Featured

Choosing between simple and complex personal finance apps

With different types of personal finance apps, which one should you develop in 2019?

When people hear the word “budgeting” or “personal finance management,” they don’t exactly think of it as a fun activity. But at the same time, many people also believe that tracking their personal finances helps them to stick to a budget.

Just think about it: why would there be so many personal finance apps in the market?

As it turns out, 63 percent of smartphone users have at least one financial app, according to Bankrate. This means people in today’s world are relying heavily on budget and personal finance apps to achieve their financial goals — be it saving enough to start a side-business or for retirement.

Simply put, the personal finance app development market is on fire. To thrive in the market with global competitors like Mint and Venmo, first, you need to carefully understand what a personal finance app is and what type of personal finance app you should develop to stand-out.

The following sections focus mainly on the type of personal finance apps you can build and how each of them work. This will hopefully give you the needed insight and help you choose the type of personal finance app you should develop in 2019.

Types of personal finance apps

There are mainly two types — simple and complex.

Most simple personal finance apps are usually manual entry apps in which users enter all their purchases on a day-to-day basis.

Complex personal finance apps, on the other hand, provide more features in addition to manual entry features such as linking bank accounts and credit cards that automatically log all transactions made either through net banking or using a credit card.

Now, since you’ve got the basic idea on the type of personal finance apps, let’s see how each of two really work at a deeper level.

Simple personal finance apps

The nature of simple personal finance app requires its users manually enter a lot of information, which is not exactly a huge selling point considering that many people use apps for convenience and automation.

To tackle this problem, simple personal finance apps can make their users’ life easier by adding the functionality of scanning receipts. Receipt scanning functionality is implemented using Optical Character Recognition (OCR) Technology.

Scanning receipts allows users to take pictures of their purchase bills or receipts, which then automatically gets converted into data and updated in the app.

There is a problem, though. The recognition quality of OCR libraries is still developing and the printed text quality on an average receipt is also poor. Not only that, but the size of these OCR libraries are rather large. So, if you use OCR for offline recognition, your mobile app size will become considerably large as well.

Most simple personal finance apps that apply OCR technology for providing receipt scanning generally communicate with cloud-based APIs.

Here are a few examples of simple personal finance apps:

Lemon Wallet: Acquired by Lifelock five years ago, Lemon Wallet offered receipt scanning functionality in their app. They implemented the functionality using machine learning combined with OCR technology to identify information on printed physical receipt and extracting required data like amount, date of purchase, and merchant’s name.

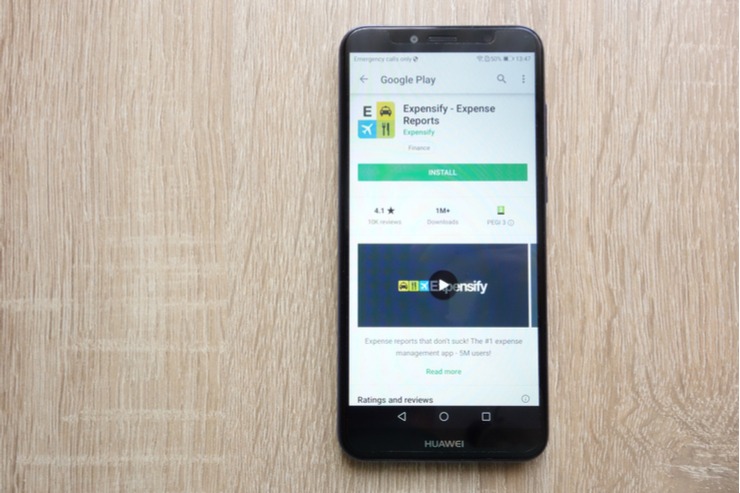

Expensify: It’s another simple personal finance app that automatically scans required information from physical receipts and stores it in an expense record. In addition, the app also offers a useful tool for capturing employees’ expenses during a business trip to make money reimbursement easier.

Complicated personal finance apps

You’re aware of the Mint personal finance mobile app, right?

The perfect personal finance mobile and web solution, Mint has been dominating the market for years. In fact, it has been recommended as the best personal finance tool by many popular platforms including The New York Times, CNET, Digital Trends, and Wired to name a few.

Now, if you want to develop a Mint-like app, you would have to give a lot of attention to security, as it requires data about the user’s income and transaction history.

You might think: security is cool but how these apps actually work?

Well, Mint and Mint-like financial apps execute account aggregation practice by employing established players like Yodlee and Intuit (owner of Mint). These systems help Mint and Mint-like apps to compile a user’s data from linked accounts such as bank savings, credit card, loans, and investments.

All of these sensitive data are then stored in the database in one place. Simply put, all of a user’s finance data is pulled from the bank account using Open Financial Exchange (OFX) — a data-stream format.

Open Financial Exchange basically helps establish a direct connection between an app and the financial institution’s — usually a bank — server using a request/response model. However, not many financial institutions have ready-to-use API for transmitting OFX data. So in this case, you’ll have to develop your own.

It’s free and open-source to build their APIs, so you’ll just need to keep in mind OFX’ specifications. However, OFX is now too old and messy, in my opinion.

Therefore, an alternative is the Open Bank Project. They claim to offer an open-source API for banks on which you can build your app or services. Check out its architecture on GitHub.

So, which type of personal finance app should you develop?

That totally depends on your business goals, your revenue strategy, and most importantly, your budget.

There’s still a lot of room for creativity and innovation in personal finance app development. If out of the two types, you’re not sure which is the way to go, get in touch with a mobile app development company that has experience in building finance apps. They’ll help you in making the right decision.

(Featured image by garagestock via Shutterstock)

—

DISCLAIMER: This article expresses my own ideas and opinions. Any information I have shared are from sources that I believe to be reliable and accurate. I did not receive any financial compensation for writing this post, nor do I own any shares in any company I’ve mentioned. I encourage any reader to do their own diligent research first before making any investment decisions.

The TopRanked.io Guide to 2026’s Biggest and Best Affiliate Opportunities

Want to earn affiliate commissions on literal billions of dollars worth of revenue? Then this week, we've got something special...

Eni Advances Energy Transition with Major Investment and Emissions Cuts

Eni showcased its “Just Transition” report in Rome, highlighting stakeholder collaboration and progress toward decarbonization goals. The company invested over...

The German Fintech Market Shows Resilience and Strong Investment Growth in 2026

Germany’s fintech sector remained resilient in 2026 despite economic crisis and rising insolvencies. Investments reached €14.2 billion, showing strong investor...

Cannabis Legalization in Germany: A Mixed Interim Assessment

Germany’s cannabis legalization has reduced criminal cases and eased pressure on the justice system, while the black market is slowly...

Sustainable Restoration of the Haus Hövener Garden in Brilon

The Brilon Construction Workers Association is restoring the Haus Hövener garden into a cultural community space, funded through a €10,000...

|

|

|  |

|

|

-

Biotech2 weeks ago

Biotech2 weeks agoMolecular Health Insolvency Leads to Restructuring Under New Company Name Lucera GmbH

-

Fintech2 days ago

Fintech2 days agoThe German Fintech Market Shows Resilience and Strong Investment Growth in 2026

-

Cannabis1 week ago

Cannabis1 week agoMedical Cannabis in England Sees Shift Toward Vaporizers and Pills Amid Rapid Market Growth

-

Africa2 weeks ago

Africa2 weeks agoBank of Africa Leads Winners at African Banker Awards