Business

US could ship new soybeans to China by mid-January after Trump-Xi truce

Soybeans and soybean products are expected to rally sharply this week after the United States and China reached a truce on tariffs over the weekend.

Wheat

Wheat was higher on Friday and higher for the week in both Chicago Winter Wheat markets, while Minneapolis Spring Wheat closed higher. Ideas are that demand for US Wheat is about to improve, and the weekly charts show that more buying is possible in the next few weeks.

Meanwhile, planting of the Winter Wheat crops in the US has been delayed due to bad weather. Too much rain and too much cold weather has made getting the crop in and established timely very difficult. World crop reports continue to indicate less production and tightening supplies. Firm prices extend from Russia to Australia on reduced world production, although Russia showed the potential for strong exports this year.

It remains very dry in Australia, although some eastern areas have seen some rain and conditions are called generally good in the west. It is reported to be wet and cold in Siberia for the Spring Wheat harvest there, and planting conditions are reported to be dry near the Black Sea. The Spring Wheat harvest in Siberia has been delayed due to snow storms.

Weekly Chicago Soft Red Winter Wheat Futures © Jack Scoville

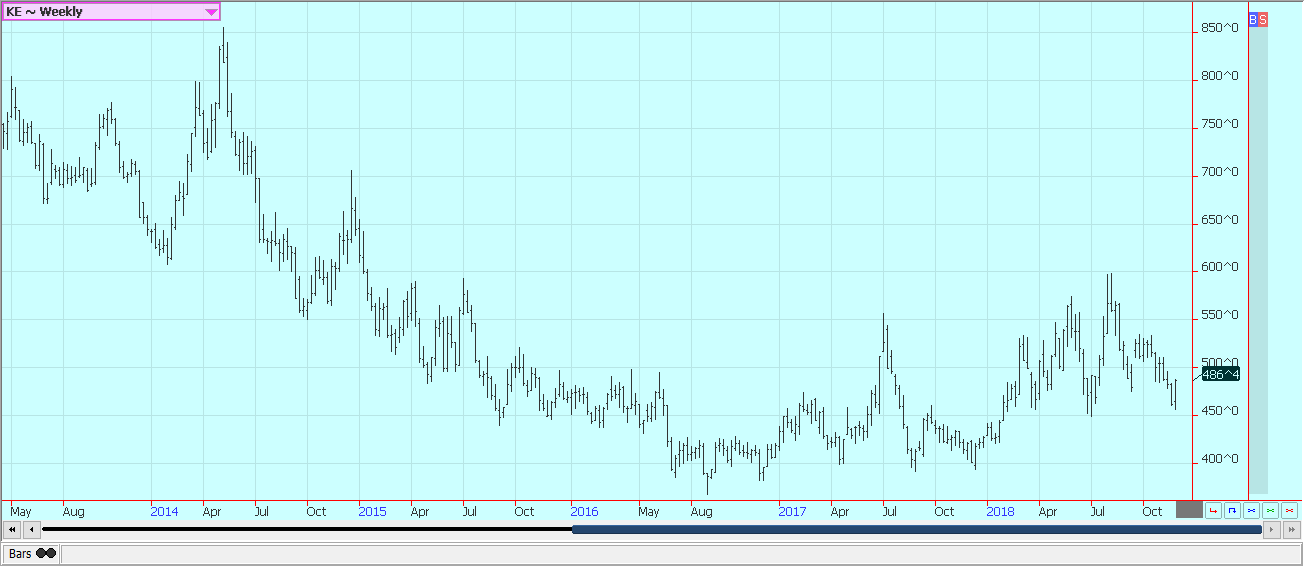

Weekly Chicago Hard Red Winter Wheat Futures © Jack Scoville

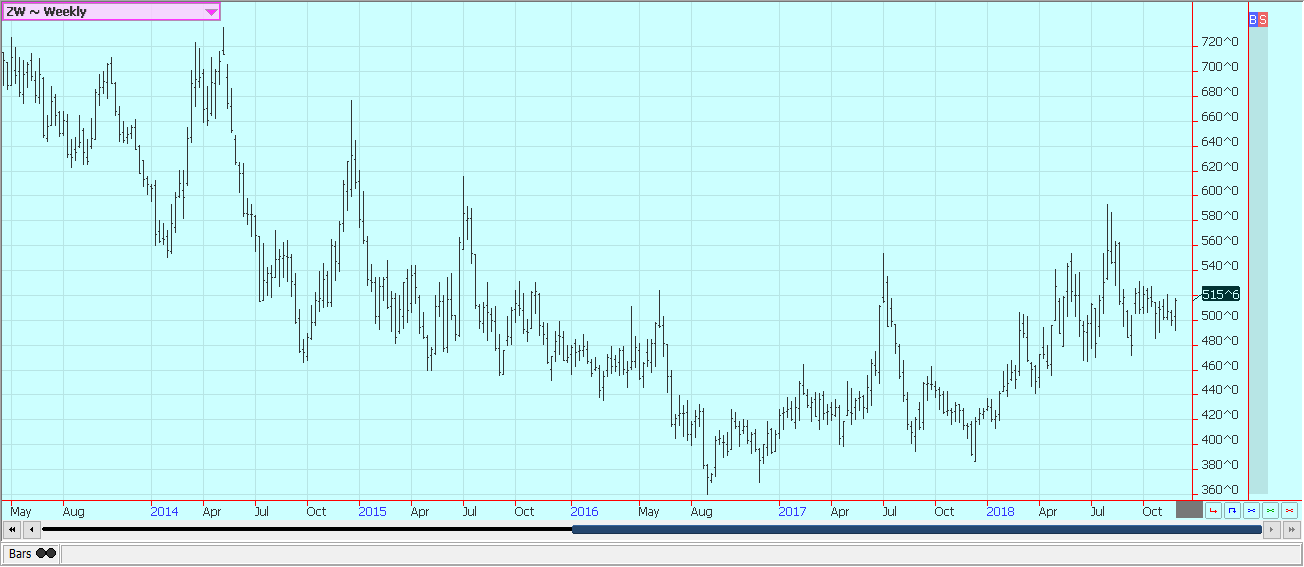

Weekly Minneapolis Hard Red Spring Wheat Futures © Jack Scoville

Corn

Corn was higher on Friday and for the week and trends are mixed on both the daily and weekly charts. Export demand as noted in the USDA weekly sales reports was above expectations and represented a strong week. The market has been worried about ethanol demand, but crude oil and products prices might be washing out and could start to show a recovery. Crude Oil futures have been in a free fall since the beginning of October.

The weather in the Midwest was not very good for harvesting over the weekend. The temperatures finally moderated from some extreme cold levels for this time of year, but precipitation was noted, including some snow for Iowa and Nebraska that extended into parts of Minnesota, Wisconsin, and Michigan. Big rains were noted to the south of the snow. Cold, but quiet conditions are expected for much of this week.

Planting progress in southern Brazil is reported to be ahead of the normal pace. Argentine planting progress is in line with its average pace. The Brazil Corn will most likely stay in the country as the short crops last year led to shortages and imports. Brazil could still be forced to import more Corn from Argentina in the near term as well. Brazil is not expected to be a player in Corn in the world market until the Winter crop becomes available in the middle of next year.

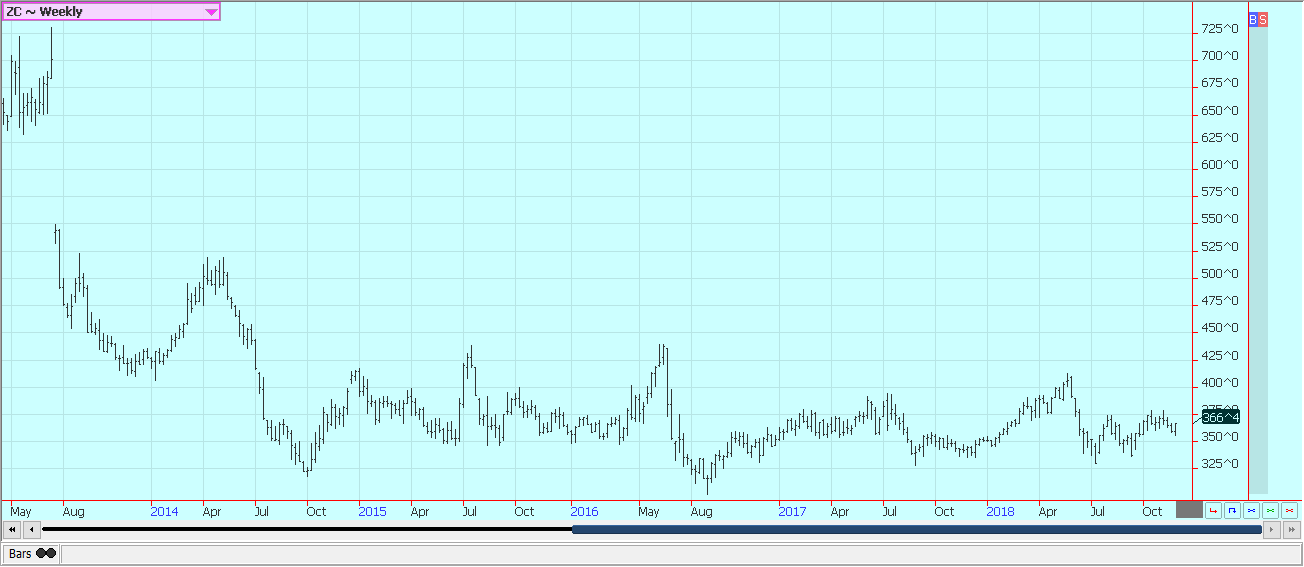

Weekly Corn Futures © Jack Scoville

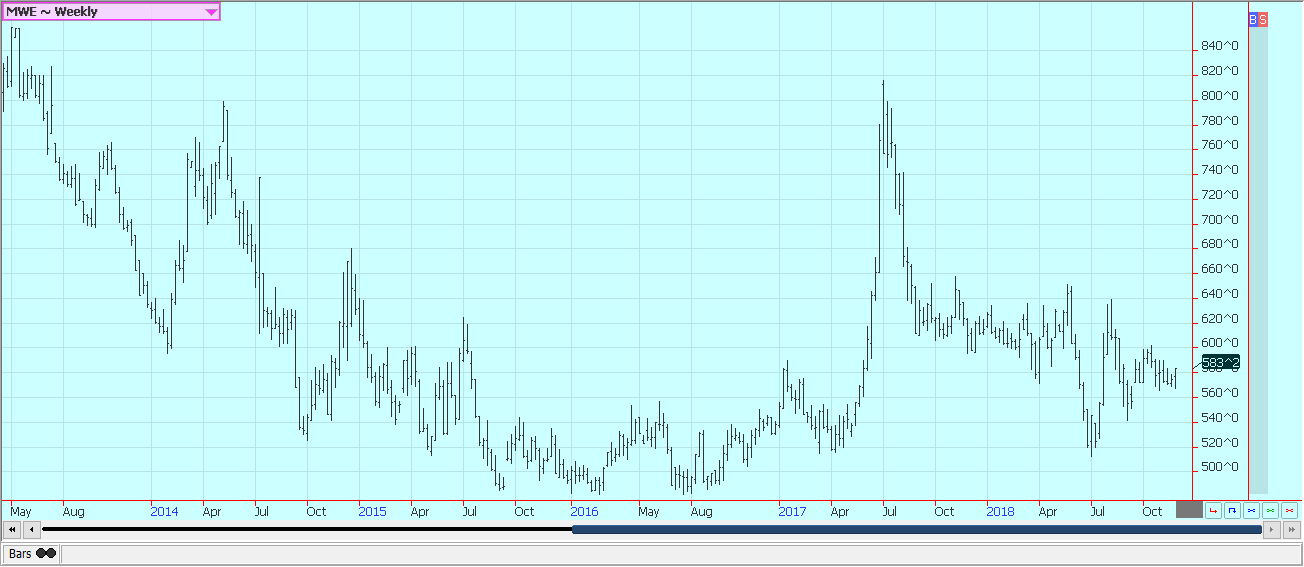

Weekly Oats Futures © Jack Scoville

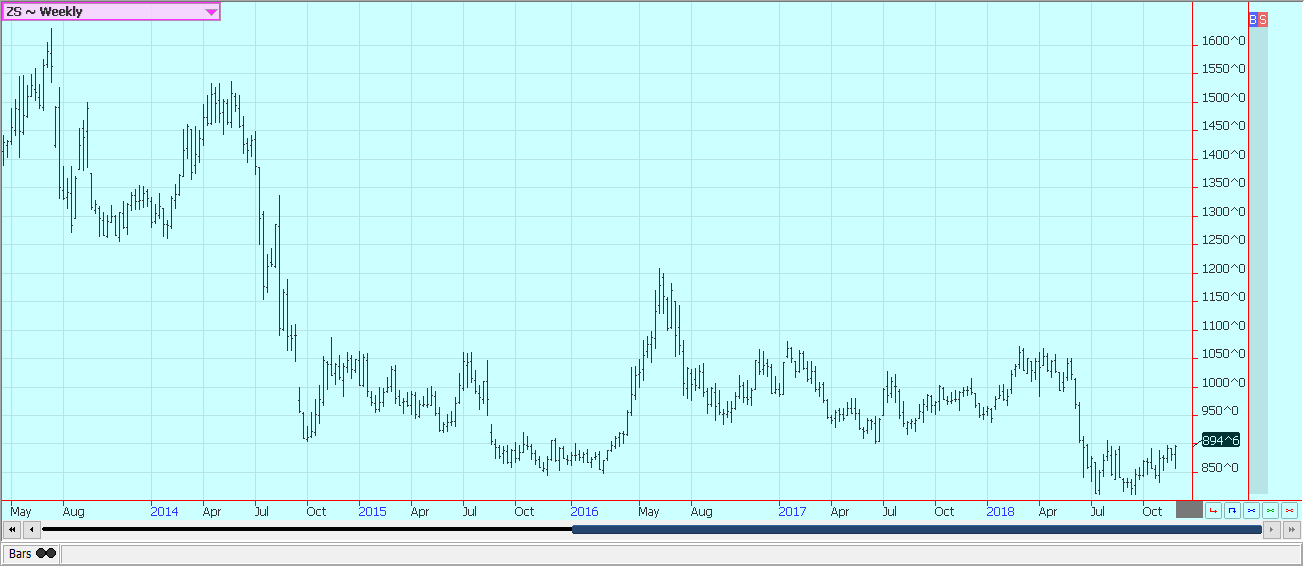

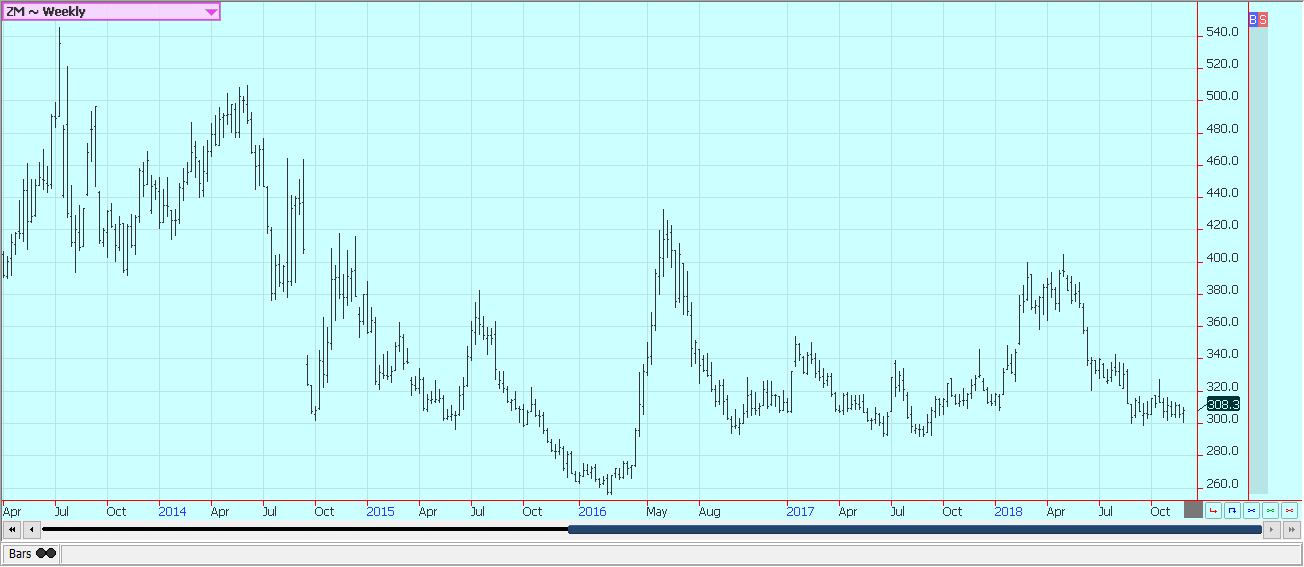

Soybeans and soybean meal

Soybeans and products were a little higher last week, and could rally sharply this week. The market has been held hostage by the tariff wars between the US and China. A truce between the two sides was made in Buenos Aires over the weekend. The US has agreed to keep the tariffs as they are in return for some Chinese buying in US ag markets and continued talks about opening up the Chinese markets and the rest of the disputed areas. China has refused to buy US Soybeans due to the trade disputes, and the US farmer has suffered, but now the market will look for business in the very short term.

The US had a huge crop this year as producers anticipated stronger prices and strong Chinese demand. Brazil has been planting and plans on bigger crops. Argentina is also planting, but most of the trade attention is on Brazil. Producers in southern areas are ahead of the normal pace for planting progress, and there are ideas that the country could start to ship new crop Soybeans to China by the middle of January, a full month or more ahead of normal.

Meanwhile, ending stocks projections for the US are very high and give little reason to expect a major rally anytime soon. Wet weather over the weekend in the Midwest and Great Plains kept any harvesting to a minimum. The weather this week should feature cold temperatures and drier conditions.

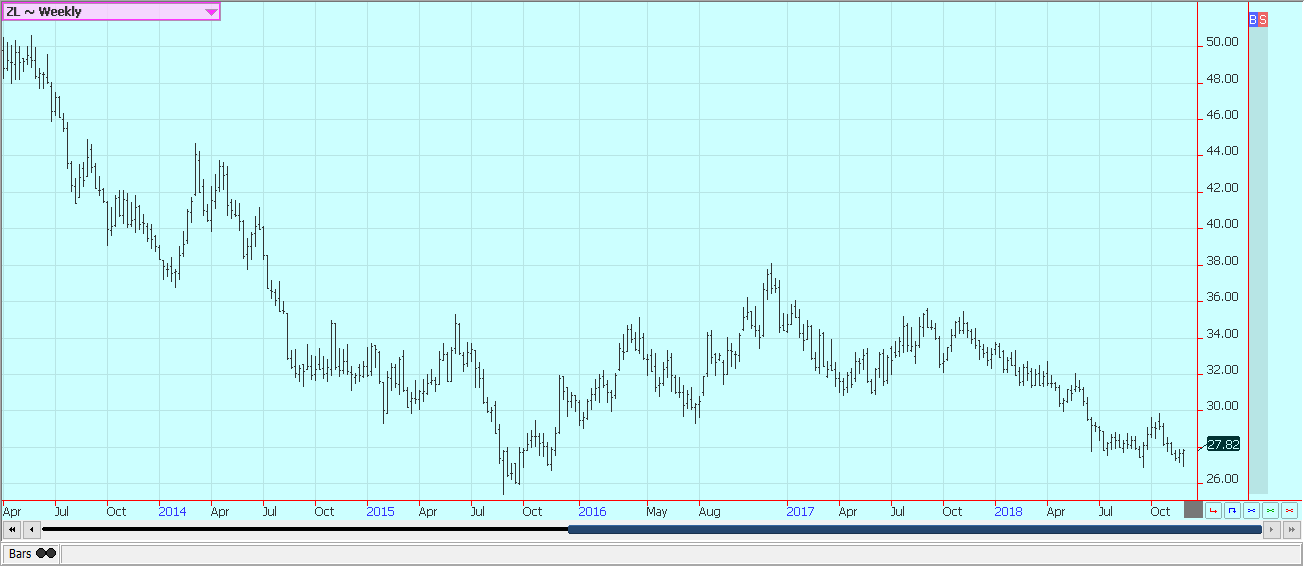

Weekly Chicago Soybeans Futures © Jack Scoville

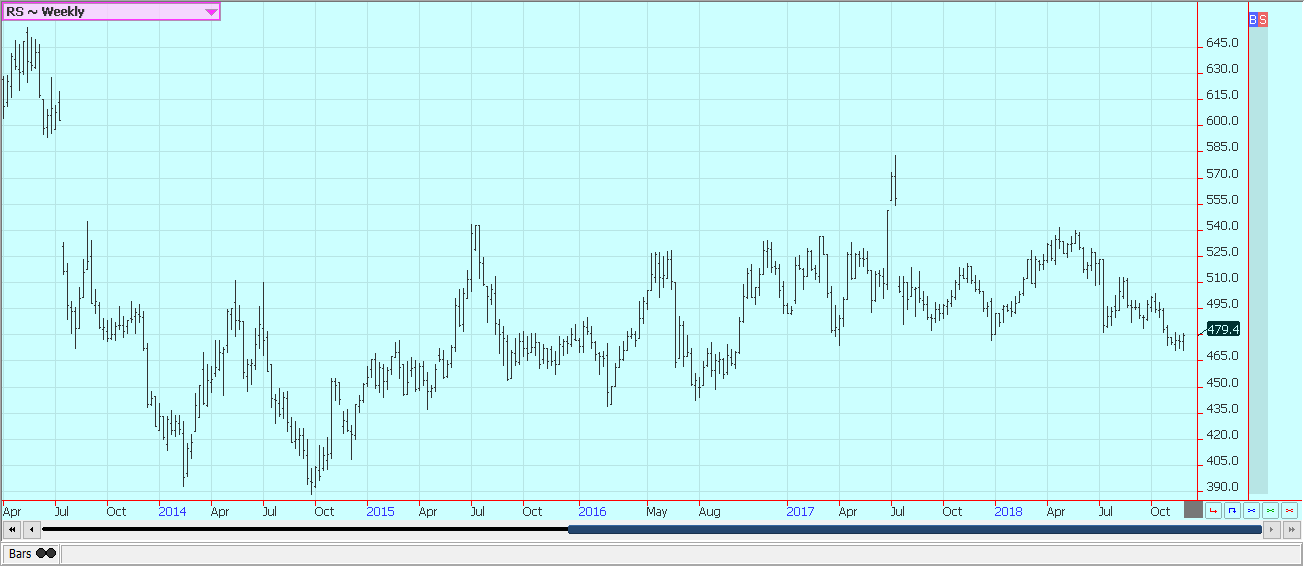

Weekly Chicago Soybean Meal Futures © Jack Scoville

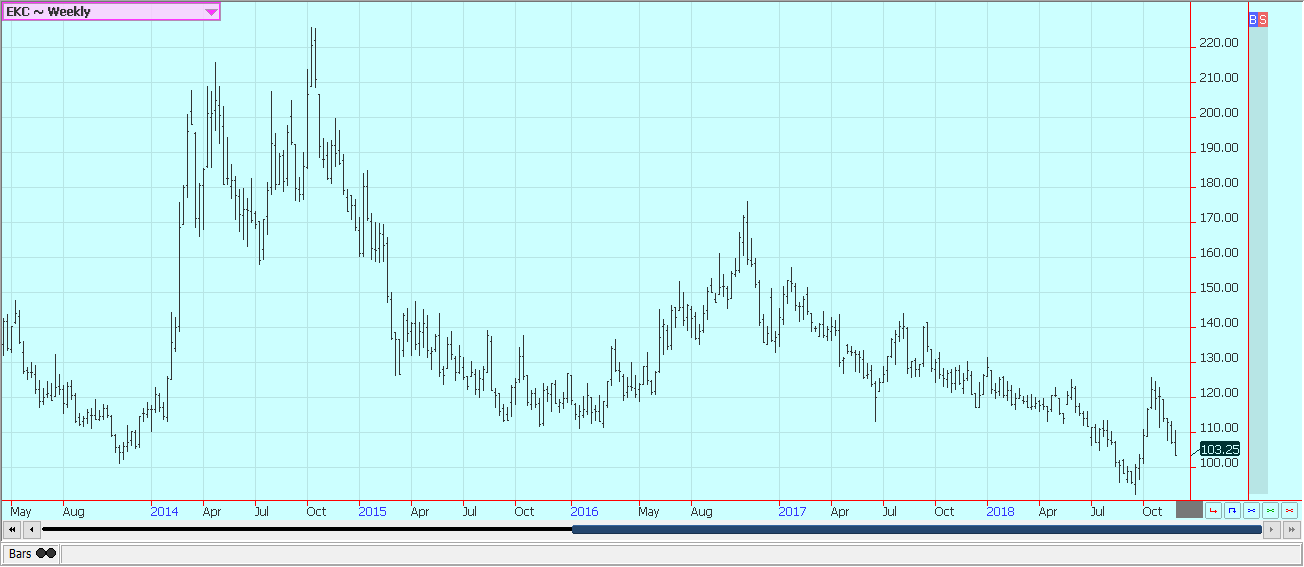

Rice

Rice was a little lower Friday after another slow session. Futures were a little higher for the week. The weekly export sales report was poor, but reflected the nature of the US market at this time. The futures market remains stuck in a trading range for now, but there will not be much selling interest unless prices rally, implying that mills and exporters will need to buy futures or pay up in the cash market if and when they need supplies.

Producers do not seem interested in further sales at this time. It is the holiday period, and this time is always a slow time for US Rice futures. Most producers would rather take part in holiday activities or go hunting rather than sell Rice, and the mills appear covered for now. The export demand is holding relatively strong. However, the exporters appear to be covered for now. It might take until after the first of the year to see much movement in Rice futures and cash markets. This is normal for the US Rice market.

Weekly Chicago Rice Futures © Jack Scoville

Palm oil and vegetable oils

World vegetable oils prices were generally higher last week on what appeared to be speculative short covering amid oversold chart patterns. The oversold nature of the market was especially true for Palm Oil. Demand remains below optimal levels in Palm Oil, and most in the market worried about finding enough demand to take up the increasing supplies. Production has been trending seasonally higher, but should start to fall soon as the weather will change and inhibit palm production. Daily charts show mixed trends and weekly charts show futures in a down trend.

Soybean Oil closed slightly higher in reaction to the strength in Palm Oil and despite weaker petroleum prices. Selling came late in the week as the petroleum markets are collapsing and causing bio fuels markets to move lower. Support is coming from less offer from South America. Canola was slightly lower on improved weather and as demand is only routine. The harvest is finally over. Farmers had a tough time getting into the fields due to rains, especially in the west, but finally wrapped up a week or so ago. Progress had been significantly behind normal, so the trade expects yield new losses. Yield reports are said to be below expectations.

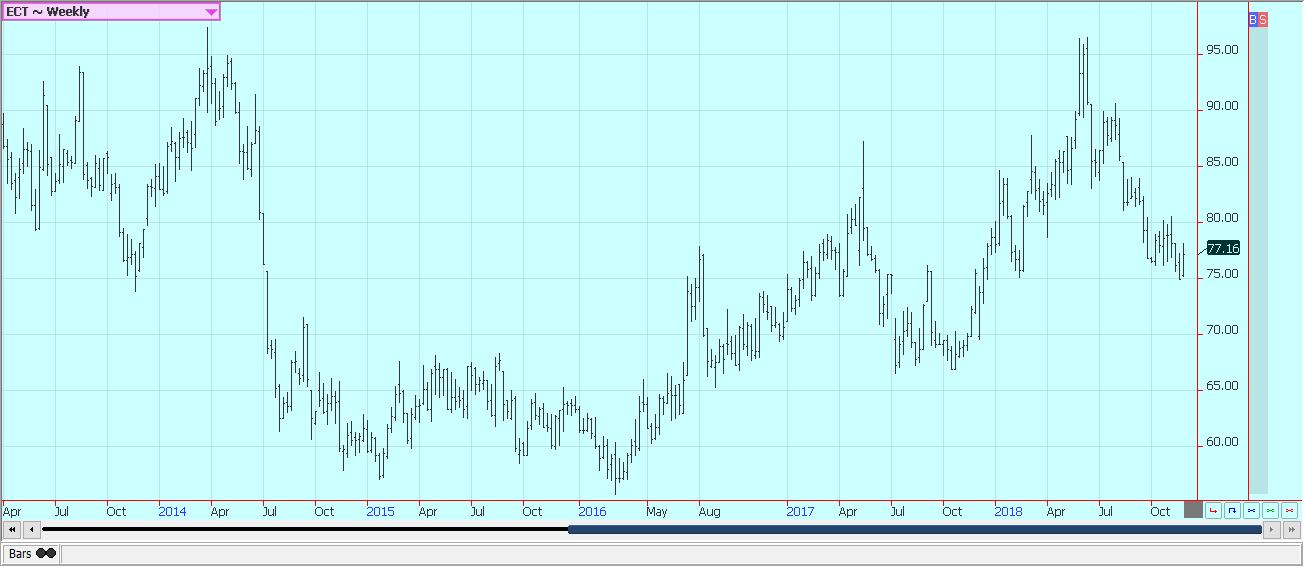

Weekly Malaysian Palm Oil Futures © Jack Scoville

Weekly Chicago Soybean Oil Futures © Jack Scoville

Weekly Canola Futures © Jack Scoville

Cotton

Cotton was higher last week. The market is likely to rally this week due to the truce in the tariff war between China and the US that was made over the weekend. Wire and anecdotal reports still suggest that the harvest pace is poor. Most of the delays have been in Texas due to too much rain, but some delays in the Southeast have also been reported. The delayed harvest could cause yield and quality losses. The market needs new demand.

Export sales for the last few weeks have been poor, and last week when sales were good. However, the better sales for one week were not enough to change attitudes about demand, and the weakness in petroleum futures meant that more poly products could be produced cheaper to compete with Cotton.

Weekly US Cotton Futures © Jack Scoville

Frozen concentrated orange juice and citrus

FCOJ was lower as cold, but not threatening weather, was reported in Florida. The weather has turned warmer and drier in the state, and an active harvest is likely. Some selling was noted on demand concerns and both the domestic and export market remain soft. The soft domestic market has been a feature for several years as more and more people look to pills or other ways to get Vitamin C.

The EU had been importing a lot of US FCOJ, but now all of that business is going to Brazil. It is still possible that a short term low has been made. The Florida FCOJ Movement and Pack report showed that inventories are now 16 percent above a year ago. That is a significant change, but less than the difference of a few months ago that ran well over 20 percent.

The Oranges harvest is active in Florida under good weather conditions. The fruit is abundant. Florida producers are seeing small sized to good sized fruit, and work in groves maintenance is active. Irrigation is being used in all areas. Packing houses are open to process fruit for the fresh market, and a couple of major processors are open in the state to take packing house eliminations.

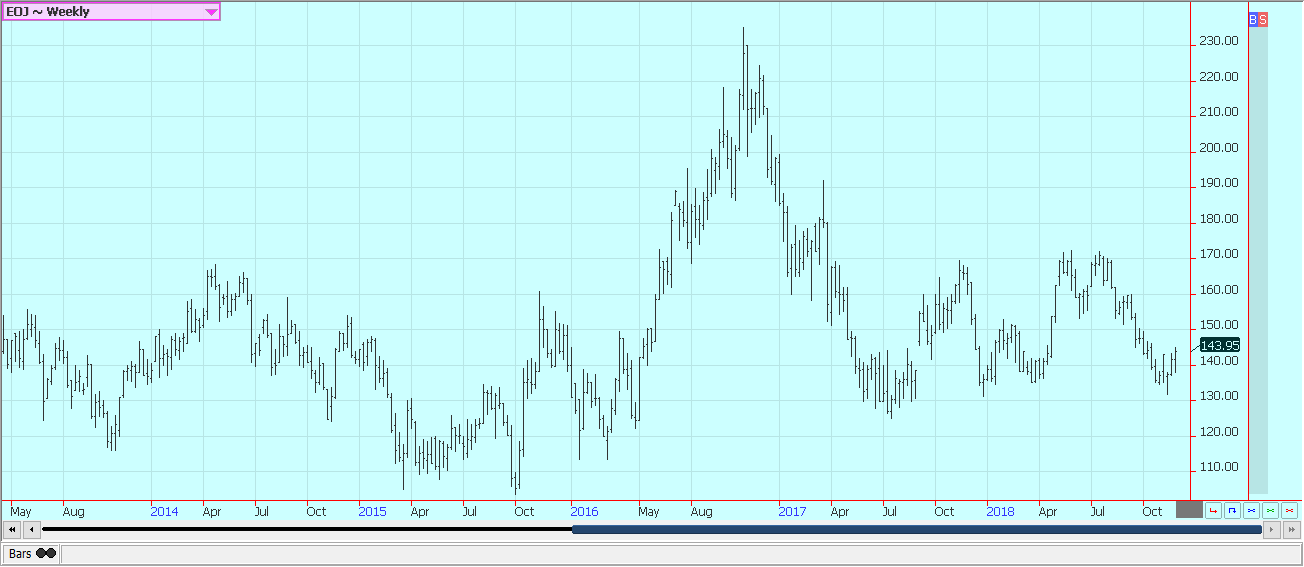

Weekly FCOJ Futures © Jack Scoville

Coffee

Futures were lower in New York and slightly higher in London last week. Currency relationships, and especially the rate between the US Dollar and the Brazilian Real, continue to be the driving force in Coffee trading, and weaker outside markets such as the extreme weakness in petroleum futures added to find selling interest on Friday. Commercials were said to be the best buyers.

The Brazil crops are getting harvested now, but are not always finding their way to the market due to the overall Real strength against the Dollar. Producers are also looking ahead to next year. El Nino remains in the forecast and Coffee areas in Brazil could be affected by drought. This is the off year for production there, anyway, and a drought would mean even less production.

Vietnam is getting close to its next harvest. Production in Vietnam is estimated at or above 30 million bags. Producers in both countries are not selling much. Some problems with too much rain have been noted in Central America. Drier conditions are wanted for harvesting, and mostly dry weather is in the forecast.

Weekly New York Arabica Coffee Futures © Jack Scoville

Weekly London Robusta Coffee Futures © Jack Scoville

Sugar

New York closed higher last week. London was higher as well. Sugar was supported by reduced selling in Brazil due to the stronger Real against the US Dollar. The Real has been gaining on the US Dollar and this has served to limit export interest in Brazil.

There are now doubts on just how much production will be seen this year in India. Wire reports indicate that pests have invaded Sugarcane fields and are eating and destroying the crop. There is no indication of losses yet, but the implication of the reports is that the losses could be significant.

Northwest India had been experiencing hot and dry weather that could cut yields. Dry conditions continue in Brazil, the EU, and Russia, but conditions are mostly good in Ukraine. Very good conditions are reported in Thailand. Brazil producers are worried about Cane production, and the market still talks about less production there this year. The dry weather in much of Europe and in southern Russia near the Black Sea has hurt Sugarbeets production potential in these areas.

Weekly New York World Raw Sugar Futures © Jack Scoville

Weekly London White Sugar Futures © Jack Scoville

Cocoa

Futures closed higher in New York and higher in London as the new main crop harvest comes to market in West Africa. Trends are still mostly down in both markets. The outlook for strong production in the coming year is still around, and ports are said to have plenty of Cocoa on offer.

The main crop harvest is in its earliest stages in some parts of West Africa. Main crop production ideas for Ivory Coast and Ghana are being reduced, with Ivory Coast now estimating its main crop production at 1.985 million tons, down from previous estimates just over 2.0 million tons. Conditions appear good in East Africa and Asia. Demand is said to be improving as offers from the new harvest start to increase.

Weekly New York Cocoa Futures © Jack Scoville

Weekly London Cocoa Futures © Jack Scoville

—

DISCLAIMER: This article expresses my own ideas and opinions. Any information I have shared are from sources that I believe to be reliable and accurate. I did not receive any financial compensation for writing this post, nor do I own any shares in any company I’ve mentioned. I encourage any reader to do their own diligent research first before making any investment decisions.

TopRanked.io Weekly Affiliate Digest: What’s Hot in Affiliate Marketing [1xBet Affiliate Program]

If you thought nobody liked cricket, then this week, we're proving you wrong. And by the time we're done, you'll...

Tether Seeks Big Four Audit to Boost USDT Transparency

Tether, issuer of USDT, plans a full audit by a Big Four firm to address transparency concerns over its $184...

H&M Advances Sustainability and Cuts Emissions by 2025

H&M Group reported that by 2025, 91% of materials were recycled or sustainably sourced, with recycled content reaching 32%. Emissions...

NHS Funds Breakthrough CAR-T Therapy Breyanzi for Lymphoma Treatment in Spain

Bristol Myers Squibb announced NHS funding for CAR-T therapy Breyanzi, enabling its use from April 1st in Spain for lymphoma...

Crypto Markets Volatile as Bitcoin Hovers, Solana Eyes AI Integration

Crypto markets remain volatile amid the Iran war, with Bitcoin near $70,000 and ETF inflows improving outlook. Ethereum faces declines...

|

|

|  |

|

|

-

Biotech2 weeks ago

Biotech2 weeks agoNovo Nordisk: Stable Growth and Defensive Biotech Stock for DACH Investors in 2026

-

Impact Investing2 days ago

Impact Investing2 days agoRidemovi Secures Financing to Drive European Expansion and Sustainable Mobility Growth

-

Impact Investing1 week ago

Impact Investing1 week agoAntarctica Warming Reshapes Global Atmospheric Circulation

-

Business5 days ago

Business5 days agoAnemic Labor Market and the End of Passive Money Flows

You must be logged in to post a comment Login