Featured

Canola market suffers from ongoing Canada-China tensions

Canada and China continue to have weaker trade relations and canola demand from China have been decimated.

The court case in which a Chinese national could be deported to the US on industrial espionage charges remains a major issue between Canada and China, and China has basically cut off purchases of Canadian Canola due to the trial.

Wheat

Winter wheat markets were lower last week and trends remain down on the weekly charts. The weekly charts show eventual swing targets near 292 for Chicago SRW and 364 in Chicago HRW. Both markets are near some important support areas on the weekly charts and could find some support now, but the overall trends should still remain down. Minneapolis could move as low as 450 basis the nearest futures. Minneapolis and Chicago HRW closed near the lows of the week and look especially weak. Minneapolis remained weak on fears of a dramatic increase in planted area to spring wheat in Canada. StatsCan confirmed the possibility last week in its planting intentions report that showed Canadian farmers are planning on planting more wheat this year at the expense of other crops, including a sizable cut in canola area.

Spring wheat prices have lost a lot and could go lower in the short term to price in the potential increase in planted area. The US spring wheat planted area was projected to be significantly down in the coming year, but an increased area in Canada is bigger and more important overall for prices. The US Spring wheat planting progress has been very slow as producers wait for the snow to melt and for the ground to dry. Any major planting delays now could mean that some US Spring wheat area lies fallow or is planted to soybeans, especially with the current weaker prices. Demand remains a problem as export sales remain weaker. Sales have improved over the last month but still, are not at levels to create any kind of bullish enthusiasm. Funds and other speculators remain very short in all three markets.

Weekly Chicago Soft Red Winter wheat Futures ©Jack Scoville

Weekly Chicago Hard Red Winter wheat Futures ©Jack Scoville

Weekly Minneapolis Hard Red Spring wheat Futures ©Jack Scoville

Corn

Corn was lower last week and made new lows for the move. There is enough supply out there for current demand and ideas of big supplies have kept prices on the defensive. Initial planting weather has not been good and fieldwork and planting are getting off to a slow start. More delays were seen over the weekend as a major storm moved through central and northern sections of the Midwest. Rain and snow were reported, with the biggest snows reported in southern sections of Minnesota and Wisconsin. Northern Iowa and northern Illinois also saw some snow. More precipitation, this time mostly big rains, are expected for much of the Great Plains and Midwest this week to keep any planting progress slow. It is more and more likely that the crop overall will be planted late, and this fact increases the likelihood that there could be a little yield loss and that some area could be switched to soybeans.

The weekly charts show that corn is in a downtrend, but the market has already come close to many objectives. Swing targets for the weekly charts are near 335 May. Oats traded higher and are finding support from tight supplies and delayed planting progress. Producers have been unable to get much done in Texas or in the northern Midwest. Weekly chart patterns are still up. US weather remains cool and wet for most of the Midwest. Brazil winter corn appears to be in good condition as the crop develops and moves to pollination. Crop estimates are high and have shown a tendency to increase as the crop develops. Most areas have seen enough rain for now. Corn prices are reported to be weakening in South America as the summer production from both Brazil and Argentina is now available. US demand has held well given the potential competition and Gulf basis levels have been steady.

Weekly Corn Futures ©Jack Scoville

Weekly Oats Futures ©Jack Scoville

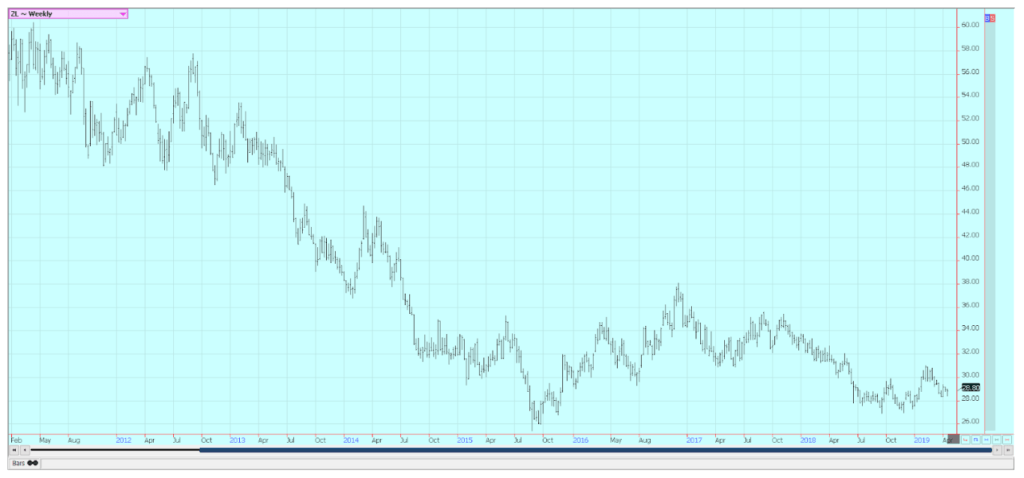

Soybeans and soybean meal

Soybeans and soybean meal were lower last week. Soybeans trends turned down last week. The weekly charts for soybeans show the potential for futures to move to about 823 and 770 basis the nearest futures contract. Soybean meal held the lows of the recent trading range, but price action overall looked weak. The market is waiting for the trade deal with China but worried about overall Chinese soybeans demand due to the Asian Swine Flu that has decimated the hog herd there. The government reports that at least 18 percent of its hog herd has been lost and private estimates show much higher loss potential. It is an indication of the very strong demand potential from China for hogs and pork and products and also an indication that soybeans and meal demand could be significantly less in the coming year as China works to eradicate the disease and then re-populate its herds.

The soybeans demand could take several years to recover as it will take time to rebuild the herds. Export differentials from the US and South America have been under pressure for this reason and also as the South American crop is now available. Prices are a little lower in Brazil than in the US despite a lack of farmer selling in Brazil. They are unhappy with the price and nervous over economic changes going on in Brazil as the new president works to overhaul the public pension system and other areas of public finance. The Real has been lower against the US Dollar in part due to the economic uncertainty. Some shifting of business back to the US could happen if the Brazil farmer holding patterns are strong enough and soybeans become scarce in Brazil ports, but basis levels right now are stable to weak.

Weekly Chicago Soybeans Futures ©Jack Scoville

Weekly Chicago Soybean Meal Futures ©Jack Scoville

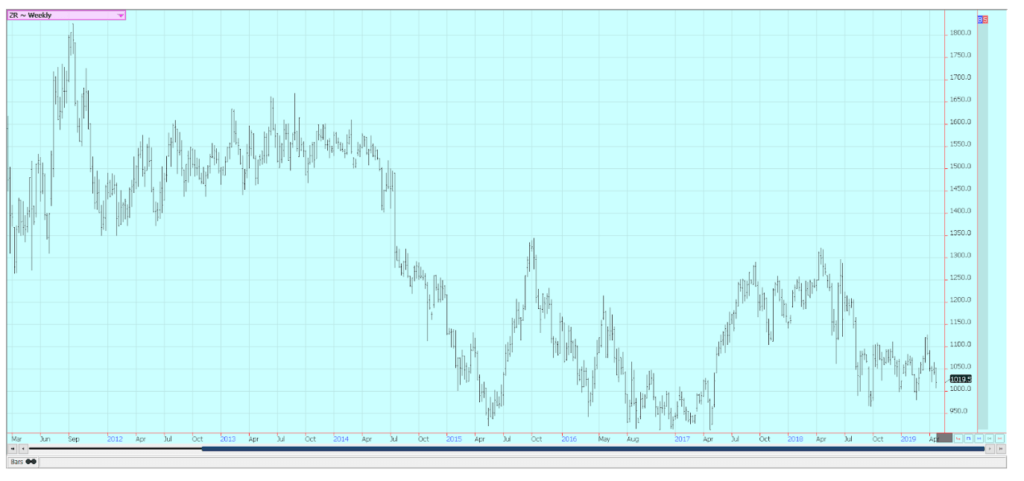

Rice

Rice was lower for the week and is now trading in the lower third of the trading range in place since the middle of last year. A strong US Dollar and flat prices in Asia have kept speculators trading from the sell side. Ideas of planting delays in rice and continued good export demand have been reasons to support futures. Planting has been active near the Gulf Coast and in Texas, and initial reports show that crops there are in good condition. Planting progress has been more sporadic to the north due to cool and wet conditions, but some planting has been done.

The market seems content to trade in a wide trading range for now and this implies that somewhat higher prices are possible over the next couple of weeks. The domestic market is using price breaks to extend forward coverage as the mills push to own rice into the next harvest. Prices have been firm in Texas due to good demand for limited supplies. Much of the rice is moving to Mexico. Prices have been firm in Arkansas due to a lack of producer selling as they wait to get the next crop planted. Some in the trade are disputing the planted area estimates from USDA. They think the planted area will be less in part due to the weather but in part due to the prices. However, the recent price drop in Soybeans might keep rice planted area higher than some expect. Current supplies are high and bearish traders point to this fact as a reason to keep prices relatively cheap or at least in a trading range.

Weekly Chicago Rice Futures ©Jack Scoville

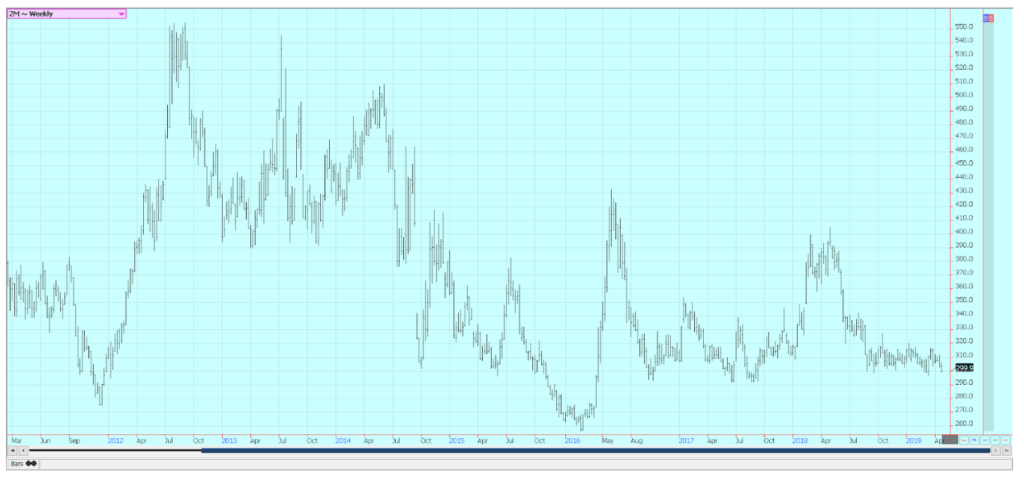

Palm oil and vegetable oils

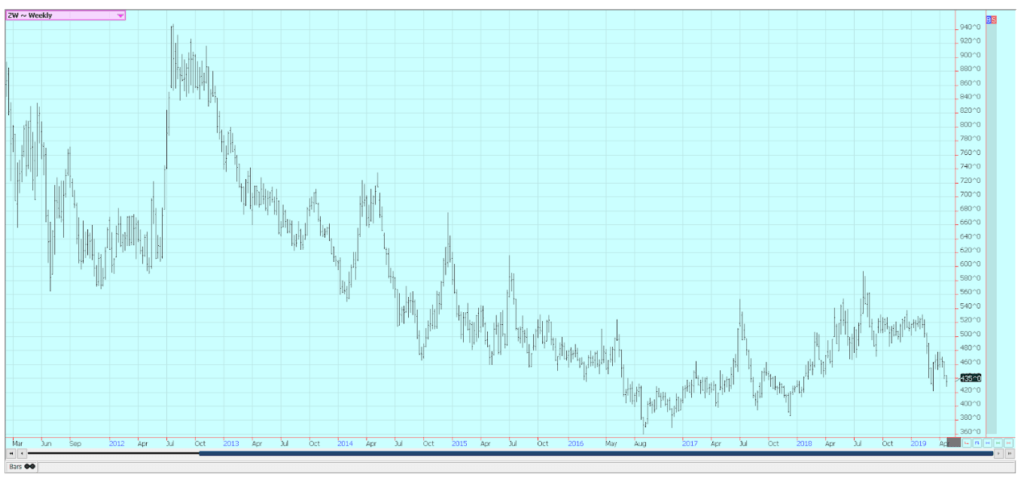

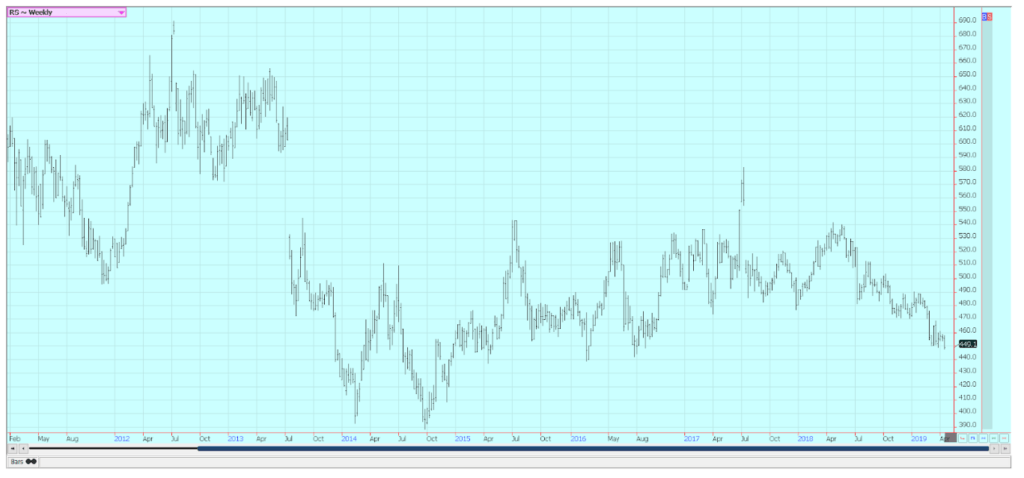

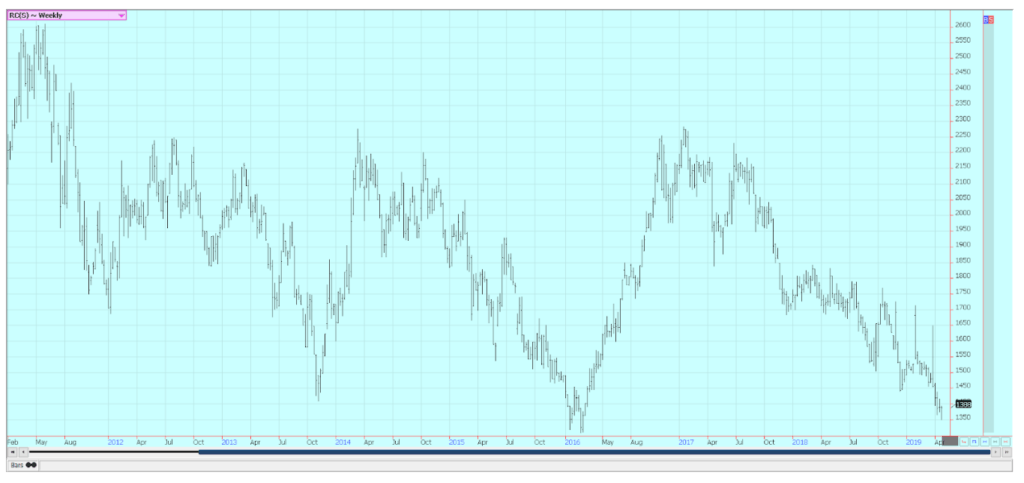

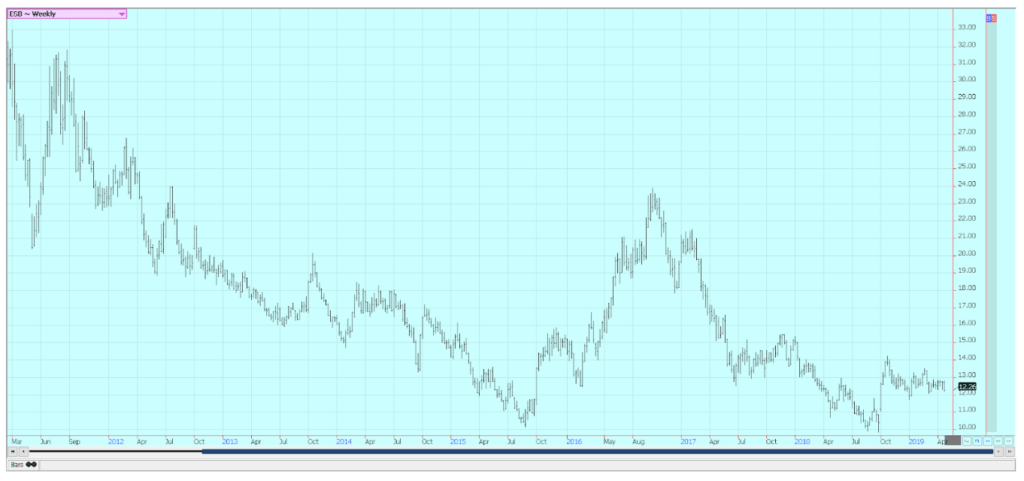

World vegetable oils markets closed lower last week. Palm oil was lower on worries about big supplies and despite strong exports so far this month. The positive MPOB data for March was not enough to keep the short term uptrend going and price trends are turning down. Canola was lower last week and made new contract lows as supplies in the country remain high and demand has softened.

The market has tried to become more stable in recent weeks but faces strong headwinds in getting demand flowing again and avoiding big ending stocks. Worries that low production and low planted area this growing season have started to support new crop prices. Soybean oil was lower. US soybean oil faces increased competition in world markets from Argentina as its soybeans are harvested and processed. Argentina will look to reclaim its position as the largest exporter of soybean oil in the world.

Weekly Malaysian Palm Oil Futures ©Jack Scoville

Weekly Chicago Soybean Oil Futures ©Jack Scoville

Weekly Canola Futures ©Jack Scoville

Cotton

Cotton was lower and closed about in the middle of the weekly trading range as futures continue to fade away from the 80.00 May level. The daily charts show that futures are developing a short term trading range. The weekly charts show that a stronger test of support near 75.00 May is likely. The weekly export sales report showed stronger demand for US cotton. There are still expectations that the US can have strong sales with other major exporters starting to run low on supplies. These expectations are starting to be fulfilled. USDA showed that planting progress was good in its weekly crop updates last week, but USDA could report slower planting progress in the reports this week due to bad weather in much of the Delta and Southeast last week.

Some rains have also appeared in western Texas. There are expectations that cotton planted area can increase this season as farmers could be attracted to cotton instead of grains such as corn or rice due to relative pricing. Anecdotal reports imply that the industry is preparing for more production as new facilities are being opened. Cotton production is poised to make a comeback in the Delta and Southeast, and the wet weather implies less corn planted and more cotton or soybeans planted. Prices and producer attitudes imply that more cotton could be planted.

Weekly US Cotton Futures ©Jack Scoville

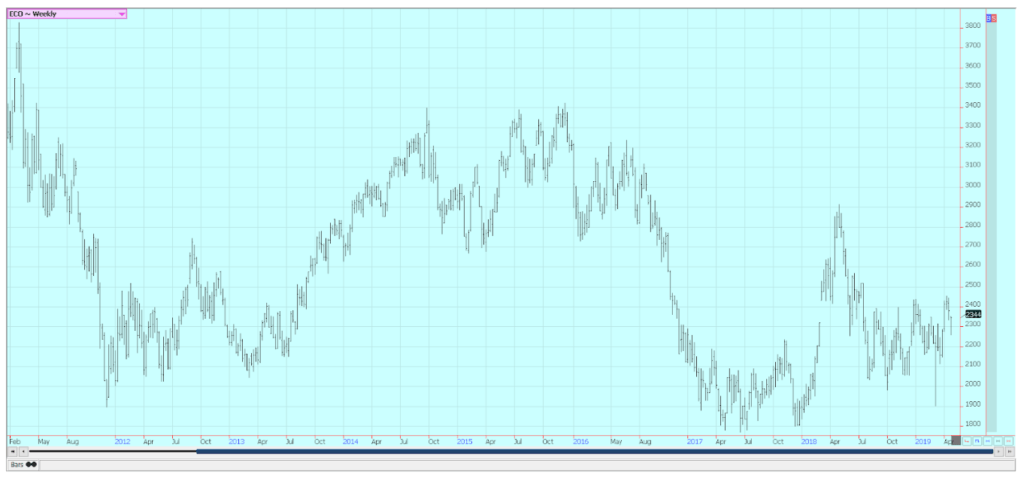

Frozen concentrated orange juice and citrus

FCOJ was lower and settled near the lows of the week. Trends are down on the daily and weekly charts as the market looks at a big oranges crop and little demand for FCOJ. Inventories inside the state are significantly higher than a year ago as Florida Citrus Mutual showed a 30 percent increase in state inventories in its weekly report. The increase is coming from less demand and higher imports along with the increased domestic production. The oranges harvest remains active in Florida as the new crop begins to develop.

Producers are concentrating on harvesting Valencias and harvest progress should be strong. Fruit for the next crop is developing and ideas are that the next crop is off to a very good start. Production is very uniform so far this year and development throughout the state is about equal. Some fruit drop is being reported, but this is normal as the trees move to the next crop and drop the old fruit. Irrigation is being used frequently to help protect crop condition. Mostly good conditions are reported in Brazil.

Weekly FCOJ Futures ©Jack Scoville

Coffee

Futures were higher for the week in New York and near unchanged for the week in London. Weakness in the Brazilian Real caused some speculative selling earlier in the week in New York, while reports of steady offers from Asia hurt Robusta in London. Futures are acting oversold, so a short term rally is possible at this time. The trade is still worried about big supplies, especially from Brazil and low demand. Brazil is dominating the market, and other exporters are having a lot of trouble finding buyers. Roasters were scaled down buyers on the extended down move and now have more than ample supplies in-house or on the way.

Prices are generally below to well below the cost of production for world producers, and prices are getting to that point for producers in Brazil and Vietnam. The inventory data from ICO and others shows ample supplies in the world market. Brazil had a big production year for the current crop, but the next crop should be less as it is the off year for production. Ideas are that the next crop might still be big as the weather has been good for the trees so far. Mostly dry conditions are in the forecast for this week. Vietnam is active in its harvest and the export pace has been good so far this year.

Weekly New York Arabica Coffee Futures ©Jack Scoville

Weekly London Robusta Coffee Futures ©Jack Scoville

Sugar

Futures were mixed last week with New York lower and London higher. The trade still is waiting for news of some kind to trigger a move out of trading ranges that have been mostly intact since late last year. Chart patterns on the weekly charts are sideways in New York and sideways in London. The fundamentals still suggest big supplies, and the weather in Brazil has improved to support big production ideas. Brazil weather is good in all areas as there is less rain in southern areas and more to the north.

However, UNICA reported a slow start to the harvest season in the center-south area due to a lot of rain. Brazil has been using a larger part of its Sugarcane harvest to produce ethanol this year instead of sugar, but Thailand has shown increased production this year. Ideas that production in India and Pakistan is being hurt by news that Indian mills are asking the government not to force them to sell Sugar into a depressed world market in order to try to maintain some control over operating losses. Very good conditions are reported in Thailand, but production this year could be less due to the reduced area and low prices. Demand for Sugar has been good, and the demand for ethanol is reported to be increasing.

Weekly New York World Raw Sugar Futures ©Jack Scoville

Weekly London White Sugar Futures ©Jack Scoville

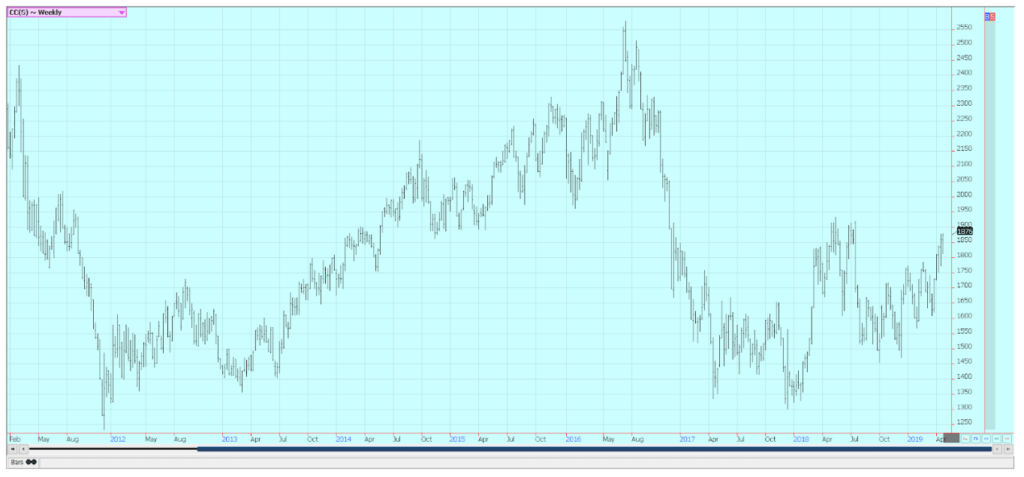

Cocoa

Futures closed lower in New York and higher in London. New York closed well off the lows in both markets and actually near the highs after testing support on the weekly charts. Trends are still up in both markets. The main crop harvest should be about over and mid-crop harvest is still a month or more away. Ivory Coast arrivals are strong as are the exports. The weekly arrivals pace is about 15 percent higher than a year ago and is holding this level.

Arrivals were reported strong in the rest of West Africa as well. Demand appears strong and the market saw stronger than expected grind data when the quarterly grind is released in the EU, North America, and Asia over the next couple of weeks. Growing conditions are generally good in West Africa. Some early week showers and cooler temperatures were beneficial, and most in West Africa expect a very good mid-crop harvest. Cameroon and Nigeria are reporting less production and prices there are reported strong. Conditions appear good in East Africa and Asia, but East Africa has been a little dry as has Malaysia.

Weekly New York Cocoa Futures ©Jack Scoville

Weekly London Cocoa Futures ©Jack Scoville

(Featured image by DepositPhotos)

—

DISCLAIMER: This article expresses my own ideas and opinions. Any information I have shared are from sources that I believe to be reliable and accurate. I did not receive any financial compensation for writing this post, nor do I own any shares in any company I’ve mentioned. I encourage any reader to do their own diligent research first before making any investment decisions.

Morocco’s Growth Holds at 4.6% as Agriculture Offsets Economic Pressures

Morocco’s economy grew 4.6% in Q1 2026, driven by a strong agricultural rebound offsetting declines in industry. Services expanded moderately...

Abivax Shares Surge as New Trial Data Eases Safety Concerns Over Ulcerative Colitis Drug

Abivax shares surged nearly 36% after positive updated trial results for its ulcerative colitis drug obefazimod reassured investors following earlier...

El Dorado Raises $9M to Expand Cross-Border Fintech Platform

El Dorado, a Latin American fintech improving cross-border financial services, raised a $9 million Series A led by Paradigm with...

Bitcoin Stalls Near $60K as Strategy Moves, ETFs Outflow, and EU MiCA Rules Take Effect

Bitcoin hovers near $60,000 with ETF outflows, while Strategy boosts reserves, sells BTC, and raises dividends to reassure investors. Ethereum...

Cannabis Dominates Global Drug Use: Trends, Risks, and Shifting Markets

Cannabis remains the world’s most widely used illicit drug, with 256 million users in 2024, surpassing all others combined. Growth...

|

|

|  |

|

|

-

Business2 weeks ago

Business2 weeks agoFed Policy Shift Raises Concerns Over Debt and Inflation Risks

-

Crypto23 hours ago

Crypto23 hours agoBitcoin Stalls Near $60K as Strategy Moves, ETFs Outflow, and EU MiCA Rules Take Effect

-

Biotech1 week ago

Biotech1 week agoGalicia Launches €805M Biotechnology Strategy to Drive Innovation and Competitiveness (2026–2030)

-

Crypto2 weeks ago

Crypto2 weeks agoBitcoin and Ethereum Markets Steady as Strategy and Bitmine Expand Holdings Amid World Cup Crypto Activity