Business

US wheat markets edge lower on prospects of huge world production increase

USDA reports predicted an increase in wheat production that would boost supplies in the world market, putting the U.S. market under pressure.

Projections of an increased production of wheat put pressure on the market, but the only major exporter that could bring more supplies is Russia.

Wheat

US wheat markets were generally lower again last week but managed to find some buying interest late in the week as some shorts elected to cover their positions. The market is still under pressure from ideas that there will be plenty of Wheat available in the world market due to the big increase in production shown by USDA in its reports a couple of weeks ago. However, the US and many other exporter countries have less this year, with only Russia the major exporter with more.

Canada has suffered through conditions very much like the US, with hot and dry weather in western sections of the Prairies and some areas that were too wet in eastern sections. Australia also suffered from the hot and dry weather at key times in the growing cycle, although conditions have improved over the last month. Still, the country is facing a smaller crop at near 20 million tons than had been originally estimated. Europe has had some wet weather in northern areas as the crop tried to mature and there will be at least a big quality loss from this area.

US export demand is improving again as US prices are very competitive in the world market, and the recent trend to a weaker US Dollar has helped. Demand has been primarily for HRW and HRS, the higher protein wheats grown in the US. The real hot weather in the US has left, and the weather in the northern Great Plains has turned dryer to aid in harvest progress. The US futures markets have given back about all the gains seen due to the bad weather, but really have no reason to work lower unless the Dollar were to rally sharply or something. Futures could hold and try to rally in the short term.

Weekly Chicago Soft Red Winter Wheat Futures © Jack Scoville

Weekly Chicago Hard Red Winter Wheat Futures © Jack Scoville

Weekly Minneapolis Hard Red Spring Wheat Futures © Jack Scoville

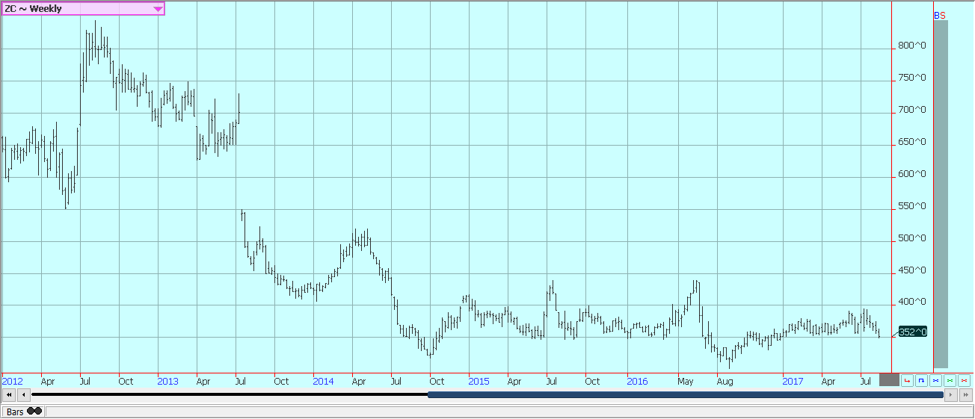

Corn

Corn and oats were lower last week as some rain and cooler temperatures moved through the Midwest. The rains missed the areas of Iowa and Illinois where it was needed the most. Variable growing conditions continue as pollination comes to an end and kernel fill continues. The USDA data will continue to affect the price for the next few weeks as private tour reports will start to be heard and as USDA will offer updated information next month with more data. However, the best data from USDA will not be seen until October.

The big event this week is the Farm Journal, formerly Pro Farmer Crop tour that kicks off today. Crop scouts should see highly variable conditions all week before a final estimate is released at the end of the week. Ideas are that variable conditions will force USDA to lower production estimates next month. There are still supplies from the previous crop to be sold by US producers, and ideas are that these supplies are big. A big offer despite weaker production will hurt any rally potential for prices.

Funds have been selling and are now thought to have established a short position. Near term price weakness is possible for the next couple of weeks as futures are now breaking down through some support areas on the weekly charts.

Weekly Corn Futures © Jack Scoville

Weekly Oats Futures © Jack Scoville

Soybeans and Soybean Meal

Soybeans and soybean meal were mixed last week on ideas of somewhat better rains for the crops in the Midwest. There was rain, but these rains hit areas already with plenty of moisture. The driest areas of Illinois and Iowa were missed. There is not a lot of rain in the forecast for this week for the Midwest, but temperatures should be moderate. The crop was planted late in many areas and is only starting to flower and set pods now.

The weather has been variable. Parts of Iowa and Missouri and central and southern Illinois have been dry and topsoil moisture levels are low. Crops in the east have been hurt where conditions have been too wet, and the plants are very small in Ohio and much of Indiana and into Michigan. Eastern Illinois showed some of the same features as other eastern states.

US Soybeans are flowering and setting pods. The crop progress is behind last year. The Farm Journal, formerly Pro Farmer Crop tour that kicks off today. Crop scouts should see highly variable conditions all week before a final estimate is released at the end of the week. Ideas are that variable conditions will force USDA to lower production estimates next month.

Weekly Chicago Soybeans Futures © Jack Scoville

Weekly Chicago Soybean Meal Futures © Jack Scoville

Rice

Rice closed lower last week and the market seems comfortable right now trading between 1200 and 1250 basis the September contract. Rice futures appear to be in a consolidation phase right now as the harvest is set to expand. The harvest remains active in Louisiana and Texas with variable yields and quality reported in Louisiana and good yields and quality reported in Texas. Harvest activity will move to other states soon.

Mississippi has seen some early cutting in southern áreas. It has been raining a lot in the state, and it looks now like the main harvest could be delayed. Arkansas and Missouri will not get started until late August at the earliest, but recent big rains in Arkansas will be a concern for the crops as Rice likes drier weather when forming grain and trying to mature. Crop potential in these states is an open question due primarily to harsh weather at the start of the growing season and variable conditions for much of the year. Current weather is mostly good in Missouri and might improve this week in Arkansas.

Asian prices remain soft. The Asian market has been weaker in the last few weeks as the next harvest comes closer in many countries. Growing conditions are improved in India as the monsoon has been better, but coverage of rains has been spotty until now and there are still chances for weaker production than expected in India this year. Most of Indochina and Southeast Asia have seen good weather.

Weekly Chicago Rice Futures © Jack Scoville

Palm Oil and Vegetable Oils

World vegetable oils markets were mixed last week, but overall price action is relatively strong. Palm oil futures held well on ideas that production data is now topped out and that trends will be for lower monthly production for the next several months. MPOB released its July data and showed production near 1.83 million tons for Malaysia, up from 1.51 million tons in the previous month.

Export reports from the private sources so far this month are lower than last month, but this has been expected by the trade. Soybean oil rallied late in the week and could have rejected a move to turn trends down on the charts. Canola remains relatively strong amid tight Canadian market conditions and adverse growing conditions. A primary negative for prices has been the strength of the Canadian Dollar against the US Dollar.

Western areas of the Prairies remain too dry but have seen some rains in the last couple of weeks to promote more stable growing conditions as the crop starts to move to maturity. Eastern areas have seen good rains, but many eastern areas have seen too much rain. Demand from both the processor side and the export side has been strong enough to generally support the Canola market.

Weekly Malaysian Palm Oil Futures © Jack Scoville

Weekly Chicago Soybean Oil Futures © Jack Scoville

Weekly Canola Futures © Jack Scoville

Cotton

Cotton was lower on follow through selling tied to the USDA production estimates and generally favorable weather conditions here in the US and around the world. Traders had expected higher production due to the increased planted area, but USDA showed production potential above all trade guesses at 30.545 million bales. The growing weather in the eastern half of the US is generally good and crop conditions are reported to be good by producers and observers. These areas include parts of Texas, the Delta, and the Southeast.

Warmer temperatures have arrived and there has been enough rain. Texas and the desert Southwest and into California has seen extreme heat and mostly dry weather, but the temperatures have moderated and rains have started to fall in the Texas Panhandle. Conditions have improved as the crop forms bolls and the bolls open.

There is increased production potential in Asia, and mostly in India and Pakistan due to improved monsoon rains. However, the monsoon has been uneven, with some areas in India flooding out and forcing some producers to replant if possible. Some areas have missed out on rains for the last few weeks, but these areas had seen flooding rains so the drier weather allowed for replanting. Some rains are expected in most areas this week amid relatively moderate temperatures.

Chinese growing conditions have improved, but crops appear to be uneven there. It has been very hot and dry in Turkey and there is talk of crop losses there. Areas to the south of Russia are in good condition. The weekly charts show that futures might have completed a bear flag last week. If so, lower prices are likely for the next few weeks.

Weekly US Cotton Futures © Jack Scoville

Frozen Concentrated Orange Juice and Citrus

FCOJ closed lower on Friday, but higher for the week as three tropical systems have formed in the Atlantic. The potential for storms increases dramatically for the next few weeks, and the systems are coming right in line with long term normals. Florida weather is very good as it is now drier after some recent rains. There are no systems in the Atlantic to cause concern about tropical storm development that could be detrimental to trees and fruit.

One System is moving away from the US in the Atlantic and into Mexico and one might fall apart before getting close to the US. The third System could develop and could move to Florida. The demand side remains weak and there are plenty of supplies in the US. Trees now are showing fruits of varying sizes and overall conditions are called good. Brazil crops remain in mostly good condition. The weekly charts show that a low could be near completion.

Weekly FCOJ Futures © Jack Scoville

Coffee

Futures were sharply lower as the US Dollar started to move a little higher and pushed the Brazilian Real lower. The trends are down again on the charts, and weaker prices should be expected this week in New York. London has been holding better as Robusta market conditions remain relatively tight and as Vietnam is not offering much.

Brazil is now at harvest, and traders and producers are reporting low quality and small beans. There is some concern about the dry weather there, but it is the dry season and rains are expected to begin to promote good first flowering soon. Some rains were seen in southern areas last week, but these rains did not move north into Minas Gerais as had been forecast, so the big areas remained dry.

Cash market conditions in Central America remain quiet as that part of the world is between harvests. There is coffee to sell, but little buying interest from major roasters. London had been stronger as supplies in the cash market are tight due to reduced Vietnamese selling and tight supplies in the country. Indonesia and Brazil have been very low on supplies as well, but Brazil is now harvesting its next Robusta crop.

Weekly New York Arabica Coffee Futures © Jack Scoville

Weekly London Robusta Coffee Futures © Jack Scoville

Sugar

Futures in London and New York were higher, but both markets are showing down trends on the weekly charts. Ideas are that there will be plenty of Sugar available to the market this year after several years when production was below demand. The big harvest in Brazil continues. Some of the processing will probably switch now to ethanol due to tax changes, but reports indicate that there is still a big over of sugar from there into the world market.

Production potential in India and Thailand seems improved for now as monsoon rains have been better than last year. It is raining in much of India now as the monsoon is active, but rains have been uneven. Some northwest areas have been flooded due to big rains. Other areas are too dry and there could be some damage to crops if more rains do not show up fairly soon. Some of the dry areas in the west should see rains this week, and flooded areas have seen drier weather in the last couple of weeks.

Thailand is getting rains. The rest of Southeast Asia is seeing average to above average rains so far this year. Some problems are being reported in Europe and Russia for the beet Sugar production.

Weekly New York World Raw Sugar Futures © Jack Scoville

Weekly London White Sugar Futures © Jack Scoville

Cocoa

Futures markets were lower last week on follow through long liquidation after the market could not move above some strong resistance areas on the charts. Futures are now back to test the lower end of the recent trading range. Ideas of generally good weather and ample supplies available for any demand keep the market in the range.

Harvest activities for the previous crop in West Africa are completed. The next harvest gets underway in the next month or so. The demand should continue to increase if prices remain relatively cheap and as retail prices continue to move lower in important consuming areas like Europe. The next production cycle still appears to be big since the growing conditions around the world are generally very good, but might be smaller than last year due to lower prices.

Offers from West Africa have been very strong until recently, and now offers have backed off as prices have fallen and amid talk that the production might be a little smaller than anticipated. West Africa has seen much better rains this year and now getting some showers mixed with hot and dry weather. Growing conditions are good. East African conditions are now called good. Good conditions are still being reported in Southeast Asia.

Weekly New York Cocoa Futures © Jack Scoville

Weekly London Cocoa Futures © Jack Scoville

Dairy and Meat

Dairy markets were higher last week, and longer term trends remain up. Butter prices continue to be the strength of the market on reports of very good demand and adequate supplies. Cheese prices have been relatively weak, but are holding firm now. Demand is good for cream, but cream has generally been available to meet the demand. However, there are some shortages of cream in a few locations.

Cream demand for butter has been very good. Demand for ice cream has been mixed depending on the region. Cheese demand still appears to be weaker. US production conditions have featured some abnormally hot weather in the west that is hurting milk production. The weaker US Dollar is helping on export ideas that might not mean much as US prices are higher, but the US Dollar weakness takes the edge off the higher internal prices.

US cattle and beef prices were lower and trends in cattle futures remain down. The beef market remains weaker in the last couple of weeks, and cattle prices have been under pressure since the release of the monthly cattle on feed report and the semiannual inventory report that showed bigger supplies are coming. Feedlots are filled and cattle will continue to be offered to the cash market. However, ideas are that more supplies are coming as weight per carcass is high and more cattle is coming to the market. A seasonal demand increase is likely now, and October is very cheap to cash, so downside potential in futures might be limited.

Pork markets and Lean Hogs futures were weaker on a seasonal trend to lower demand. Ideas are that futures are too cheap to cash and that the spread between the two need to come together more than they are now. Demand has been lower for the last couple of weeks and this has affected pricing. Demand starts to work lower as most of the Summer buying is done. There are big supplies out there for any demand. The charts show that the market could work lower.

Weekly Chicago Class 3 Milk Futures © Jack Scoville

Weekly Chicago Cheese Futures © Jack Scoville

Weekly Chicago Butter Futures © Jack Scoville

Weekly Chicago Live Cattle Futures © Jack Scoville

Weekly Feeder Cattle Futures © Jack Scoville

Weekly Chicago Lean Hog Futures © Jack Scoville

Futures and options trading involves substantial risk of loss and may not be suitable for everyone. The valuation of futures and options may fluctuate and as a result, clients may lose more than their original investment. In no event should the content of this website be construed as an express or implied promise, guarantee, or implication by or from The PRICE Futures Group, Inc. that you will profit or that losses can or will be limited whatsoever.

Past performance is not indicative of future results. Information provided in this report is intended solely for informative purpose and is obtained from sources believed to be reliable. No guarantee of any kind is implied or possible where projections of future conditions are attempted.

The leverage created by trading on margin can work against you as well as for you, and losses can exceed your entire investment. Before opening an account and trading, you should seek advice from your advisors as appropriate to ensure that you understand the risks and can withstand the losses.

—

DISCLAIMER: This article expresses my own ideas and opinions. Any information I have shared are from sources that I believe to be reliable and accurate. I did not receive any financial compensation in writing this post, nor do I own any shares in any company I’ve mentioned. I encourage any reader to do their own diligent research first before making any investment decisions.

PayPal’s Slowdown: From Fintech Leader to Low-Growth Dividend Stock

PayPal has shifted from fintech leader to low-growth, value-style stock, losing over 25% in market value and trading at a...

Tilray (TLRY) Falls as Bearish Momentum Persists Despite Marketing Push

Tilray (TLRY) fell 3.32% to $4.44, remaining below key moving averages and signaling continued bearish pressure. Despite a £1 million...

ESG Gap Persists as Firms Struggle to Link Sustainability to Financial Value

KPMG’s Global Survey shows a major gap between ESG awareness and financial integration. While 72% of managers understand sustainability strategies,...

Bitcoin and Ethereum Slide as Market Pressure Builds Amid Strategy Concerns and Layer 2 Disruptions

Bitcoin fell below $60,000 with heavy ETF outflows, pressured by concerns over Strategy’s finances and its STRC stock decline. Ethereum...

AI Venture Builder Launches €600K Crowdfunding Round to Scale Secure AI Solutions

AI Venture Builder, an Italian-British firm developing AI applications and vertical startups, returns to CrowdFundMe with a equity campaign. After...

|

|

|  |

|

|

-

Crypto2 weeks ago

Crypto2 weeks agoBitcoin Rises on Iran Deal as Crypto Markets React to AI and SpaceX News

-

Africa1 day ago

Africa1 day agoBank of Africa Expands Sino-African Trade Partnerships in Beijing

-

Biotech1 week ago

Biotech1 week agoBavarian Biotech Sector Expands with Record Funding and Startup Growth in 2025

-

Business3 days ago

Business3 days agoMarkets Diverge as Oil Falls, Rates Hold, and Inflation Persists

You must be logged in to post a comment Login