Business

US wheat prices at their lowest while corn planting conditions improve in South America

Wheat and other agricultural products continue to fluctuate due to weather conditions and other factors.

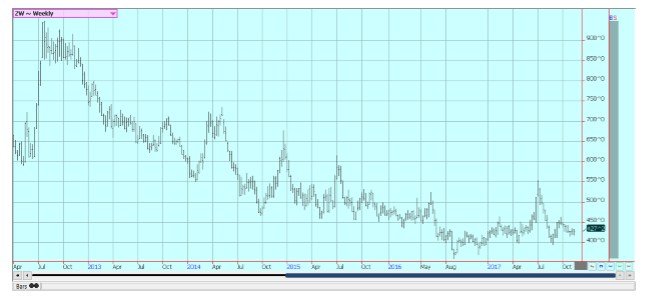

Wheat

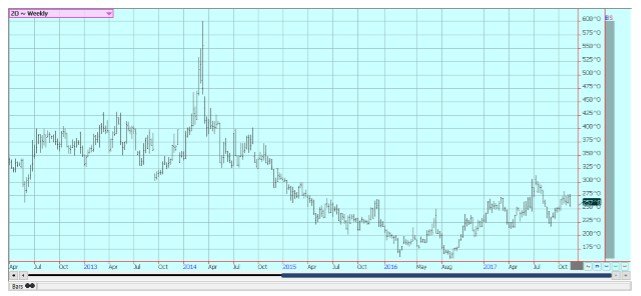

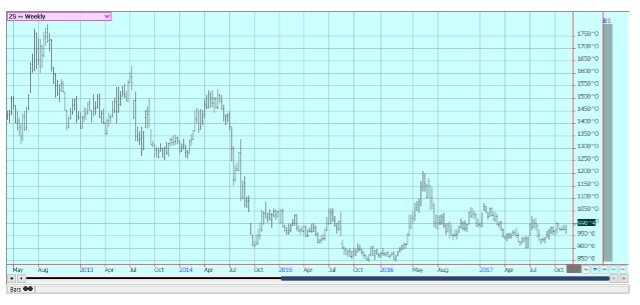

US markets closed slightly lower in Chicago last week. The weekly charts show that winter wheat prices are at the lowest levels since harvest and might now be cheap enough for sideways to higher trends to develop. Minneapolis has started on an uptrend and the indications of good demand for higher protein wheats continue. Futures traders still hope for improving demand as Egypt was able to buy despite a court ruling there that prohibited Ergot in any wheat imports. The prices were not really strong, but at least the deal got done.

The market is noting dry conditions in western Kansas and other parts of the western Great Plains and the La Nina Winter weather forecast. The long-range forecast calls for warmer and drier than normal conditions in the South and Southwest, and it is possible that Winter Wheat will suffer under more stressful conditions. The market continues to be worried about Russia and its ability to control the world wheat offer and price.

World estimates, in general, remain large and US offers will need to be low to take business. It will be another small US crop as farmers continue to reduce planted area year after year in response to the low world and US prices, due mostly to strong competition mostly from Russia. Prices might not improve much for the coming year as Russia expects another big crop that could be big enough to offset lost production in places like the US and Canada and also Argentina and Australia.

Weekly Chicago Soft Red Winter Wheat Futures © Jack Scoville

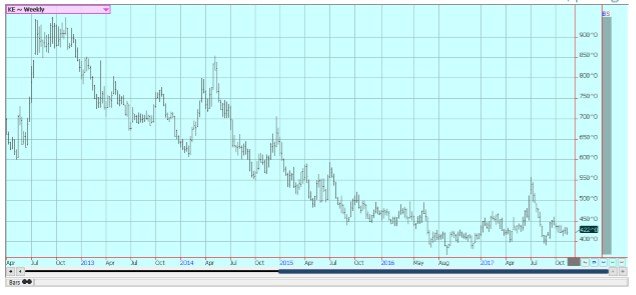

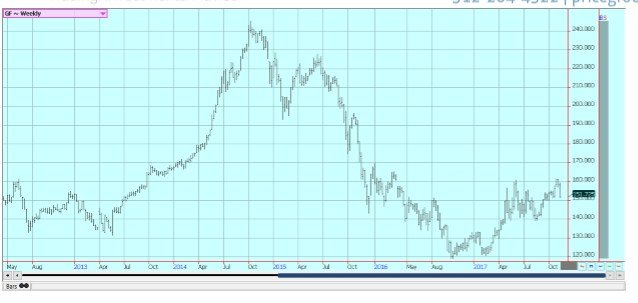

Weekly Chicago Hard Red Winter Wheat Futures © Jack Scoville

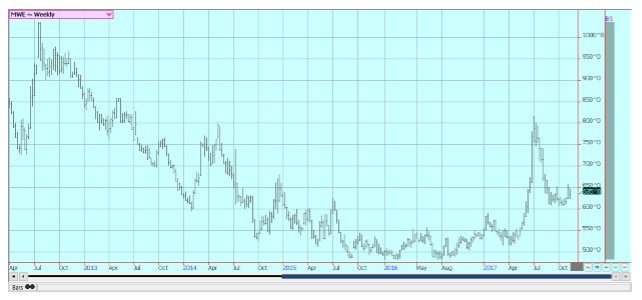

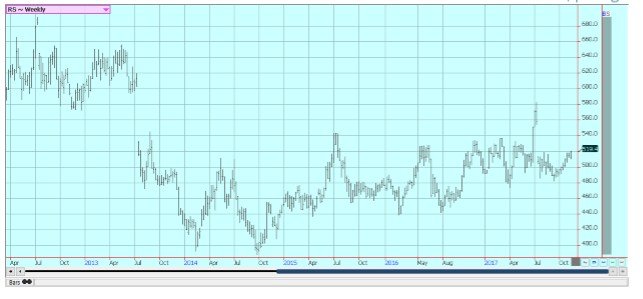

Weekly Minneapolis Hard Red Spring Wheat Futures © Jack Scoville

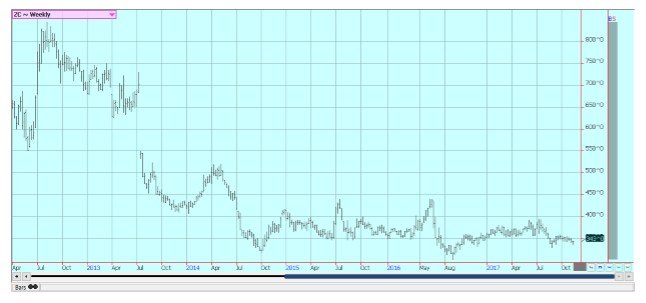

Corn

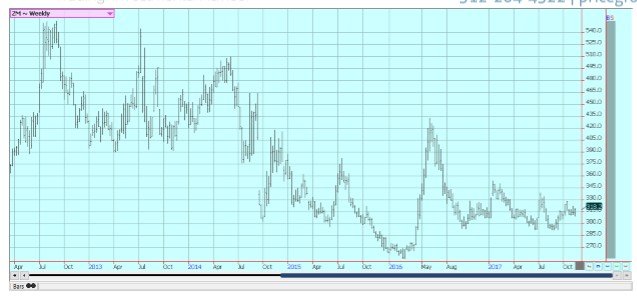

Corn closed near unchanged last week and oats closed lower. Some speculative buying was seen, mostly for seasonal considerations. Speculators have been very short and corn prices usually rally around Thanksgiving time. The trade is also looking at the potential for dry weather to develop in southern Brazil and Argentina. Oats closed lower and prices are now through swing targets and support areas on the weekly charts. More and more traders expect a short covering rally in corn.

Ideas of big supplies and less than great demand keep pulling the market down fundamentally, but it has been the funds who have established a huge and near record short position in futures. Farmers are not selling much corn even in the last part of the harvest due to weak basis and futures price levels. Basis levels have improved, but farmer offers remain down, although farmers have been actively delivering on contracts.

Corn planting is reported to be active in Argentina and southern Brazil amid improved conditions as the rains have stopped for now and are not expected to return in the short term. Not much selling is reported in South America. La Nina has started and could create dry weather in South America that could really hurt yields. It is common for Argentina and southern Brazil to have drought in La Nina years, so the weather in these areas will be watched carefully.

Weekly Corn Futures © Jack Scoville

Weekly Oats Futures © Jack Scoville

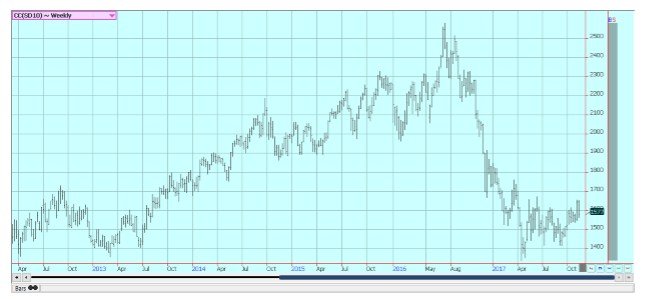

Soybeans and Soybean Meal

Soybeans and products were higher on Friday on seasonal considerations. Soybeans and products normally rally around Thanksgiving, and it looks like that particular rally is underway now. The fundamental reason for Soybeans to work lower was fears of reduced Chinese demand and ideas of improved planting conditions in Brazil. China might be forced to reduce demand as the government is making it harder to get safety permits. Some GMO Soybeans have made it into the human food chain, and this news has caused the government to slow the process until it can identify the problems. However, there was talk of active Chinese buying of US Soybeans on Friday.

Meanwhile, it is wetter in the north of Brazil and drier to the south and into Argentina and planting speed can be increased. The crop is close to an average planting pace now after a slow start. Planting progress in Argentina is a little behind the averages, but at about the same pace as last year. Some beneficial rains have been reported in Mato Grosso and Mato Grosso do Sul, and reports indicate that fieldwork is active. It remains too wet to the south, but it has been drier in Argentina.

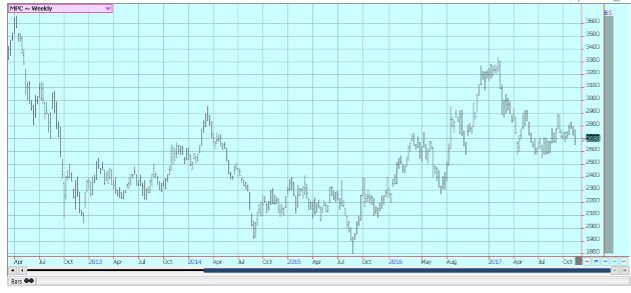

The US harvest is now about over in all areas of the US. The yield data generally runs behind year-ago levels, but are still very strong overall. Basis levels continue to improve in the interior as the harvest comes to a close. Soybeans are still holding an uptrend that started in mid-August but has found significant selling on rallies above $10.00 per bushel.

Weekly Chicago Soybeans Futures © Jack Scoville

Weekly Chicago Soybean Meal Futures © Jack Scoville

Rice

Rice closed sharply higher for the week in response to new demand news. Reports hit the market at midweek that Iraq had bought 90,000 tons of milled long grain Rice from the US, and this was big demand news for the trade. The news caught speculators short in the futures market and some commercials perhaps a little short in the cash market. Futures had been very undervalued in relation to the US domestic cash market, so the move higher has been fast. Futures and cash markets are now more in line with each other.

The volumes traded until last week reflect the slow domestic cash market. Rice is reported to be mostly sold already in Texas and Louisiana and has been getting sold in other states. Farmers now are more interested in hunting or holiday activities and so buying paddy Rice will be difficult. The Delta harvest is over and farmers are holding out for higher prices. The second harvest in Texas and Louisiana is coming to a close with more variable yields and quality. Reports from the country indicate good to very good yields and quality for the main harvest. The charts show that futures are now close to some big resistance areas, so some pressure to move lower this week is possible.

Weekly Chicago Rice Futures © Jack Scoville

Palm Oil and Vegetable Oils

World vegetable oils prices were a little lower. The biggest loser for the week was palm oil, and that market got hurt when private sources reported weaker exports from Malaysia. This news comes on top of news that MPOB showed higher than expected production at about 2.01 million tons for October. Palm oil futures fell through an uptrend line that has held since the middle of July, so trends are now down. Futures are at a big support area, but likely will see further price weakness in the next several weeks.

Canola was higher, in part on currency considerations and in part on late week price action in Chicago soybeans and soybean oil. It has turned cold in the Prairies, so farmers are not as willing to sell. Farmers in the US are not selling a lot of soybeans, either, and prices are starting to turn higher for seasonal considerations as the soy complex often rallies during the Thanksgiving week.

The US demand for soybean oil in biofuels should remain strong as the US moved to put punitive tariffs on imports from Indonesia and Argentina. Both countries are fighting these moves, and the process is moving to the courts. A final decision from the courts and then a real solution to the issue will likely take some time to be found.

Weekly Malaysian Palm Oil Futures © Jack Scoville

Weekly Chicago Soybean Oil Futures © Jack Scoville

Weekly Canola Futures © Jack Scoville

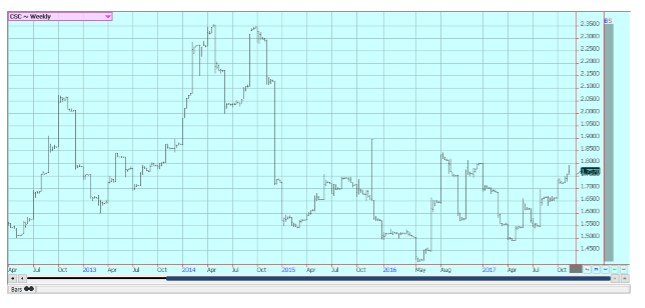

Cotton

Cotton was higher again Friday in response to very strong weekly export sales and on ideas that overall demand has been underestimated. The report gave the market Bulls a shot in the arm at a time when the futures market could be bottoming. The chart patterns suggest that futures could move higher over time, but needs to move above 7000 December and hold above that level to force speculative buying. Speculators are already long, so the breakout could be hard to sustain if it comes.

The futures market is watching the harvest roll along and is debating the demand for the US and world cotton. The Cotton quality has been dropping as the harvest moves forward, and the lower quality seems to be the biggest effects from the hurricanes seen during the growing season and then the freeze in the west at the tail end of the growing season.

Some traders say that USDA is seriously underestimating demand for the fiber, while the others look to the high USDA ending stocks estimates and suggest that any demand can be easily met. Futures had a muted reaction to the USDA reports and held to the range seen for the last few weeks. Farmers are reported to be quiet sellers right now. Harvest conditions are good in just about all areas.

Weekly US Cotton Futures © Jack Scoville

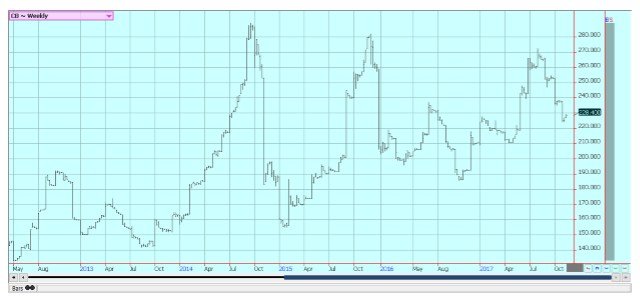

Frozen Concentrated Orange Juice and Citrus

FCOJ closed higher on Friday and for the week as the small crop in Florida impacted the market. Production was lower again at 50 million boxes in the recent USDA reports and the market had held strong ever since. The report once again highlighted the damage from the hurricane this year, and ideas are that production in coming reports will drop even more. Brazil weather has improved as groves are now getting rains, but suffered from drought at the flowering time. It was also very hot and it is possible that production from Sao Paulo state will be less.

The weekly charts indicate that higher prices are coming over time. Trees in Florida that are still alive now are showing fruits of good sizes, although many have lost a lot of the fruit. Florida producers are actively harvesting what is left as cleanup from the hurricane is about over now. The emphasis is on the fresh fruit market now, with processors mostly getting packinghouse eliminations at this time.

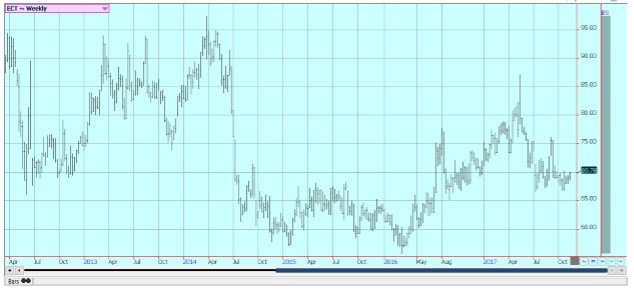

Weekly FCOJ Futures © Jack Scoville

Coffee

Futures were lower in New York and in London last week, with commercials scale down buyers and speculators still the best sellers in New York. Traders tried to move the market above the recent range, but the rally attempt failed to hold and the market closed back in the middle of the range on Friday. The trends are sideways on the charts in New York as traders look at the potential for a big crop in Brazil. The daily and weekly charts still imply that New York is about to complete a bottom and that prices could move higher for the next few weeks. London trends are mostly down.

The Brazil weather and tree condition is the main fundamental reason for movement in New York prices and could become the major reason to buy the market soon. Rains have been reported to coffee areas in Minas Gerais again, and many areas are reporting good conditions now after the earlier stress caused by the cold and dry winter.

The rains will need to continue and be in good amounts as it has been very dry and trees have been stressed for a year or more in some cases. Some were stressed after the production last year, while others suffered due to the dry and cold winter. Even so, improved weather now could mean a very good crop, although most likely not a huge crop of over 50 million bags.

Cash market conditions in Central America are more active as the harvest continues. Differentials have been stable but weak in the region. Colombian exports have held well as production appears to be good. Differentials have been stable and relatively strong.

Weekly New York Arabica Coffee Futures © Jack Scoville

Weekly London Robusta Coffee Futures © Jack Scoville

Sugar

Futures were higher and short-term trends in New York remain up. London chart patterns are also up. The market is rallying as mills in Brazil have decided to make more ethanol. Brazil is importing US ethanol to make up for short production, so the move by sugar mills in Brazil to supply the local ethanol market instead of the world sugar market makes economic sense. The move comes even as the ISO now estimates the world sugar production surplus at 5 million tons for the year.

There does not seem to be any big demand coming from any real direction, especially as China has cut back on imports and the year to year loss in demand is a very big amount. Upside price potential is limited as there are still projections for a surplus in the world production, and these projections for the surplus seem to be bigger. But, futures are going higher for now and have completed a big low on the daily and weekly charts.

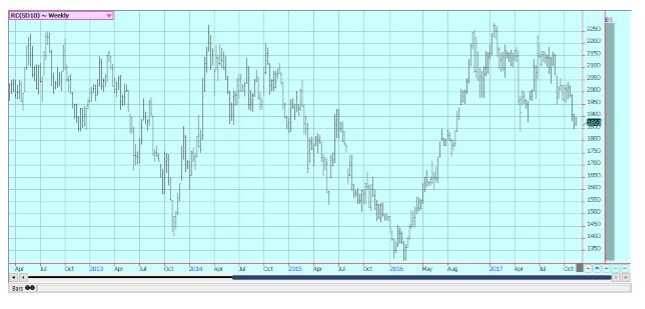

Weekly New York World Raw Sugar Futures © Jack Scoville

Weekly London White Sugar Futures © Jack Scoville

Cocoa

Futures closed a little lower on Friday and lower for the week. Prices remain strong overall in response to positive demand news from as the North American and the European grind data released last month, but the uptrend faltered again last week. The data showed increased demand. World production ideas remain high. Harvest reports show good to very good production will be seen this year in West Africa. Ghana and Ivory Coast expects a very good crop this year.

However, there have been some reports in Ivory Coast that diseases are hitting the crops and could reduce output in the end. Farmers have invested less in chemicals to protect and nourish crops due to low prices. Nigeria and Cameroon are reporting good yields on the initial harvest, and also good quality. The growing conditions in other parts of the world are generally good. East Africa is getting better rains now. Good conditions are still seen in Southeast Asia.

Weekly New York Cocoa Futures © Jack Scoville

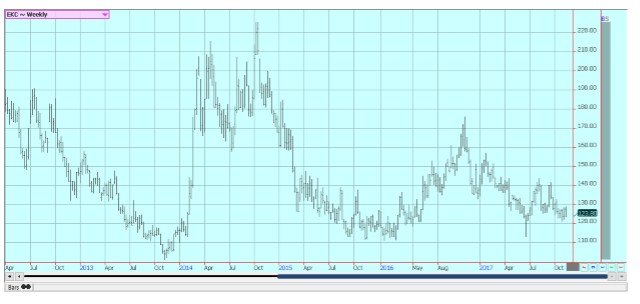

Weekly London Cocoa Futures © Jack Scoville

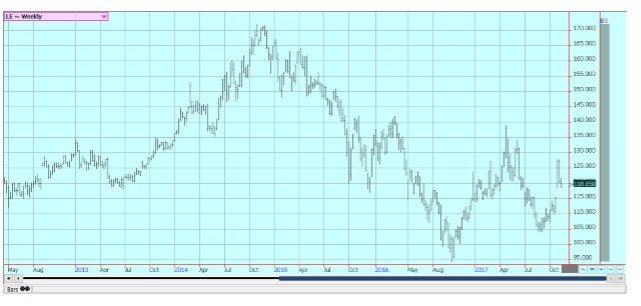

Dairy and Meat

Dairy markets were sharply lower again last week and milk futures made new lows for the move and also new contract lows. USDA reports ample supplies, but good to very good demand in just about all parts of the US. Milk and cheese demand has been mixed, but butter demand has weakened and prices in this market have moved sharply lower. Demand is good for cream, but cream has generally been available to meet the demand.

Cream demand for butter has been very good. Demand for ice cream has been mixed depending on the region but is holding well due to mild weather in much of the US until late last week. Cheese demand still appears to be weaker and inventories appear high. US production has been generally strong.

US cattle and beef prices were lower, and futures prices have been moving lower. Beef prices are mixed, and cattle traded about $2.00 per hundredweight lower last week. Ideas are that packers are still enjoying very strong margins at this time and can afford to pay more for cattle. This did not happen last week.

Cattle prices were steady to slightly weaker amid lighter than expected volume. It is the threat of increased supplies down the road that keeps the packers from buying aggressively. Feedlots are full, but ideas are that the big offer of cattle has passed. The monthly Cattle on Feed report showed big placements, so prices should move lower this week in both live cattle and feeder cattle futures.

Pork markets and lean hogs futures were lower. Ideas are that futures are reflecting the weaker supply and demand fundamentals now, but the overall market seems to be holding. Demand has been improved for the last couple of weeks and this has affected pricing. There are still ideas of bug supplies out there, but the market seems to have the supply side priced.

The weekly charts show that the market is trying to form a low at current prices, and futures have been cheap enough that a low is possible at this time. The weekly charts suggest that futures are developing a new trading range between about 6000 and 6800 basis nearest futures.

Weekly Chicago Class 3 Milk Futures © Jack Scoville

Weekly Chicago Cheese Futures © Jack Scoville

Weekly Chicago Butter Futures © Jack Scoville

Weekly Chicago Live Cattle Futures © Jack Scoville

Weekly Feeder Cattle Futures © Jack Scoville

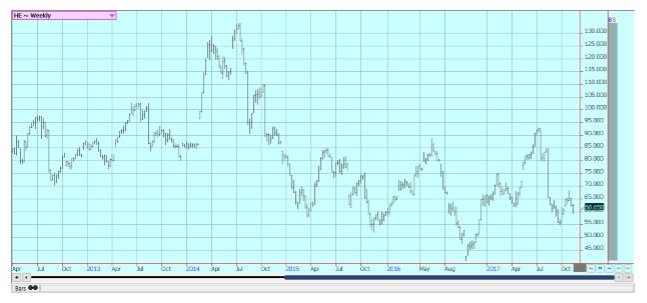

Weekly Chicago Lean Hog Futures © Jack Scoville

—

DISCLAIMER: This article expresses my own ideas and opinions. Any information I have shared are from sources that I believe to be reliable and accurate. I did not receive any financial compensation in writing this post, nor do I own any shares in any company I’ve mentioned. I encourage any reader to do their own diligent research first before making any investment decisions.

Youth Cannabis Use in Colorado Is Falling — But the Full Story Is More Complex

The 2026 Colorado survey shows teen cannabis use fell to 10 percent in 2025, down from 21 percent in 2015....

Morocco’s Growth Holds at 4.6% as Agriculture Offsets Economic Pressures

Morocco’s economy grew 4.6% in Q1 2026, driven by a strong agricultural rebound offsetting declines in industry. Services expanded moderately...

Abivax Shares Surge as New Trial Data Eases Safety Concerns Over Ulcerative Colitis Drug

Abivax shares surged nearly 36% after positive updated trial results for its ulcerative colitis drug obefazimod reassured investors following earlier...

El Dorado Raises $9M to Expand Cross-Border Fintech Platform

El Dorado, a Latin American fintech improving cross-border financial services, raised a $9 million Series A led by Paradigm with...

Bitcoin Stalls Near $60K as Strategy Moves, ETFs Outflow, and EU MiCA Rules Take Effect

Bitcoin hovers near $60,000 with ETF outflows, while Strategy boosts reserves, sells BTC, and raises dividends to reassure investors. Ethereum...

|

|

|  |

|

|

-

Fintech1 week ago

Fintech1 week agoMollie Expands Across EEA With €350M Investment to Strengthen European Payments Network

-

Crowdfunding5 days ago

Crowdfunding5 days agoAI Venture Builder Launches €600K Crowdfunding Round to Scale Secure AI Solutions

-

Impact Investing2 weeks ago

Impact Investing2 weeks agoAI Adoption in Italian Retail Stalls Despite Strong Experimentation

-

Cannabis1 day ago

Cannabis1 day agoCannabis Dominates Global Drug Use: Trends, Risks, and Shifting Markets

You must be logged in to post a comment Login