Markets

How the weather and the return of the pandemic influence the futures market

New York and London sugar futures were a little lower on weaker world petroleum prices. The markets now show a reversal in trends to down on the weekly charts. Coronavirus has returned to the US and Europe and has caused some demand concerns. Brazil mills have been producing more Sugar and less Ethanol due to weak world and domestic petroleum prices. About 45% of the crush this year will go to Sugar.

Wheat

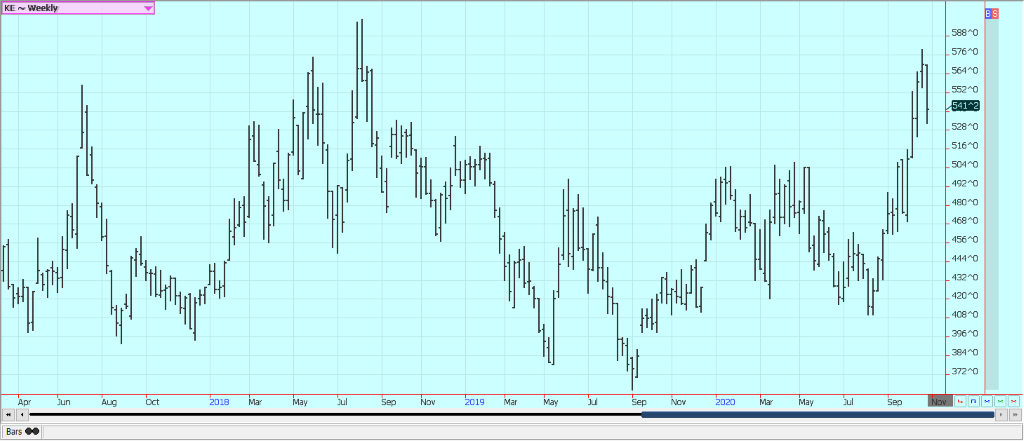

Winter Wheat markets were lower as the weather turned better for crop development. US weather is much improved with some precipitation reported in much of the western Great Plains. Only southwest Kansas and southeast Colorado are still dry. Parts of eastern Ukraine and southern Russia are getting some showers too. Western Australia is expected to get some rains this week. The rains in the US are the most substantial and will have helped solve the longer-term drought problem out there. The showers in Ukraine and Russia are too late to give much help, but some plants will become better established. The demand has held well and world prices remain high at the moment, with Russian prices quoted at $257.00 per ton. The market in Russia has remained high on limited supply as farmers hold the Wheat back due to the drought.

Weekly Chicago Soft Red Winter Wheat Futures

Weekly Chicago Hard Red Winter Wheat Futures

Weekly Minneapolis Hard Red Spring Wheat Futures

Corn

Corn and Oats were lower last week despite some great export demand in the Corn market. The weekly SDA export sales report showed sales of over 2.4 million tons and then USDA announced on Thursday that Mexico had bought 1.4 million tons of US Corn. There was no export demand from China last week in the daily announcements. US weather was tough for harvesting last week with wet and cold conditions for much of the Midwest. Conditions are much improved this week with warmer and drier weather and the harvest is underway again. Yield reports have generally been good except for the drought and derecho areas of Iowa.

Weekly Corn Futures

Weekly Oats Futures

Soybeans and Soybean Meal

Soybeans and Soybean Meal closed lower on less Chinese demand. China has not appeared in the daily sales announcements from USDA in over a week now and the market is feeling the loss. China still needs to buy for crushers, but appears to have bought what was necessary for the reserve. The weather in the US is good for any remaining harvest as it has turned drier and warmer this week after a cold and wet week last week. The weather in South America is improved. Showers and rains have fallen in most of Brazil and much of Argentina. Southern Brazil and Paraguay have missed out on the good rains but did get a few showers. Soybeans are actively being planted in Brazil.

Weekly Chicago Soybeans Futures

Weekly Chicago Soybean Meal Futures

Rice

Rice was higher last week for November, but lower in the other months. An improved weekly export sales report was seen once again. Export demand has been strong in general. Reports indicate that domestic demand has been poor to average with better consumer demand more than offset by much less demand from schools and other institutions. The harvest is mostly over in northern states with good field yields reported. Southern Louisiana and Texas are waiting for the second crop harvest to start. Producers had to endure Hurricane Delta and then Zeta in Louisiana, and some of the second crop Rice got hurt. Quality is said to be very good everywhere.

Weekly Chicago Rice Futures

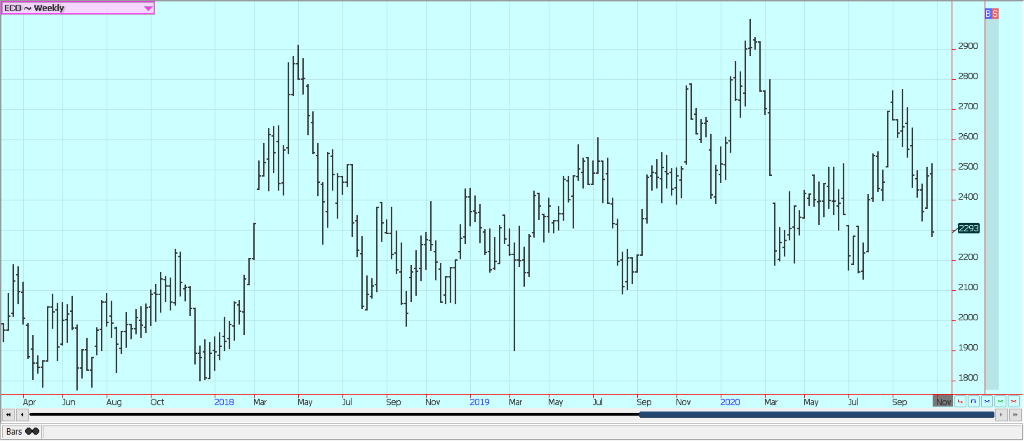

Palm Oil and Vegetable Oils

Palm Oil closed higher on ideas of decreasing production and private reports of stronger demand. Ideas are that MPOB can show lower ending stocks this month. Chart trends are trying to turn up again. It is seasonally a time for trees to produce more due to more regular rains. Getting workers to do the harvest remains hard and the lack of labor has been a big problem. At least some of the plantation owners have asked for more migrant workers to cover the lack of workers that can be sourced locally. Soybean Oil and Canola were lower on weaker US and world petroleum prices. Trends are mostly sideways in Soybean Oil and in Canola. Canola farmers are selling due to harvest pressure, and industry and speculators are starting to sell now. The Canadian Dollar is higher but Canola is still considered relatively cheap in the world market. Harvest in the Prairies is almost done and yields are reported to be very strong.

Weekly Malaysian Palm Oil Futures

Weekly Chicago Soybean Oil Futures

Weekly Canola Futures

Cotton

Cotton closed lower for the week and the weekly charts show a trend reversal to down. Hurricane Zeta moved through the Delta and Southeast a couple of weeks ago and did some damage to Cotton. Open bolls were reported in both regions and Cotton fiber was discolored or else blown out of the bolls due to the rain and winds. The discolored Cotton is getting a chance to recover now as it has turned dry and the fiber can be naturally bleached by the Sun. It should stay drier for the next week or longer. The weekly export sales report showed improved demand last week and was considered a reason to buy futures. There was no major Chinese demand. Demand should stay generally weak as long as the Coronavirus is around. Shopping is hard to do and many people are still unemployed.

Weekly US Cotton Futures

Frozen Concentrated Orange Juice and Citrus

FCOJ was near unchanged once again last week. Florida has been spared any hurricanes or other serious storms this year in a year that has been very active for tropical storms. The Coronavirus is still promoting the consumption of FCOJ at home. Restaurant and food service demand has been much less as no one is really dining out. Florida production prospects for the new crop were hurt by an extended flowering period, but the weather is good now with frequent showers to promote good tree health and fruit formation. Brazil has been too dry and irrigation is being used. Showers are falling in Brazil now. Mexican crop conditions are called good to very good with ample rains.

Weekly FCOJ Futures

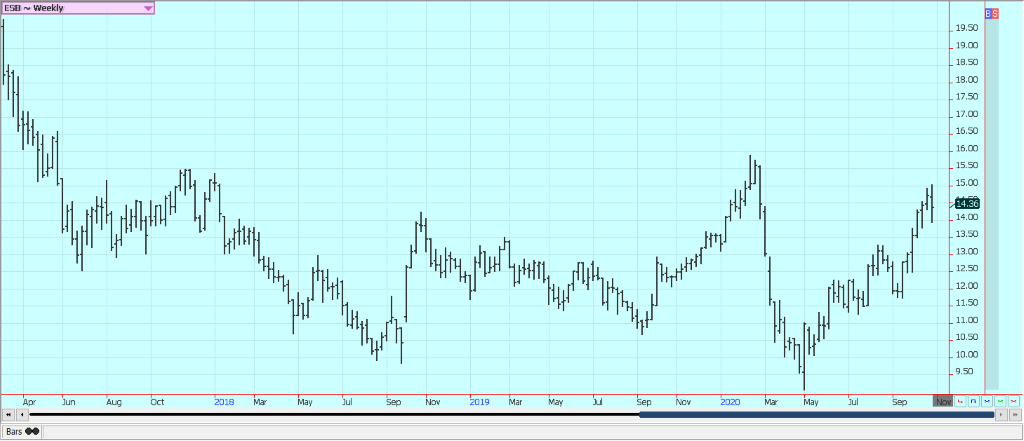

Coffee

Futures were a little lower last week in New York and higher in London. London had been better supported due to stronger demand ideas and worries about the weather in Vietnam as the country is getting too much rain now and flooding is being reported in the Central Highlands. The rains should continue for another week. The demand from coffee shops and other foodservice operations is still at very low levels as consumers are still drinking Coffee at home. Reports indicate that consumers at home are consuming blends with more Robusta and less Arabica. The Brazil harvest is over and producers are selling due to the recent extreme weakness in the Real. Ideas are that production is very strong this year as it is the on year for the trees. Central America is also offering right now and offers are increasing. The weather is good in Colombia and Peru.

Weekly New York Arabica Coffee Futures

Weekly London Robusta Coffee Futures

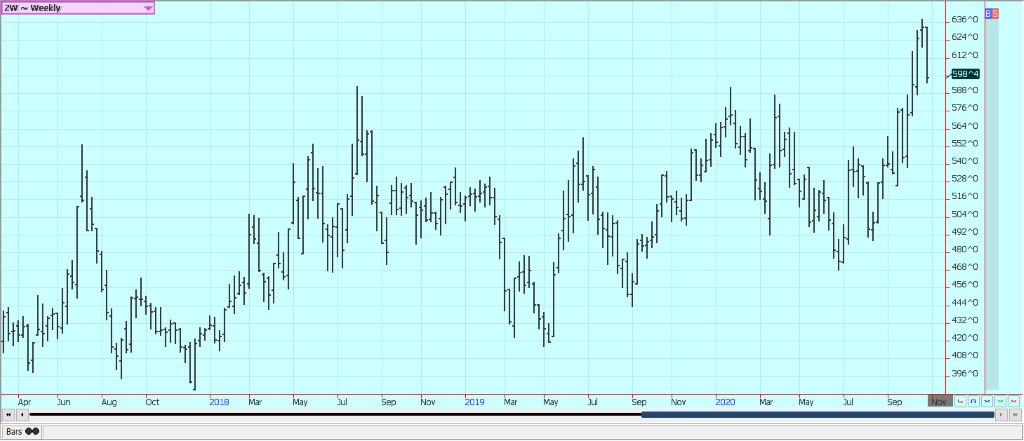

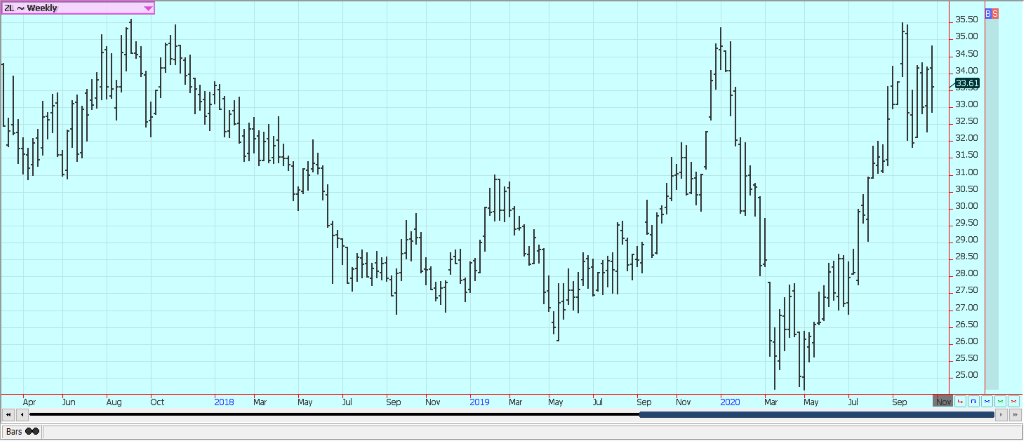

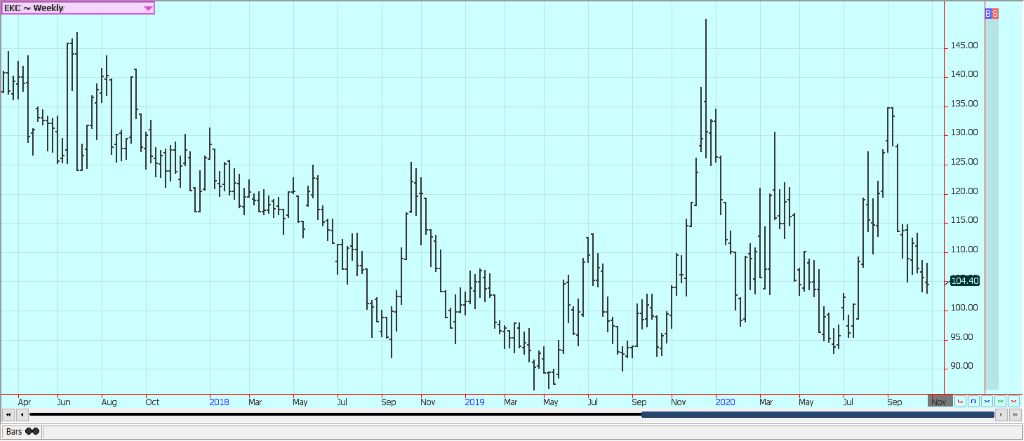

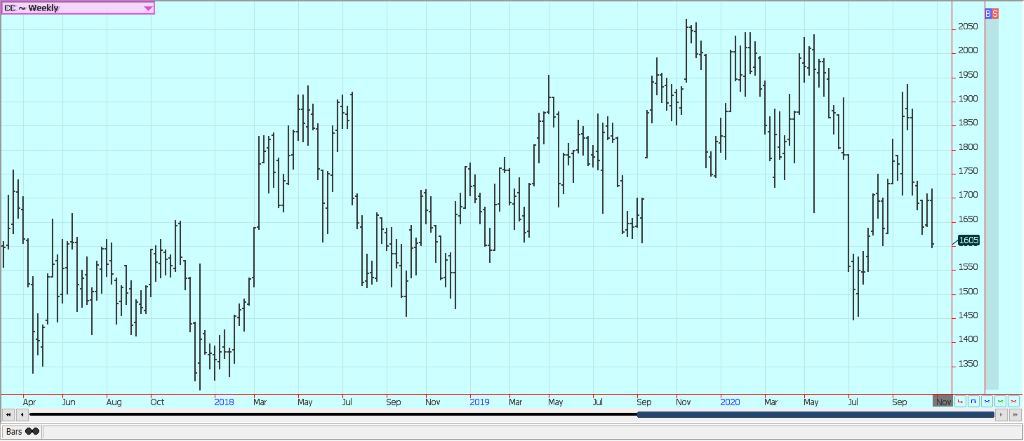

Sugar

New York and London were a little lower on weaker world petroleum prices. The markets now show a reversal in trends to down on the weekly charts. Coronavirus has returned to the US and Europe and has caused some demand concerns. Brazil mills have been producing more Sugar and less Ethanol due to weak world and domestic petroleum prices. About 45% of the crush this year will go to Sugar, from 35% last year. It has been dry lately to affect Sugarcane production and producers are less aggressive sellers. Rains are falling now to improve Sugarcane growing conditions. India has a very big crop of Sugarcane this year but the exports have been hard to make. The Indian government has not yet announced the subsidy for exporters of Sugar so no one knows how much to charge yet. Thailand might have less this year due to reduced planted area and erratic rains during the monsoon season. Rains are moving through the country now from Vietnam and the Pacific. The EU is having problems with its Sugarbeets crop due to weather and disease. Demand appears to be about average.

Weekly New York World Raw Sugar Futures

Weekly London White Sugar Futures

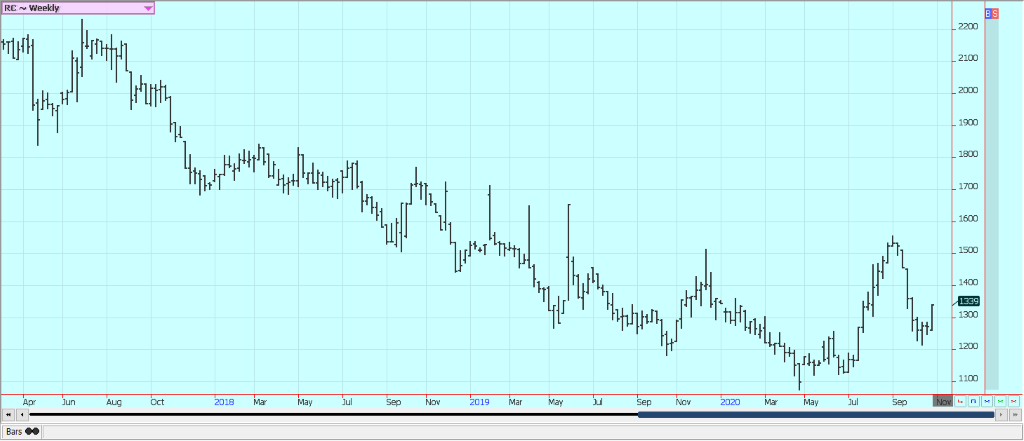

Cocoa

New York and London were lower on demand concerns caused by the return of the Coronavirus to Europe and the US. The weekly charts show that downtrends are established again. The harvest for the next main crop is almost done for much of West Africa and very strong production is expected. There are a lot of demand worries as the Coronavirus is making a comeback in the US. Europe is also seeing a return of the pandemic. The North American and European cocoa grinds were at least 4% lower than a year ago and the Asian cocoa grind was down 10% from last year. Ivory Coast at the tail end of the presidential campaign season and some violence is expected.

Weekly New York Cocoa Futures

Weekly London Cocoa Futures

__

(Featured image by wobogre via Pixabay)

DISCLAIMER: This article was written by a third party contributor and does not reflect the opinion of Born2Invest, its management, staff or its associates. Please review our disclaimer for more information.

This article may include forward-looking statements. These forward-looking statements generally are identified by the words “believe,” “project,” “estimate,” “become,” “plan,” “will,” and similar expressions. These forward-looking statements involve known and unknown risks as well as uncertainties, including those discussed in the following cautionary statements and elsewhere in this article and on this site. Although the Company may believe that its expectations are based on reasonable assumptions, the actual results that the Company may achieve may differ materially from any forward-looking statements, which reflect the opinions of the management of the Company only as of the date hereof. Additionally, please make sure to read these important disclosures.

Futures and options trading involves substantial risk of loss and may not be suitable for everyone. The valuation of futures and options may fluctuate and as a result, clients may lose more than their original investment. In no event should the content of this website be construed as an express or implied promise, guarantee, or implication by or from The PRICE Futures Group, Inc. that you will profit or that losses can or will be limited whatsoever. Past performance is not indicative of future results. Information provided on this report is intended solely for informative purpose and is obtained from sources believed to be reliable. No guarantee of any kind is implied or possible where projections of future conditions are attempted. The leverage created by trading on margin can work against you as well as for you, and losses can exceed your entire investment. Before opening an account and trading, you should seek advice from your advisors as appropriate to ensure that you understand the risks and can withstand the losses.

SBTi Net-Zero Standard 2.0 Enhances Corporate Climate Action

The Science Based Targets initiative (SBTi) has released Corporate Net-Zero Standard Version 2.0, a major update to its global framework...

Europe’s Cannabis Shift: Rising Use, and New Risks

EUDA report shows cannabis remains Europe’s most used illegal drug, with 22 million adults trying it. Use is highest among...

Remote Work Reshapes Sales Management: Key Lessons for Moroccan Leaders

Remote work is rapidly expanding among Moroccan managers, yet practices lag behind. Insights from France show higher productivity but weakening...

Corn Prices Slip Amid Strong Crop Conditions and Favorable Weather

Corn was lower again last week on Midwest rains despite a neutral WASDE report. The report showed slightly higher beginning...

Advances in Biomarkers and Targeted Therapies Transform Kidney Care in Autoimmune Disease

New biomarkers and targeted therapies are reshaping the management of kidney damage in autoimmune diseases like lupus and vasculitis. Experts...

|

|

|  |

|

|

-

Biotech6 days ago

Biotech6 days agoThe German Biotech Industry Faces Funding Crunch Despite Market Stability

-

Crypto2 weeks ago

Crypto2 weeks agoCardano in Decline as Hoskinson Distances Himself Amid Growing Uncertainty

-

Markets1 day ago

Markets1 day agoRising Inflation, Fed Uncertainty, and Market Excess Amid War and SpaceX Mania

-

Markets1 week ago

Markets1 week agoJobs Strength Triggers Market Reversal as Inflation and Rates Take Focus