while...

WNBA Removes Cannabis From Banned Substances List in New CBA

WNBA removed cannabis from its banned substances list in a new CBA running 2026–2032, aligning with NBA policy and allowing...

|

|

|  |

|

|

-

Crypto6 days ago

Crypto6 days agoBitcoin Rises on Iran Deal as Crypto Markets React to AI and SpaceX News

-

Crowdfunding2 weeks ago

Crowdfunding2 weeks agoHistoric KiHa 2101 Railcar Restored in Japan Through Community Effort

-

Biotech3 days ago

Biotech3 days agoBavarian Biotech Sector Expands with Record Funding and Startup Growth in 2025

-

Impact Investing1 week ago

Impact Investing1 week agoEU Approves €23B Italian Renewable Energy Plan to Boost Climate Goals

You must be logged in to post a comment Login