Featured

The demand on the futures markets influenced by speculative selling

Rice was a little lower on Friday and for the week on what appeared to be speculative selling tied to ideas of weaker demand. Demand has been solid for exports but less for the mills and this remains the feature of the trade. The export demand has been primarily for paddy Rice and not for milled Rice. The cash market has not felt any increased demand lately.

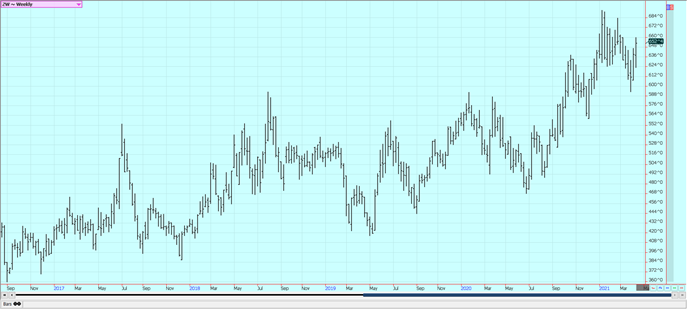

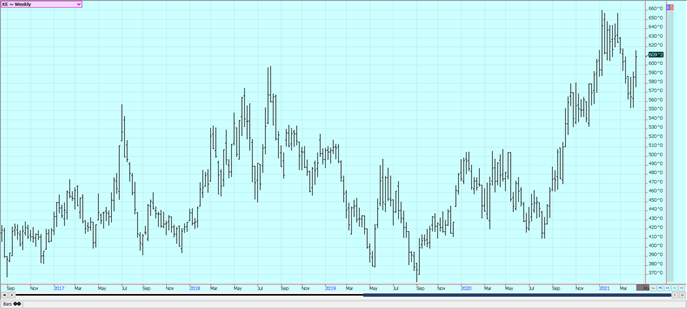

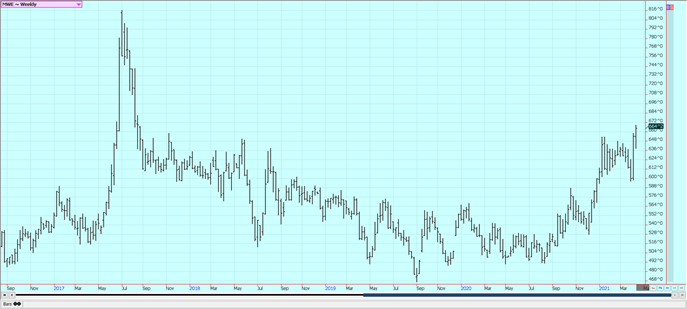

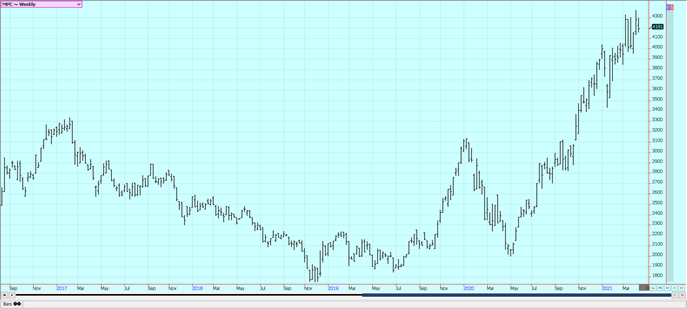

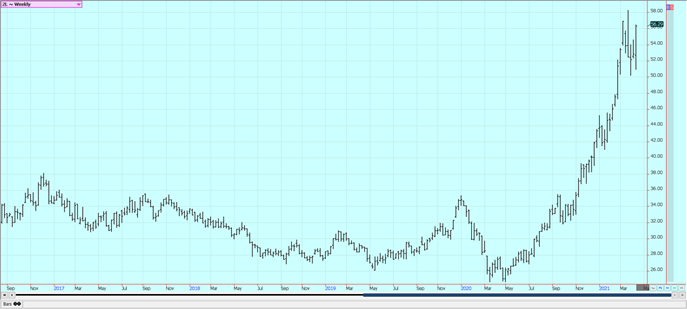

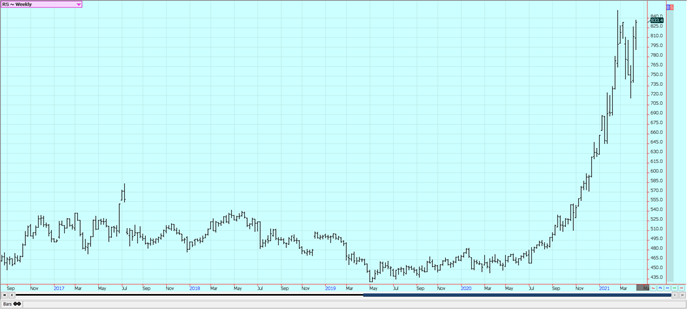

Wheat: Wheat markets were higher last week as Wheat remains a weather market. The weather remains too dry in the northern Great Plains and in the Canadian Prairies and farmers can’t plant. It has been very cold and some Winterkill was possible in the central and southern Great Plains. Any damage is expected to be light. There will be some precipitation with the colder air which should be mostly light but beneficial for the short term. Demand remains disappointing with net cancellations of export sales in the weekly report last week. The chart trends are up on the daily charts and on the weekly charts.

Weekly Chicago Soft Red Winter Wheat Futures

Weekly Chicago Hard Red Winter Wheat Futures

Weekly Minneapolis Hard Red Spring Wheat Futures

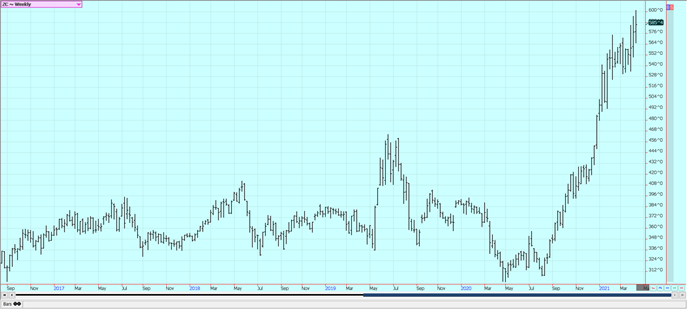

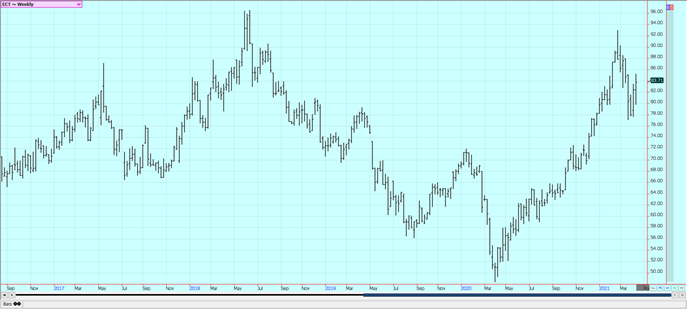

Corn: Corn closed higher on what appeared to be speculative buying based on ideas of strong demand and long-term weather outlooks for warm and dry weather west of the Mississippi River. There are also concerns about the production potential for the Safrinha crop in Brazil. Oats were higher. Chinese demand had been strong until recently and it looks like they need the Corn. Prices inside China for Corn remain extremely high. It is drier in central and parts of northern Brazil, and farmers have finally harvested the Soybeans area and planted the Winter Corn. The Winter Corn crop progress is well behind normal and it has been dry in major growing areas. Some showers are possible in southern areas this week. Showers could also fall in the north for some temporary support to Corn in both areas, but much more and more general rains are needed. Demand for US Corn has been coming at a stronger pace than estimated by USDA and it looks like US ending stocks can be significantly less than current projections by the end of the year.

Weekly Corn Futures:

Weekly Oats Futures

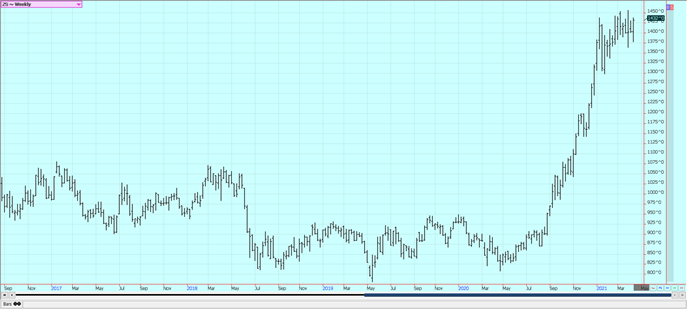

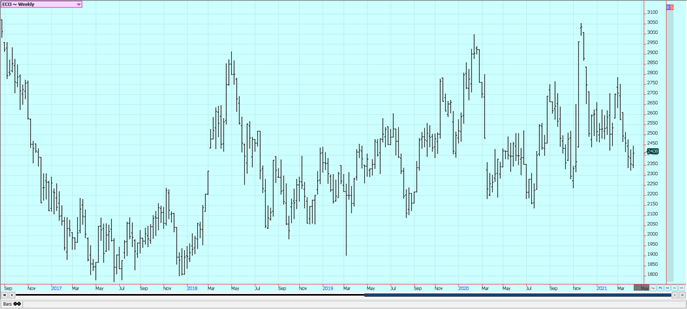

Soybeans and Soybean Meal: Soybeans were higher and Soybean Meal was about unchanged last week. Soybeans have been rallying with Corn and Soybean Oil. Also, there is still crush demand and export demand even though the demand is less now than before. The US does not have a lot of Soybeans in the country anymore as most producers have already sold. Buyers are scrambling for what is left. The Brazil harvest had been delayed due to late planting dates early due to dry weather and now too much rain that has caused harvest delays and some quality problems in the north as well. Harvest activities have increased but the harvest remains very slow overall. China has been buying for next year here but now is buying mostly in South America. US internal demand has been strong. Soybean Meal is under pressure on ideas of big production caused by the big rally in Soybean Oil. Production of DDG can increase in the near future as ethanol demand improves and more people start driving again.

Weekly Chicago Soybeans Futures:

Weekly Chicago Soybean Meal Futures

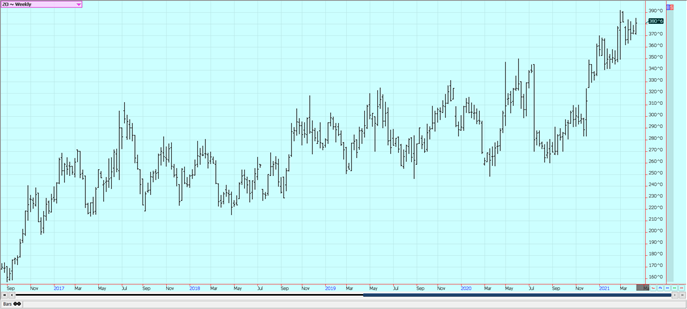

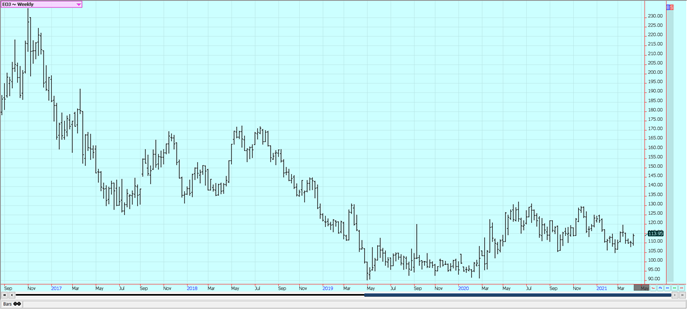

Rice: Rice was a little lower on Friday and for the week on what appeared to be speculative selling tied to ideas of weaker demand. Demand has been solid for exports but less for the mills and this remains the feature of the trade. The export demand has been primarily for paddy Rice and not for milled Rice. The cash market has not felt any increased demand lately and mill operations are reported to be on the slow side. Texas is about out of Rice, but there is Rice available in the other states, especially Arkansas. Asian and Mercosur markets were steady to lower last week. New crop Rice is getting planted in Texas and planting is more than three-quarters done in Louisiana. Mississippi and Arkansas are starting planting.

Weekly Chicago Rice Futures

Palm Oil and Vegetable Oils: World vegetable oil prices were higher last week with the most strength in Soybean Oil and Canola. Palm Oil closed lower last week on reports of good demand from the private sources for the first part of April. Ideas of tight supplies are still around but MPOB did show higher than expected ending stocks in its March data released last week. The production of Palm Oil is down in both Malaysia and Indonesia. Canola was higher on ideas of tight supplies combined with a drought in the Canadian Prairies. Soybean Oil was higher and closed at the highs of the week. Worries about South American production are supporting both markets. Demand is thought to be great with crush margins favoring a lot of production of vegetable oils to feed the demand. The demand for biofuels is about to increase and is one reason to see much stronger Soybean Oil prices.

Weekly Malaysian Palm Oil Futures:

Weekly Chicago Soybean Oil Futures

Weekly Canola Futures:

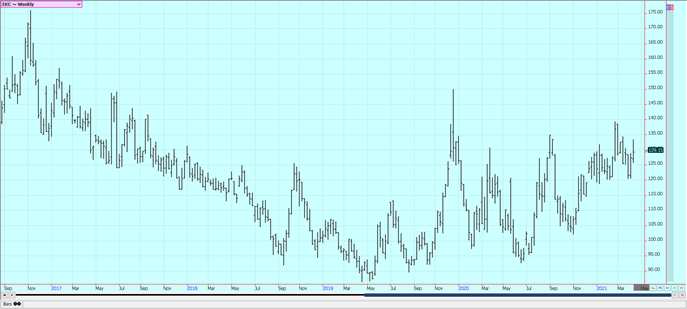

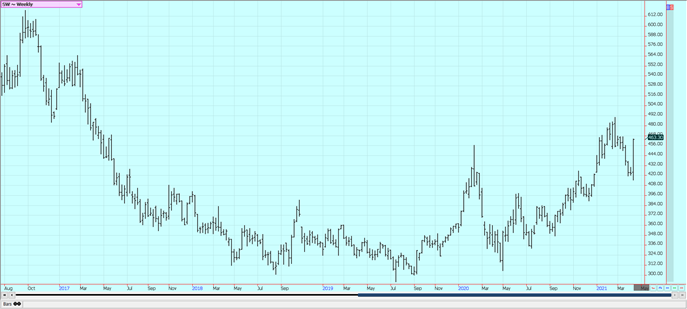

Cotton: Futures were higher for the week and trends are still up on the daily and the weekly charts. Prices were lower on Friday on what appeared to be speculative profit-taking. The demand for US Cotton in the export market has been strong even with the Coronavirus causing disruptions at the retail level around the world. The US stock market has been generally firm to help support ideas of a better economy here and potentially increased demand for Cotton products. It is dry in western and southern Texas and the planting of Cotton is being delayed. Some showers are expected in western areas in the next couple of days to help there, but it is still dry overall. It has also been cold which has hurt any early establishment of the crops.

Weekly US Cotton Futures

Frozen Concentrated Orange Juice and Citrus: FCOJ closed a little higher and continued to break out higher from recent trading ranges on the daily and weekly charts as production of Oranges has been less this year. The demand for FCOJ is said to be weaker. The weather has turned warmer so less flu is around and the increased vaccination pace means that the coronavirus is less. Moderate temperatures are expected for Florida this week. The weather in Florida is good with a few showers or dry weather to promote good tree health and fruit formation. The hurricane season is coming and a big storm could threaten trees and fruit. It is dry in Brazil and crop conditions are called good even with drier than normal soils. Stress to trees could return if the dry weather continues as is in the forecast. Mexican crop conditions in central and southern areas are called good with rains, but earlier dry weather might have hurt production. It is dry in northern and western Mexican growing areas.

Weekly FCOJ Futures

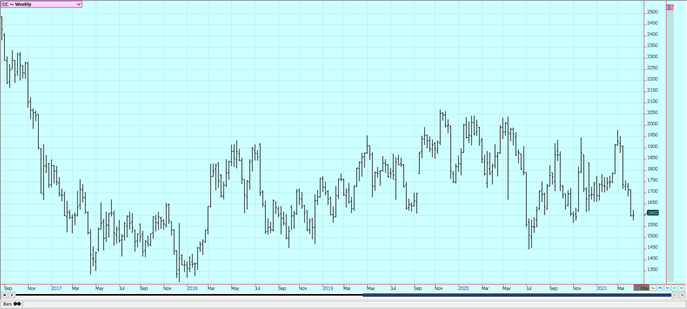

Coffee: New York closed higher last week even with a big down move on Friday and London closed a little higher. The main fundamental feature to the market is the weather in Brazil and the production prospects in the country. Some cooperatives and the export association are calling for a significant reduction in production with a 30% loss in production potential mentioned. It was dry at flowering time and has been dry again recently. It is also the off-year in the two-year production cycle. Production conditions elsewhere in Latin America are mixed with good conditions reported in northern South America and improved conditions reported in Central America after devasting floods early in the growing cycle. Conditions are reported to be generally good in Asia and Africa.

Weekly New York Arabica Coffee Futures

Weekly London Robusta Coffee Futures

Sugar: New York and London closed higher for the week with London turning higher in reversal type trading on the weekly charts. Ideas of stronger Ethanol demand helped support Sugar prices last week as the competition is back for crushing and refining use. Current Sugar demand is called average. Dry conditions were reported in Brazil. It is raining in south-central Brazil and the production of cane is looking good for the next harvest. The region has been dry overall so the rains that have fallen have been very timely. Production has been hurt due to dry weather earlier in the year. Traders are worried about a delayed Brazil harvest and lack of space at Brazil ports for Sugar shipments due to the high Soybeans shipments and delayed nature of the harvest of the Soybeans. India is exporting Sugar and is reported to have a big cane crop this year. Thailand is expecting improved production after drought-induced yield losses last year. Exports are expected by USDA to be higher in the coming year.

Weekly New York World Raw Sugar Futures

Weekly London White Sugar Futures

Cocoa: New York closed higher while London held to a sideways range last week. The main crop harvest is over in West Africa and the mid crop harvest is active. Ports in West Africa have been filled with Cocoa. That is changing a bit as the governments of Ivory Coast and Ghana have given up on their fair wage scheme to try to tax exporters and buyers. European demand has been slow as the quarterly grind data showed a 3% decrease from a year ago in grindings. This has been caused by less demand created by the pandemic. Asian demand improved as pandemic conditions there are much better than Europe. North American data could also show less grind this time, but probably for the last time as the vaccines are getting distributed and economies are starting to open.

Weekly New York Cocoa Futures

Weekly London Cocoa Futures

—

(Featured image by Quangpraha via Pixabay)

DISCLAIMER: This article was written by a third party contributor and does not reflect the opinion of Born2Invest, its management, staff or its associates. Please review our disclaimer for more information.

This article may include forward-looking statements. These forward-looking statements generally are identified by the words “believe,” “project,” “estimate,” “become,” “plan,” “will,” and similar expressions. These forward-looking statements involve known and unknown risks as well as uncertainties, including those discussed in the following cautionary statements and elsewhere in this article and on this site. Although the Company may believe that its expectations are based on reasonable assumptions, the actual results that the Company may achieve may differ materially from any forward-looking statements, which reflect the opinions of the management of the Company only as of the date hereof. Additionally, please make sure to read these important disclosures.

Futures and options trading involves substantial risk of loss and may not be suitable for everyone. The valuation of futures and options may fluctuate and as a result, clients may lose more than their original investment. In no event should the content of this website be construed as an express or implied promise, guarantee, or implication by or from The PRICE Futures Group, Inc. that you will profit or that losses can or will be limited whatsoever. Past performance is not indicative of future results. Information provided on this report is intended solely for informative purpose and is obtained from sources believed to be reliable. No guarantee of any kind is implied or possible where projections of future conditions are attempted. The leverage created by trading on margin can work against you as well as for you, and losses can exceed your entire investment. Before opening an account and trading, you should seek advice from your advisors as appropriate to ensure that you understand the risks and can withstand the losses.

Tilray Acquires HelloMD to Expand Medical Cannabis Digital Platform

Tilray Brands acquired HelloMD, a digital healthcare and medical cannabis platform, pending court approval on June 29, 2026. The deal...

Spanish Crowdfunding Market Reaches Record €761.6M in 2025, Driven by Real Estate and Crowdlending Growth

Spanish crowdfunding market reaches record €761.6M in 2025, driven by strong real estate dominance and rapid crowdlending growth, while donations...

Swedish fintech Lysa is preparing to enter the European ETF market

Swedish fintech Lysa is entering the European ETF market, registering its first ETF and expanding beyond its robo-advisor model. Managing...

Bitcoin Stalls Near $60K as Strategy Moves, ETFs Outflow, and EU MiCA Rules Take Effect

Bitcoin hovers near $60,000 with ETF outflows, while Strategy boosts reserves, sells BTC, and raises dividends to reassure investors. Ethereum...

Morocco’s Growth Holds at 4.6% as Agriculture Offsets Economic Pressures

Morocco’s economy grew 4.6% in Q1 2026, driven by a strong agricultural rebound offsetting declines in industry. Services expanded moderately...

|

|

|  |

|

|

-

Business2 weeks ago

Business2 weeks agoMarkets Diverge as Oil Falls, Rates Hold, and Inflation Persists

-

Biotech3 days ago

Biotech3 days agoAbivax Shares Surge as New Trial Data Eases Safety Concerns Over Ulcerative Colitis Drug

-

Markets1 week ago

Markets1 week agoCommodity Markets Pause as Oil Falls, Metals Correct, and Grains Show Mixed Signals

-

Fintech1 week ago

Fintech1 week agoPayPal’s Slowdown: From Fintech Leader to Low-Growth Dividend Stock